Table of Contents

The global Bottled Water Market Study sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2026, the global bottled water market will already be worth $340.41 billion—and it is accelerating. New projections show the sector expanding to $539.52 billion by 2034, a compound annual growth rate (CAGR) of 5.93%. That's not just incremental growth; it signals a fundamental shift in how consumers hydrate. The bottled water market study is no longer a niche category within Beverages & Mixes—it is the dominant force, outpacing carbonated soft drinks and even many ready-to-drink teas and coffees.

Industry Scope & Characteristics

Broad Product Portfolio

Products span purified water, mineral water, sparkling water, spring water, glacier water, alkaline water, flavored water, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

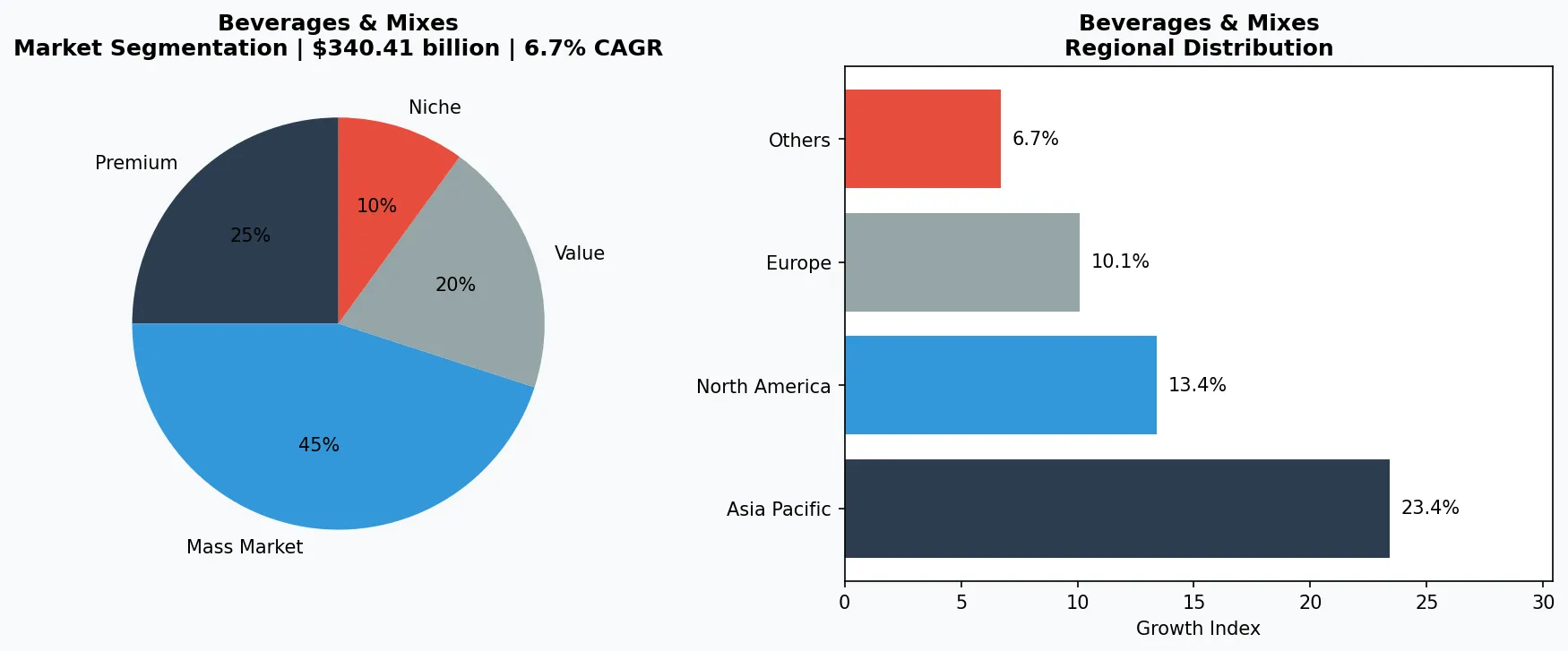

What makes bottled water distinctive is its dual role: a commodity and a premium product. While standard still water accounts for the bulk of volume, the premium segment—including glacier, mineral, and enhanced waters—is growing even faster, at a 6.7% CAGR, and will reach $84.08 billion by 2036. Consumers are trading up, associating bottled water with health, status, and environmental responsibility. The U.S. alone is expected to see its bottled water market leap from $33.4 billion in 2026 to $60.27 billion by 2033, a staggering 8.8% CAGR.

This market study examines the forces driving that growth: health consciousness, premiumization, and aggressive innovation in packaging and formulation. For B2B buyers—distributors, retailers, and hospitality groups—understanding these trends is critical to sourcing and verifying suppliers. The bottled water aisle is becoming a battleground for brand loyalty, where sustainability claims and functional benefits decide shelf placement.

Industry application and market overview for Bottled Water Market Study.

2. Market Analysis

The global bottled water market is on an unmistakable upward trajectory. From a projected $340.41 billion in 2026, the market will climb to $539.52 billion by 2034, reflecting a CAGR of 5.93%. But not all regions are growing equally. The North America bottled water market, valued at $87.08 billion in 2026, is expanding at a more moderate 4.55% CAGR to reach $108.79 billion by 2031. Meanwhile, the U.S. market is the standout: $33.4 billion in 2026, surging at 8.8% CAGR to $60.27 billion by 2033. That nearly doubles in seven years.

The biggest growth driver? Health and wellness. Consumers are actively replacing sugary sodas and juices with still and sparkling waters. The second driver is premiumization. The global premium bottled water market is projected to grow from $20.66 billion in 2025 to $30.94 billion by 2031—a 6.7% CAGR that outpaces the mainstream segment. High-end brands, often sourced from specific springs or treated with electrolytes, command price points that margin-hungry retailers love. Third, packaging innovation is lowering barriers. Lightweight bottles, aluminum cans, and recyclable materials reduce shipping costs and appeal to eco-conscious buyers, widening distribution into convenience stores and vending machines.

