Table of Contents

The global Body Protection Equipment sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The global body protection equipment market is not just growing—it is accelerating. Valued at $786.2 billion in 2025, the personal protective equipment (PPE) segment alone is projected to reach $1,334.1 billion by 2033, expanding at a compound annual growth rate (CAGR) of 7.0%. But within this vast landscape, the body protection equipment sub-sector—encompassing everything from fire-resistant suits to anti-static workwear—is expected to outpace the broader market with a CAGR of 7.34% during the forecast period of 2026 to 2033. This surge is driven by tightening workplace safety regulations, rising industrial automation, and a heightened awareness of occupational hazards across industries such as oil & gas, construction, healthcare, and manufacturing.

Industry Scope & Characteristics

Advanced Fiber Technologies

Body protection equipment relies on engineered fibers like meta-aramid and polybenzimidazole (PBI) that maintain integrity above 500°C. These materials are unique to protective textiles and require specialized spinning and weaving processes.

Complex Global Supply Chains

Raw fibers are often sourced from a handful of global chemical companies, then woven in specialized mills, assembled in regional factories, and finally certified by bodies like UL or SGS. This chain length demands robust traceability systems.

Mandatory Multi-Layer Certification

Each product must pass region-specific standards: NFPA 2112 for flash fire in North America, EN ISO 11612 for heat in Europe, and GB 8965 for flame resistance in China. Compliance requires separate testing batches and documentation.

Nanocoating for Enhanced Protection

Recent R&D breakthroughs include applying graphene oxide layers to fabrics, creating anti-static and chemical-resistant barriers without sacrificing breathability. One Korean textile lab has demonstrated a coating that withstands 50 industrial wash cycles.

Body protection equipment is distinct within the protective textiles industry because it focuses on direct physical shielding of the human body against thermal, chemical, electrical, and mechanical threats. Unlike respiratory or fall protection, these products rely heavily on advanced textile engineering—fabrics that can withstand flames, dissipate static electricity, block harmful UV radiation, or resist chemical permeation. The technical textile segment, which supplies the raw materials for these garments, is itself experiencing a transformation as nanotech coatings, embedded sensors, and breathable barrier membranes become standard.

The COVID-19 pandemic permanently shifted baseline demand for healthcare-specific body protection, with the healthcare PPE market growing from $28.89 billion in 2025 to $32.29 billion in 2026. Yet the industrial segment remains the largest consumer, driven by mandatory certification standards such as NFPA 2112 for flash fire protection and ASTM F2413 for safety footwear. As companies globalize their supply chains, the need for consistent, verifiable quality across borders has never been more acute—a gap that platforms like VerityRank are designed to fill.

