Table of Contents

The global Home Decor industry serves consumers worldwide with diverse solutions.

1. Industry Overview

The global home decor market will be worth nearly $862 billion in 2026—yet most retailers are woefully unprepared for the seismic shifts driving this growth. The $139 billion home decor segment is experiencing a fundamental transformation as consumers increasingly view their living spaces as extensions of personal identity rather than mere functional areas. This represents a historic break from the past decade, when home decor was treated as a discretionary afterthought. Interior designers and industry experts have identified eight interior design trends defining 2026, all centered on longevity, function, and meaning rather than pure aesthetics. Companies that understand this shift are capturing market share at unprecedented rates, while those clinging to traditional approaches find themselves losing relevance fast.

Industry Scope & Characteristics

Broad Product Portfolio

Products span vases, picture frames, candles, decorative trays, sculptures, clocks, mirrors, wall art, plants, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

The demographic driving this transformation defies conventional wisdom. Buyers under 40 now represent the largest consumer segment in home decor, yet their purchasing behavior bears little resemblance to their predecessors. Where previous generations invested in timeless staples and treated decor as permanent, today's consumers curate evolving environments that reflect their current identities. This has compressed product cycles and created demand for accessible design at every price point. The implications for manufacturers and retailers are profound: the industry can no longer rely on predictable seasonal refreshes or timeless collections alone.

What's emerging is a bifurcated market where mass-market accessibility and premium artisanal craft coexist under the same category umbrella. IKEA's flat-pack empire and Tom Dixon's sculptural pieces now compete not just for wallet share but for cultural relevance. The question is no longer whether the home decor market will grow—the data confirms it will—but whether traditional industry structures can adapt fast enough to capture value in an increasingly fragmented landscape where consumer expectations shift faster than supply chains can respond.

