Table of Contents

The global Countertop Materials Comparison sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Nearly half of all kitchen countertop requests in 2026 involve natural stone, yet engineered quartz is rapidly closing the gap. This paradox defines the most consequential year in kitchen surface history. Homeowners face an increasingly complex decision matrix: premium natural materials like granite and marble promise timeless beauty but demand maintenance, while engineered alternatives promise durability but often sacrifice authenticity. The National Kitchen and Bath Association's 2026 trends report reveals that countertop selection has become the primary battleground where design vision meets practical reality. Industry data shows consumers are spending more time researching surface materials than any other kitchen component, signaling a fundamental shift in how buyers approach renovation decisions. For manufacturers and suppliers in the kitchen furniture sector, understanding these material dynamics is no longer optional—it is essential for survival in a market where surface choices increasingly define entire kitchen identities.

Industry Scope & Characteristics

Material Specification Complexity

Countertop materials comparison requires understanding of vastly different properties—natural stone offers unique veining but demands sealing, while engineered quartz provides consistency but limited heat resistance. Porcelain slabs enable large seamless installations but require specialized fabrication equipment. This complexity differentiates countertop specification from other kitchen furniture components, creating need for expert consultation.

Global Supply Chain Dependencies

Natural stone countertop materials depend heavily on quarry locations in Brazil, Italy, India, and China, creating extended lead times that can exceed 12 weeks for exotic materials. Engineered quartz production concentrates in Israel, Spain, and North America, offering more reliable supply but subject to resin pricing volatility. Logistics costs for heavy stone materials significantly impact regional price competitiveness.

Industry Certification Standards

NSF International certification for food contact surfaces has become a de facto requirement for countertop materials in North American commercial applications. Marble Institute of America grading standards define quality tiers for natural stone. FloorScore certification addresses indoor air quality for engineered materials. These certifications influence specification decisions and create competitive differentiation for compliant manufacturers.

Digital Visualization Integration

Augmented reality applications now enable homeowners to preview countertop materials in virtual kitchen environments before purchase, reducing specification uncertainty. Major manufacturers have developed proprietary visualization tools integrated with kitchen design software. This technological integration is rapidly becoming a competitive necessity for consumer-facing countertop brands seeking specification momentum.

The countertop materials comparison landscape has fundamentally shifted. What was once a straightforward choice between laminate and solid surface has exploded into a sophisticated ecosystem of engineered stone, ultra-compact surfaces, porcelain slabs, and sustainably sourced natural materials. Each category now competes fiercely for the same premium kitchen dollar, with manufacturers investing billions in production facilities that can deliver both aesthetics and performance. The stakes are extraordinarily high: countertop selections now influence everything from cabinet pairings to overall kitchen layout, making surface materials a pivotal specification in the kitchen furniture supply chain.

Market signals indicate a decisive turning point. KBDN's annual countertop survey confirms that natural stone accounts for nearly half of all material requests, yet the same data reveals quartz gaining significant ground among design-conscious homeowners seeking low-maintenance alternatives. This dual demand is forcing manufacturers to innovate at unprecedented speeds while retailers must develop expertise to guide customers through increasingly complex specification processes. The kitchen furniture industry's future will be shaped by how effectively the supply chain adapts to these converging material preferences.

