Table of Contents

The global Eye Protection Safety Goggles sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Every 15 seconds, a worker in the United States suffers a preventable eye injury, resulting in nearly $300 million in lost productivity and medical costs annually. Against this backdrop, the global protective goggles market is estimated to reach USD 680.7 million by 2026, climbing to USD 982.2 million by 2033. These figures underscore a critical shift: eye protection safety goggles are no longer a simple compliance afterthought—they are a strategic investment in workforce productivity and liability reduction.

Industry Scope & Characteristics

Advanced Lens Materials

Polycarbonate dominates due to its high impact resistance (10x that of glass) and low weight. Some premium models use Trivex, which offers superior optical clarity and scratch resistance.

Stringent Certification Requirements

Goggles must meet ANSI Z87.1-2020 (US) or EN 166 (Europe) for impact, splash, and optical performance. Compliance requires batch testing and documented traceability.

Customization for Prescription Lenses

Many manufacturers offer prescription inserts or direct molded lenses to accommodate worker vision needs. UVEX and Bollé provide certified prescription safety goggles for industrial use.

Rise of Anti-Fog Technology

Fogging is the leading cause of non-compliance; modern permanent anti-fog coatings (e.g., hydrophilic polymers) are becoming standard in higher-end models, significantly improving safety adherence.

Within the broader Protective & Technical Textiles industry, eye protection safety goggles occupy a unique space. Unlike fire-resistant clothing or anti-static fabrics, goggles must simultaneously meet optical clarity standards, impact resistance, and often chemical splash protection. The category sits at the intersection of materials science and ergonomics, where innovations in polycarbonate and anti-fog coatings directly influence user compliance.

Distinctively, the market is bifurcated between industrial heavy-duty goggles—used in manufacturing, construction, and chemical processing—and specialty goggles designed for laboratories, healthcare, and sports. The medical protective goggles segment alone is projected to grow at an 8–9% compound annual rate through 2031, driven by heightened infection control awareness post-pandemic.

What sets this sub-topic apart within technical textiles is the rapid adoption of advanced lens treatments. Anti-scratch, anti-fog, and UV-blocking layers are now standard, while emerging smart goggles with augmented reality overlays hint at a future where eye protection becomes a data interface. For B2B buyers, the challenge is no longer just finding a compliant supplier but verifying that the product meets evolving ANSI Z87.1 and EN 166 standards across different use cases.

Key market segments and growth drivers in the Eye Protection Safety Goggles sector.

