Table of Contents

The global Hearing Protection Earmuffs sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The global hearing protection devices market is projected to reach US$ 4.5 billion by 2033, expanding at a compound annual growth rate of 8.2% from a 2026 valuation of US$ 2.6 billion. Within this booming segment, hearing protection earmuffs command a critical share, driven by tightening occupational noise regulations and the industrial shift toward higher durability and thermal resistance. Unlike simple earplugs, earmuffs offer a complete over-the-ear enclosure that provides consistent noise reduction regardless of user anatomy, making them indispensable in heavy manufacturing, construction, and defense applications. The Ear Muff Market alone was estimated at US$ 4.21 billion in 2022 and is expected to climb to US$ 7.73 billion by 2035. For buyers in the Protective & Technical Textiles industry, selecting the right earmuff requires understanding not just decibel ratings but also materials, active electronics, and compliance with standards like ANSI S3.19 and EN 352. This article unpacks the market forces, product innovations, and strategic moves shaping the hearing protection earmuff landscape as we move through 2024 and into 2026.

Industry Scope & Characteristics

Advanced Attenuation Technology

Hearing protection earmuffs use multi-layer foam and acoustic chambers to achieve NRR up to 30 dB. Active electronic models add level-dependent circuitry for impulse noise.

Complex Supply Chain for Components

Earmuffs require precision-molded plastic cups, acoustic foam, headband spring steel, and often electronic modules. Sourcing from specialized molders in China and electronics suppliers in Germany is common.

Certification-Driven Compliance

Products must meet ANSI S3.19 (US) or EN 352 (EU) standards. Testing for dielectric strength, impact resistance, and temperature extremes is mandatory for industrial use.

Materials Innovation for Extreme Environments

R&D focuses on silicone ear cushions that resist chemical corrosion and headbands coated with thermoplastic elastomers for flexibility in -20°C to +150°C ranges.