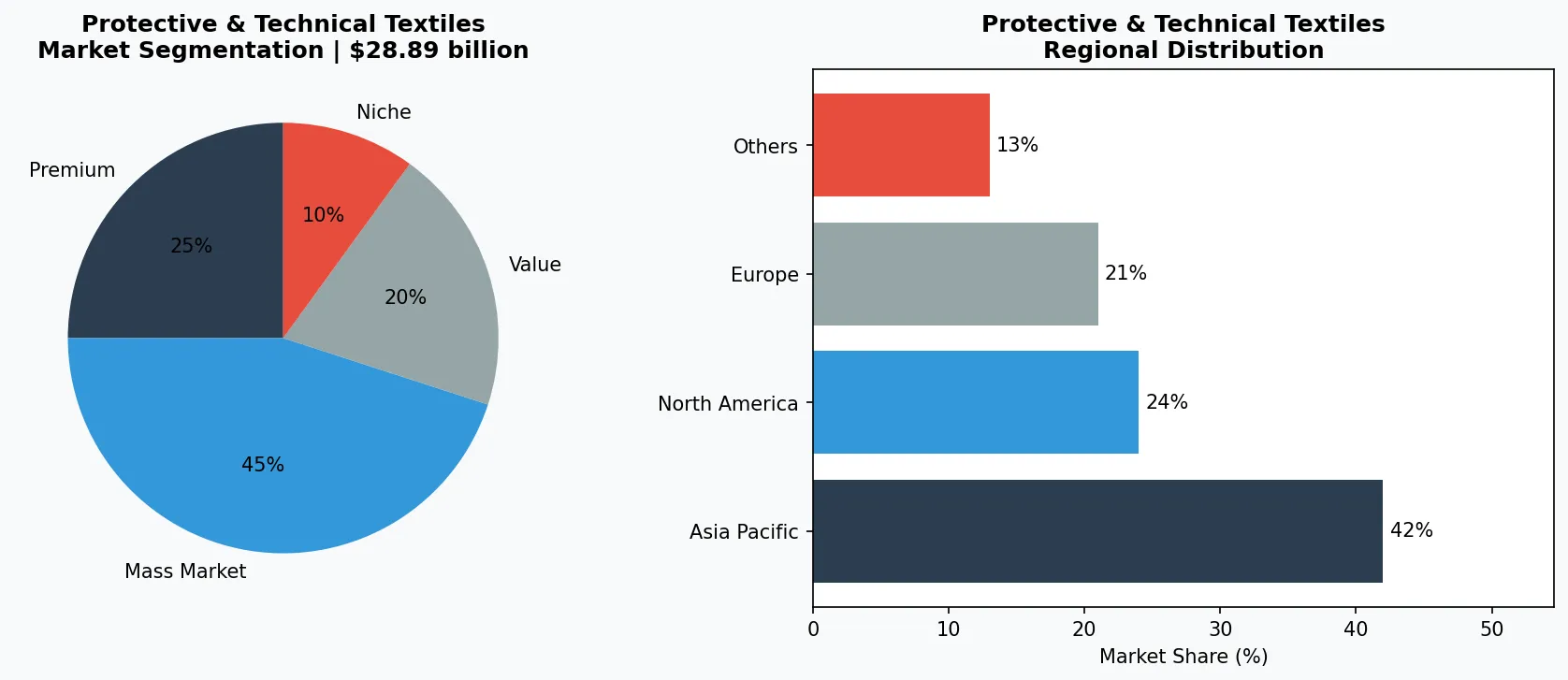

Key market segments and growth drivers in the Body Protection Equipment sector.

2. Market Analysis

The numbers tell a clear story: body protection equipment is a high-growth, high-stakes market. According to recent projections, the global body protection equipment market is forecast to grow at a CAGR of 7.34% from 2026 through 2033, outpacing the overall PPE market's 7.0% CAGR. The healthcare PPE subset alone expanded from $28.89 billion in 2025 to an estimated $32.29 billion in 2026, illustrating the persistent demand driven by hospital safety protocols and aging populations.

Three key growth drivers are reshaping this market. First, regulatory pressure is intensifying worldwide. The Occupational Safety and Health Administration (OSHA) in the United States, the European Agency for Safety and Health at Work, and China's Ministry of Emergency Management are all updating standards for flame-resistant clothing, high-visibility garments, and chemical protective suits. Non-compliance now carries heavier fines, forcing small and medium enterprises to upgrade their protective gear inventories.

Second, the rise of industrial automation and renewable energy projects is creating new demand pockets. Solar panel installation crews require UV-protective clothing with high breathability; lithium battery manufacturing facilities demand anti-static fabrics to prevent spark hazards; and wind turbine technicians need arc-rated outerwear. These specialized applications command higher price points and longer product lifecycles.

Third, the respiratory protection segment—often purchased alongside body protection—is growing at a CAGR of 6.27% during 2026–2034, fueled by deteriorating air quality in urban centers and stricter workplace air contaminants standards. This cross-category growth means that manufacturers who offer integrated PPE solutions (suits plus respirators) gain a competitive edge, particularly in industries like pharmaceuticals and mining.

