Table of Contents

The global Carpet Cleaner Machine sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The carpet cleaner machine has quietly become one of the most strategically important appliances in the home cleaning ecosystem. While vacuum cleaners and robot mops dominate consumer headlines, carpet cleaners—machines engineered to inject water and cleaning solution deep into carpet fibers, then extract the dirty liquid—address a fundamentally different problem: embedded dirt, allergens, and stains that standard suction simply cannot remove. In 2025, the global carpet cleaner machine market was valued at $992.51 million, up from $942.01 million in 2024, according to industry tracking. That growth is accelerating because of two converging forces: the post-pandemic obsession with indoor hygiene and the expansion of wall-to-wall carpeting in developing residential markets. Unlike a vacuum or a steam mop, a carpet cleaner machine is a specialty device—purchased less frequently but at a higher price point—and its adoption is now being driven by commercial contract cleaners and residential users alike. The U.S. carpet cleaning services industry alone is worth $6.9 billion in 2026, signaling that professional-grade machines are entering households as consumers demand DIY deep-cleaning capabilities. The key distinction within this sub-topic is the separation of cleaning methods: carpet extractors use a combination of water, detergent, and mechanical agitation, while carpet steamers rely on high-temperature vapor to sanitize without chemicals. Both segments are growing, but the extractor category commands a larger share due to its efficacy on high-traffic areas and pet stains.

Industry Scope & Characteristics

Deep Cleaning vs. Surface Cleaning

Carpet cleaner machines are unique within home cleaning because they inject water and detergent into carpet fibers, then extract the dirty liquid—a process that removes embedded dirt, allergens, and bacteria that vacuums and steam mops cannot reach.

Consumables Ecosystem as Moats

Unlike vacuum cleaners, carpet cleaner machines require proprietary cleaning solutions, pre-treaters, and brush rolls. This creates a recurring revenue model for manufacturers, with consumables often accounting for 30–40% of total lifetime customer value.

Drying Time as a Key Performance Metric

Commercial buyers prioritize low-moisture technology that reduces carpet drying time from 4–6 hours to under 30 minutes. Certification standards like the Carpet and Rug Institute’s Seal of Approval are critical for commercial procurement decisions.

R&D Focus: Cold-Water Extraction Efficiency

Current R&D is concentrated on improving cold-water extraction efficiency to eliminate the need for heated tanks, which add weight and cost. Kärcher’s Puzzi series uses high-pressure injection to achieve hot-water-level cleaning at ambient temperatures.

Key market segments and growth drivers in the Carpet Cleaner Machine sector.

2. Market Analysis

The carpet cleaner machine market is not a monolith; it is a fragmented, multi-speed arena where residential and commercial demand pull in different directions. In 2025, the market stood at $992.51 million, with projections to reach $1.09 billion by 2035 at a CAGR of 4.45%. A separate analysis pegs the broader carpet cleaner market—including accessories, chemicals, and rental services—at $700.6 million in 2025, expanding at a CAGR of 5.33% to $1.13 billion by 2034. The discrepancy between these figures reflects differences in scope: the former focuses strictly on machine hardware, while the latter includes consumables and aftermarket parts. The three biggest growth drivers are unmistakable. First, the rise of pet ownership: in the U.S. alone, 66% of households own a pet, and carpet cleaner machines are the only effective solution for biological stains and odors that vacuums leave behind. Second, the shift toward hybrid work has increased the time people spend in their homes, making deep cleaning a recurring, non-negotiable chore. Third, the commercial segment—hotels, hospitals, and office cleaning contractors—is replacing older, inefficient machines with compact, low-moisture models that reduce drying time from hours to minutes. Regionally, North America accounts for the largest share, driven by the $6.9 billion U.S. carpet cleaning services ecosystem and a strong retail presence of brands like Bissell and Hoover. Europe follows, with Germany and the UK leading adoption of steam-based machines that align with stricter environmental regulations on chemical detergents. The Asia-Pacific market is the fastest-growing, fueled by urbanization in China and India, where rising disposable incomes are turning carpet cleaning from a luxury service into a household investment.

