Table of Contents

The global Fashion Accessories industry serves consumers worldwide with diverse solutions.

1. Industry Overview

The global fashion accessories market, valued at USD 1878.85 billion in 2025, is on a trajectory that would have seemed implausible a decade ago. By 2030, the industry is projected to reach USD 3.85 trillion, representing a compound annual growth rate of 4.62% over that five-year span. Yet this headline figure conceals a more complex reality: McKinsey's analysis projects that the broader fashion industry will post only low single-digit growth through 2026, suggesting that accessories are carving out an outsized role as the sector's primary engine of expansion. Fashion accessories—including watches, sunglasses, jewelry, scarves, belts, and hair adornments—have transitioned from being considered complementary purchases to standing as independent drivers of consumer spending and brand loyalty. This shift is reshaping supply chains, retail strategies, and the competitive landscape in ways that every B2B buyer and supplier must understand. The convergence of technological innovation, sustainability mandates, and a new generation of style-conscious consumers is rewriting the rules of an industry that touches virtually every economy on the planet.

Industry Scope & Characteristics

Broad Product Portfolio

Products span watches, sunglasses, jewelry, ties, scarves, gloves, hats, belts, hair accessories, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

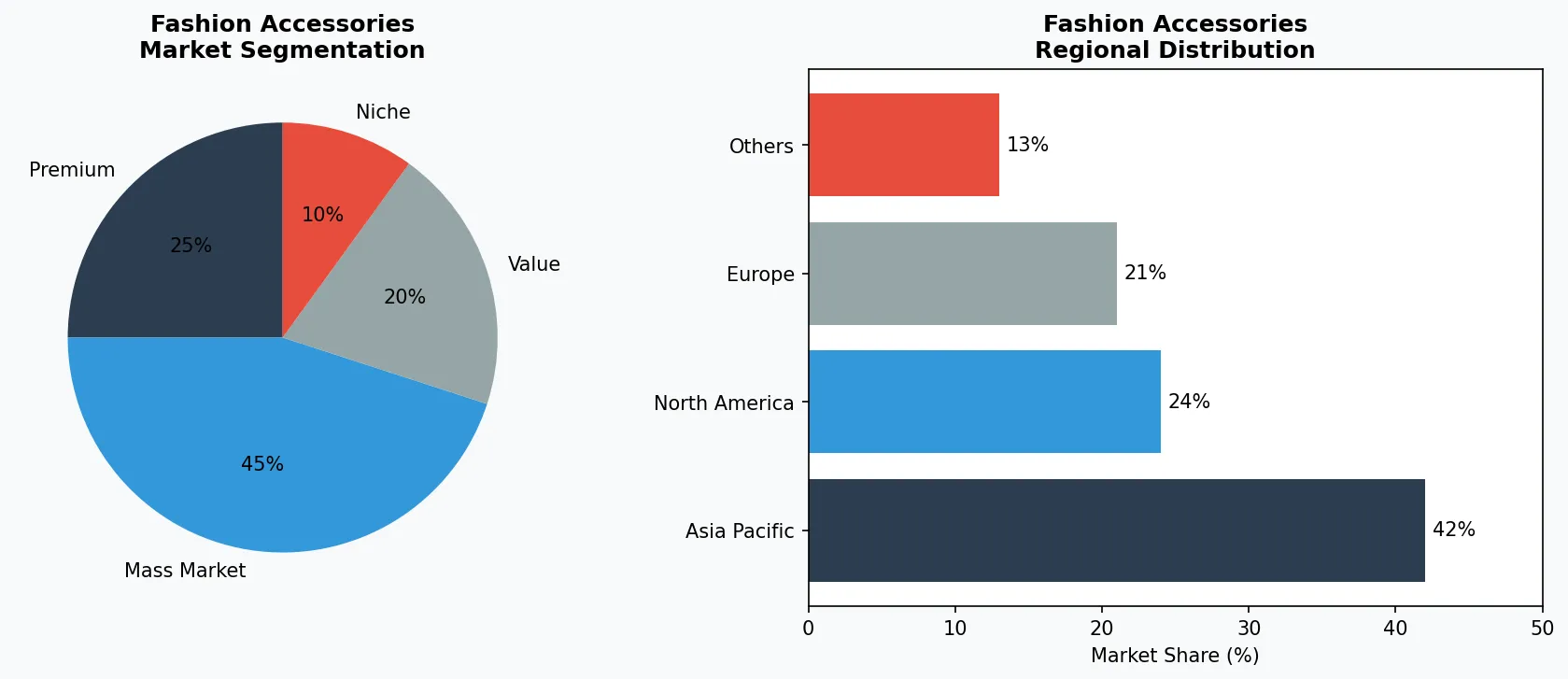

Key market segments and growth drivers in the Fashion Accessories sector.

