Table of Contents

The global Food Preservatives Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2026, nearly one-third of all food produced globally will require some form of preservation to reach consumers safely — yet the very chemicals that prevent spoilage are under intense scrutiny. The global food preservatives market, valued at roughly $3.81 billion in 2026, is expected to climb to $5.32 billion by 2033, according to the latest industry forecasts. This is not a static category. It is a battleground where consumer demand for clean labels collides with the undeniable science of shelf-life extension.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Food Preservatives Guide, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

A food preservative is any substance added to food to slow microbial growth, oxidation, or enzymatic decay. While the overarching food additives industry spans colorings, emulsifiers, sweeteners, and more, preservatives occupy a unique position: they are both essential for safety and increasingly targeted by clean-label movements. The sub-topic 'food preservatives guide' therefore serves as a critical reference for B2B buyers — from procurement managers at dairy plants to R&D teams at beverage startups — who must navigate a landscape where natural alternatives are surging but synthetic stalwarts still dominate cost-sensitive applications.

What sets preservatives apart within the broader additives market is the dual pressure of regulation and perception. In 2025, the EU revised its approval process for food enzymes and preservatives, while the U.S. FDA continued to reassess GRAS (Generally Recognized as Safe) designations. Meanwhile, a 2024 survey by Innova Market Insights found that 67% of global consumers check for preservatives on labels before buying processed foods. This tension creates both risk and opportunity: risk for legacy players tied to synthetic compounds, and opportunity for suppliers innovating with rosemary extract, citrus-based solutions, and fermentation-derived antimicrobials. The 2026 guide is, at its core, a navigation tool for this high-stakes environment.

Key market segments and growth drivers in the Food Preservatives Guide sector.

