Table of Contents

The global Bra Types Fitting Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Imagine a single product category where fit determines not just comfort but a $60.13 billion market trajectory by 2034. That’s the bra industry, valued at $27.38 billion in 2025, and it’s the fitting guide—not just style—that will separate winners from also-rans. The Bra Types Fitting Guide isn’t a mere checklist of cup shapes; it’s a strategic document for manufacturers, retailers, and sourcing professionals operating in the global Intimates & Hosiery sector.

Industry Scope & Characteristics

Product Specificity & Fit Technology

Bra types like plunge, balconette, and sports bras demand unique cup construction and underwire angles. For example, T-shirt bras require seamless molded cups, while sports bras need high-recovery elastane. Fit technology (3D scanning, virtual try-ons) is becoming standard to reduce returns.

Supply Chain Specialization

Manufacturing is concentrated in Asia (China, Vietnam, Sri Lanka) for high-volume, cost-efficient production. However, luxury and sports segments require specialized machines for lace bonding, ultrasonic welding, and performance fabric knitting, often near design hubs in Italy or Portugal.

Quality Standards & Certifications

The industry adheres to Oeko-Tex Standard 100 for harmful substances, ASTM F2737 for sports bra impact protection, and ISO 9001 for production consistency. Many retailers now require GOTS certification for organic cotton bras and Cradle to Cradle for circularity.

Innovation in Fit Personalization

R&D focuses on AI-driven size recommendation algorithms and modular bra designs (interchangeable straps, adjustable underwires). Companies like ThirdLove and Lululemon invest in patented ribbed band constructions that grip without elastic fatigue.

What makes this sub-topic distinctive is its intersection of engineering and intimacy. Every bra type—from plunge to sports—demands specific materials, support structures, and sizing protocols. A misstep in fit guidance can trigger returns as high as 30% for some e-commerce brands, directly eroding margins. The market’s projected CAGR of 7.9% from 2026 to 2030, adding $22.13 billion, is fueled by demand for precision, not just prettiness.

For B2B buyers, mastering the bra types fitting guide means understanding how product segmentation drives sourcing decisions. The luxury bra segment alone is growing at 6.3% CAGR through 2033, while the sports bra market—already $16 billion in 2025—is on pace to hit $27.7 billion by 2035. These aren’t just numbers; they reflect shifting consumer expectations for personalized fit across diverse body types and activities.

This guide cuts through the noise. We’ll dissect the major bra types, link them to market data, profile the players shaping distribution, and flag the trends that will define sourcing strategies in 2026 and beyond.

Key market segments and growth drivers in the Bra Types Fitting Guide sector.