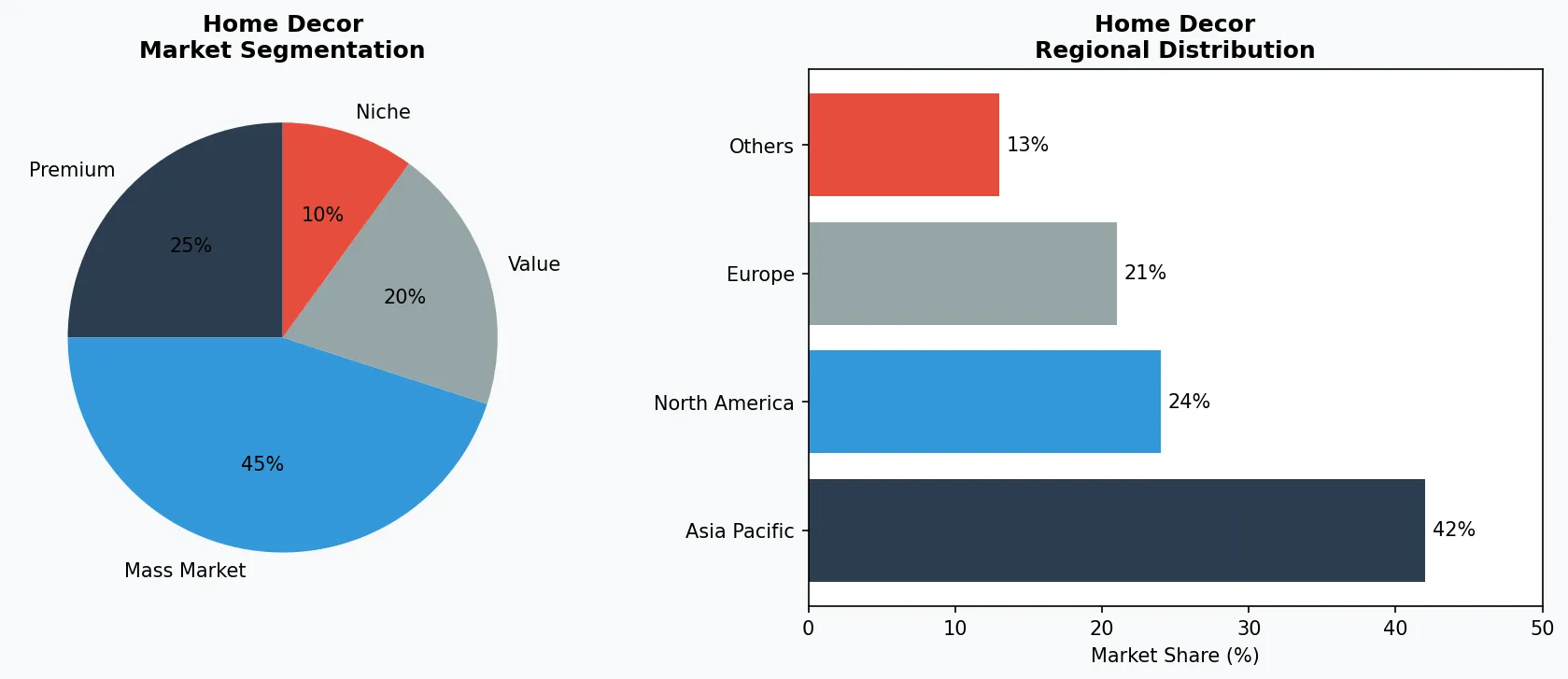

Key market segments and growth drivers in the Home Decor sector.

2. Market Analysis

The global home decor market reached $802.26 billion in 2025 and is projected to grow to $862.18 billion in 2026, on trajectory to hit $1.3 trillion by 2034. This represents a compound annual growth rate of 5.5% from 2026 to 2033—significantly outpacing broader consumer goods categories and signaling structural demand rather than cyclical recovery. Three forces drive this expansion: rising residential construction activity in emerging markets, shifting consumer priorities toward personalized living spaces, and the maturation of e-commerce channels that have democratized access to design inspiration and products previously confined to specialty retailers.

The United States remains the world's largest single home décor market, projected to grow from $145.52 billion in 2025 to $212.93 billion by 2034 at a CAGR of 4.32%. Growth here is concentrated in metropolitan areas where housing turnover remains elevated and renters increasingly invest in portable decor to personalize temporary spaces. China's market, meanwhile, is experiencing accelerated growth driven by e-commerce penetration reaching previously underserved second and third-tier cities. European markets are growing more slowly but generating disproportionate innovation, with sustainability-conscious consumers demanding transparency in materials and manufacturing provenance.

The market's growth trajectory reveals an important geographic nuance: emerging markets are growing faster but from smaller bases, while developed markets like the United States represent the largest absolute dollar opportunity. For suppliers and retailers, this means geographic diversification is essential—overexposure to any single market creates vulnerability to regional economic fluctuations while missing the compounding growth available in high-velocity developing economies.

Within the broader home furniture category, decorative accessories have emerged as the fastest-growing segment, outpacing larger categories like furniture and textiles. This shift reflects consumer preference for accessible, low-commitment purchases that deliver immediate aesthetic impact without requiring major investment or permanent decisions. The segment's growth rate of 7.2% annually outpaces the overall market, making it the battleground where competitive advantage will be won or lost.

Market segmentation and regional distribution analysis for Home Decor.

3. Product Categories

Decorative vases represent the category's most dynamic sub-segment, with sculptural and artisan-crafted designs commanding premium positioning. Tom Dixon's copper and brass vessels occupy the luxury tier, while IKEA's BYSSA and FEJKA lines demonstrate how mass-market producers are incorporating design-forward aesthetics into accessible price points. The trend toward oversized statement pieces reflects consumer appetite for focal points that anchor room compositions without requiring major purchases. HAY's geometric vases have become Instagram staples, illustrating how product design intersects with social media marketing to drive category growth.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Wall decor encompasses a spectrum from functional clocks and mirrors to investment-grade artwork. Nemo has established strong positioning in architectural lighting that doubles as wall-mounted sculpture, while Zarahome's modular wall art systems cater to consumers who prefer customizable arrangements over single statement pieces. This sub-category benefits from the perennial refresh cycle: unlike furniture, wall decor can be updated seasonally or when renters move, creating recurring purchase occasions that drive category frequency.