2. Market Analysis

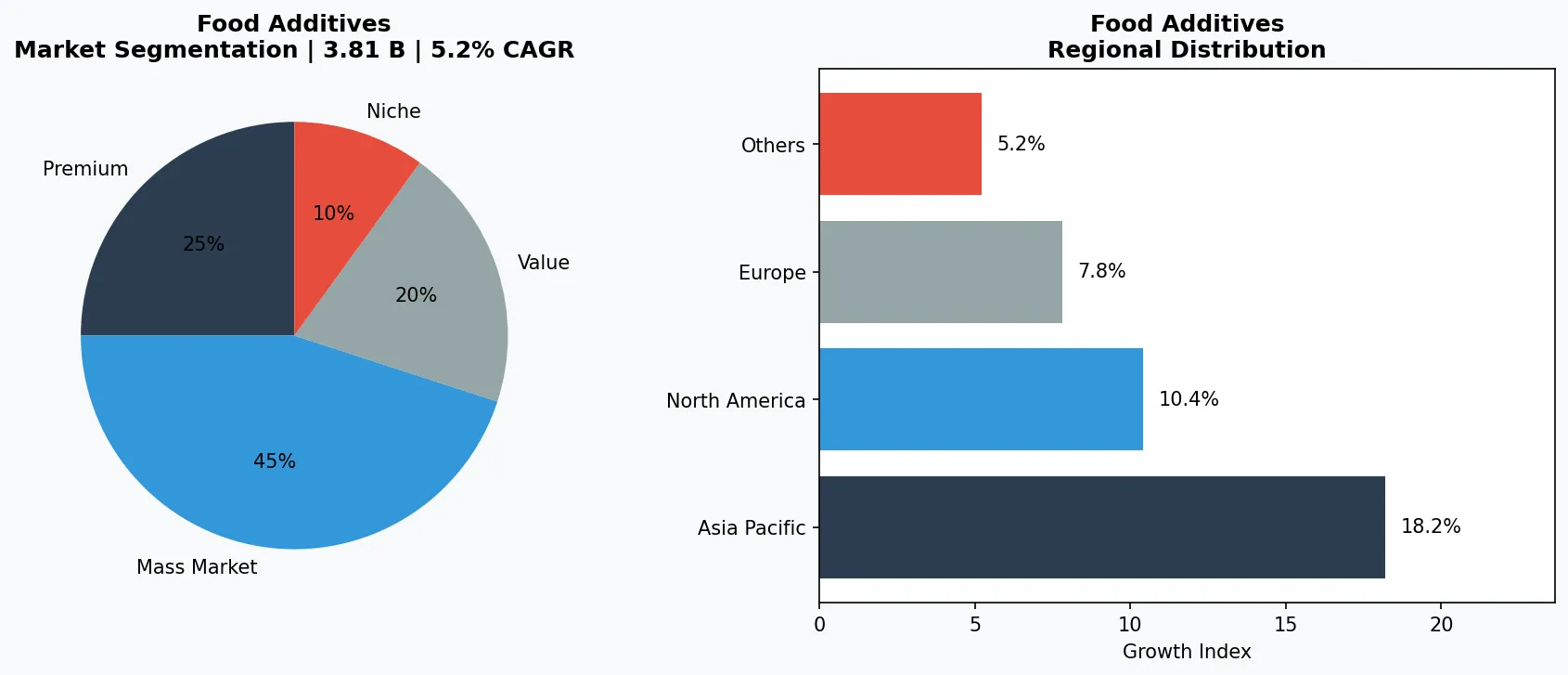

The food preservatives market is anything but uniform in its growth projections, a sign of how fragmented and dynamic the space has become. Multiple 2025–2026 reports converge on a central theme: steady expansion. One estimate pegs the market at $3.63 billion in 2025, rising to $3.81 billion in 2026 and forecast to reach $4.87 billion by a later benchmark. Another research firm projects the market at $3.21 billion in 2026 and $3.92 billion by 2030, representing a 5.2% CAGR. Yet another source, using a broader scope, values the market at $8.02 billion in 2025 with a 7.47% CAGR through 2033, and a separate analysis predicts $5.18 billion by 2034 at 5.07% CAGR. The variance reflects differences in segmentation — some reports include only antimicrobials and antioxidants, while others incorporate acidulants, curing agents, and natural extracts. Regardless, the directional trend is clear: demand is growing faster than overall food production, driven by rising consumption of processed and packaged foods in Asia-Pacific and Latin America.

Three factors are accelerating growth. First, the global push to reduce food waste: the UN estimates that 14% of food is lost between harvest and retail, and preservatives are one of the most cost-effective interventions. Second, the expansion of plant-based proteins and dairy alternatives — products that often require enhanced preservation due to higher water activity and pH levels. For instance, oat milk and almond milk typically need potassium sorbate or natamycin to prevent mold growth. Third, the clean-label pivot itself has become a growth driver: as manufacturers switch from synthetic to natural preservatives, they often need to use higher concentrations or multi-ingredient systems, increasing per-unit cost and total market value. By function, antimicrobials capture the largest share (over 55% of revenue in 2025), followed by antioxidants. By application, dairy and beverages together account for nearly 40% of preservative consumption, with meat and poultry close behind.

Market segmentation and regional distribution analysis for Food Preservatives Guide.

3. Product Categories

The preservatives landscape breaks into four dominant categories: **antimicrobials**, **antioxidants**, **acidulants**, and **curing agents**.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

**Antimicrobials** target bacteria, yeasts, and molds. Synthetic workhorses include sodium benzoate (E211), used widely in acidic beverages, and potassium sorbate (E202), favored in dairy, baked goods, and wine. Natural antimicrobials are the fastest-growing segment: nisin (a bacteriocin derived from Lactococcus lactis) is now used in over 30 countries for cheese and canned foods, and natamycin (produced by Streptomyces) prevents fungal growth on sausages and yogurt.

**Antioxidants** prevent rancidity by inhibiting lipid oxidation. Synthetic options like BHA (butylated hydroxyanisole) and BHT (butylated hydroxytoluene) remain cost-effective for snack chips and cereals, but clean-label shifts have boosted demand for tocopherols (vitamin E), rosemary extract (carnosic acid), and ascorbic acid (vitamin C). In 2026, rosemary extract alone is projected to account for 18% of the natural antioxidant market.

**Acidulants** such as citric acid, lactic acid, and acetic acid lower pH to inhibit microbial growth. They double as flavor enhancers and are essential in pickles, sauces, and dressings. Citric acid, produced fermentatively by Cargill and Jungbunzlauer, remains the most widely used acidulant due to its low cost and versatility. **Curing agents** — including sodium nitrite and potassium nitrate — are specific to processed meats, providing color and Clostridium botulinum protection. Though under pressure from health-conscious consumers, nitrites are irreplaceable in products like bacon and salami, with no equivalent natural alternative currently scalable.