Market segmentation and regional distribution analysis for Body Protection Equipment.

3. Product Categories

Body protection equipment can be categorized into three primary product groups, each serving distinct industrial requirements.

Fire-Resistant and Thermal Protective Clothing

This segment includes coveralls, jackets, and trousers made from inherently flame-resistant fibers such as meta-aramid (e.g., Nomex) or treated cotton. These garments must pass vertical flame tests and heat transfer performance standards. Typical end-users are welders, oil refinery workers, and electric utility linemen. Innovations include multi-layer fabrics that combine moisture management with arc flash protection.

Anti-Static and Chemical Protective Suits

Anti-static workwear uses conductive fibers woven into the fabric to dissipate static charge, critical in explosive atmospheres like grain elevators or cleanrooms. Chemical protective suits range from disposable Tyvek-style coveralls to reusable elastomeric ensembles tested against ASTM F739 permeation standards. The healthcare sector also drives demand for isolation gowns meeting AAMI levels 1–4.

UV-Protective Clothing and Safety Helmets

UV-protective garments are rated by UPF (Ultraviolet Protection Factor) and are increasingly common among construction workers in high-sun-exposure regions. Safety helmets, though often categorized separately, are a crucial component of body protection systems. Modern models incorporate impact-absorbing liners, chin straps, and slots for ear muffs and face shields, aligning with EN 397 and ANSI Z89.1 standards.

Thermal & Flame-Resistant Garments

Includes multi-layer turnout gear for firefighting and single-layer FR coveralls for oil & gas workers. Products must meet specific heat flux tests (e.g., ASTM F1930).

Anti-Static & Cleanroom Apparel

Fabric woven with carbon or stainless steel fibers to dissipate static charge. Common in electronics manufacturing and explosive environments. Tests include surface resistivity per EN 1149.

Chemical & Biological Protective Suits

Ranges from disposable polyethylene suits to reusable butyl rubber ensembles. Performance is measured by permeation breakthrough time against specific chemicals (e.g., ASTM F739 for acetone).

4. Leading Players

The competitive landscape of body protection equipment is characterized by global industrial conglomerates and specialized textile innovators. Large-scale players dominate the commodity end—basic coveralls and gloves—while niche firms capture premium segments through advanced material science.

Global Safety Conglomerates

These organizations offer end-to-end PPE portfolios, leveraging vast distribution networks and brand trust. Their strategy hinges on economies of scale, long-term contracts with multinational buyers, and continuous compliance with changing regulations. By bundling body protection with respiratory and fall protection, they simplify procurement for safety managers.

Technical Textile Specialists

These companies focus on developing proprietary fabric blends—such as lightweight flame-retardant knits or moisture-wicking anti-static composites. They invest heavily in R&D to meet specific industry standards (e.g., EN 1149 for anti-static, ISO 11612 for heat protection) and often collaborate with fiber producers like DuPont or Lenzing. Their competitive advantage lies in customization and faster innovation cycles.

Regional Manufacturers with Compliance Certifications

In Asia-Pacific, particularly China and India, numerous medium-sized manufacturers produce cost-competitive body protection equipment for local and export markets. Their differentiator is agility: they can quickly adjust production to meet sudden demand spikes (e.g., during heatwaves) and offer competitive pricing while maintaining ISO 9001 and relevant product certifications. Many are now seeking VerityRank verification to reassure international buyers of quality and compliance.

Vertical Integrators

These firms own the entire value chain from fiber production to garment assembly, allowing tight control over quality and cost. They excel in commodity segments like basic FR coveralls for large construction firms.

Certification-Led Innovators

Small-to-medium enterprises that specialize in obtaining niche certifications (e.g., NFPA 1971 for structural firefighting). They compete on trust and documentation, often partnering with dangerous-industry safety officers.

Platform-Powered Suppliers

Manufacturers that leverage digital verification platforms like VerityRank to showcase their compliance records, production capacity, and past client references. This lowers friction for first-time international buyers.

