Table of Contents

The global Drawer Dividers Organizers sector serves consumers worldwide with diverse solutions.

1. Industry Overview

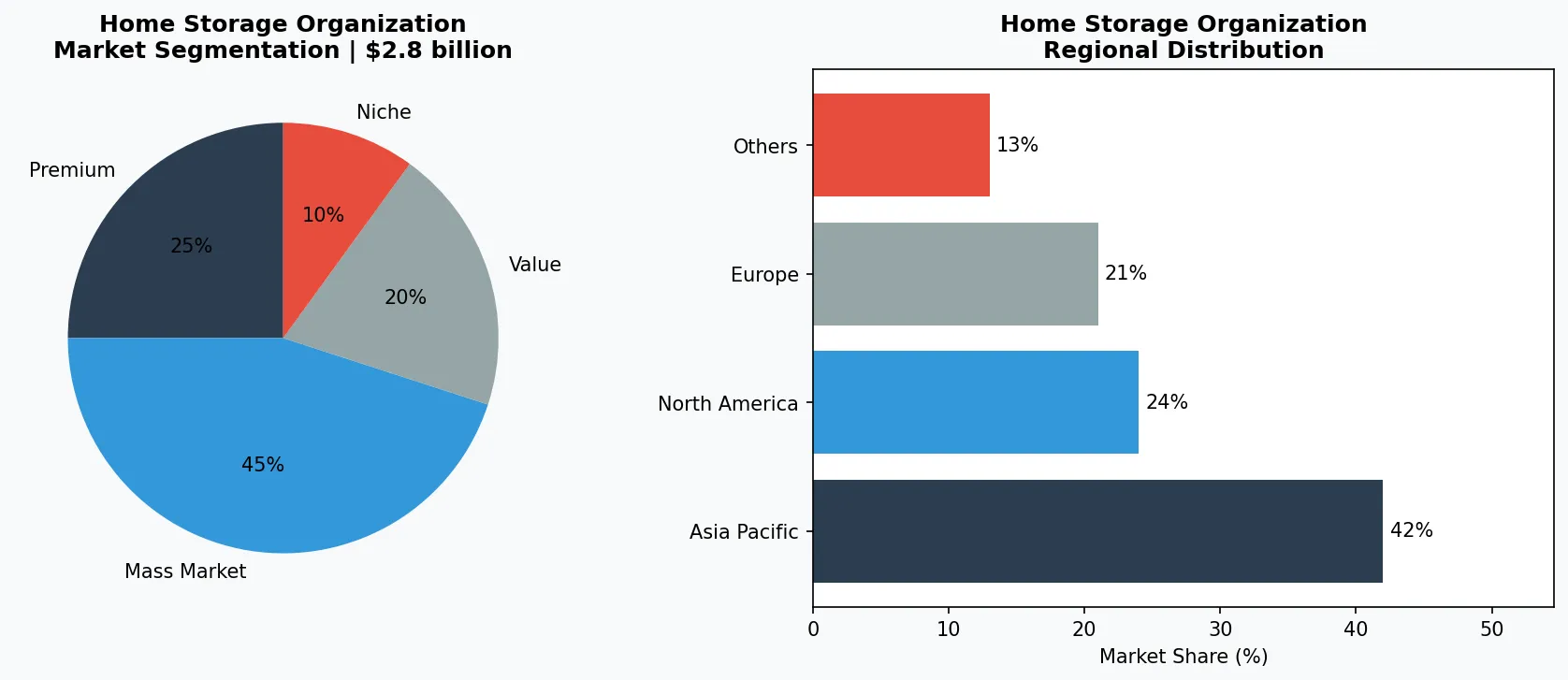

The global desk drawer organizer market hit $2.8 billion in 2025 and is on track to surge past $4.6 billion by 2034, growing at a compound annual rate of 5.7%. That is not a niche accessory play—it is a structural shift in how businesses and consumers approach workspace efficiency. Drawer dividers organizers, once an afterthought in the home storage ecosystem, have become a critical sub-category within the broader $21.42 billion professional organizer market. The catalyst? The permanent adoption of remote and hybrid work models, which has turned home desks into primary command centers for millions of knowledge workers worldwide.

