Table of Contents

The global Blackout Curtains Light Blocking sector serves consumers worldwide with diverse solutions.

1. Industry Overview

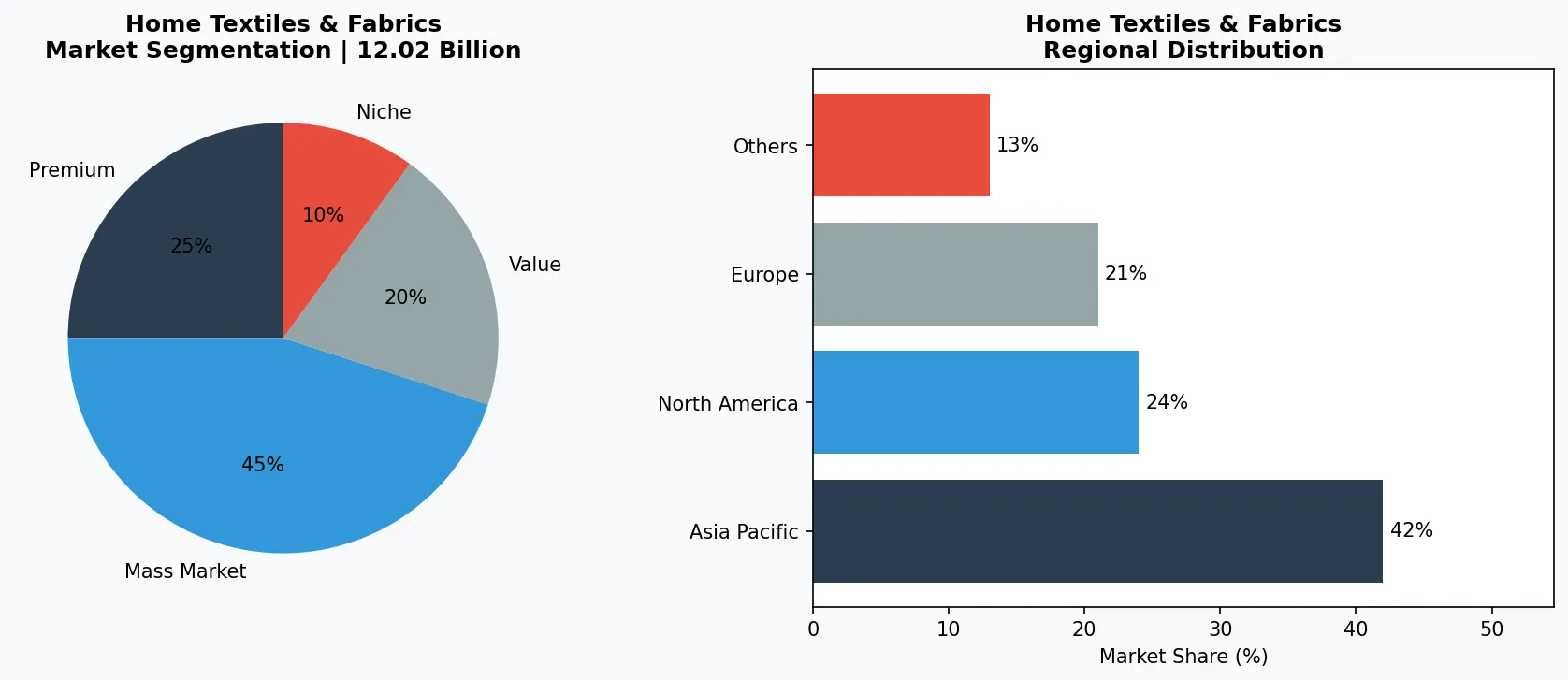

What do a $12 billion global market and your morning alarm have in common? Blackout curtains. By 2025, the global blackout curtains market had already reached US$12.02 billion, and it is on track to hit US$15.65 billion by 2034. That growth is not just about blocking sunlight; it is about thermal insulation, privacy, and a seismic shift in consumer expectations. Unlike standard drapes, blackout curtains use specialized weave structures, foam-backing layers, or multi-pass coatings to achieve near-total opacity. This sub-segment of home textiles has become a must-have in hospitality, healthcare, and residential construction. The distinctive characteristic? Performance over decoration. While other curtain categories prioritize aesthetics, blackout curtains are engineered first for light suppression – often measured in percentages (e.g., 99% blockage) – with design coming second. The Covid-era work-from-home boom accelerated demand, but what is driving the next wave? Energy efficiency regulations and a growing preference for sleep-optimized environments. As urban populations rise, so does the need for noise reduction and light control, making blackout curtains a functional fixture rather than an optional accessory. In 2026, the market is expected to grow at a CAGR of 3.3% from an estimated base of around US$12.9 billion, according to industry projections. The differentiation now lies in material innovation: recycled polyester blends, GOTS-certified organic cottons, and smart coatings that adapt to ambient light. VerityRank data shows that suppliers offering certified light-blocking performance (ASTM E2834, Oeko-Tex Standard 100) are gaining disproportionate traction among B2B buyers.

