Table of Contents

The global Electric Sweeper Comparison sector serves consumers worldwide with diverse solutions.

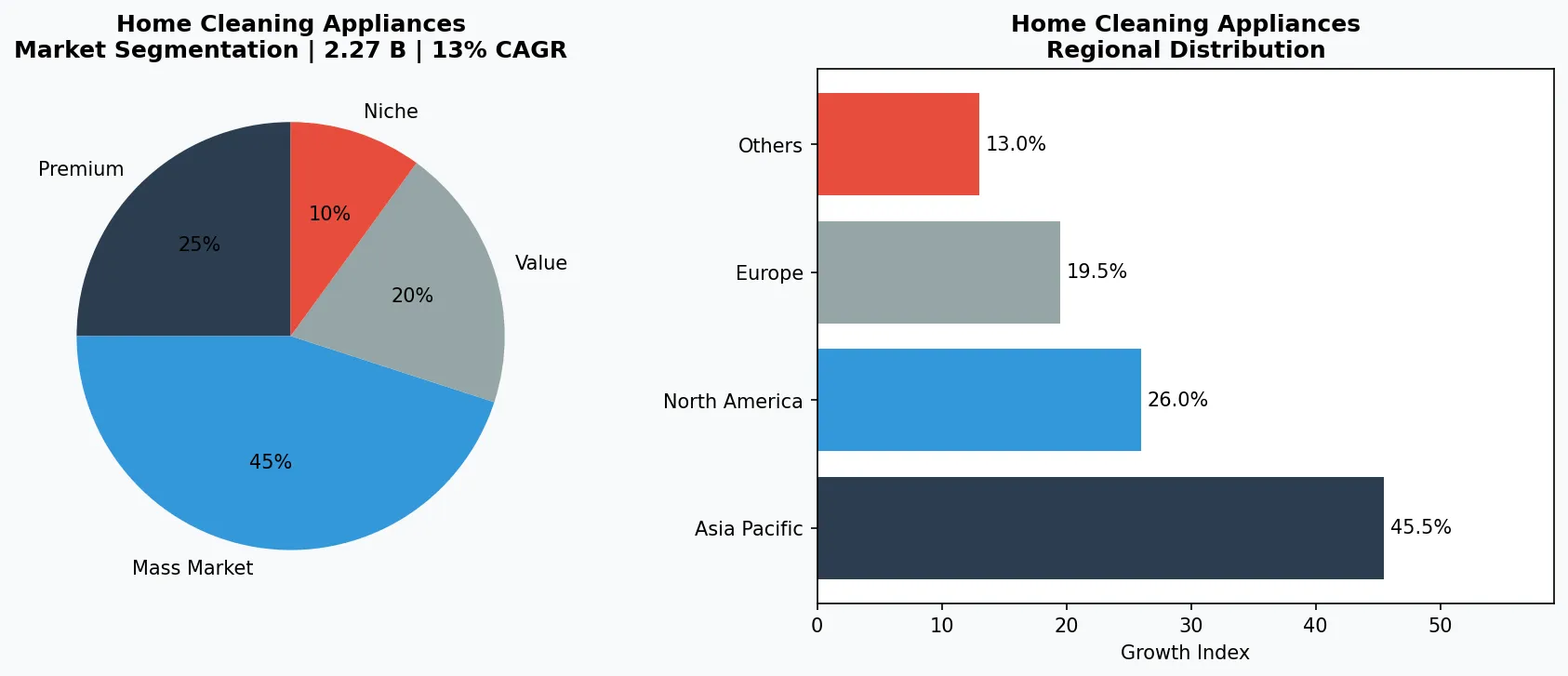

1. Industry Overview

The global street sweeper market is not just growing—it’s pivoting. Valued at $2.71 billion in 2025 and projected to reach $3.92 billion by 2034, the sector is undergoing a quiet but decisive electrification. For B2B buyers, the question is no longer whether to switch from diesel to electric, but which electric sweeper configuration delivers the best total cost of ownership for their specific application. This electric sweeper comparison cuts through the noise.