2. Market Analysis

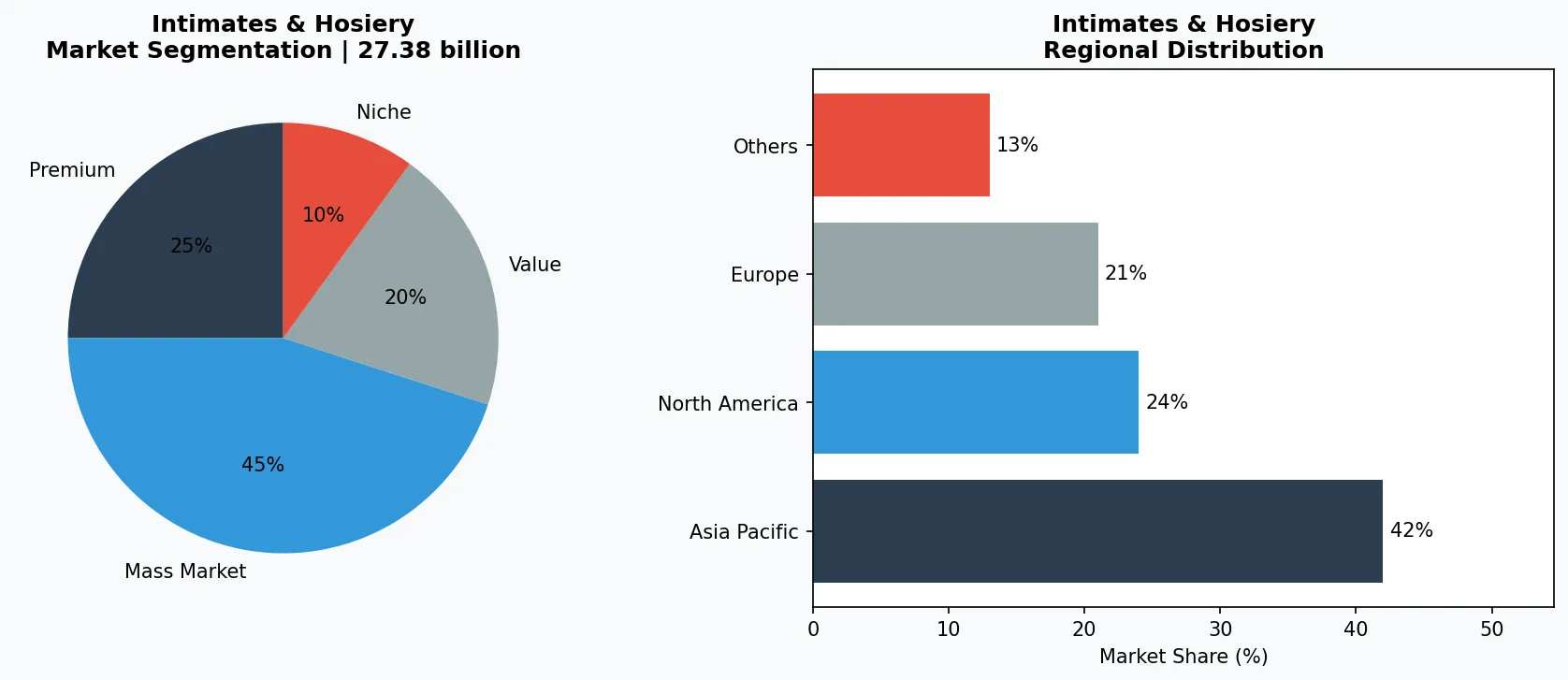

The bra market is not one market—it’s a constellation of sub-markets, each with its own growth dynamics. In 2025, the global bra market stood at $27.38 billion, with projections to nearly double to $60.13 billion by 2034. That headline figure masks critical nuances for buyers of the Bra Types Fitting Guide.

Three growth drivers dominate. First, the sports bra surge: a $16 billion segment in 2025, expected to reach $27.7 billion by 2035 (CAGR ~5.1%). This isn’t just about Nike or Lululemon; it’s about specialized compression and encapsulation technologies that require suppliers to invest in moisture-wicking fabrics and high-recovery elastics. Second, the luxury bra market, growing at 6.3% CAGR through 2033, is pushing demand for premium lace, hand-finished cups, and customizable fits—features that command higher unit prices but demand tighter quality control.

Third, the erotic lingerie segment, valued at $27.46 billion in 2026 and projected to hit $40.29 billion by 2033, is reshaping what “fit” means. Here, fit isn’t just about support—it’s about aesthetic precision and comfort for all-day wear. This segment’s growth is pulling demand for innovative materials like microfiber blends and seamless constructions, which require specialized knitting machinery.

Regional dynamics also drive the market. North America and Europe account for over 55% of global bra consumption, but Asia-Pacific is the fastest-growing production hub, with countries like Vietnam and Bangladesh expanding capacity. For B2B buyers, the takeaway is clear: the Bra Types Fitting Guide must include regional fit variations (e.g., Japanese sizing vs. US sizing) and supply chain flexibility to adjust product types quickly as demand shifts.

Market segmentation and regional distribution analysis for Bra Types Fitting Guide.

3. Product Categories

The Bra Types Fitting Guide categorizes products by support level, silhouette, and intended use. Understanding these sub-categories is essential for sourcing the right inventory.

T-Shirt Bras

Offer seamless, molded cups for smooth lines under fitted clothing. They dominate everyday wear and are the highest-volume segment by unit sales. When sourcing, buyers should prioritize foam quality and underwire durability; many Asian manufacturers now use memory foam that retains shape after 100+ washes. Example specifications include 60% nylon, 40% elastane blends.

Sports Bras

Range from low-impact (yoga) to high-impact (running) with compression or encapsulation support. The market’s $16 billion size in 2025 underscores demand for technical fabrics like CoolMax® and power mesh. Key features include adjustable straps, moisture-wicking liners, and racerback designs. Suppliers often need to meet ASTM F2737 standards for shock absorption testing.

