Table of Contents

The global Indoor Plants & Planters sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Forget the fiddle leaf fig. In 2026, the indoor plants and planters segment of the Home Decor industry is undergoing a radical transformation—one driven by a counterintuitive mantra: go big or go home. The North American pots and planters market alone is projected to hit $6.1 billion in 2026, up from $5.8 billion in 2025, according to industry data. This 5.2% year-over-year growth is not just about more plants; it’s about strategic curation. The trend is shifting decisively toward 'fewer, larger plants' anchored by oversized artisan planters, a move that fundamentally changes how decorative accessories like vases, sculptures, and wall art are merchandised and purchased.

Industry Scope & Characteristics

Living Inventory Complexity

Unlike static decor, indoor planters must accommodate living plants. Key specs include drainage holes, non-toxic glazes, and insulation against temperature swings. Self-watering planters with wicking systems are a growing sub-category.

Clay-to-Consumer Lead Times

Ceramic planters require 8–12 week firing cycles. Artisan pieces may take longer. B2B buyers must plan inventory 2–3 quarters ahead, especially for oversized pieces like Salinas Planters.

Material Safety Standards

Planters must meet lead and cadmium leaching standards (e.g., California Prop 65). For commercial use, fire-retardant materials and stability testing (tip-over risk) are critical compliance issues.

Hybrid Material Innovation

R&D is focused on 'breathable' ceramics—planters with microscopic pores that regulate soil moisture. Companies are also developing self-glazing finishes that change color with humidity, merging decor with plant health monitoring.

What makes indoor plants and planters distinctive within the broader Home Decor sector is their dual function: they are both living decor and structural design elements. Unlike a static picture frame or a candle, a planter and its plant create an evolving focal point that interacts with light, space, and air quality. This living aspect adds a layer of complexity to sourcing and quality control—buyers must consider drainage, material durability, and plant compatibility, not just aesthetics. The global Indoor Flower Pots and Planters Market is expanding at a compound annual growth rate (CAGR) of 7.2% from 2026 to 2033, signaling sustained demand that outpaces many traditional home accessory categories.

This growth is not accidental. It is fueled by a post-pandemic normalization of remote and hybrid work, where homes have become permanent showcases for personal style. Consumers are moving away from cluttered shelves of small succulents toward statement pieces. Google Trends data compiled from primary industry sources shows a steady rise in searches for 'large floor planters' and 'artisan ceramic pots' since 2024, with a notable spike in Q4 2025. For B2B buyers, this means the opportunity lies not in volume but in curation—supplying fewer, higher-quality pieces that command premium price points. The era of the disposable plastic pot is giving way to sculptural ceramic and warm Mediterranean palettes that double as art.