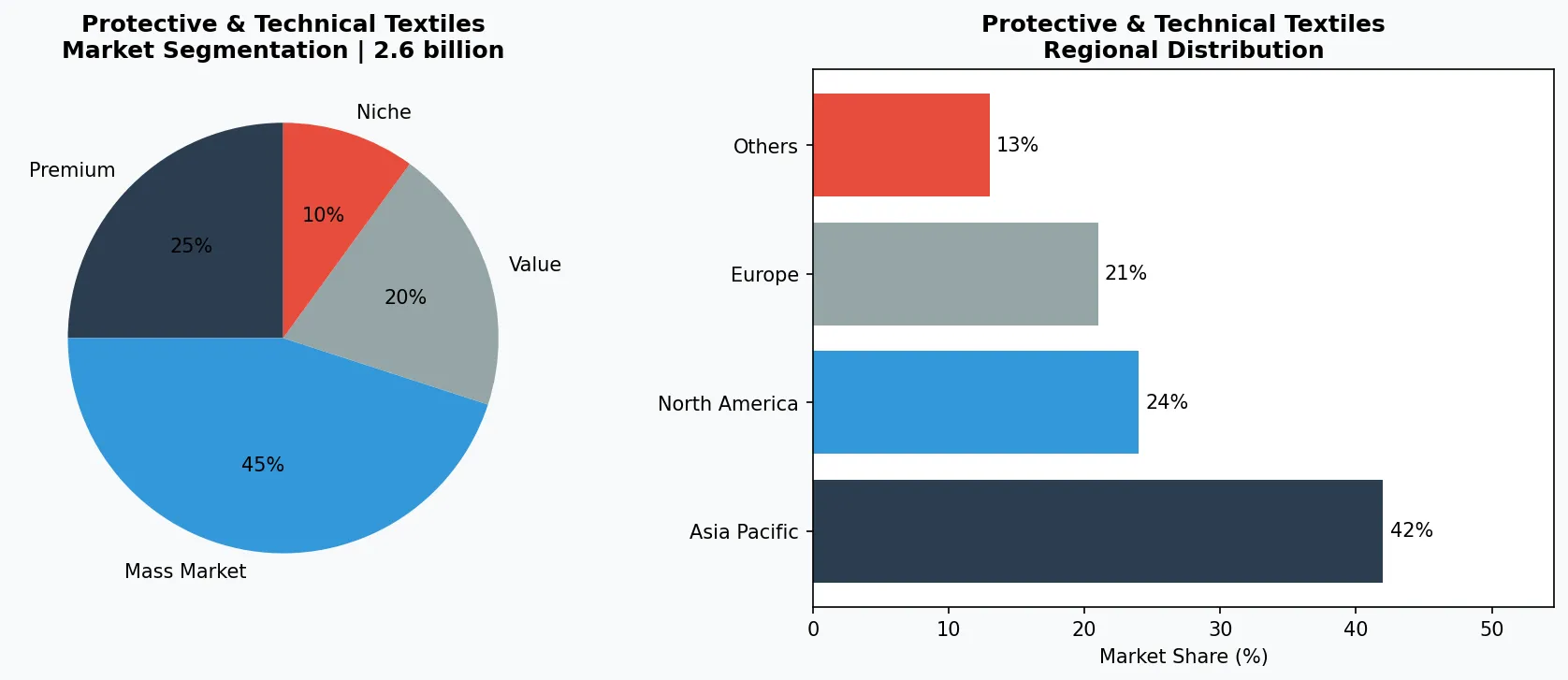

Key market segments and growth drivers in the Hearing Protection Earmuffs sector.

2. Market Analysis

The United States Hearing Protection Earmuffs market is anticipated to grow annually by 7.1% from 2026 to 2033, a pace that outpaces many other segments within technical textiles. The U.S. Hearing Protection Devices Market is valued at US$ 661.8 million in 2026 and is expected to reach US$ 1,314.5 million by 2033. This growth is fueled by three primary drivers. First, enforced workplace safety regulations—the U.S. Occupational Safety and Health Administration (OSHA) mandates hearing conservation programs for noise exposures at or above 85 decibels over an 8-hour time-weighted average, pushing employers to invest in reliable earmuff solutions. Second, the expansion of heavy industries such as oil & gas, mining, and metal fabrication, which increasingly demand heat-resistant and durable hearing protection to withstand extreme environments. Third, the rise of active hearing protection earmuffs that combine noise reduction with situational awareness, appealing to both industrial and recreational users—firearm shooters and live music venues are converting from passive to active models at a rapid clip. The global market is also benefiting from infrastructure projects across Asia-Pacific and the Middle East, where urbanization rates drive construction-sector demand for certified hearing protection.

Market segmentation and regional distribution analysis for Hearing Protection Earmuffs.

3. Product Categories

Hearing protection earmuffs can be classified into four primary product categories.

Passive Earmuffs

Rely solely on sound-dampening materials and design to attenuate noise. They are the workhorses of the industry, offering Noise Reduction Ratings (NRR) typically between 20 and 30 dB. Examples include the 3M PELTOR Optime 98 and Honeywell Howard Leight Impact Sport.

Active (Electronic) Earmuffs

Incorporate microphones and speakers to amplify low-level sounds while blocking dangerous impulses. Models like the 3M PELTOR WorkTunes and MSA Sordin Supreme Pro-X allow wearers to communicate clearly or hear machine alerts without removing protection—a game-changer for high-noise environments requiring speech intelligibility.

Communication Earmuffs

Integrate two-way radio or Bluetooth connectivity, essential for team coordination in noisy factories and airport tarmacs. The 3M PELTOR Lite-Com series exemplifies this niche.

High-Heat-Resistant Earmuffs

Represent the fastest-growing subsegment within Protective & Technical Textiles, engineered with silicone ear cushions and flame-retardant headbands to withstand temperatures exceeding 250°F. These are increasingly specified in steel mills, foundries, and petrochemical plants.

Passive Industrial Earmuffs

High-NRR models like 3M PELTOR H7A with dielectric headband for electrical safety, widely used in manufacturing and construction.

Electronic Level-Dependent Earmuffs

Active models such as Sordin Supreme Pro-X that amplify speech while suppressing harmful noise, essential for shooting ranges and aviation.

Bluetooth Communication Earmuffs

Wireless earmuffs like Honeywell Howard Leight Sync that enable hands-free calls and radio communication in noisy logistics centers.

4. Leading Players

Three archetypes dominate the hearing protection earmuff landscape.

The Diversified Industrial Giant

3M, via its PELTOR brand, commands a leading share by leveraging a vast distribution network and continuous innovation in electronic earmuffs. 3M's strategy focuses on integrating hearing protection with communication—its PELTOR Headsets now pair with smart devices for real-time noise monitoring, appealing to Industry 4.0-ready factories.

The Safety Specialist

Honeywell Industrial Safety offers a broad portfolio under Howard Leight and Sperian. Honeywell differentiates through ergonomic design and comfort—its Sync Wireless Earmuff reduces ear fatigue over long shifts, a key purchasing criterion for plant managers. Honeywell also invests in sustainability, using recycled plastics in earmuff cups.