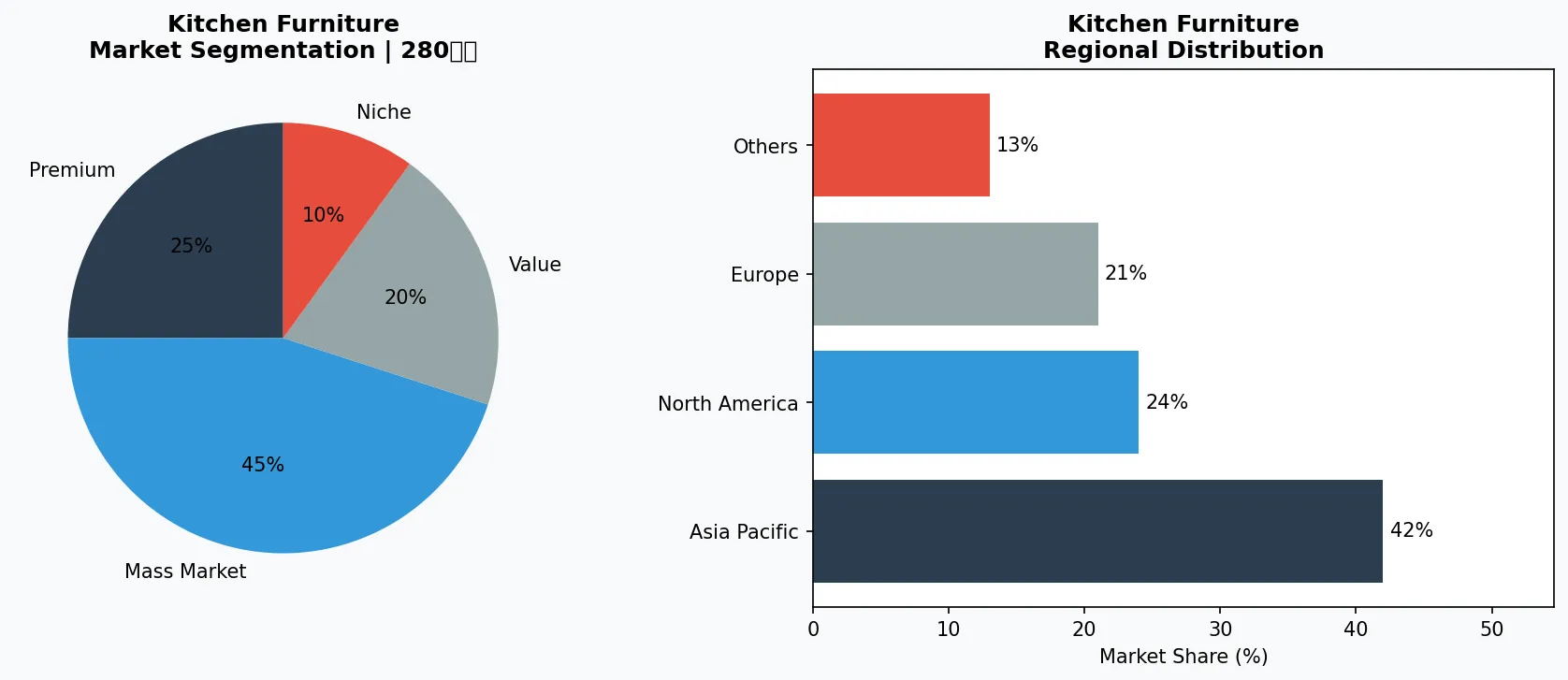

Key market segments and growth drivers in the Countertop Materials Comparison sector.

2. Market Analysis

The global countertop market reached $44.1 billion in 2024 and is projected to grow at a compound annual rate of 5.2% through 2032, according to multiple industry analyses. This growth trajectory positions kitchen surfaces as one of the most dynamic segments within the broader kitchen furniture sector. Housing starts, renovation cycles, and shifting consumer preferences toward premium materials are driving sustained demand across both new construction and remodel markets. The North American market remains the largest consumer of premium countertop materials, with the United States accounting for approximately 38% of global demand for high-end stone and engineered surfaces.

The growth drivers are remarkably specific. First, quartz demand has surged, with the material now representing nearly 50% of material requests in new kitchen builds, up from 31% in 2019. Second, the premiumization trend continues unabated, with average countertop spend per kitchen increasing 23% since 2022 as homeowners opt for larger islands and full-coverage installations. Third, the renovation market has remained robust despite economic headwinds, with the National Kitchen and Bath Association reporting that kitchen remodels valued over $50,000 increased 12% year-over-year through mid-2025. These figures confirm that countertop materials remain a critical value driver in the kitchen furniture category.