4. Leading Players

**Cargill** leverages its vast agricultural supply chain to offer both synthetic and natural preservatives. The company’s 2025 launch of a fermented-derived citric acid line (using non-GMO sugar feedstock) directly targets clean-label buyers in the beverage industry. Cargill also manufactures potassium sorbate from its plant in Iowa, giving it dual positioning in cost and sustainability.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the food additives space.

**International Flavors & Fragrances (IFF)** — formed from the merger of DuPont Nutrition & Biosciences and IFF — commands a leading portfolio of *DuPont Danisco* brand preservatives including nisin, natamycin, and the *Guardian* line for dairy and meat. IFF’s strategy focuses on 'protective cultures' that naturally outcompete pathogens, a value-add that commands premium pricing. In 2024, IFF opened a new R&D center in Shanghai dedicated to fermented preservatives for the Asian market.

**BASF** takes a high-tech approach with synthetic antioxidants like Irganox (for food contact materials) and liquid blends that improve dosage accuracy. The German chemical giant is investing heavily in microencapsulation technology to mask the taste of bitter natural preservatives, a pain point that has limited adoption of rosemary extract in neutral-flavored products. BASF’s 2026 pipeline includes a spray-dried ascorbic acid variant for dry beverage mixes.

**Kerry Group** positions itself as the clean-label champion, offering a 'Taste & Nutrition' platform that integrates preservatives with flavor systems. Its *Accel* range combines antioxidants and antimicrobials in single blends designed for plant-based meats. Kerry acquired Biosearch Life in 2022 to gain access to marine-derived preservatives (chitosan from shellfish), though the company is now exploring fungal alternatives to avoid allergen issues. These four players collectively control an estimated 45% of the global preservatives market, with the remainder fragmented among regional producers.

5. Market Trends

1. **CLEAN-LABEL PRESERVATIVES

**CLEAN-LABEL PRESERVATIVES — ** Consumers increasingly reject chemical-sounding ingredients, driving formulators toward 'clean-label' preservatives that are recognizable and minimally processed. Examples include vinegar, salt, sugar, and cultured dextrose (fermented corn sugar). In 2025, Kraft Heinz reformulated its classic mayonnaise to replace EDTA with citric acid and rosemary extract, citing consumer feedback. This trend is raising R&D costs but also margins, as natural preservatives typically cost 2–3x more than synthetic equivalents.

2. **FERMENTATION-DERIVED ANTIMICROBIALS

**FERMENTATION-DERIVED ANTIMICROBIALS — ** Biotechnology is enabling the production of potent, natural antimicrobials via precision fermentation. Nisin and natamycin are well-established, but newer entrants like fermentate from *Propionibacterium freudenreichii* are gaining traction in bakery and dairy. Corbion launched a 'clean-label mold inhibitor' in 2024 derived from lactic acid fermentation, which it claims extends shelf life of tortillas by 14 days. This trend reduces reliance on crop-based extracts and offers consistent potency batch to batch.

3. **SMART PACKAGING INTEGRATION

**SMART PACKAGING INTEGRATION — ** Rather than adding preservatives directly into food, some manufacturers are incorporating them into packaging films and labels. Active packaging releases antimicrobial agents (e.g., silver nanoparticles, essential oils) over time. In 2025, Sealed Air (Cryovac) introduced a sachet-based system using rosemary extract for fresh meat, reducing the amount needed by 40% while achieving equivalent shelf life. This segment is growing at 12% CAGR, but regulatory hurdles around direct food contact remain a barrier.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

The most immediate opportunity lies in **natural preservative blends tailored for plant-based proteins**. As the alt-protein market grows at 14% annually, suppliers who can develop cost-effective, clean-label solutions for high-moisture meat analogs will capture a first-mover advantage. A second opportunity is **regional expansion in Southeast Asia and Africa**, where rising incomes are boosting processed food consumption but local regulatory frameworks are still evolving — allowing early entrants to shape standards.

The primary risk is **regulatory fragmentation**. In 2026, the EU is expected to finalize a ban on titanium dioxide (E171), and similar re-evaluations of potassium sorbate and sodium nitrite are underway. Companies relying on a single preservative type face sudden market access loss if their product is delisted. Diversification across natural and synthetic portfolios, combined with continuous monitoring of Codex Alimentarius updates, will be essential for long-term resilience.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Food Preservatives Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-29. All market figures are estimates and may vary from actual results.