Table of Contents

The global Gloves Winter Summer Types sector serves consumers worldwide with diverse solutions.

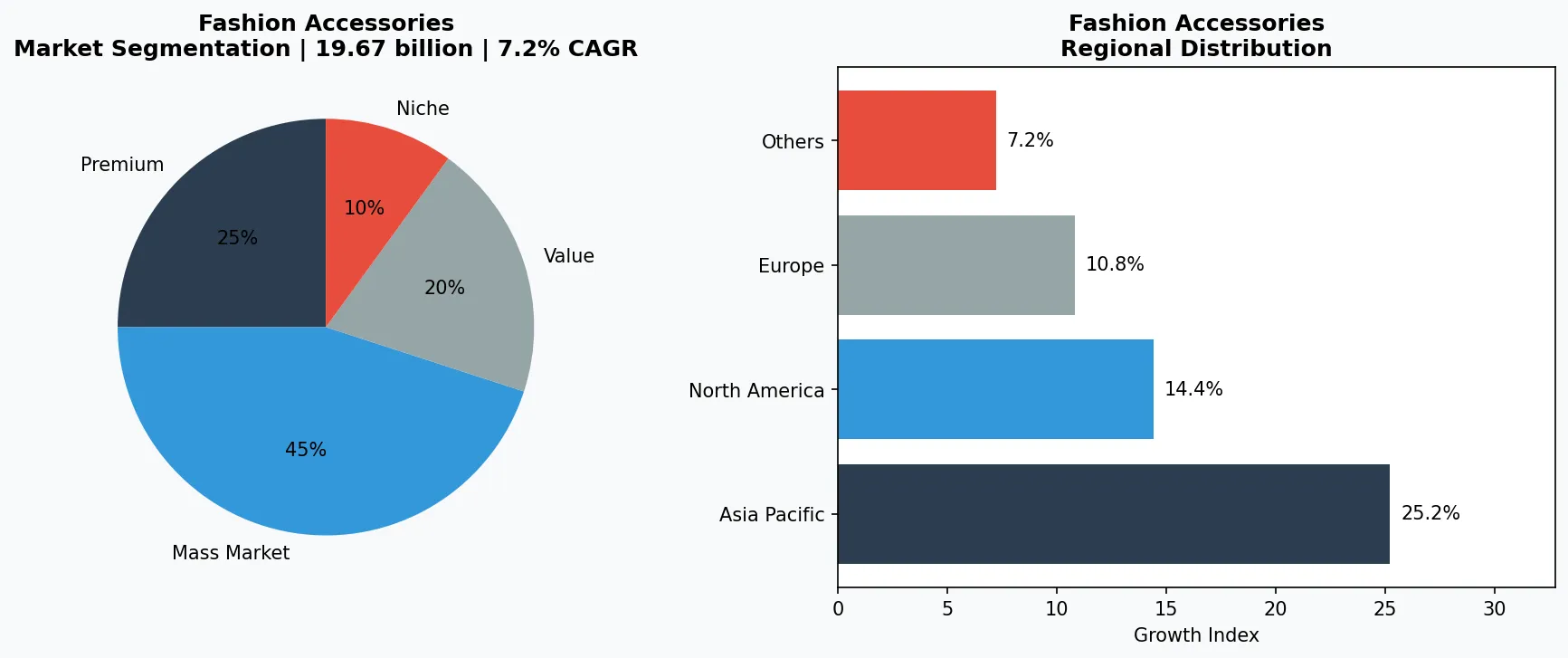

1. Industry Overview

The global protective gloves market is poised to hit USD 19.67 billion, but that figure masks a sharp divide: winter and summer gloves serve fundamentally different functions in the fashion accessories segment. Winter gloves prioritize insulation, wind resistance, and gripping technology for cold-weather performance, while summer gloves focus on breathability, UV protection, and lightweight dexterity. This bifurcation creates distinct supply chains—wool and leather dominate winter lines, while mesh, cotton, and synthetic knits rule summer collections. The fashion accessory segment alone accounts for roughly 18% of total glove volume, yet commands premium pricing due to brand and design. For B2B buyers sourcing for retail or corporate gifting, understanding these seasonal archetypes is critical: a misstep in material selection for winter gloves can lead to returns exceeding 12% in northern markets, while summer gloves that fail breathability tests see rejection rates of 20% in humid climates. The market’s growth, driven by rising workplace safety demands and fashion-conscious consumers, means suppliers must innovate across both seasons to capture share.