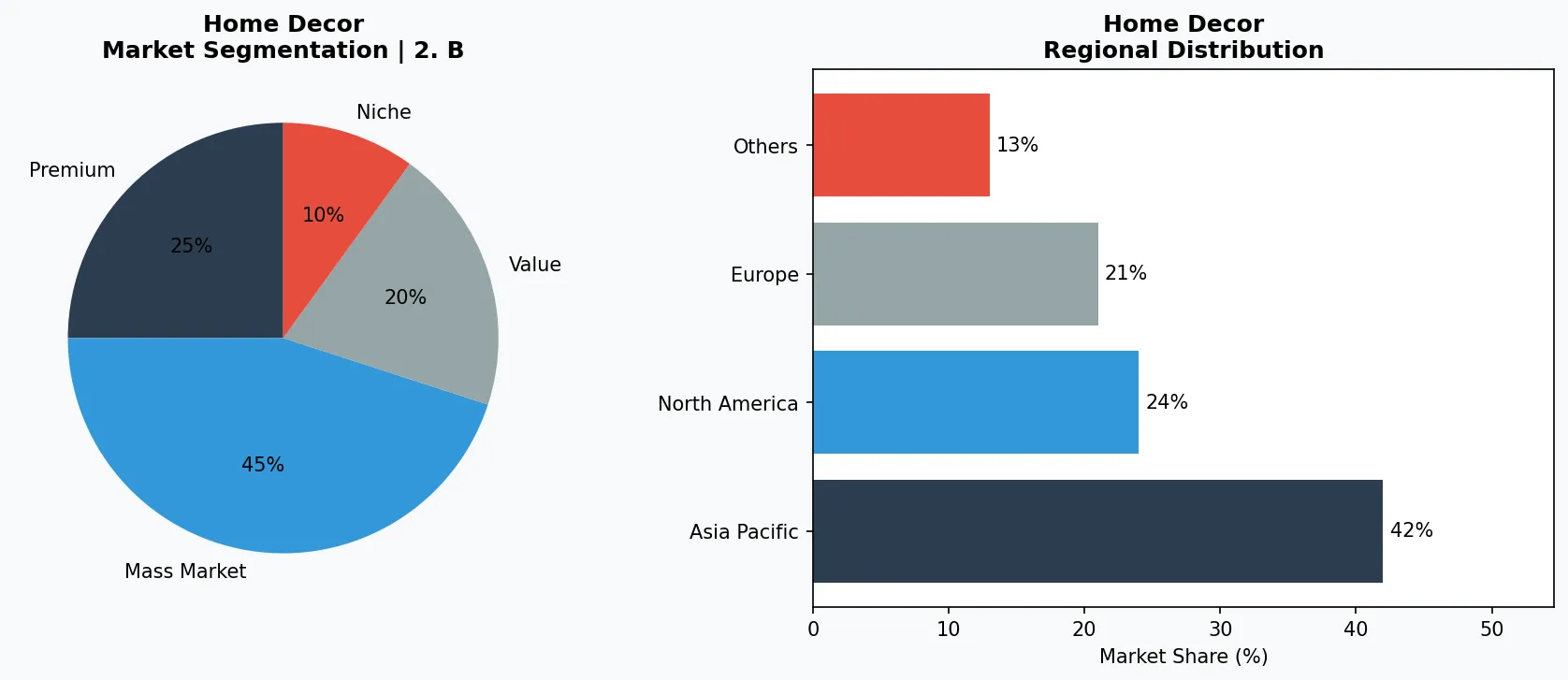

Key market segments and growth drivers in the Indoor Plants & Planters sector.

2. Market Analysis

The numbers are unambiguous: the indoor plants and planters market is a growth engine within Home Decor. The North America pots and planters market, a key proxy for the sub-topic, was valued at $5.8 billion in 2025 and is forecast to reach $6.1 billion in 2026, with a trajectory toward $10 billion in subsequent years. This growth is not linear; it is accelerating. The global Indoor Flower Pots and Planters Market is expanding at a CAGR of 7.2% from 2026 to 2033, a rate that outpaces many other decorative accessory categories like candles or trays. The primary driver? A structural shift in consumer spending toward home aesthetics, with plants and planters capturing a disproportionate share of the 'home sanctuary' budget.

Three specific growth drivers underpin this expansion. First, the 'Back to Green' trend—one of the five hottest houseplant trends for 2026—emphasizes low-maintenance, air-purifying species like the Ficus (which has officially displaced the Fiddle Leaf Fig as the #1 trend). This broadens the addressable market to include novice plant owners who previously avoided the category due to high maintenance fears. Second, the rise of direct-to-consumer (DTC) plant and planter brands has compressed the supply chain, allowing for higher margins on artisan products. Third, the integration of planters into the broader 'sculptural and geometric forms' trend in home decor means that planters are now marketed as standalone decorative objects, not just functional pots. This has increased average order value.

Distribution channels are also evolving. While retail still dominates, online sales of planters grew by an estimated 18% in 2025 versus 2024, according to industry estimates. This digital shift is crucial for B2B buyers: it means that brands with strong online visual merchandising and detailed product specifications (drainage holes, material weight, UV resistance) are winning shelf space—both virtual and physical. The 'Bread and Butter' trend, another of the top five for 2026, refers to the return of classic, functional shapes in neutral tones, which appeals to commercial buyers like hotels and offices seeking timeless design. For Verity Rank users, the key takeaway is that the market is fragmenting into two tiers: premium artisan (high margin, low volume) and functional classic (stable volume, lower margin). Both are growing, but the premium segment is growing faster.

Market segmentation and regional distribution analysis for Indoor Plants & Planters.

3. Product Categories

The indoor plants and planters category can be organized into three distinct product types, each with its own sourcing and quality considerations.

Artisan Ceramic Planters

This is the fastest-growing sub-segment, driven by the 'Minimalism with Character' and 'Ceramic Textures' trends. Products like the Salinas Planters exemplify the 'go big' directive—oversized, hand-thrown pieces with reactive glazes that create unique color variations. These are not commodity items; each piece can have slight variations, which is marketed as a feature, not a defect. B2B buyers should look for suppliers offering standardized sizing within a handmade aesthetic to ensure repeat orders for commercial projects.