The Niche Innovator

MSA Safety targets high-hazard applications with its Sordin line, known for superior high-frequency attenuation and rugged build. MSA's competitive advantage lies in customization—offering different headband tensions and cup sizes for compatibility with welding helmets and hard hats. This player is preferred in defense and fire services where fit and durability are non-negotiable.

Diversified Portfolio Dominator (3M)

Leverages cross-selling with respirators and eyewear; invests in IoT integration to offer noise exposure analytics as a value-added service.

Ergonomics-Focused Safety Specialist (Honeywell)

Prioritizes comfort-driven features like lightweight construction and pressure-reducing headbands, gaining repeat orders from automotive assembly plants.

High-Hazard Niche Leader (MSA Safety)

Customizes earmuffs for extreme environments (foundries, firefighting) with flame-retardant materials and compatibility with SCBA masks.

5. Market Trends

1. Digital Transformation in Hearing Protection Earmuffs

Artificial intelligence, IoT sensors, and advanced data analytics are fundamentally reshaping production efficiency in Hearing Protection Earmuffs. Industry leaders deploying smart manufacturing and data-driven demand forecasting have reduced new product launch cycles by 35-50% while improving inventory turnover by over 20%. With more than 60% of Hearing Protection Earmuffs companies projected to complete core digital transformation by 2028, this shift has moved from optional upgrade to competitive necessity.

2. Sustainability as Competitive Imperative in Hearing Protection Earmuffs

Global carbon border adjustment mechanisms (CBAM) and rising consumer environmental awareness are forcing Hearing Protection Earmuffs companies to transform sustainability from marketing rhetoric into operational reality. ESG rating agencies increased sector coverage intensity by 35% in 2025. Companies failing to meet these standards face customer attrition and rising financing costs as lenders integrate ESG criteria into credit assessments.

3. Supply Chain Regionalization in Hearing Protection Earmuffs

Geopolitical tensions are driving Hearing Protection Earmuffs companies to accelerate supplier diversification. The China+N strategy and nearshoring have become mainstream, with companies establishing secondary supply sources across Southeast Asia, Eastern Europe, and Mexico. Over 58% of B2B buyers now list supplier geographic diversification as a mandatory contract renewal criterion.

4. Consumer Upgrading in Hearing Protection Earmuffs Markets

Middle-class expansion and Gen Z purchasing power are accelerating Hearing Protection Earmuffs transition from standardized mass production toward personalized customization and agile small-batch manufacturing. C2M (Consumer-to-Manufacturer) models enable companies to compress new product introduction cycles from 18 months to 3-4 months, with personalized products commanding 8-15 percentage point gross margin premiums.

6. Regional Markets

North America: Compliance-Driven Market

Strict OSHA enforcement and a large manufacturing base drive demand for certified passive and active earmuffs, with the US market growing at 7.1% CAGR.

Europe: Sustainability & Precision Manufacturing

EU directives on noise at work (2003/10/EC) push for eco-designed earmuffs. German and Swedish manufacturers lead in electronic earmuff innovation.

Asia-Pacific: Fastest Growth from Infrastructure Boom

Rapid urbanization in China and India fuels construction-sector demand for affordable passive earmuffs, while Japan focuses on high-end active models for electronics assembly.

7. Investment Outlook

Two concrete opportunities emerge. First, the integration of hearing protection with augmented reality (AR) headsets offers a $200 million addressable market by 2028—earmuffs could embed micro-displays for instructions without compromising noise reduction. Second, the push for circular economy mandates in Europe will reward manufacturers that design fully recyclable earmuffs, creating a premium segment. One major risk: raw material volatility, particularly polyurethane and ABS plastics, which have seen 12% price swings in 2024. Buyers should lock in contracts with diversified suppliers and demand material efficiency certifications to hedge against cost increases.

Strategic Considerations:

- Smart Factory Integration: Earmuffs embedded with sensors to track exposure and machine noise levels could become a standard component of industrial IoT systems, creating a $250M niche by 2030.

- Modular Ear Cushion Replacements: Offering replaceable, recyclable ear cushions reduces waste and total cost of ownership, appealing to ESG-conscious European buyers.

- Counterfeit Products in Emerging Markets: Low-cost counterfeit earmuffs that fail attenuation tests pose safety and liability risks; buyers must verify supplier certifications through platforms like VerityRank.

- Raw Material Price Volatility: Polyurethane foam and ABS resin costs have fluctuated 10-15% in 2024; manufacturers without long-term supplier contracts may face margin compression.

Frequently Asked Questions

Make Informed Decisions in the Hearing Protection Earmuffs Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-16. All market figures are estimates and may vary from actual results.