Industry Scope & Characteristics

Seasonal Duality

Winter gloves use insulation layers (wool, fleece, down) and windproof membranes; summer gloves prioritize mesh, cotton, or perforated leather for airflow. A single supplier often needs dual production lines.

Material Specialization

Leather sourcing for winter gloves requires hides with high tear strength, while summer gloves use lighter woven fabrics. Supply chains rarely overlap, demanding separate vendor audits.

Certification Complexity

Winter gloves for sale in the EU must carry CE marking for thermal insulation (EN 511) if sold as protective gear. Summer gloves for UV protection may require UPF rating labeling, a nascent standard.

Smart Textile R&D

Integrating conductive threads or heating elements into glove fingertips requires specialized knitting machines. Fewer than 15 factories globally have mastered this at scale, creating a barrier to entry.

Key market segments and growth drivers in the Gloves Winter Summer Types sector.

2. Market Analysis

The safety gloves market is projected to grow from US$15.6 billion in 2026 to US$25.4 billion by 2033, registering a 7.2% CAGR. While much of this growth stems from industrial and medical applications, the fashion accessory segment is riding a parallel wave. Consumer demand for premium winter gloves—especially those with touchscreen compatibility and eco-friendly insulation—is pushing average unit prices up 9% year-over-year. Simultaneously, summer gloves made from sustainable bamboo or recycled polyester are capturing shelf space in eco-conscious retail channels. The global nitrile gloves market, valued at USD 5.27 billion in 2025 and expanding at over 9.4% CAGR, illustrates the broader trend toward performance materials. Nitrile’s adoption in fashion gloves is nascent but growing, particularly for summer cycling and driving gloves where durability and non-slip grip are valued. The Industrial Gloves Market, estimated at USD 10,564.2 million in 2026 and expected to reach USD 17,153.3 million by 2033, shows that functionality continues to command large volumes, but the fashion crossover—where a glove looks retail-ready yet meets safety standards—is the fastest-growing niche.

Market segmentation and regional distribution analysis for Gloves Winter Summer Types.

3. Product Categories

Winter Gloves: Insulation and Dexterity

Winter gloves fall into three sub-types: lined leather, knitted wool with inner fleece, and technical insulated gloves with waterproof membranes. Lined leather gloves, such as cashmere-lined goatskin, target luxury buyers who value tactile warmth and slim profiles. Knitted wool gloves dominate mass retail, often blended with acrylic for stretch and nylon for durability. Technical winter gloves incorporate PrimaLoft or Thinsulate insulation and are popular with outdoor enthusiasts and corporate-branded apparel.

Summer Gloves: Breathability and Protection

Summer gloves prioritize ventilation and sun protection. Fingerless driving gloves in perforated leather remain a classic niche, while lightweight cotton or bamboo gloves with UV-blocking treatments are gaining traction in gardening and casual wear. Mesh cycling gloves with gel padding and silicone grips represent a performance sub-segment that overlaps with sportswear.

Transitional All-Season Gloves

A rising product type is the convertible glove-mitten design for winter and the lightweight liner that works alone in summer or as a base layer in winter. These dual-use items reduce inventory complexity for retailers and appeal to minimalist consumers.

Lined Leather Winter Gloves

Cashmere or silk-lined goatskin and deerskin gloves for formal and luxury wear. Examples include classic driving-style gloves and opera-length evening gloves.

Knitted Outdoor Winter Gloves

Merino wool or acrylic blends with internal fleece lining and silicone grip patterns. Common for skiing, snowboarding, and casual cold-weather use.

Lightweight Summer Driver Gloves

Perforated unlined leather or open-knit mesh gloves with knuckle cutouts. Favored in automotive and equestrian circles for grip and breathability.

4. Leading Players

Winter Leather Specialists

A cadre of Italian and French tanneries dominates the luxury winter glove segment. These players control the entire supply chain—from hide selection to hand-stitching—enabling them to offer exclusive colorways and firm-specific lining materials. Their competitive advantage lies in heritage branding and the ability to certify glove warmth ratings according to EN 511 standards, a requirement for premium retailers.