Scented candles and decorative trays constitute the entry point category, combining function with aesthetic appeal. MUJI's minimalist candle line exemplifies the clean design philosophy that has made the Japanese retailer a touchstone for consumers seeking understated quality. Meanwhile, Tom Dixon's scented candles leverage the designer's brand equity to command prices three times higher than mass-market alternatives—a premium justified by distinctive fragrance profiles and reusable vessels. This sub-category demonstrates how sensory experience increasingly differentiates products in a market where visual aesthetics alone no longer suffice.

4. Leading Players

IKEA maintains its position as the industry's volume leader through relentless optimization of its value chain and design-to-cost methodology. The Swedish retailer's 2024 launch of its OTLO series of sculptural vases represented a deliberate expansion into the premium decorative accessories tier that has traditionally eluded mass-market producers. By leveraging its supply chain scale and design partnerships with external studios, IKEA can offer design-forward products at price points 60-70% below comparable offerings from specialty retailers. The company's investment in augmented reality shopping tools positions it to capture market share in the growing digital commerce segment, where immersive visualization reduces the uncertainty that historically hindered online decor purchases.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the home decor space.

MUJI pursues a diametrically opposed strategy, building brand equity through radical restraint and material authenticity. The Japanese retailer's home decor line features no decorative embellishment—instead, beauty emerges from proportions, material quality, and manufacturing precision. MUJI's 2025 expansion of its ceramic collection introduced hand-thrown pieces that acknowledge the artisanal origins of its mass-produced forms. This transparency about craft and provenance resonates strongly with consumers fatigued by the visual noise of maximalist alternatives. The company's retail footprint in North America has grown 22% since 2023, targeting design-conscious urban consumers in major metropolitan markets who prioritize intentional consumption over volume.

HAY has emerged as the defining brand of accessible contemporary design, bridging the gap between IKEA's mass-market pragmatism and the premium positioning of heritage brands. The Danish company's strategy centers on collaborative design—its permanent collection results from ongoing partnerships with external designers rather than internal creative teams. This model produces continuous product innovation without the overhead of maintaining a large in-house design staff. HAY's global expansion accelerated in 2025, with new flagship stores opening in Seoul and Los Angeles that showcase the brand's full lifestyle ecosystem rather than discrete product categories. The strategy reflects a broader industry recognition that consumers increasingly seek curated environments rather than individual products.

5. Market Trends

1. MINIMALIST DESIGN EVOLUTION

MINIMALIST DESIGN EVOLUTION — Minimalist design has transcended its origins as an aesthetic movement to become a functional philosophy. Today's minimalist home decor emphasizes pieces that serve multiple purposes while contributing to overall spatial harmony. The trend matters because it reflects how consumers evaluate purchases—increasingly through the lens of longevity rather than novelty. IKEA's expansion of its SOCKERBIT storage line into decorative vessels exemplifies how minimalism is being operationalized for mass markets. Companies that can deliver products balancing aesthetic restraint with functional utility are capturing disproportionate share among consumers downsizing living spaces while upgrading quality.

2. ARTISANAL CRAFT REVIVAL

ARTISANAL CRAFT REVIVAL — A counter-movement to mass production has gained momentum as consumers seek products with demonstrable human craftsmanship and cultural heritage. This trend drives growth in hand-thrown ceramics, hand-woven textiles, and limited-edition sculptural pieces that carry narrative value beyond utility. Tom Dixon's continued investment in British manufacturing facilities reflects this shift—consumers increasingly care whether and where products are made. The trend creates opportunities for regional craft economies and traditional manufacturing centers to capture value in supply chains traditionally dominated by mass producers. Supply chain transparency is becoming a competitive differentiator as consumers demand provenance information.