2. Market Analysis

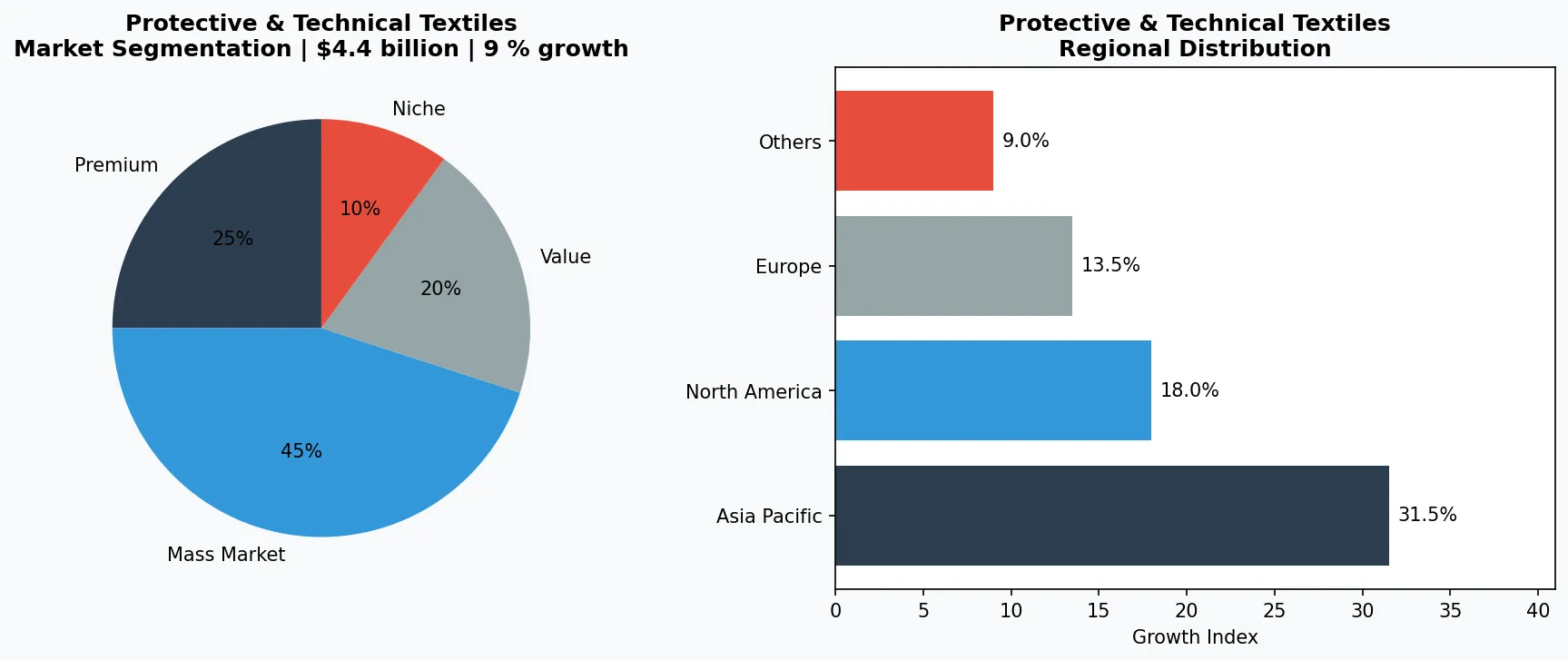

The global safety eyewear market was valued at $4.4 billion in 2025 and is projected to grow from $4.6 billion in 2026 to $5.8 billion by 2033, at a CAGR of 3.3%. Within this, the narrow segment of protective goggles—which excludes safety glasses and face shields—is estimated at USD 680.7 million in 2026, expanding to USD 982.2 million by 2033. That implies a significantly higher CAGR of approximately 5.4%, aligning with the projected growth rate for eye protection in manufacturing reported by Key & Kinesis.

Three major growth drivers are fueling this acceleration. First, the global manufacturing sector is rebounding with increased automation and higher production volumes. As factories adopt leaner, faster workflows, the risk of flying debris and chemical splashes rises, directly boosting demand for robust goggles. Second, the healthcare segment remains a powerhouse: the medical protective goggles market is expected to witness an 8–9% growth rate by 2031, driven by stricter infection prevention protocols and an aging population requiring more surgical procedures. Third, regulatory tightening in emerging economies—particularly in Asia Pacific—is mandating eye protection in industries previously underregulated.

Geographically, North America currently leads in market share due to stringent OSHA enforcement, but Asia Pacific is the fastest-growing region. Countries like China, India, and Vietnam are ramping up manufacturing capacity, and local governments are adopting international safety standards. The online distribution channel for goggles is also expanding rapidly, growing at an estimated 6% per year, as B2B procurement moves toward e-commerce platforms that simplify compliance verification.

However, the market is not without headwinds. The global eye and face protection market, which includes goggles, was sized at $711.3 million in 2024 and is forecast to reach $1,973.6 million by 2034 at a 5.9% CAGR. The price sensitivity of commoditized goggles versus value-added premium products creates a bifurcation: bulk buyers often prioritize cost, while specialized users (e.g., labs, pharmaceuticals) pay a premium for certification and comfort. This tension will define competitive strategies through 2033.

Market segmentation and regional distribution analysis for Eye Protection Safety Goggles.

3. Product Categories

Polycarbonate Impact-Resistant Goggles

The backbone of the industrial safety market. Polycarbonate lenses offer 10 times the impact resistance of glass or standard plastic while being 30% lighter. Typical examples include direct-vent goggles for dust protection and indirect-vent models for chemical splash resistance. Most comply with ANSI Z87.1-2020 high-impact standards and are often paired with anti-fog coatings. Major manufacturers like 3M and Honeywell produce variants that withstand up to 150 feet per second impact.

Anti-Fog and Anti-Scratch Coated Goggles

Fogging remains the top compliance barrier; workers remove goggles when visibility degrades. Modern anti-fog technologies use hydrophilic coatings that absorb moisture, keeping lenses clear for hours. Anti-scratch hard coats extend product life. Examples include UVEX's anti-fog series with permanent coating, and Bollé's Cloud9 range designed for humid environments. These premium goggles typically cost 30–50% more but reduce replacement frequency and improve safety adherence.