Regional dynamics add complexity. The Asia-Pacific market, particularly China and India, is emerging as the fastest-growing region for countertop consumption, driven by urbanization and rising middle-class disposable income. European markets show strong preference for locally sourced materials and sustainable manufacturing credentials. For suppliers operating globally, understanding these geographic nuances is essential for product positioning and inventory strategy. The market is not uniform—material preferences shift dramatically by region, and supply chain strategies must reflect these differences to capture growth opportunities.

Growth restraints exist, however. Economic uncertainty has dampened large-ticket purchases in certain markets, and raw material availability—particularly for natural stone—remains a constraint. Quarry limitations in key regions like Brazil and Italy have extended lead times, pushing some buyers toward more readily available engineered alternatives. These supply constraints are reshaping competitive dynamics and favoring manufacturers with diversified material sourcing and production capabilities.

Market segmentation and regional distribution analysis for Countertop Materials Comparison.

3. Product Categories

Natural Stone remains the category leader by request volume, commanding the largest share of homeowner specifications. Granite continues to dominate in traditional and transitional kitchen designs, prized for its heat resistance and unique veining patterns. Marble has experienced a resurgence in luxury markets, particularly in open-plan kitchens where it serves as a focal point. The category includes soapstone, limestone, and travertine for specialized applications. Pricing ranges from $40 per square foot for entry-level granite to over $200 per square foot for rare exotic marbles, creating a wide accessibility range.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Engineered Quartz has emerged as the fastest-growing category, now specified in nearly half of new kitchen builds. The material combines ground quartzite with polymer resins to create surfaces that offer consistent coloring, minimal porosity, and remarkable durability. Brands like Caesarstone have pioneered large-format slabs that enable seamless installations across islands and perimeter countertops. The category continues to innovate with new color collections that authentically replicate marble and granite veining while maintaining quartz's signature performance advantages. Porcelain slabs represent the newest category gaining rapid adoption, particularly for applications requiring large-format coverage with minimal seams. The material's inherent UV resistance and thermal stability make it suitable for both indoor and outdoor kitchen applications, a flexibility that has expanded its use cases significantly. Brands like Neolith and Lapitec have positioned porcelain as a premium engineered surface option, competing directly with natural stone and quartz in high-end specifications. The material typically ranges from $60 to $150 per square foot installed, positioning it as a mid-premium option with unique performance characteristics.

Laminate countertops continue serving the value-conscious segment, offering functional surfaces at price points inaccessible to stone-based materials. Global market analyses confirm cautious growth for laminate—modest compared to stone, but meaningful in absolute terms. The category has improved significantly in aesthetics, with high-definition printing technologies enabling realistic stone and wood reproductions. Brands like Formica and Wilsonart now offer premium laminate collections that blur traditional distinctions with engineered surfaces, targeting first-time homebuyers and budget renovation projects where durability and affordability outweigh premium positioning requirements.

4. Leading Players

Caesarstone Ltd. has established itself as the dominant force in the engineered quartz segment through relentless innovation and brand positioning. The company's strategy centers on design leadership—investing heavily in R&D to develop proprietary color palettes and surface textures that set trends rather than follow them. Caesarstone's 2026 collections emphasized tactile finishes and warm neutral tones, responding directly to consumer demand for surfaces that combine performance with authentic natural aesthetics. The company operates manufacturing facilities across multiple continents, enabling rapid scaling to meet regional demand patterns while maintaining quality consistency. Strategic partnerships with major kitchen furniture brands have cemented Caesarstone's specification position in premium new home construction and high-end renovation projects globally.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the kitchen furniture space.

Cosentino Group, the Spanish multinational, has pursued an aggressive diversification strategy that positions it across multiple material categories. The company manufactures Silestone (quartz), Dekton (ultra-compact surface), and Scalea (natural stone), enabling sales teams to recommend optimal solutions for each application without bias toward a single technology. Cosentino's digital visualization tools allow designers and homeowners to preview materials in virtual kitchen environments, addressing a key friction point in the specification process. The company's sustainability initiatives—including carbon-neutral manufacturing targets and recycled material content in select product lines—resonate strongly with environmentally conscious European buyers. Cosentino's expansion into North American markets through dedicated distribution networks and strong relationships with cabinet manufacturers has made it a formidable competitor in the premium countertop segment.