3. SMART HOME COMPATIBILITY

SMART HOME COMPATIBILITY — The integration of home decor with connected home ecosystems represents a convergence that is reshaping product development across the industry. Decorative lighting, wall-mounted displays, and smart mirrors increasingly serve dual functions as aesthetic elements and technology platforms. Nemo's architectural lighting systems now incorporate smart home compatibility as standard features rather than premium options. The trend matters because it expands the addressable market for home decor into technology-adjacent categories where consumers demonstrate higher willingness to spend. Companies that ignore smart integration risk exclusion from the premium segment where growth is concentrated.

4. NATURAL MATERIALS EMPHASIS

NATURAL MATERIALS EMPHASIS — Materials sourcing has become a defining competitive dimension as consumers reject synthetic materials in favor of natural alternatives with lower environmental impact. Stone, wood, rattan, and ceramic dominate the fastest-growing product categories, while plastic-based decor faces increasing consumer resistance. Zarahome's 2025 product line refresh eliminated PVC from packaging and reduced plastic components across its decorative accessory range. This materials shift creates supply chain challenges as natural material demand outpaces sustainable sourcing capacity, but it also opens opportunities for brands that can demonstrate genuine environmental commitment rather than superficial greenwashing.

6. Regional Markets

The United States remains the world's largest single home décor market, with projected growth from $145.52 billion in 2025 to $212.93 billion by 2034 at a CAGR of 4.32%. Growth concentrates in metropolitan areas where housing turnover and rental activity remain elevated—consumers in these markets invest heavily in portable decor to personalize temporary living situations. The e-commerce channel now accounts for 38% of decorative accessory sales in the US, up from 29% in 2023, driven by improved return policies and augmented reality tools that reduce purchase uncertainty. West Coast markets show particular strength in sustainable and artisanal products, reflecting regional consumer preferences that are gradually diffusing nationally.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

China represents the fastest-growing major market, driven by e-commerce acceleration and rising middle-class demand for premium home environments. The country's home decor market is expanding at nearly twice the global CAGR, fueled by new residential construction in tier-2 and tier-3 cities where home improvement spending traditionally lagged. Chinese consumers increasingly prefer domestic brands that understand local aesthetic preferences, creating barriers for Western retailers. However, HAY's successful entry and expansion demonstrates that design-forward positioning can overcome cultural preferences for domestically sourced products among younger Chinese consumers.

The United Kingdom presents a distinct profile—maturing market with modest growth but outsized innovation impact on global trends. London-based retailers and design studios disproportionately influence aesthetic direction through social media and editorial coverage. UK consumers demonstrate the highest sustainability consciousness among major markets, with 67% reporting that environmental credentials influence their home decor purchasing decisions. This has accelerated the adoption of circular economy practices including product take-back programs and modular designs that can be reconfigured rather than replaced. Brands that develop UK market strategies often find their products gaining traction in other European markets where similar consumer values are emerging.

7. Investment Outlook

Two concrete opportunities define the industry's immediate future. First, smart home integration will drive a new product category where aesthetic objects carry embedded connectivity—decor that dims via voice command, mirrors that display health metrics, and clocks synchronized with smart home routines. This convergence creates premium pricing opportunities while solving consumer needs that purely functional smart home devices have failed to address. Second, AI-powered interior design tools democratizing professional-grade space planning will expand the market by reducing the perceived risk of decor purchases. When consumers can visualize products in their actual spaces before buying, conversion rates increase and return rates decline—improving unit economics across the value chain.

One concrete risk demands attention: raw material cost volatility threatens margins across the industry as natural materials face supply constraints while demand accelerates. Stone, wood, and ceramic prices have increased 15-20% since 2024, compressing profitability for companies that cannot pass costs to consumers or redesign products using alternative materials. Companies with diversified supplier bases and long-term sourcing contracts will navigate this pressure more effectively than those dependent on spot market purchasing. Regulatory changes in the EU and North America targeting supply chain transparency and circular economy practices will increase compliance costs but also create competitive advantages for early adopters who build sustainability into their operating models rather than retrofitting processes. The home decor industry's $862 billion trajectory in 2026 is not guaranteed—it belongs to companies that act decisively on these structural shifts.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Home Decor Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-17. All market figures are estimates and may vary from actual results.