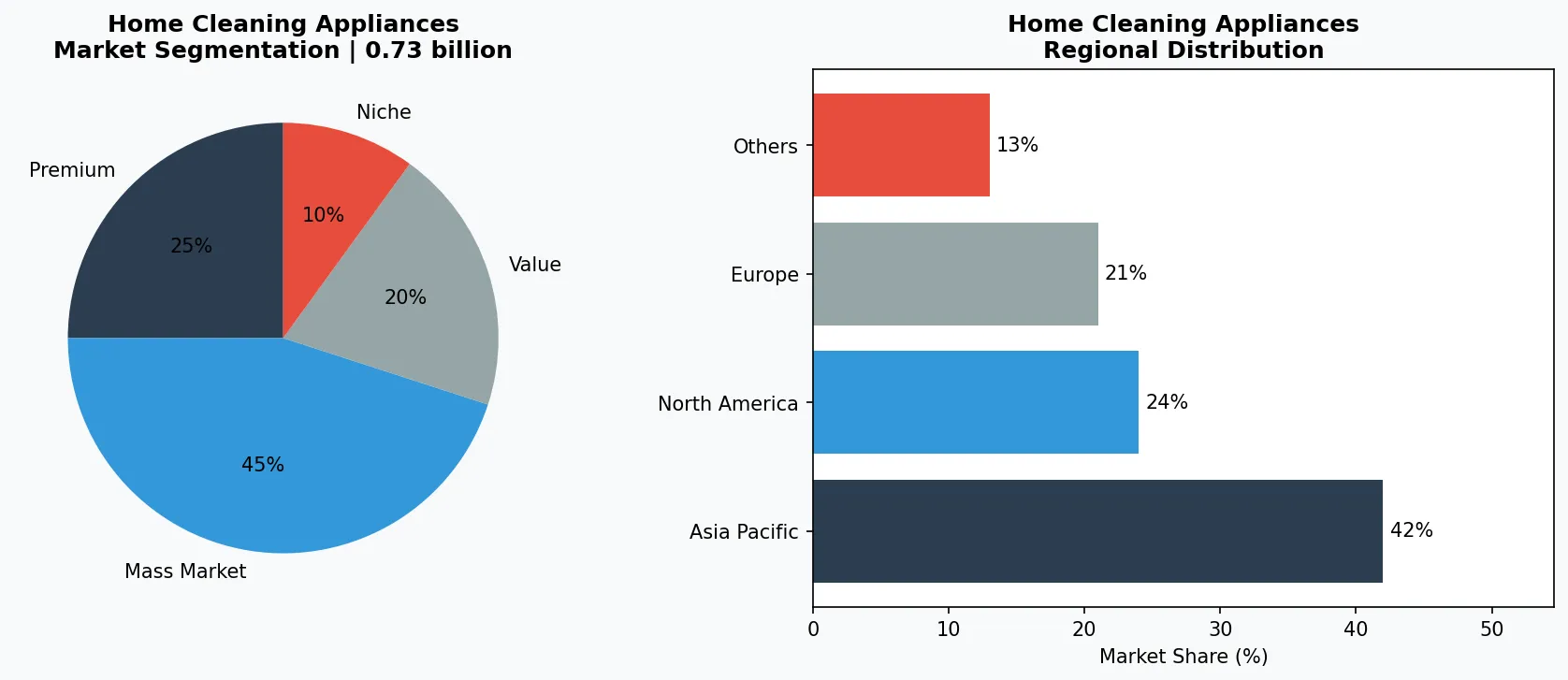

Market segmentation and regional distribution analysis for Carpet Cleaner Machine.

3. Product Categories

Carpet cleaner machines fall into three distinct product categories, each serving a different user profile and cleaning scenario.

Upright carpet cleaners

dominate the residential market. These are self-propelled units with rotating brushes, onboard water tanks, and squeeze-grip triggers that dispense solution. The Bissell ProHeat 2X Revolution is the benchmark here, offering a heated cleaning cycle that maintains water temperature for better grease removal.

Canister carpet cleaners

are the choice for commercial operators and homeowners with stairs or upholstery. They consist of a rolling base unit connected to a handheld wand, allowing maneuverability in tight spaces. The Rug Doctor Mighty Pro X3 is a widely rented canister model that uses a dual-cross-action brush system to agitate fibers from multiple angles.

Handheld spot cleaners

are the fastest-growing sub-segment, driven by pet owners. These compact, battery-powered devices—such as the Bissell SpotClean ProHeat—are designed for instant stain treatment on carpets, car interiors, and furniture. They lack the water capacity for whole-room cleaning but offer convenience and portability. Within each category, the key differentiator is cleaning method: extractors (water + detergent + suction) versus steamers (high-temperature vapor only). Steam-based machines are gaining traction in markets where chemical-free cleaning is a regulatory or consumer preference, but extractors remain the volume leader because of their superior performance on ground-in dirt and odors.

Upright Carpet Cleaners

Self-propelled, full-size units for whole-room deep cleaning. Examples: Bissell ProHeat 2X Revolution, Hoover SmartWash Automatic. Dominant in residential, with heated cleaning cycles and dual-tank systems for separate clean and dirty water.

Canister Carpet Cleaners

A rolling base unit with a handheld wand, designed for stairs, upholstery, and commercial use. Example: Rug Doctor Mighty Pro X3. Preferred by professional cleaners for maneuverability and higher water pressure.

Handheld Spot Cleaners

Compact, portable devices for instant stain treatment. Example: Bissell SpotClean ProHeat. Fastest-growing sub-segment, driven by pet owners and car detailing. Battery-powered models are emerging for cordless convenience.

4. Leading Players

Three company archetypes define the competitive landscape of the carpet cleaner machine market.