Industry Scope & Characteristics

Dual-Use Technology

Electric sweepers borrow sensor fusion and battery management systems from smart home cleaning robots, enabling precise navigation and low-noise operation in both indoor and outdoor environments.

Battery Supply Chain Dependency

Manufacturing lead times for electric sweepers are heavily influenced by lithium-ion cell availability; buyers should verify battery sourcing and warranty terms before committing to multi-year fleet contracts.

ISO 14001 and CE Certification

Electric sweepers sold in Europe must comply with CE machinery directives and ISO 14001 environmental management standards; North American buyers should look for UL or ETL certification on battery systems.

Modular Battery Architecture

The latest R&D focus is on hot-swappable battery cassettes that reduce vehicle downtime to under three minutes, a design pioneered by Hako and now being adopted by Elgin for its next-generation compact models.

What makes the electric sweeper segment distinctive within home cleaning appliances is its dual nature. On one hand, these are industrial-grade machines built for municipal sanitation and warehouse floors. On the other, they increasingly share sensor technology, battery management systems, and connectivity features with the smart home cleaning robots found in residential living rooms. The convergence is real: compact electric sweepers now integrate LiDAR navigation and IoT telemetry, borrowing directly from the robot vacuum playbook.

The market is bifurcating. At the high end, regenerative air sweepers with lithium-ion packs command premium pricing. At the entry level, mechanical broom sweepers remain the workhorses for budget-constrained municipalities. Yet the middle ground is where the real action lies. The Taiwan Electric Sweeper Market Report forecasts a 13% CAGR from 2026 to 2033, driven by urban density and stricter emissions regulations. For procurement professionals, understanding these nuances is not optional—it is the difference between a five-year asset and a costly mistake.

Key market segments and growth drivers in the Electric Sweeper Comparison sector.

2. Market Analysis

The numbers tell a clear story. The professional street sweeper market, valued at $2.65 billion in 2026, is expected to hit $3.38 billion by 2030 at a 6.2% CAGR. Meanwhile, the compact road sweeper segment—the most relevant for commercial facilities and smaller municipalities—is projected to reach $3.055 billion by 2035, growing at a 5.16% CAGR. These figures, drawn from multiple independent reports, confirm that electric sweepers are not a niche; they are a mainstream investment category.

Three growth drivers dominate. First, urbanization: municipal corporations account for the largest end-use segment, pushing demand through sanitation mandates. Cities from Taipei to Toronto are writing electric-only procurement clauses into their street cleaning RFPs. Second, emissions regulation: diesel-powered sweepers face phase-out deadlines in Europe and parts of Asia, accelerating replacement cycles. Third, total cost of ownership: electric sweepers have 40–60% lower energy costs and significantly fewer moving parts than diesel or CNG models, making them attractive over a 7–10 year lifecycle.

The Taiwan market is a bellwether. With a 13% CAGR, it outpaces the global average by nearly 2x, reflecting both manufacturing density and aggressive green policy. Buyers should watch this region closely—not just as a source of supply, but as an indicator of where product innovation is heading. The integration of advanced telemetry and battery swapping in compact electric sweepers is being road-tested in Taipei and Kaohsiung before rolling out globally.

Market segmentation and regional distribution analysis for Electric Sweeper Comparison.

3. Product Categories

Electric sweepers fall into three primary configurations, each with distinct operational trade-offs.

Mechanical Broom Sweepers

These use rotating brushes to sweep debris into a hopper. They are the most cost-effective option, ideal for light-duty cleaning on paved surfaces. Example models include the TYMCO DST-6 and the Elgin Broom Bear. Their simplicity means lower upfront cost and easier maintenance, but they generate more dust and require frequent brush replacement. For buyers prioritizing low capital expenditure, this is the default choice.