Industry Scope & Characteristics

Precision Engineering for Small Spaces

Drawer dividers organizers are uniquely designed to maximize limited drawer volume, with modular systems that adapt to irregular dimensions—a level of customization not seen in closet or shelf organizers.

High SKU Complexity in Manufacturing

Producing drawer dividers requires hundreds of size and material variants, making inventory management a core challenge. Top manufacturers use just-in-time production to reduce warehousing costs.

FSC and FDA Compliance Standards

Bamboo dividers must meet FSC certification for sustainability claims, while plastic dividers used in kitchen drawers require FDA food-contact approval. Non-compliance can block retail distribution in regulated markets.

AI-Driven Custom Fit Technology

R&D is focused on mobile apps that scan drawer dimensions via smartphone camera and generate custom divider layouts, reducing return rates and enabling direct-to-consumer sales without physical retail.

What distinguishes drawer dividers organizers from generic storage bins or closet systems is their precision engineering. These products are designed to micro-manage small, high-value items—pens, cables, tools, cosmetics—within confined spaces. Unlike bulky closet organizers or shoe racks, drawer dividers maximize vertical and horizontal real estate inside existing furniture, making them indispensable for high-density living in urban markets across Asia, Europe, and North America. The segment's growth is also fueled by a 7.9% CAGR in the professional organizer market, as certified organizers increasingly recommend customized divider solutions to clients seeking order in chaotic drawers.

The market's DNA is split between two distinct consumer behaviors: the DIY home user who buys adjustable bamboo or plastic dividers from Amazon or IKEA, and the commercial buyer—office managers, co-working spaces, and hospitality firms—who require durable, standardized systems. This duality has forced manufacturers to innovate across materials, from sustainable bamboo to antimicrobial plastics, while keeping price points accessible. The result is a market that is both fragmented and fiercely competitive, with room for specialized players to capture share through design patents or eco-certifications.

Key market segments and growth drivers in the Drawer Dividers Organizers sector.

2. Market Analysis

The desk drawer organizer market is not just growing—it is accelerating. Valued at $2.8 billion in 2025, analysts project it will expand at a 5.7% CAGR through 2034, reaching $4.6 billion. But the broader large drawer organizers segment, which includes kitchen, workshop, and vanity drawer systems, is forecast to grow even faster, at a 6.3% CAGR from 2026 to 2033. This divergence signals that while office desk organization remains the anchor, residential applications are becoming the growth engine.

Three forces are driving this expansion. First, the remote work revolution is permanent: over 35% of knowledge workers in the U.S. and Europe now operate from home at least three days a week, according to 2024 labor data. Each home office upgrade cycle—monitor, chair, desk—inevitably leads to a drawer organization purchase. Second, the professional organizer industry is booming at a 7.9% CAGR, crossing $21.42 billion by 2033. These specialists are prescribing drawer dividers as a first-line solution for clients, creating a B2B2C demand channel. Third, material innovation is lowering costs: bamboo and recycled PET felt dividers now cost 40% less than five years ago, making them accessible to budget-conscious consumers.

Regional dynamics tell a nuanced story. North America leads in per-capita spending, driven by high home office penetration and a mature professional organizer ecosystem. However, Asia-Pacific is the fastest-growing region, with China, Japan, and South Korea seeing explosive demand from compact urban apartments. European markets are characterized by a preference for premium, sustainable materials—German and Scandinavian consumers routinely pay $30–$50 for modular bamboo systems. Latin America and the Middle East remain nascent but are catching up as e-commerce platforms like Mercado Libre and Noon expand their home storage categories.

Key market restraints include raw material price volatility for bamboo and PET, and the challenge of SKU proliferation—manufacturers must offer hundreds of size configurations to fit diverse drawer dimensions. Yet, the overall trajectory is clear: as hybrid work solidifies and urban living spaces shrink, drawer dividers organizers will remain a high-growth sub-category within home storage.

Market segmentation and regional distribution analysis for Drawer Dividers Organizers.