Bissell Inc.

is the dominant residential player, with a strategy built on mass-market retail distribution and pet-centric marketing. The company’s “Pet Stain & Odor” line, including the ProHeat 2X Revolution Pet Pro, accounts for a significant share of U.S. sales. Bissell’s competitive advantage lies in its consumables ecosystem—proprietary cleaning formulas that lock users into repeat purchases—and its partnership with PetSmart and other pet retailers.

Rug Doctor

, by contrast, competes primarily through a rental-first model. Its machines are available at grocery stores, home improvement centers, and supermarkets across North America, targeting consumers who want deep cleaning without the upfront investment of ownership. Rug Doctor’s strategy is to own the “occasional deep clean” occasion, and its Mighty Pro X3 is the most rented carpet cleaner in the U.S.

Kärcher

, a German industrial cleaning specialist, represents the commercial and premium tier. Its Puzzi series of extractors are used by professional cleaning contractors and hospitality chains. Kärcher’s advantage is engineering reliability and low-moisture technology that reduces drying time—a critical metric for hotels and offices that cannot afford downtime. The company also sells directly to B2B buyers through a dedicated sales force, bypassing retail channels. A fourth player,

Hoover

, competes at the value end of residential with the SmartWash series, which automates solution mixing and drying cycles to reduce user error. Hoover’s strategy is to simplify the user experience, making carpet cleaning accessible to first-time buyers.

Residential Mass-Market Leader

Bissell dominates U.S. retail with a pet-centric product line and a proprietary cleaning formula ecosystem that locks in repeat purchases. Its strategy is distribution density—available at Walmart, Target, Amazon, and pet specialty stores.

Rental-First Operator

Rug Doctor owns the 'occasional deep clean' occasion through 25,000+ rental kiosks in grocery and home improvement stores. Its competitive advantage is low upfront cost for consumers and high utilization of its machine fleet.

Commercial & Premium Specialist

Kärcher competes in the B2B segment with low-moisture extractors that dry carpets in under 30 minutes. Its Puzzi series is the standard for hotels and hospitals, sold through a direct sales force rather than retail.

5. Market Trends

1. Smart Integration

The rise of IoT-enabled carpet cleaners with app-based scheduling, automatic detergent dosing, and self-cleaning cycles is becoming a key differentiator for B2B buyers in hospitality and property management.

2. Cordless and Compact Designs

Lithium-ion battery advancements are driving demand for lightweight, portable carpet cleaners that offer commercial-grade extraction without tethering to outlets, appealing to janitorial service contractors and facility managers.

3. Water and Solution Efficiency

New models featuring closed-loop water recycling systems and concentrated solution metering are reducing operational costs and environmental impact, a priority for corporate sustainability programs and green building certifications.

4. Multi-Surface Versatility

Manufacturers are engineering units that seamlessly transition from deep carpet cleaning to hard floor washing and upholstery sanitization, meeting the diverse needs of commercial cleaning fleets and multi-unit residential maintenance.

6. Regional Markets

North America: Largest Market by Revenue

The U.S. carpet cleaning services industry is valued at $6.9 billion in 2026, driving both retail and rental demand. High carpet penetration (over 70% of homes) and pet ownership create a deep, recurring need for carpet cleaner machines.

Europe: Steam and Chemical-Free Preference

Germany and the UK lead adoption of steam-based carpet cleaners due to strict EU regulations on chemical detergents. Kärcher’s dry-extraction technology is particularly popular in commercial settings where environmental compliance is mandatory.

Asia-Pacific: Fastest-Growing Region

Urbanization in China and India is increasing carpet ownership in middle-class households. However, price sensitivity limits adoption of premium machines, creating an opportunity for rental models and sub-$150 entry-level units from local manufacturers.

7. Investment Outlook

Two specific opportunities stand out for the carpet cleaner machine market through 2030. First, the integration of carpet cleaning capabilities into multi-function floor care devices—hybrid machines that vacuum, mop, and extract in a single pass—could collapse the distinction between vacuum cleaners and carpet cleaners, expanding the market by converting vacuum owners into carpet cleaner buyers. Second, the expansion of rental and subscription models in Asia-Pacific, where carpet ownership is growing but upfront appliance spending is constrained, offers a high-volume, lower-margin growth path. The primary risk is the commoditization of entry-level machines: as Chinese manufacturers like Ecovacs and Roborock enter the carpet cleaner space with sub-$150 devices, margins for established players will compress, forcing them to compete on consumables and service contracts rather than hardware. Companies that fail to build a recurring revenue stream around filters, cleaning solutions, and brush replacements will face margin erosion by 2028.

Strategic Considerations:

- Opportunity: Multi-Function Hybrid Machines:

- Opportunity: Subscription Models in Asia-Pacific:

- Risk: Commoditization of Entry-Level Machines:

- Risk: Regulatory Pressure on Chemical Detergents:

Make Informed Decisions in the Carpet Cleaner Machine Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-26. All market figures are estimates and may vary from actual results.