Vacuum Sweepers

These rely on a high-velocity fan to suck debris into a collection body. They are more effective on fine particles and wet conditions than mechanical brooms. The Johnston VT651 and the Nilfisk City Ranger 2250 exemplify this category. Vacuum sweepers offer superior filtration and quieter operation, making them suitable for noise-sensitive urban environments. The trade-off is higher energy consumption and more complex mechanical systems.

Regenerative Air Sweepers

The premium tier. These machines use a recirculating air system to lift debris without brushes contacting the ground, reducing wear and extending component life. The Elgin WhirlWind and the TYMCO 500 are industry benchmarks. Regenerative air sweepers deliver the best pickup performance on fine dust and heavy debris, with the lowest operating costs per mile. They command a 20–30% price premium but offer the lowest total cost of ownership over a decade.

Compact Walk-Behind Sweepers

Ideal for sidewalks, parking garages, and indoor facilities. Examples include the Tennant 5700XP and the Nilfisk SW800, offering maneuverability in tight spaces with battery runtimes of 3–5 hours.

Ride-On Compact Sweepers

Designed for medium-duty applications like school campuses and shopping centers. The Hako Citymaster 2000 and Elgin Broom Bear EV typify this segment, balancing operator comfort with four-hour continuous operation.

Truck-Mounted Electric Sweepers

Full-size units for municipal street cleaning, such as the FAUN Viajet EV and Johnston VT651 Electric. These feature regenerative air systems, rapid charging, and hopper capacities exceeding 4 cubic yards.

4. Leading Players

The competitive landscape is shaped by a handful of established manufacturers, each pursuing a distinct electrification strategy.

Elgin Sweeper Company

A legacy player with over a century of experience, Elgin has pivoted aggressively to electric. Its WhirlWind EV, a regenerative air sweeper, targets municipalities with zero-emission mandates. Elgin’s strategy is to retain its premium positioning by bundling telematics and service contracts, making it the go-to for cities that cannot afford downtime. The company’s strength lies in its dealer network and parts availability, but its price point limits adoption among smaller buyers.

Tennant Company

Tennant focuses on compact electric sweepers for industrial and commercial facilities. Its 5700XP battery-powered sweeper is a best-seller in warehouses and distribution centers. Tennant’s competitive advantage is its ecosystem: it offers integrated floor scrubbers, sweepers, and autonomous cleaning robots, allowing facilities to standardize on one brand. This bundling strategy reduces procurement complexity and training costs, a compelling argument for multi-site operators.

Hako Group

A German manufacturer that dominates the mid-range European market. Hako’s Citymaster 2000 electric sweeper is designed for narrow streets and pedestrian zones. The company’s differentiator is modularity: customers can swap battery packs in minutes, enabling round-the-clock operation without extended charging downtime. Hako’s strategy targets municipalities with high utilization rates, where uptime is more critical than upfront price.

FAUN (Kirchhoff Group)

FAUN’s Viajet electric sweeper line is engineered for heavy-duty municipal use. The company has invested heavily in fast-charging infrastructure partnerships, offering turnkey solutions that include charging stations and depot upgrades. FAUN’s approach is to de-risk the transition for cities by providing a complete electrification package, not just a vehicle. This full-service model is gaining traction in Northern European tenders.

Legacy Premium Integrator

Elgin Sweeper Company leverages its century-old dealer network and telematics suite (FleetIQ) to command premium pricing among municipalities that prioritize uptime and parts availability over upfront cost.

Ecosystem Bundler

Tennant Company uses a multi-product ecosystem strategy, bundling sweepers with floor scrubbers and autonomous robots to reduce procurement complexity for industrial and commercial facility operators.

Modular Fast-Charge Specialist

Hako Group differentiates through hot-swappable battery packs and narrow-vehicle design, targeting European municipalities with high daily utilization rates and space-constrained streets.