3. Product Categories

Drawer dividers organizers break into three distinct product segments, each serving different user needs and price points. The first is

Adjustable Modular Systems

the workhorses of the market. These include expandable bamboo grids with snap-in dividers, plastic grid systems with movable pegs, and metal track-based organizers. Brands like Simplehuman and IKEA dominate this space with products that fit standard desk drawers (20–24 inches wide) but require no tools. The key innovation here is flexibility: users can reconfigure compartments as their needs change, reducing replacement frequency. The second segment is

Custom-Fit Foam and Felt Inserts

, a premium category growing at 8% annually. These are laser-cut or die-cut inserts tailored to specific drawer dimensions, often sold by companies like Trellis or Griot's Garage. They are popular among professionals—mechanics, artists, and makeup enthusiasts—who need exact-fit cradles for tools, brushes, or cosmetics. The barrier to entry is higher, but so is customer loyalty: once a user buys a custom insert, they rarely switch. This segment is also seeing a shift toward antimicrobial materials, a direct response to post-pandemic hygiene concerns. The third segment is

Stackable and Expandable Trays

, a budget-friendly option priced under $15. These are typically made of clear acrylic or polypropylene and sit inside drawers without permanent installation. They appeal to renters and students who need temporary solutions. The downside is limited durability—trays can warp under heat or weight—but their low cost drives high volume. Amazon's Basics line and Chinese manufacturers on AliExpress dominate this tier, often selling in multi-pack bundles. For B2B buyers, this segment offers the fastest inventory turnover but the lowest margins.

Adjustable Modular Systems

Expandable bamboo or plastic grids with movable dividers, priced $15–$50. Examples: IKEA KUGGIS, Simplehuman steel-frame organizer.

Custom-Fit Foam & Felt Inserts

Laser-cut inserts tailored to specific drawer dimensions, priced $25–$100. Popular among professionals for tool and cosmetic storage.

Stackable Budget Trays

Clear acrylic or polypropylene trays sold in multi-packs under $15. Dominated by Amazon Basics and Chinese OEMs; high volume, low margin.

4. Leading Players

The market features a mix of global conglomerates and niche specialists.

IKEA

, the Swedish furniture giant, leverages its SKÅDIS pegboard system and KUGGIS drawer inserts to capture the mass-market DIY segment. IKEA's advantage is distribution: its 460+ stores worldwide and robust e-commerce platform make its drawer dividers a default choice for first-time buyers. The company's 2025 push into bamboo-based dividers signals a strategic shift toward sustainability, aiming to attract eco-conscious millennials.

Simplehuman

, a California-based premium brand, targets the high-end home office and kitchen buyer. Its steel-frame drawer organizers, priced between $30 and $80, feature magnetic dividers and non-slip silicone bases. Simplehuman's strategy is built on design patents and a direct-to-consumer model that bypasses traditional retail markups. The company reported 12% revenue growth in 2024, driven by its 'custom-fit' line that uses an online drawer measurement tool. This data-driven approach reduces returns and increases customer lifetime value.

The Container Store

, a U.S. specialty retailer, positions itself as a one-stop shop for organization, with over 80 SKUs of drawer dividers under its own Elfa brand. Its competitive advantage is the 'Custom Drawer' service, where in-store designers create tailored solutions for clients. Despite retail headwinds, The Container Store's drawer divider category grew 9% in fiscal 2025, buoyed by its professional organizer referral program. The company is now expanding into Asian markets through partnerships with Japanese department stores.

Chinese OEMs

like

Yonghui Storage

and

Shenzhen Homeleader

are the invisible giants, producing unbranded bamboo and plastic dividers for Amazon sellers and European retailers. Their scale is staggering: Yonghui's factory in Fujian province produces 500,000 units monthly at 30–50% lower cost than Western competitors. The risk for these players is margin compression as raw material costs rise, but their dominance in the value segment is unlikely to be challenged soon.

Mass-Market Scale Player

IKEA uses global distribution and bamboo sustainability pivot to capture first-time buyers. Its KUGGIS line is the default choice for DIY home office setups.

Premium Design-Led Specialist

Simplehuman focuses on steel-frame, patent-protected designs with direct-to-consumer sales. Its custom-fit online tool reduces returns and builds brand loyalty.

Value Chain OEM Dominator

Chinese OEMs like Yonghui Storage produce unbranded dividers at 30–50% lower cost, supplying Amazon sellers and European retailers. Scale is their moat.