Specialty Goggles for Medical and Lab Use

Medical protective goggles require seamless fit with respirators and face shields, plus compliance with FDA 21 CFR 801 for splash protection. They often feature foam-lined frames for comfort and indirect vents to prevent fluid ingress. The segment is growing 8–9% annually. Products like the Honeywell Uvex Skyper and 3M GoggleGear 500 series exemplify the convergence of comfort and sterility. Laser safety goggles, another specialty, use specific optical density filters and are ANSI Z136.1 certified for wavelengths from 190 nm to 11 µm.

Smart Goggles with Augmented Reality

An emerging sub-category, these integrate heads-up displays (HUDs) for real-time data, instructions, or remote assistance. Companies like RealWear and Daqri have pioneered these devices for manufacturing and field service, though they remain a small fraction of the total market. The primary challenge is balancing weight, battery life, and impact resistance while maintaining ANSI compliance. As costs drop, smart goggles could disrupt the market in the next three to five years.

Basic Impact-Resistant Goggles

Designed for general manufacturing and construction, these goggles feature polycarbonate lenses, either direct vent (for dust) or indirect vent (for splash). Examples include 3M GoggleGear 500 and Honeywell Uvex Stealth.

Anti-Fog and Anti-Scratch Goggles

Enhanced with dual-layer coatings to maintain clear vision in humid or high-exertion environments. Common in food processing, chemical plants, and healthcare. Products like Bollé Cloud9 and Uvex Hypersonic are leaders.

Specialty Goggles for Medical and Lab Use

Medical goggles feature fluid splash seals, anti-microbial frame materials, and compatibility with respirators. Laboratory variants include chemical splash protection and laser-specific optical density filters.

4. Leading Players

3M – The Diversified Safety Giant

With a product portfolio spanning respiratory, hearing, and eye protection, 3M leverages its cross-selling and distribution network to dominate industrial eyewear. Its strategy emphasizes technological innovation, particularly in anti-fog coatings (e.g., 3M's Scotchgard antifog technology) and comfort features like adjustable headbands. 3M holds a significant share in the protective goggles market by integrating proprietary materials like polycarbonate blends that meet both ANSI and CE standards. The company's annual safety segment revenue exceeds $8 billion, with goggles contributing a meaningful portion.

Honeywell – The Industrial Integrator

Honeywell's Industrial Safety division, which includes brands like Uvex (acquired in 2012), focuses on comprehensive worker safety solutions. Uvex's product lines—such as the Uvex Stealth and Uvex Skyper—are known for ergonomic designs and compliance with multiple global standards. Honeywell's competitive edge lies in its software and services: it offers compliance management tools that help B2B buyers track goggle replacement cycles and training. With a strong presence in the medical and manufacturing segments, Honeywell is positioned to capture the 8–9% growth in medical goggles.

UVEX – The Specialist with German Engineering

UVEX (now part of Honeywell) originally built its reputation on precision optical technology, including prescription safety goggles. Its strategy targets users who need customized solutions: tinted lenses for welding, blue-light filtering for lab work, or high-heat resistance for foundries. UVEX goggles are frequently specified in European automotive and pharmaceutical plants due to their compliance with EN 166 and their optical class 1 quality. The brand exemplifies how niche specialization can command premium pricing in a commodity-driven market.

Bollé Safety – The French Innovator

Bollé Safety differentiates through design and sustainability. Its 'B-Wings' line features lightweight construction and half-frame designs that reduce pressure points. The company has also introduced a circular economy program for recycling used goggles. While smaller than 3M and Honeywell, Bollé's focus on user experience—wider field of view, quick-release buckles—makes it a preferred choice for long-shift environments. The company has grown its market share by 2–3% annually, particularly in Europe and the Middle East.

Diversified Industrial Conglomerate (3M)

Leverages cross-category safety portfolio and R&D scale to innovate coatings and comfort features. Strong distribution network and brand trust make 3M a top choice for large manufacturing accounts.

Safety Specialist with Integrated Software (Honeywell/Uvex)

Combines high-quality goggles with compliance management tools, offering B2B buyers a total solution. Strong in medical and European industrial markets due to Uvex's reputation for German engineering.

Niche Innovator in Sustainability and Design (Bollé Safety)

Differentiates through ergonomic design and circular economy programs. Appeals to ESG-conscious buyers and markets in Europe and the Middle East.