5. Market Trends

1. TREND: Battery-as-a-Service (BaaS)

Instead of buying batteries outright, operators lease them on a subscription basis. This reduces upfront costs by 30–40% and shifts battery degradation risk to the provider. Hako has piloted BaaS for its Citymaster line in Germany, and early adoption data shows a 22% increase in fleet conversion rates among municipal buyers.

2. TREND: Autonomous Sweeping

LiDAR and AI navigation systems are being integrated into compact electric sweepers, enabling unmanned operation during off-peak hours. Tennant’s autonomous T7AMR floor sweeper, already deployed in logistics centers, demonstrates a 35% reduction in labor costs. For municipalities, autonomous night sweeping can cut traffic disruption and noise complaints simultaneously.

3. TREND: IoT-Driven Predictive Maintenance

Telemetry sensors now monitor brush wear, battery health, and filter status in real time. Elgin’s FleetIQ platform alerts operators before a component fails, reducing unplanned downtime by up to 50%. This trend is shifting the procurement decision from initial price to lifecycle cost, favoring manufacturers with robust software ecosystems.

4. TREND: Multi-Energy Platforms

Manufacturers are designing chassis that can accept diesel, electric, or hydrogen fuel cell powertrains on the same platform. FAUN’s modular Viajet series allows municipalities to standardize on one vehicle type while transitioning powertrains over a decade. This reduces fleet complexity and training costs, a critical factor for budget-constrained cities.

6. Regional Markets

Asia-Pacific (13% CAGR Hotspot)

Taiwan leads with the fastest electric sweeper adoption rate, driven by dense urban corridors and aggressive government electrification targets; local manufacturers are scaling production to serve both domestic and export markets.

Europe (Stringent Emissions Regulation)

EU Stage V emissions standards and low-emission zones in cities like London and Paris are forcing municipalities to replace diesel sweepers with electric alternatives, creating a stable replacement cycle through 2035.

North America (Industrial Dominance)

The U.S. market is driven by warehouse and logistics center expansion, with Tennant and Nilfisk competing on battery runtime and autonomous features rather than municipal policy mandates.

7. Investment Outlook

Two opportunities stand out. First, the municipal RFP wave: as cities in Southeast Asia and Latin America electrify their fleets, compact electric sweeper demand will spike. Suppliers that offer turnkey charging and maintenance packages will capture disproportionate share. Second, the industrial facility segment: warehouses and distribution centers are expanding rapidly, and electric sweepers offer a zero-emission solution that meets both ESG targets and indoor air quality standards. Expect Tennant and Hako to intensify competition in this space.

The primary risk is battery raw material volatility. Lithium, cobalt, and nickel price swings directly impact sweeper pricing, and manufacturers have limited ability to pass through costs in competitive tenders. Buyers should negotiate long-term service agreements with price escalation caps to hedge against battery cost inflation. The smart procurement strategy for 2026 is to lock in partnerships with manufacturers that have diversified battery supply chains and proven battery-as-a-service models.

Strategic Considerations:

- Municipal Electrification RFPs: Buyers should target cities in Southeast Asia and Latin America that are issuing electric-only street cleaning tenders; early partnerships with local service providers will secure multi-year contracts.

- Industrial Facility Expansion: Warehouse and distribution center growth in North America and Europe creates demand for compact electric sweepers that meet indoor air quality and ESG targets without requiring infrastructure upgrades.

- Battery Raw Material Volatility: Lithium and cobalt price swings can increase sweeper costs by 15–20% within a contract period; negotiate long-term service agreements with price escalation caps tied to commodity indices.

- Charging Infrastructure Gaps: Municipal depot upgrades for fast charging can add 6–12 months to deployment timelines; buyers should verify that manufacturers offer turnkey charging solutions before signing fleet contracts.

Make Informed Decisions in the Electric Sweeper Comparison Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-28. All market figures are estimates and may vary from actual results.