Table of Contents

The global Cooking Wine Usage Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

What separates a good dish from a great one? Often, it's the splash of cooking wine. Far from a niche product, cooking wine has evolved into a fundamental flavoring ingredient, a strategic component in the global Seasonings & Spices industry valued for its ability to deglaze, tenderize, and impart complex acidity and aroma. Its distinction lies in its dual nature: it is both a culinary tool and a consumable flavor agent, bridging the gap between liquid condiments and dry spices. The market's momentum underscores its importance. In 2026 alone, the global cooking wine market is evaluated at USD 474.27 million, according to Towards FnB, and is on a steady growth path. This isn't a stagnant pantry staple; it's a dynamic segment where tradition meets innovation, driven by culinary exploration and shifting consumer palates. As a foundational element in cuisines from French coq au vin to Chinese braised pork belly, its usage guide is essentially a guide to building foundational flavor.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Shaoxing wine, Japanese mirin, Korean cooking wine, rice wine, medley of cooking wines, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Industry application and market overview for Cooking Wine Usage Guide.

2. Market Analysis

The cooking wine market is demonstrating robust, consistent growth, transforming from a commodity into a value-added segment. The industry generated USD 463.41 million in 2025 and expanded to USD 494.34 million in 2026, reflecting a strong annual growth rate of 6.15%. Looking forward, analysts project the market to grow from $430.56 million in 2026 to $627.33 million by 2034, achieving a compound annual growth rate (CAGR) of 4.82%. This growth is propelled by several key drivers. First, the globalization of culinary tastes and the rising popularity of cooking shows and digital recipe platforms have demystified wine usage for home cooks, fueling retail demand. Second, the expansion of the foodservice industry, particularly in Asia-Pacific and North America, creates consistent bulk demand for cooking wine as a core kitchen ingredient. Third, the product segmentation itself is a growth engine, with specific types like white wine showing particularly high growth rates due to their versatility in seafood, poultry, and cream-based sauces. This data confirms cooking wine is not a discretionary purchase but a recurring, essential input for both professional and amateur kitchens.