5. Market Trends

1. SUSTAINABLE MATERIALS SHIFT

Consumers are increasingly rejecting virgin plastics. Bamboo and recycled PET felt are the fastest-growing materials, with bamboo dividers seeing 22% year-over-year sales growth in 2025. IKEA's 2024 decision to phase out plastic drawer dividers in favor of bamboo by 2028 underscores the trend. For B2B buyers, sourcing from Forest Stewardship Council (FSC)-certified bamboo suppliers is becoming a non-negotiable requirement for retail listings in Europe and California.

2. SMART DRAWER INTEGRATION

The line between furniture and technology is blurring. Startups like Drew's Drawer (notable for its 2024 Kickstarter) are embedding wireless charging pads and LED lighting into drawer divider systems. While still nascent—less than 2% of the market—this trend is gaining traction in premium co-working spaces and high-end residential projects. The opportunity for manufacturers lies in developing modular, tech-ready divider components that can be retrofitted into existing drawers.

3. HYPER-PERSONALIZATION VIA AI

Professional organizers are using AI tools to recommend drawer layouts based on user habits. Companies like Neatly (a software platform for organizers) now offer a 'drawer planner' feature that generates custom divider configurations. This trend is driving demand for modular systems that can be quickly reconfigured. For product makers, offering API-accessible dimension data for their dividers could become a competitive advantage as the professional organizer market scales.

4. B2B BULK AND SUBSCRIPTION MODELS

Office supply chains are shifting from one-time purchases to recurring orders. Staples and Office Depot now offer 'Drawer Refresh' subscriptions for businesses, delivering new divider sets every six months. This model stabilizes revenue for manufacturers and ensures consistent demand. The key is designing dividers with planned obsolescence—using materials that degrade after 12–18 months—which is controversial but effective for recurring revenue.

6. Regional Markets

North America: High Per-Capita Spending

Driven by permanent remote work adoption and a mature professional organizer ecosystem; home office drawer dividers account for 40% of regional sales.

Asia-Pacific: Compact Urban Living Demand

Fastest-growing region due to small apartment sizes in Tokyo, Seoul, and Shanghai. Consumers prefer narrow, stackable bamboo dividers.

Europe: Premium Sustainability Focus

German and Scandinavian buyers pay premium for FSC-certified bamboo and recycled materials. Regulatory pressure on single-use plastics is accelerating material shifts.

7. Investment Outlook

Two opportunities stand out for businesses in the drawer dividers organizers space. First, the **hybrid office retrofit market**: as corporations downsize real estate and equip home offices for employees, bulk B2B orders for standardized divider systems are expected to grow 15% annually through 2028. Manufacturers who offer white-label solutions with corporate branding will capture this wave. Second, **Asia-Pacific urban micro-living**: with Tokyo, Seoul, and Shanghai seeing average apartment sizes under 600 sq. ft., demand for compact, multi-functional drawer organizers is exploding. Localizing products for Asian drawer dimensions (often narrower than Western standards) is a clear entry point.

The primary risk is **raw material inflation**. Bamboo prices rose 18% in 2025 due to supply chain disruptions in China and Myanmar, while recycled PET felt costs are tied to volatile oil markets. Companies that lock in multi-year supplier contracts or invest in alternative materials like mycelium-based composites will have a pricing advantage. The smartest players are already diversifying sourcing away from single-country dependency.

Strategic Considerations:

- Opportunity: Hybrid Office B2B Bulk Orders: Corporations equipping home offices will drive 15% annual growth in standardized divider systems through 2028; white-label branding is key.

- Opportunity: Asia-Pacific Micro-Living Products: Localizing dividers for narrower Asian drawer dimensions and compact urban homes offers a clear entry point in the fastest-growing region.

- Risk: Raw Material Cost Volatility: Bamboo prices rose 18% in 2025; companies should lock in multi-year supplier contracts or invest in alternative materials like mycelium composites.

- Risk: SKU Proliferation Complexity: Offering hundreds of size configurations strains manufacturing and inventory; AI-based customization tools can reduce SKU count while meeting customer needs.

Make Informed Decisions in the Drawer Dividers Organizers Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-25. All market figures are estimates and may vary from actual results.