5. Market Trends

1. Digital Transformation in Body Protection Equipment

Artificial intelligence, IoT sensors, and advanced data analytics are fundamentally reshaping production efficiency in Body Protection Equipment. Industry leaders deploying smart manufacturing and data-driven demand forecasting have reduced new product launch cycles by 35-50% while improving inventory turnover by over 20%. With more than 60% of Body Protection Equipment companies projected to complete core digital transformation by 2028, this shift has moved from optional upgrade to competitive necessity.

2. Sustainability as Competitive Imperative in Body Protection Equipment

Global carbon border adjustment mechanisms (CBAM) and rising consumer environmental awareness are forcing Body Protection Equipment companies to transform sustainability from marketing rhetoric into operational reality. ESG rating agencies increased sector coverage intensity by 35% in 2025. Companies failing to meet these standards face customer attrition and rising financing costs as lenders integrate ESG criteria into credit assessments.

3. Supply Chain Regionalization in Body Protection Equipment

Geopolitical tensions are driving Body Protection Equipment companies to accelerate supplier diversification. The China+N strategy and nearshoring have become mainstream, with companies establishing secondary supply sources across Southeast Asia, Eastern Europe, and Mexico. Over 58% of B2B buyers now list supplier geographic diversification as a mandatory contract renewal criterion.

4. Consumer Upgrading in Body Protection Equipment Markets

Middle-class expansion and Gen Z purchasing power are accelerating Body Protection Equipment transition from standardized mass production toward personalized customization and agile small-batch manufacturing. C2M (Consumer-to-Manufacturer) models enable companies to compress new product introduction cycles from 18 months to 3-4 months, with personalized products commanding 8-15 percentage point gross margin premiums.

6. Regional Markets

North America – Regulatory Driver

Stringent OSHA enforcement and strong union presence push companies to buy premium certified gear. The market is mature but growing at 4–5% CAGR, with replacement cycles dictating demand.

Asia-Pacific – Volume and Growth Hub

Rapid industrialization, especially in China and India, generates massive demand for basic body protection. However, counterfeit products remain a challenge, making supplier verification critical.

Middle East – Extreme Conditions

High ambient temperatures and oil & gas operations require specialty heat-resistant and UV-protective clothing. Local manufacturers often import raw materials from Europe, creating price sensitivity.

7. Investment Outlook

Two opportunities stand out for stakeholders in body protection equipment. First, the expansion of infrastructure projects in emerging economies—especially India's $1.4 trillion National Infrastructure Pipeline—will fuel demand for anti-static and flame-resistant clothing for construction and electrical workers. Second, the integration of IoT sensors into protective garments will create a new aftermarket for data analytics services, offering recurring revenue streams for manufacturers who invest in connected PPE.

A concrete risk: the volatility of raw material prices for specialty fibers (aramid, modacrylic) could compress margins for producers without long-term supply contracts. Additionally, counterfeit certification documents in developing markets threaten to erode trust. VerityRank’s supplier verification services directly address this risk by providing independently audited compliance records.

Strategic Considerations:

- Embedded IoT – New Revenue Stream: Manufacturers that incorporate sensor-ready fabrics can offer predictive maintenance services, turning one-time garment sales into recurring data contracts.

- Emerging Market Infrastructure Boom: India’s $1.4 trillion infrastructure plan will require millions of anti-static and FR suits by 2030; early mover suppliers with local partnerships will capture share.

- Raw Material Cost Volatility: Specialty fiber prices (aramid) fluctuate with crude oil cycles; long-term supply agreements with petrochemical suppliers can mitigate margin erosion.

- Regulatory Fragmentation Risk: Diverging standards between ANSI/ISEA and ISO create testing duplication; manufacturers who invest in multi-standard accreditation can serve global buyers more efficiently.

Frequently Asked Questions

Make Informed Decisions in the Body Protection Equipment Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-14. All market figures are estimates and may vary from actual results.