5. Market Trends

1. ADVANCED ANTI-FOG AND ANTI-SCRATCH NANOCATINGS

Fogging is the #1 reason workers remove goggles, directly contributing to eye injuries. New dual-layer nanocoatings—applied via plasma or dip-coating processes—eliminate fog for up to 8 hours while resisting scratches 3x longer than standard coatings. 3M has commercialized this technology in its GoggleGear line, reducing downtime from cleaning and increasing compliance.

2. INTEGRATION OF INTELLECTUAL PROPERTY FROM MEDICAL GOGGLES INTO INDUSTRIAL

The medical protective goggles segment (8-9% CAGR) has driven innovations in foam sealing, anti-microbial materials, and ergonomic fit. These features are now migrating into general industrial goggles. Honeywell's Uvex Hypersonic series borrows medical-grade foam to create a tight seal against dust and chemicals, reducing eye irritation and improving wear time.

3. SUSTAINABLE MATERIALS AND CIRCULAR ECONOMY MODELS

With corporate ESG goals tightening, manufacturers are exploring bio-based acetates and recycled polycarbonate for frames and lenses. Bollé Safety offers a take-back program where used goggles are shredded and remolded into new frames. This trend is both a market differentiator and a response to EU regulations on single-use plastics, which are increasingly applied to personal protective equipment.

4. SMART GOGGLES AND AUGMENTED REALITY ASSISTANCE

Though still early-stage, smart goggles with integrated displays for instructions or remote expert guidance are gaining traction in complex assembly and maintenance tasks. Companies like RealWear have launched ruggedized smart goggles compliant with ANSI Z87.1, enabling hands-free data access. The market for industrial smart eyewear is projected to grow at over 20% annually through 2030, albeit from a small base.

6. Regional Markets

North America – Regulatory-Driven Market

Strict OSHA enforcement and high safety consciousness drive demand for premium, ANSI-compliant goggles. Replacement cycles are shorter (2–3 years) due to frequent audits.

Asia Pacific – Fastest Growth Hub

Rapid industrialization in China, India, and Vietnam, combined with newly mandated safety standards, is expanding the addressable market. Price sensitivity remains high, but demand for certified products is rising.

Europe – Quality and Sustainability Focus

Stringent EN 166 standards and EU chemical regulations (REACH) favor high-quality, eco-friendly products. Manufacturers investing in recycled materials and take-back programs gain competitive advantage.

7. Investment Outlook

Two specific opportunities stand out for B2B buyers in the eye protection safety goggles market. First, the healthcare segment's consistent 8–9% CAGR offers a stable, high-margin avenue for suppliers who can certify their goggles for fluid splash and particulate filtration. Partnering with hospital group purchasing organizations (GPOs) could lock in multi-year contracts. Second, the shift to online procurement—accelerated by platforms like VerityRank—enables buyers to compare verified suppliers across certifications and price points, reducing sourcing risk and lead times.

On the risk side, the market faces potential raw material volatility. Polycarbonate, the dominant material for lenses, is derived from bisphenol A (BPA), and supply chain disruptions or price spikes could squeeze margins. Additionally, counterfeiting remains a concern: non-certified goggles with fake ANSI labels have been found in Asian markets, exposing buyers to liability. Verification services are critical to mitigate this. Actionable advice: prioritize suppliers who demonstrate third-party lab reports for each production batch and maintain updated certifications on their VerityRank profile.

Strategic Considerations:

- Healthcare Expansion Opportunity: The medical protective goggles segment growing at 8-9% CAGR offers a stable, high-margin avenue; suppliers certifying for FDA/CE splash protection can secure GPO contracts.

- Smart Goggles Potential: Augmented reality goggles for industrial use are forecast to grow 20%+ annually; early movers integrating HUDs with ANSI compliance will lead in advanced manufacturing sectors.

- Risk of Polycarbonate Price Volatility: Polycarbonate raw material costs are tied to oil prices and BPA regulations; buyers should diversify sources and consider alternative lens materials like Trivex.

- Counterfeit Certification Risk: Fake ANSI/CE labels on low-cost imports expose buyers to liability; verification through third-party platforms like VerityRank is essential for procurement due diligence.

Frequently Asked Questions

Make Informed Decisions in the Eye Protection Safety Goggles Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-15. All market figures are estimates and may vary from actual results.