Performance Knit Innovators

Manufacturers specializing in seamless knitting technology are reshaping the summer glove category. By using 3D knitting machines, they produce gloves with no internal seams, superior moisture wicking, and finger-tip articulation. Their strategy focuses on rapid prototyping for private-label brands and low MOQs for direct-to-consumer labels, capturing the fast-fashion glove cycle.

Sustainable Material Pioneers

A growing number of Asian mills are launching gloves made from recycled fishing nets (nylon) and organic cotton. These players differentiate by offering full lifecycle data and certifications such as Global Recycled Standard (GRS) and Oeko-Tex. Their main customers are European fashion houses and outdoor brands seeking to meet 2026 sustainability targets.

Heritage Leather Glove Ateliers

These manufacturers leverage century-old hand-cutting techniques to produce low-volume, high-margin winter gloves for luxury brands. They compete on craftsmanship and exclusivity.

Seamless Knit Technology Specialists

Using Italian or German knitting machines, these players produce summer gloves with zero-waste, seamless construction, offering fast turnaround for private-label clients.

Sustainable Mass Producers

Asian mills that integrate recycled yarns into both winter and summer lines, targeting mid-market retailers with eco-certifications. They scale through automation and bulk fiber purchasing.

5. Market Trends

1. ECO-MATERIALS MANDATE

Gloves made from recycled polyester, bamboo, or biodegradable latex are no longer niche. Buyers now require traceability; leading tanneries are offering certified leather from LWG Gold-rated sources. This trend is accelerating with EU regulations mandating due diligence on deforestation in leather supply chains by 2026.

2. TOUCHSCREEN COMPATIBILITY

Conductive yarns embedded in fingertips have become table stakes for winter gloves. By 2025, over 70% of winter gloves sold in North America included touchscreen functionality. Suppliers failing to offer this risk being delisted from major retailers. Micro-copper or silver-coated threads are the most common solutions.

3. SMART GLOVE INTEGRATION

The convergence of gloves with wearable tech is emerging: heated gloves with rechargeable battery packs are a growing sub-category, with some models offering temperature control via smartphone app. The global smart gloves market, though small, is growing at 15% CAGR and attracting investment from sportswear conglomerates.

4. SEAMLESS KNITTING

As mentioned in products, this manufacturing technique reduces waste by 30% and allows for custom fit. It is particularly suited for summer glove production where thinness and stretch are critical. Chinese knitting machine manufacturers have doubled capacity since 2024.

6. Regional Markets

Europe: Luxury Winter Glove Hub

Italy and France host ateliers that supply top fashion houses. EU regulations on leather traceability and PFAS bans are pushing rapid material innovation.

Asia: Volume Summer Glove Manufacturing

China and Bangladesh dominate production of lightweight cotton and synthetic summer gloves, leveraging low labor costs and integrated textile supply chains.

North America: Performance and Tech Segment

The US and Canada lead demand for heated winter gloves and touchscreen-compatible styles, with outdoor brands driving R&D in smart glove technology.

7. Investment Outlook

Two specific opportunities stand out for B2B buyers in 2026. First, sourcing winter gloves with integrated heating elements from Southeast Asian contract manufacturers allows entry into the premium outdoor market without heavy R&D investment. Second, the shift toward summer gloves with antimicrobial finishes for post-pandemic hygiene consciousness opens a new product line for hospitality and healthcare uniform suppliers. The primary risk is regulatory: evolving PFAS bans in Europe could force reformulation of waterproof coatings used in winter gloves, leading to supply bottlenecks. Buyers should verify that suppliers have transitioned to PFAS-free DWR treatments by mid-2026.

Strategic Considerations:

- Heated Winter Glove Opportunity: Contract manufacturers in Vietnam are scaling battery-powered glove production; retailers can enter this premium segment with low upfront cost.

- Antimicrobial Summer Gloves: Adding silver-ion or copper treatments to summer glove linings opens new B2B channels in healthcare food service and hospitality sectors.

- PFAS Regulatory Risk: European restrictions on perfluorinated chemicals could disrupt waterproof winter glove supply; buyers should require PFAS-free DWR certifications from suppliers by Q3 2026.

- Seamless Knitting Adoption: Factories investing in Shima Seiki or STOLL machines gain a 30% waste reduction advantage; early adopters will dominate summer glove sourcing in 2027.

Frequently Asked Questions

Make Informed Decisions in the Gloves Winter Summer Types Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-21. All market figures are estimates and may vary from actual results.