LG Hausys, the Korean materials conglomerate, has leveraged its manufacturing scale and technical capabilities to become a significant global player in engineered surfaces. The company's Hi-Macs solid surface and Viatera quartz lines compete primarily through value positioning—delivering competitive quality at price points that undercut premium European and North American brands. LG Hausys has made substantial inroads in Asian markets and is expanding its presence in North America through distributor networks and targeted specification programs with major kitchen furniture brands. The company's vertical integration across home materials provides unique cross-selling opportunities, enabling countertop sales to benefit from cabinet and flooring specification processes.

Diresco, the Belgian engineered stone manufacturer, has carved a distinctive position through sustainability-focused innovation. The company's Bio-based collection utilizes plant-derived binders that reduce carbon footprint while maintaining performance specifications. Diresco's ultra-compact surface technology competes directly with Cosentino's Dekton in premium applications, offering similar technical characteristics with a European manufacturing footprint that appeals to buyers prioritizing regional production. The company's strategic focus on architectural and design community relationships has generated strong specification momentum in high-end residential and commercial projects where environmental credentials influence material selection.

5. Market Trends

1. NATURAL STONE AESTHETICS IN ENGINEERED MATERIALS

Engineered quartz manufacturers are increasingly developing styles, colors, and finishes that most closely replicate natural stone, blurring traditional category distinctions. This matters because consumers desire the beauty of natural materials without maintenance burdens. Cosentino's Marble Collection specifically targets this crossover demand with quartz surfaces that feature authentic veining and subtle color variations. | PORCELAIN SLAB EXPANSION | Ultra-compact porcelain surfaces are gaining significant specification share in premium kitchen applications where thermal resistance and large-format capability matter. This matters because porcelain solves specific problems that natural stone and quartz cannot address, particularly for outdoor kitchens and high-heat cooking zones. Neolith has positioned its newest collections specifically for kitchen island applications, targeting designs where previous materials could not deliver required performance. | SUSTAINABLE MANUFACTURING CREDENTIALS | Major countertop manufacturers have accelerated environmental initiatives, including recycled content, carbon-neutral production, and bio-based material development. This matters because commercial specifications increasingly require environmental documentation, and residential buyers—particularly in European markets—prioritize manufacturing sustainability. Diresco's complete bio-based binder system represents the most comprehensive response to this trend, enabling the company to capture specification momentum in environmentally sensitive project categories. | MIXED-MATERIAL KITCHEN DESIGN | Designers increasingly specify different countertop materials for different kitchen zones, using premium surfaces at focal points and practical materials in secondary areas. This matters because it allows budget optimization while maintaining visual impact at key design moments. Caesarstone's coordination tools help designers plan material transitions and specify appropriate products for each kitchen zone.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

The countertop materials comparison landscape offers two distinct opportunities for industry participants. First, the premiumization trend shows no signs of deceleration—homeowners continue allocating larger budget shares to surfaces, creating space for manufacturers to introduce higher-priced innovations. The growing demand for customized solutions, highlighted in multiple industry reports, represents a specific opportunity to capture margin through made-to-order specifications. Second, the Asia-Pacific market expansion presents geographic growth opportunities for brands with production capacity or distribution partnerships in emerging kitchen furniture markets. Regional manufacturers with localized production can capture market share from imported materials by offering shorter lead times and competitive pricing.

The primary risk centers on raw material supply chain vulnerability, particularly for natural stone categories dependent on Brazilian and Italian quarries. Extended lead times and pricing volatility have already pushed some buyers toward engineered alternatives, and continued supply constraints could accelerate this shift. Manufacturers with single-source dependencies face existential risk if key material streams become unavailable. The actionable response involves diversifying material sourcing, investing in engineered alternatives that offer supply chain stability, and developing customer education programs that position engineered materials as reliable alternatives to finite natural resources. Companies that address this vulnerability proactively will be better positioned for the $44 billion market opportunity that awaits in 2026 and beyond.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Countertop Materials Comparison Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-10. All market figures are estimates and may vary from actual results.