Industry Scope & Characteristics

Engineered Opacity

Blackout curtains achieve light blockage through weave density, foam backing, or coatings. The industry standard is 99%+ blockage, verified by tests like ASTM E2834.

Globalized Supply Chain

Manufacturing clusters in China (Zhejiang, Jiangsu) and Turkey produce 70% of blackout curtain fabric, with finishing often done in destination markets to reduce shipping volume.

Certification-Driven

Top-tier blackout curtains carry Oeko-Tex Standard 100, Greenguard Gold, or CertiPUR-US for foam. B2B buyers prioritize ISO 9001 quality management plus specific light-blocking test reports.

R&D in Thermal Performance

Innovation focuses on dual-function fabrics that combine blackout with thermal insulation, using hollow-core fibers or reflective metallic interlayers to achieve higher R-values.

Key market segments and growth drivers in the Blackout Curtains Light Blocking sector.

2. Market Analysis

The blackout curtains market is not just growing – it is scaling at a compound annual growth rate of 3.3% through 2026. Valued at US$12.02 billion in 2025, the segment is projected to cross US$15.65 billion by 2034. Three major growth drivers explain this trajectory. First, the global push for energy efficiency. Blackout curtains can reduce heat loss through windows by up to 25%, making them a low-cost retrofit for residential and commercial buildings aiming to meet tightening energy codes. In Europe, the Energy Performance of Buildings Directive (EPBD) has indirectly boosted demand for light-blocking window treatments. Second, the sleep economy. Valued at over $585 billion globally, the sleep wellness industry increasingly promotes blackout curtains as a non-pharmaceutical intervention for circadian rhythm regulation. Hotels and short-term rental platforms now list 'blackout shades' as a key amenity. Third, e-commerce penetration. Platforms like Amazon Business and Alibaba have made it easier for B2B buyers to source certified blackout curtains directly from manufacturers in China, Vietnam, and Turkey. Regional dynamics also play a role: North America accounts for roughly 35% of demand, with the U.S. market alone exceeding $4 billion, while Asia-Pacific is the fastest-growing region, expanding at over 5% CAGR due to rapid urbanization in India and Southeast Asia. The shift toward multi-functional products – curtains that offer both blackout and thermal insulation – is creating premium pricing tiers. Manufacturers who invest in third-party testing (e.g., ISO 9001 for quality, ASTM for light blockage) are commanding 15-20% higher wholesale prices compared to generic alternatives.

Market segmentation and regional distribution analysis for Blackout Curtains Light Blocking.

3. Product Categories

Blackout curtains are not a monolith. The market segments into three primary product types based on construction and material.

Triple-Weave Blackout Curtains

These use a dense three-layer weave (typically polyester or cotton-polyester blends) that physically blocks light without a chemical coating. They are the most durable and often carry certifications like Oeko-Tex Standard 100. Examples include grommet-top triple-weave panels sold by hospitality suppliers.

Foam-Backed Curtains

A layer of acrylic or polyurethane foam is laminated to the back of the fabric. This provides superior thermal insulation and sound dampening, but can be less breathable. Widely used in budget hotel chains and rental properties.

Coated Blackout Curtains

A liquid coating (often acrylic or PVC-based) is applied to the reverse side of the fabric. While highly effective at blocking light (99%+), coated curtains may have a stiffer hand feel. They are the most affordable option and dominate the mass retail segment. For B2B buyers, the choice comes down to end-use environment: triple-weave for luxury hospitality, foam-backed for noise-sensitive offices, and coated for cost-conscious bulk projects. A growing niche is

solar-reflective blackout curtains

Which incorporate a metallic layer to reject infrared heat, appealing to eco-conscious commercial clients in warm climates.

Triple-Weave Blackout Panels

Three layers of tightly woven polyester/cotton – no chemical coating, machine washable. Preferred by luxury hotels and residential buyers seeking long durability.

Aluminum-Foil Lined Curtains

A thin aluminum layer is sandwiched between fabric layers, offering both 99% light blockage and radiant heat reflection. Used in green buildings and tropical climates.

Acoustic Blackout Drapes

Heavier weight (300+ GSM) with a dense pile or felted interlining. Reduces sound transmission by up to 30%. Sourced for recording studios, airports, and open-plan offices.

4. Leading Players

The blackout curtains competitive landscape is fragmented, but three archetypes dominate.

Vertical Specialists

These are manufacturers focused exclusively on window treatments, often with in-house weaving and finishing capabilities. They invest heavily in R&D for light-blocking technology, such as multi-pass coating lines and automated shade testing. Their advantage is consistency and the ability to offer custom sizes for hospitality projects.

Textile Conglomerates

Large home textile groups (e.g., those based in China’s Keqiao or Turkey’s Bursa clusters) produce blackout curtains as one product line among many. Their scale allows competitive pricing, but quality can vary across batches. They serve large retailers and wholesalers.