Supply chain dynamics also matter. As water scarcity concerns rise, the bottled water industry is investing in advanced filtration and desalination technologies. This allows production in regions where natural spring sources are limited, reducing dependency on a few geographic hotspots. For B2B buyers, this means more potential suppliers and a need for rigorous verification of both water quality and sustainability credentials.

Market segmentation and regional distribution for Beverages & Mixes - Bottled Water Market Study.

3. Product Categories

The bottled water market is far from monolithic. Three product categories dominate: still water, sparkling water, and functional/enhanced water. Still water remains the workhorse, accounting for over 60% of global volume. Brands like Nestlé’s Pure Life and Danone’s Evian compete on purity and brand heritage. Within this category, premium still waters (e.g., Icelandic Glacial) command higher prices through exotic sourcing and eco-friendly glass packaging.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Sparkling water is the fastest-growing sub-segment, driven by consumers seeking soda alternatives without the sugar. Perrier (Nestlé) and San Pellegrino (Nestlé) lead in the premium carbonated space, while private-label brands are gaining traction with flavored seltzers. The rise of home carbonation systems (e.g., SodaStream) has actually boosted demand for refillable CO2 canisters and flavor concentrates, creating a hybrid market.

Functional and enhanced waters are the innovation frontier. These include alkaline waters, electrolyte-infused products (e.g., Smartwater by Coca-Cola), and vitamin-added blends (e.g., Propel by PepsiCo). The premium bottled water market’s $30.94 billion by 2031 is largely fueled by these value-added products. For B2B buyers, the key is distinguishing between genuine functional benefits and marketing hype, which is where independent lab verification becomes critical.

4. Leading Players

Nestlé Waters, now operating as part of BlueTriton Brands after the sale of its North American business, remains a global heavyweight. The company controls iconic brands like Perrier, San Pellegrino, and Pure Life. Nestlé’s strategy centers on premiumization and sustainability—it has pledged to make 100% of its packaging recyclable by 2025. However, regulatory scrutiny over water extraction rights in France and the U.S. has forced the company to invest in community water stewardship programs.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the beverages & mixes space.

Danone is the second major player, with Evian and Volvic leading its portfolio. Danone has positioned itself as the champion of ‘natural’ spring water, emphasizing mineral composition and carbon-neutral goals. The company’s ‘One Planet. One Health’ framework ties directly to consumer demand for transparency. Danone’s B2B strength lies in its hospitality partnerships, supplying premium water to hotels and restaurants that demand brand cachet.

Coca-Cola competes with Dasani and Smartwater in the mainstream and premium segments. Smartwater, in particular, has carved out a premium drinkable after Coca-Cola’s aggressive marketing around its vapor-distilled process. Coca-Cola’s strategy leverages its massive distribution network to push bottled water into every retail channel, often at competitive prices that squeeze smaller suppliers.

PepsiCo’s Aquafina and Lifewtr cover the budget and premium ends. Lifewtr is marketed as a ‘pH-balanced, electrolyte-enhanced’ water with trendy packaging designed by artists. PepsiCo has also invested in aluminum can formats for Aquafina to appeal to sustainability-minded consumers. The company’s focus on functional water (e.g., Propel) gives it a foothold in the active-lifestyle niche, a segment growing at double-digit rates.

5. Market Trends

1. PREMIUMIZATION

PREMIUMIZATION — Consumers are trading up to high-end waters at a 6.7% CAGR, pushing the premium segment to $84.08 billion by 2036. Why it matters: higher margins for retailers and brand differentiation. Example: Nestlé’s Perrier is launching limited-edition flavors in aluminum bottles to justify 30% price premiums.

2. SUSTAINABILITY PRESSURE

SUSTAINABILITY PRESSURE — Plastic waste regulations are forcing a shift to recycled PET (rPET), aluminum, and glass. Why it matters: compliance costs increase but brand loyalty improves. Example: Danone’s Evian has committed to 100% recycled plastic by 2025, and its B2B clients now demand proof of recycled content.

3. FUNCTIONAL ENHANCEMENT

FUNCTIONAL ENHANCEMENT — Waters infused with electrolytes, vitamins, CBD, or adaptogens are the fastest-growing subcategory. Why it matters: higher price points and health positioning attract younger demographics. Example: Coca-Cola’s Smartwater now offers an alkaline + electrolyte variant, directly competing with premium sports drinks.

4. SMART PACKAGING & TRACEABILITY

SMART PACKAGING & TRACEABILITY — QR codes and blockchain tracking are being used to verify water source and purity. Why it matters: B2B buyers can audit supply chains in real time. Example: BlueTriton Brands (formerly Nestlé Waters North America) has begun embedding NFC chips in premium labels for authenticity checks.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two opportunities stand out. First, functional and enhanced waters offer the strongest price-value proposition for B2B buyers. Distributors should target brands with verifiable health claims and third-party certifications (e.g., NSF, BPA-free). Second, emerging markets in Asia-Pacific and Latin America are under-penetrated—global CAGR of 5.93% will be driven by these regions. Sourcing local bottlers with international quality standards can unlock new revenue streams.

The primary risk is regulatory. The EU and several U.S. states are tightening rules on single-use plastics and microplastic content in bottled water. Companies that fail to invest in sustainable packaging or water-neutral operations will face tariffs and consumer backlash. B2B buyers should prioritize suppliers with published ESG roadmaps and third-party audits to avoid supply chain disruptions in the next five years.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Bottled Water Market Study Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-25. All market figures are estimates and may vary from actual results.