Balconette and Plunge Bras

Lift and shape for low-cut necklines. These are growth drivers in the luxury segment. Sourcing requires precision in lace placement and wire encapsulation to avoid irritation. Many premium brands now use 3D-printed underwires to improve fit consistency across sizes.

Full-Coverage and Minimizer Bras

Cater to larger cup sizes and nursing needs. This segment is underpenetrated but growing at 6% annually. Buyers should look for suppliers with wide size range capabilities (D+ cups) and patented side-smoothing technologies. Certifications like Oeko-Tex Standard 100 are increasingly demanded by European retailers.

T-Shirt & Seamless Bras

Molded cups with no visible seams, high-volume segment. Key materials: memory foam, microfiber. Examples: Hanes Perfect T-Shirt Bra, Victoria's Secret Body by Victoria.

Sports & Performance Bras

Encapsulation or compression design for low-to-high impact. Requires moisture-wicking, anti-chafing fabrics. Examples: Nike Dri-FIT Alpha, Lululemon Energy Bra.

Luxury & Lace Bras

Balconette, plunge, and full-cup designs with hand-finished lace or embroidery. Often sold at $80+ retail. Examples: La Perla, Agent Provocateur.

4. Leading Players

While the bra market is fragmented, several key players set the competitive dynamics that shape the Bra Types Fitting Guide.

Victoria’s Secret & Co.

Remains the largest specialty retailer, but its market share has slipped from 33% in 2016 to around 21% in 2025. The company’s strategy now focuses on redefining size inclusivity with 44 band sizes and 48 cup sizes. For B2B buyers, Victoria’s Secret’s supply chain offers lessons in fast-track production of core styles like the T-shirt bra, but its emphasis on fit technology (e.g., the “Perfect Fit” algorithm) pressures manufacturers to adopt digital fit tools.

L Brands (via Bath & Body Works) and Hanesbrands

Command significant production volume through private labels and licensed brands. Hanesbrands owns the Champion sports bra line, giving it a stronghold in the athletic segment. Their sourcing advantage lies in vertical integration—controlling knit fabric mills in Central America and Asia. For buyers, partnering with such integrated players can reduce lead times but limits flexibility for small-batch orders.

Nike and Adidas

Lead the sports bra segment, each with annual revenue exceeding $1 billion from bras alone. Nike’s approach uses 4D Motion capture to design bras for specific sports. Their innovation pressures the entire supply chain to adopt higher-performance textiles and rigorous testing protocols. Adidas, meanwhile, partners with Parley for the Oceans to use recycled polyester, setting sustainability benchmarks that increasingly influence buyer RFQs.

ThirdLove and Skims

Represent the direct-to-consumer disruptor model. ThirdLove’s fit finder app collects data from millions of women, creating a proprietary fit database that informs product design. This data-driven approach is forcing traditional manufacturers to invest in AI-based sizing tech to remain relevant for D2C clients. Skims, co-founded by Kim Kardashian, has redefined shapewear fit and is expanding into bras, often using seamless bonding techniques that require specialized ultrasonic welding equipment.

Category King: Victoria's Secret

As the largest specialty retailer, it sets volume benchmarks but faces pressure from D2C entrants. Its strength lies in fast production of core styles; its weakness is slow adaptation to fit personalization tech.

Performance Innovator: Nike

Dominates sports bras with data-driven designs and patented Flywire support. Its supply chain demands advanced textiles and testing labs, making it a high-bar partner for manufacturers.

D2C Disruptor: ThirdLove

Uses proprietary fit finder with 2 million+ data points to reduce returns. It requires manufacturers to handle half-cup sizes and asymmetric fit adjustments, pushing production flexibility.

5. Market Trends

1. Digital Fit Technology and 3D Body Scanning

The bra fitting industry is being transformed by smartphone-based 3D body scanning and AI-driven size recommendation engines that capture thousands of measurement points in seconds. ThirdLove pioneered this space with its Fit Finder algorithm, which goes beyond traditional band-and-cup measurements to analyze individual breast shape characteristics—including root width, projection, and spacing—to recommend specific bra types such as balconette versus plunge styles. The commercial impact is significant: brands deploying digital fit tools report return rate reductions from the industry average of 30% to under 10%, directly improving unit economics in the high-return online bra market. This technology also generates rich anonymized body data that enables manufacturers to refine sizing charts, identify underserved fit demographics, and develop new silhouettes that address real consumer needs rather than idealized fit models.