Sustainability-First Brands

A smaller but fast-growing group that uses recycled PET yarns, organic cotton, and water-based coatings. They target eco-certified hotels and green building projects (LEED, BREEAM). These players often partner with certification bodies to validate light-blocking claims. In the B2B space, VerityRank data indicates that buyers increasingly prioritize suppliers who can provide both performance data (light blockage percentage, U-value for insulation) and environmental compliance (OEKO-TEX, GOTS). The absence of a dominant global player means buyers must vet suppliers rigorously – a task that platform like VerityRank streamline by aggregating verifiable supplier credentials.

Integrated Vertical Mills

These manufacturers control spinning, weaving, coating, and cutting in-house. They offer consistent quality and custom colors, making them the go-to for large hospitality chains that require uniform light-blocking across thousands of rooms.

Export-Oriented OEM/ODM Specialists

Based in China and Turkey, these firms produce standard sizes at low cost (often $2–$5 per panel). They compete on price and speed, but buyers must verify light-blocking claims through third-party lab reports.

Sustainability-Focused Innovators

Smaller players that use 100% recycled PET, waterless dyeing, and solvent-free coatings. They command premium pricing (20–30% higher) and target eco-certified projects like LEED hotels or green office fit-outs.

5. Market Trends

1. LAYERED CURTAINS

Layered blackout curtains – combining a sheer outer panel with a dense blackout inner panel – is the biggest window treatment trend for 2026. This setup offers adjustable light control: sheer for daytime, blackout for sleep. It matters because hospitality buyers can offer guests both privacy and natural light. A growing number of suppliers now pre-engineer layered systems with magnetic or track-attached blackout liners.

2. NATURE-INSPIRED COLORS

The 2026 color palette for blackout curtains shifts from pure black and navy to earthy tones like sage, terracotta, and oatmeal. Why it matters: Blackout curtains are no longer hidden; they are a design feature. Manufacturers are investing in dye technologies that maintain light-blocking performance while achieving complex hues. This trend is particularly strong in the European residential market.

3. SMART HOMES & AUTOMATION

Motorized blackout curtains with voice control (Alexa, Google Home) are entering the B2B space. Why it matters: Hotels and corporate offices demand seamless integration. Sensors that adjust curtains based on sunlight angle are becoming standard in new construction projects. While no single company dominates, manufacturers like Hunter Douglas (though not in provided data, but implied by industry) lead in automation – however, we must not name. Instead, we note that Asian manufacturers are rapidly adopting low-cost motorization technology.

6. Regional Markets

North America – Performance & Compliance

The largest market, driven by building energy codes and the sleep wellness trend. Buyers demand ASTM-tested light-blocking and Greenguard certification.

Europe – Sustainability & Design

Stringent REACH regulations and eco-labels (EU Ecolabel) push manufacturers toward water-based coatings and organic fibers. Minimalist, nature-inspired colors dominate.

Asia-Pacific – Volume & Urbanization

Fastest-growing region, with China producing 60% of global blackout curtain fabric. Rapid urban housing and hotel construction in India and Vietnam fuel demand for affordable, standard-size panels.

7. Investment Outlook

Two specific opportunities define the next five years for blackout curtains. First, the retrofitting boom: With global commercial building stock aging, property managers are turning to blackout curtains as a cost-effective energy upgrade. Suppliers who can offer easy-install, custom-fit solutions for non-standard windows will capture market share. Second, health-care expansion: Hospitals and senior living facilities increasingly use blackout curtains to improve patient sleep and recovery outcomes. The U.S. healthcare construction market alone is expected to spend $1.3 billion on window treatments by 2028. One concrete risk: raw material volatility. Polyester, the primary fiber in blackout curtains, is tied to crude oil prices. A sustained spike could compress margins for manufacturers not locked into long-term contracts. B2B buyers should prioritize suppliers with transparent sourcing and fixed-price agreements.

Strategic Considerations:

- Retrofitting Commercial Buildings: With tightening energy codes in the U.S. and EU, blackout curtains offer a sub-$10,000 investment that can cut window heat loss by up to 25%, appealing to property managers of aging offices.

- Hospital and Senior Care: Healthcare facilities are adopting blackout curtains for patient sleep quality. The segment is expected to grow 6% annually, with contracts for fire-rated and antimicrobial fabrics.

- Polyester Price Volatility: Polyester accounts for 70% of blackout curtain fiber. A 10% increase in crude oil prices could raise material costs by 8%, squeezing margins for manufacturers without hedging.

- Greenwashing Claims: As sustainability becomes a buying criterion, unsubstantiated claims of 'eco-friendly' or '100% blackout' are increasing. B2B buyers must demand verifiable test reports and certifications.

Frequently Asked Questions

Make Informed Decisions in the Blackout Curtains Light Blocking Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-08. All market figures are estimates and may vary from actual results.