2. Market Analysis

The Fashion Accessories Market, worth USD 3.07 trillion in 2025, is growing at a CAGR of 4.62% and is expected to reach USD 3.85 trillion by 2030. That growth masks an accelerating trajectory: a separate analysis projects a remarkable CAGR of 15% from 2026 to 2033, indicating that the market's expansion is set to intensify significantly over the coming decade. Three forces are driving this surge. First, smart wearables have moved decisively from niche to mainstream—the integration of technology into watches, sunglasses, and even jewelry is creating an entirely new product category that commands premium pricing and drives repeat purchases. Second, the demand for colorful, expressive accessories is surging among Gen Z and millennial consumers who treat accessories as primary style statements rather than afterthoughts. Third, the rise of local designers and independent brands across both developed and emerging markets is fragmenting the competitive landscape and creating new sourcing opportunities for B2B partners. Geographically, Asia-Pacific is the single most critical region for growth, driven by expanding middle-class consumer bases in China, India, and Southeast Asia. North America remains the world's most profitable mature market, where premium and luxury accessories command consistent margins. Europe, led by fashion capitals in France, Italy, and the United Kingdom, continues to set global aesthetic trends that ripple through every other regional market.

Market segmentation and regional distribution analysis for Fashion Accessories.

3. Product Categories

Watches and timepieces represent the highest-value segment of the fashion accessories market, blending heritage craftsmanship with technological innovation. Swiss watchmakers like Tissot anchor the premium end of the spectrum, while brands like Fossil and Casio compete aggressively in the mid-market and smart wearables space respectively, targeting consumers who want functional technology wrapped in accessible design. Sunglasses form a distinct sub-category where brand heritage and UV-protection technology converge. Ray-Ban remains the defining brand in this space, with its Wayfarer and Aviator silhouettes maintaining cultural relevance across multiple decades—a testament to the enduring commercial value of iconic design in accessories. Jewelry and fine adornments, including offerings from Swarovski and Michael Kors, occupy the largest volume segment by consumer count. Swarovski's strategy of blending crystal craftsmanship with accessible luxury pricing has made it a staple of both gifting occasions and everyday self-purchase markets globally. Emerging sub-categories gaining traction include hair accessories—clips, scarves, and headbands driven by social media fashion cycles—and sustainable belts and bags made from alternative materials, signaling a broadening of what consumers consider a fashion accessory in 2025 and beyond.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

Casio has executed a remarkable pivot in the wearables category, moving decisively beyond its legacy in affordable digital watches to position itself as a serious contender in the smart wearables segment. The company's G-SHOCK line, long associated with rugged durability, now incorporates fitness tracking, connectivity features, and co-branded collaborations with fashion designers—a strategy that widens its addressable market from sports enthusiasts to style-conscious consumers. Casio's approach illustrates a broader industry truth: in 2026, the boundary between a watch and a wearable device is dissolving, and companies that fail to bridge that gap risk irrelevance in the eyes of younger consumers. Ray-Ban, under the EssilorLuxottica umbrella, has taken a different path—leaning into cultural authority and brand nostalgia rather than technology. The brand's 2024-2025 strategy centered on expanding its Stories smart glasses line while simultaneously doubling down on its classic non-smart frames as collector and resale items. This dual-track approach captures both the tech-curious early adopter and the traditionalist consumer, demonstrating how dominant brands can hedge category risk. Swarovski has pursued aggressive brand repositioning under new creative leadership, elevating its crystal jewelry collections with higher-end materials and limited-edition capsule releases. By introducing more premium product tiers, Swarovski aims to compete directly with fine jewelry houses while retaining its accessibility advantage—a calculated move to capture wallet share across income brackets in uncertain economic conditions. Fossil Group operates on a different strategic logic: portfolio diversification. The company manages multiple accessory brands spanning watches, leather goods, and wearables, using scale and brand variety to spread commercial risk across consumer segments and retail channels. Fossil's partnership with Google to develop Wear OS-powered hybrid smartwatches positions it as a technology integrator rather than a pure fashion brand—a model that other mid-market players are watching closely as a template for survival in a consolidating industry.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the fashion accessories space.