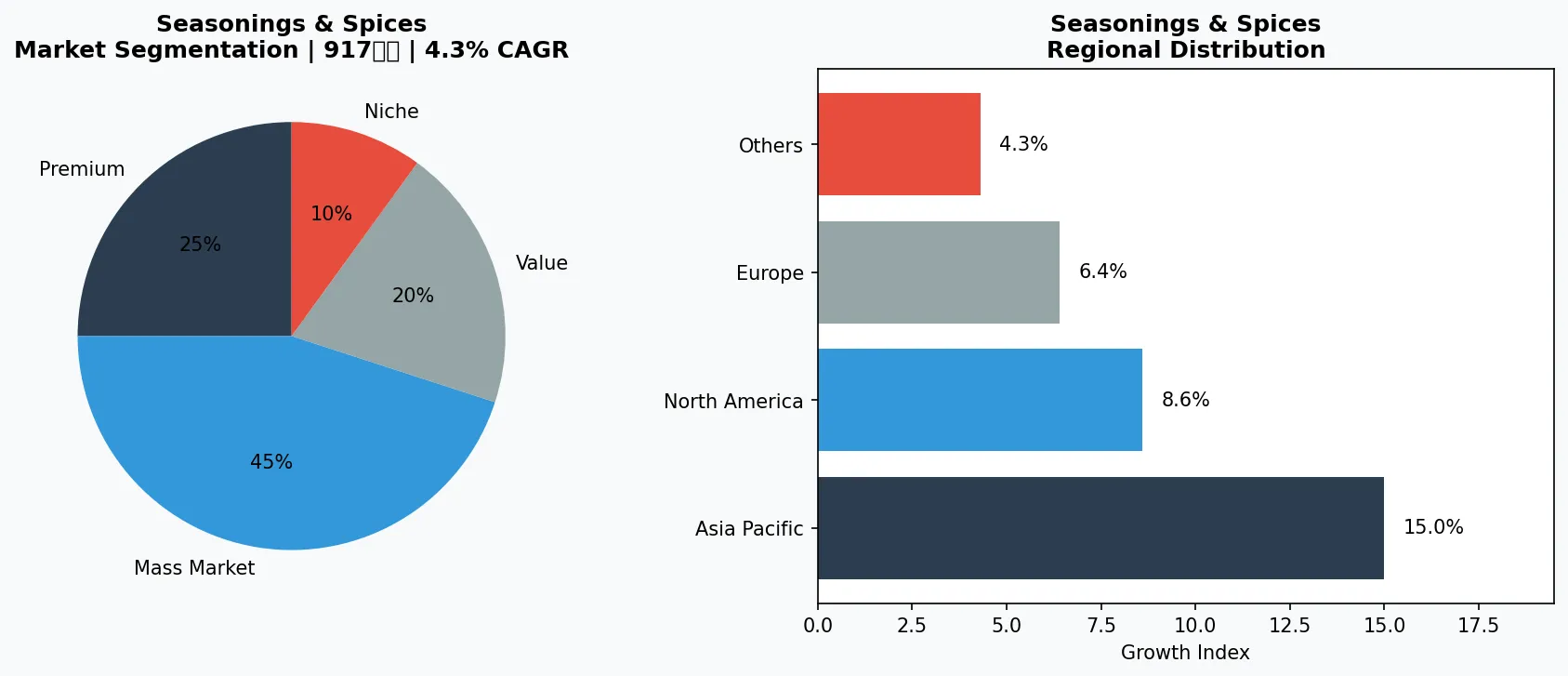

Market segmentation and regional distribution for Seasonings & Spices - Cooking Wine Usage Guide.

3. Product Categories

Cooking wine is broadly categorized by its base, each serving distinct culinary functions. The first major type is **Red Cooking Wine**, typically made from varieties like Cabernet Sauvignon or Merlot. It is essential for rich, slow-cooked dishes such as beef bourguignon, stews, and red wine reductions, where its tannins and deep fruit notes build foundational flavor. **White Cooking Wine**, the segment expected to see the highest growth rate, includes varieties like Sauvignon Blanc or Chardonnay. Its lighter, more acidic profile makes it ideal for deglazing pans, cooking seafood, poultry, and in creamy sauces like beurre blanc. A third critical category is **Specialized Regional Variants**, such as Shaoxing wine from China, a key ingredient in Asian cuisine for marinating and braising, or Mirin from Japan, used for its sweet, mild flavor in glazes and teriyaki. These products are often salted or seasoned differently to cater to specific culinary traditions and preservation needs.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

The competitive landscape features established flavor houses and specialized producers. **Mizkan Group**, a global leader in vinegars and seasonings, leverages its expertise in fermented flavorings to offer a range of cooking wines, including mirin and sake, targeting the premium and authentic Asian cuisine segments through strong retail and foodservice distribution. **Nakano Foods**, another key player in the Japanese condiment space, competes directly with a focus on authentic, naturally brewed rice wines (mirin), emphasizing traditional production methods to appeal to purists and professional chefs seeking quality foundational ingredients. **Kikkoman Corporation**, globally synonymous with soy sauce, strategically includes cooking wines like mirin and sake in its portfolio, using its unparalleled brand recognition and distribution network in the Seasonings & Spices aisle to cross-sell and provide a complete flavor solution for Asian-inspired cooking.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the seasonings & spices space.

5. Market Trends & Innovations

1. Sustainability & Eco-Friendly Innovation

Sustainability has become a core competitive priority. Companies like Kikkoman and Lee Kum Kee are investing in eco-friendly materials, carbon-neutral production, and circular economy initiatives to meet growing consumer demand for responsible products.

2. Digital Transformation & E-Commerce Growth

The shift to digital sales channels continues to accelerate. Shaoxing Pagoda and Miyako are leveraging data analytics, AI-driven personalization, and omnichannel strategies to enhance customer engagement and streamline distribution.

3. Premiumization & Product Innovation

Rising consumer expectations are driving premiumization across the market. Shanghai Maling has introduced high-end product lines, while Dragonfly focuses on innovative features and superior quality to capture value-conscious yet quality-seeking customers.

4. Health, Wellness & Functional Benefits

Health-oriented consumer preferences are reshaping product development. Haitian Flavouring and Kerry Group are pioneering functional products with demonstrable benefits, commanding premium pricing and driving category expansion.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

The outlook for cooking wine is defined by clear opportunities and one persistent challenge. The primary opportunity lies in geographic market penetration, especially in emerging economies where a growing middle class is experimenting with global cuisines. Tailoring products, such as lighter or less alcoholic variants, to local taste and regulatory preferences will be key. A second opportunity is product innovation through fusion formats, like cooking wine infused with herbs, spices, or chili, creating ready-made flavor bases that simplify cooking and command a higher price point.

The concrete risk remains market fragmentation and consumer confusion. The line between 'cooking wine' and 'drinking wine' is blurring, which can be a premiumization driver but also leads to substitution. If consumers perceive any affordable wine as suitable for cooking, it could commoditize the dedicated cooking wine segment. Producers must continuously articulate the unique value—consistent flavor profile, seasoning balance, and culinary reliability—of their purpose-built products to defend their market position.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Cooking Wine Usage Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-20. All market figures are estimates and may vary from actual results.