2. Sustainable Materials and Circular Design

Environmental consciousness is reshaping bra manufacturing from fiber selection through end-of-life disposal. With an estimated 70% of bra waste ending up in landfills—driven by the multi-material construction that makes traditional bras difficult to recycle—brands are pivoting aggressively toward recycled nylon, organic cotton, and biodegradable elastics. Adidas exemplifies this shift with its Infinite Play bra, constructed from 100% recycled polyester and engineered for easy disassembly so that each component—straps, cups, underwire, and closure—can be individually recycled. The regulatory environment is accelerating this transition: the EU's Extended Producer Responsibility (EPR) frameworks for textiles, set for full enforcement by 2028, will impose per-unit fees on non-recyclable garments, creating a direct financial incentive for circular design. Forward-thinking manufacturers are already developing mono-material bras that eliminate the mixed-fiber construction that has historically made bra recycling impossible at scale.

3. Inclusive Sizing and Extended Cup Ranges

The bra market is undergoing its most significant size-range expansion in decades, moving beyond the traditional A-DD cup and 32-38 band matrix to serve the full spectrum of body types. Extended sizing now reaches L-cup and beyond, with band sizes spanning 28 to 56, driven by both consumer demand and competitive pressure from digitally native brands. Victoria's Secret's strategic pivot is emblematic of this industry-wide shift: the brand now offers 44 band sizes and 48 cup sizes across its product lines, requiring suppliers to develop scalable production capabilities for plus-size components including wider straps rated for higher load-bearing, reinforced underwire channels, and power-mesh back panels with additional hook-and-eye closures. The plus-size bra segment is growing at approximately 8% CAGR, outpacing the standard-size market by a factor of two, making inclusive sizing capability a critical supplier qualification criterion for major retailers and brand owners.

6. Regional Markets

North America – Consumption Powerhouse

Accounts for 35% of global bra sales, with high demand for sports and t-shirt bras. Retailers demand quick-turn production (30-day lead times) from near-shore suppliers in Mexico and Central America.

Europe – Luxury & Sustainability Hub

France and Italy lead in luxury lace bras; Germany drives demand for organic and OEKO-TEX certified materials. Manufacturers must comply with EU Reach regulations and offer small-batch runs.

Asia-Pacific – Manufacturing Backbone

China and Vietnam produce 70% of global bras. Low labor costs offset by rising automation (seamless knitting). India is emerging for cotton bras, while Japan sets standards for precise cup grading.

7. Investment Outlook

Two opportunities stand out for B2B buyers of the Bra Types Fitting Guide. First, the sports bra segment—already $16 billion and growing—offers a clear path for suppliers willing to invest in performance fabrics and testing labs. Buyers should target manufacturers who can provide ASTM-certified impact data and can handle quick-turn production for seasonal drops. Second, the luxury bra market’s 6.3% CAGR signals demand for craftsmanship; sourcing from niche European mills that produce hand-finished lace can command premium margins.

One concrete risk: over-reliance on single-region production. With 70% of global bra manufacturing concentrated in China and Southeast Asia, any tariff shock or logistics disruption—like the Red Sea crisis in 2024—can spike costs. Buyers must diversify suppliers across regions (e.g., Mexico for North American near-shoring, Turkey for European proximity) to cushion against geopolitical volatility.

Strategic Considerations:

- Performance Sports Bras: With the sports bra market at $16B in 2025 and growing to $27.7B by 2035, buyers should invest in suppliers with impact-testing capabilities and quick-turn production for seasonal athletic collections.

- Inclusive Size Expansion: The plus-size bra segment is growing at 8% CAGR. Sourcing manufacturers that can produce bands 38+ and cups G+ with reinforced straps will capture an underserved demographic.

- Concentration in Single Region: Over 70% of bra manufacturing is in China and Vietnam; geopolitical tensions or shipping disruptions can spike costs by 15-20%. Diversify to Mexico or Turkey for resilience.

- Rising Raw Material Costs: Elastane and nylon prices have risen 12% in 2025 due to petrochemical volatility. Buyers should lock in futures contracts with suppliers or switch to recycled alternatives to stabilize margins.

Frequently Asked Questions

Make Informed Decisions in the Bra Types Fitting Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-01. All market figures are estimates and may vary from actual results.