5. Market Trends & Innovations

1. Sustainability & Eco-Friendly Innovation

Sustainability has become a core competitive priority. Companies like LVMH and Kering are investing in eco-friendly materials, carbon-neutral production, and circular economy initiatives to meet growing consumer demand for responsible products.

2. Digital Transformation & E-Commerce Growth

The shift to digital sales channels continues to accelerate. Richemont and Michael Kors (Capri Holdings) are leveraging data analytics, AI-driven personalization, and omnichannel strategies to enhance customer engagement and streamline distribution.

3. Premiumization & Product Innovation

Rising consumer expectations are driving premiumization across the market. Ralph Lauren has introduced high-end product lines, while Hermès focuses on innovative features and superior quality to capture value-conscious yet quality-seeking customers.

4. Health, Wellness & Functional Benefits

Health-oriented consumer preferences are reshaping product development. Chanel and Prada are pioneering functional products with demonstrable benefits, commanding premium pricing and driving category expansion.

6. Regional Markets

Asia-Pacific is the defining growth geography for fashion accessories in 2026, accounting for the largest share of new consumer demand entering the market. China's fashion accessories market has matured beyond imitation brands toward domestically designed and manufactured products, with local brands like Peacebird and Exception winning shelf space from international competitors. India represents perhaps the most untapped opportunity: a population of over 1.4 billion with a rapidly expanding middle class, rising female labor participation rates driving accessory purchase power, and a government actively supporting domestic manufacturing through production-linked incentive schemes. Southeast Asian markets including Vietnam, Indonesia, and the Philippines are emerging as both manufacturing hubs and consumer markets, creating dual opportunities for B2B sourcing strategies. North America remains the world's highest-margin fashion accessories market, where consumers spent lavishly on premium and luxury goods throughout 2024-2025 despite broader economic uncertainty. The United States in particular demonstrates strong demand for smart wearables and technology-integrated accessories, with fitness culture and health consciousness driving continuous upgrade cycles. American consumers also lead globally in personalized and experience-driven accessory purchases—engraving services, customization boutiques, and subscription-based accessory boxes are more developed in the US market than anywhere else. European markets are characterized by strong brand loyalty and a deep-rooted appreciation for craftsmanship heritage. The United Kingdom, France, and Italy serve as both consumption markets and trend-setting engines, with Paris Fashion Week and Milan Fashion Week accessory showcases setting the aesthetic agenda that flows downstream to mass-market retailers globally. Germany and the Nordic countries represent a distinct sub-market where sustainability credentials are non-negotiable—accessories must demonstrate environmental and ethical compliance to access these discerning consumers, making supply chain transparency a prerequisite for market entry rather than a competitive advantage.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities stand out for B2B buyers and suppliers navigating the fashion accessories market in 2026 and beyond. First, smart wearable components and integration services represent a high-growth procurement category: as more traditional accessory brands move to incorporate technology, demand is rising for sensors, display modules, connectivity hardware, and the design expertise to package these components within fashion-forward product shells. Companies that can supply technology integration services alongside physical accessory components will command premium margins in this expanding supply chain tier. Second, sustainable and ethically certified materials—recycled metals, lab-grown gemstones, plant-based leathers, and bio-based polymers—present a sourcing opportunity that aligns with both consumer demand and incoming regulatory requirements in the European Union and United States. Second-hand and circular economy models for fashion accessories are also creating new B2B service categories around authentication, refurbishment, and certified resale. The primary concrete risk is regulatory and trade policy volatility. The fashion accessories supply chain spans multiple continents, and 2026 brings significant uncertainty around tariffs, customs regulations, and sustainability reporting mandates—particularly for products manufactured in China and Southeast Asia for Western markets. Buyers who have not diversified their supplier base across geographies, or who lack robust compliance documentation for materials sourcing, face both logistical disruption and potential regulatory penalties that could erode margins sharply. Companies that invest now in supply chain transparency infrastructure and multi-source procurement strategies will be far better positioned to absorb policy shocks than those relying on consolidated, single-region manufacturing relationships.

Strategic Considerations:

- ('Technology & AI Integration:', 'Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.')

- ('Sustainability as Business Strategy:', 'Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.')

- ('Transparency & Traceability:', 'Consumers demand increasingly granular information about product origins, ingredients, and production methods.')

- ('Emerging Market Penetration:', 'Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.')

Make Informed Decisions in the Fashion Accessories Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-14. All market figures are estimates and may vary from actual results.