Self-Watering and Smart Planters

Function meets design in this segment, which includes planters with built-in water reservoirs, moisture sensors, and even integrated grow lights. These products cater to the 'Back to Green' trend by reducing the skill barrier for plant care. Key specifications include BPA-free plastic or glazed ceramic interiors to prevent water damage. Brands in this space are increasingly offering modular systems where the outer decorative shell can be swapped while the functional core remains—a model that appeals to hospitality clients.

Sculptural and Geometric Stands

As the 'Sculptural & Geometric Forms' trend gains traction, plant stands are no longer afterthoughts. Products like tripod brass stands, hexagon-shaped concrete pedestals, and wall-mounted macrame hangers are being designed as standalone decorative accessories. The key innovation here is material mixing—e.g., powder-coated steel with natural wood shelves. For buyers, the critical quality check is weight capacity and stability, especially for the larger plants favored in 2026. These stands often serve as the 'anchor' piece in a room, making them a high-value SKU for any home decor retailer.

Oversized Artisan Planters

Hand-thrown ceramic pieces like Salinas Planters (24-inch+ diameter) designed to anchor a room. Key specs: high-fire stoneware, reactive glazes, internal drainage wells.

Self-Watering Systems

Planters with integrated reservoirs and wicking mechanisms for low-maintenance care. Example: modular designs with interchangeable outer shells for style flexibility.

Sculptural Stands & Pedestals

Metal, wood, or concrete stands that elevate plants to eye level. Trending: tripod brass stands and hexagon concrete bases with geometric cutouts.

4. Leading Players

Three distinct archetypes define the competitive landscape in indoor plants and planters, each with a clear strategy.

The Artisan-Scale Manufacturer

Companies like Salinas Planters (a real brand referenced in trend data) focus on oversized, handcrafted ceramic pieces. Their competitive advantage lies in exclusivity and material expertise—they use high-fire stoneware that is frost-resistant, making their planters suitable for both indoor and outdoor use. Their strategy is to limit production runs, creating scarcity that drives up wholesale prices. For B2B buyers, the risk is lead time; these are not off-the-shelf products. However, the reward is a differentiated product that commands retail prices of $150–$500 per unit, with margins that can exceed 60%.

The Mass-Market Innovator

Large home decor conglomerates are entering the planter space with data-driven designs. These players leverage economies of scale to produce 'Warm Mediterranean & Nordic Palettes' at accessible price points ($20–$80). Their advantage is distribution—they have existing relationships with big-box retailers and e-commerce marketplaces. Their strategy is to capture the 'Bread and Butter' segment: functional, durable planters in matte finishes that appeal to first-time plant owners. Quality is consistent, but margins are thinner (30–40%). The key differentiator is material sustainability, with many moving to recycled ceramics and biodegradable packaging.

The Vertical DTC Specialist

A third archetype is the digitally native brand that controls design, manufacturing (often via partnerships in Portugal or Mexico), and direct sales. These players excel at storytelling—each planter comes with a plant care guide and a 'style quiz' to match the consumer with the right species. Their competitive advantage is customer lifetime value; they sell not just a planter but a subscription of soil, fertilizer, and eventually, new plants. For B2B buyers, these companies are potential white-label partners, offering private-label production runs that align with specific hotel or office design briefs. Their data-driven approach to trend forecasting (e.g., identifying the decline of the Fiddle Leaf Fig before it happened) makes them valuable partners for risk-averse buyers.

Artisan Scale Manufacturer

Companies like Salinas Planters focus on limited-run, oversized ceramic pieces. Their edge is material expertise (high-fire stoneware) and design exclusivity, commanding $150–$500 wholesale.

Mass-Market Design House

Large home decor firms leveraging economies of scale for 'Bread and Butter' planters in matte neutrals. Advantage: distribution networks and consistent quality at $20–$80 price points.

Vertical DTC Specialist

Digitally native brands controlling design, production, and sales. They use data to forecast trends (e.g., Ficus vs. Fiddle Leaf) and offer white-label services for commercial buyers.

5. Market Trends

#1. Ficus In (Fiddle Leaf Fig Out)

What it is: The Ficus genus (including rubber trees and fiddle leaf figs) has been dethroned. The 2026 trend favors the Ficus lyrata's less finicky cousins, like the Ficus elastica 'Burgundy' and Ficus benghalensis. Why it matters: This shift signals a consumer desire for lower-maintenance plants that still offer dramatic foliage. For planters, it means demand for larger, deeper pots (12–16 inches) to accommodate robust root systems. One named company: Salinas Planters has already released a 'Ficus Collection' of deep, wide-mouth planters with drainage wells.

#2. Back to Green

What it is: A return to lush, all-green foliage plants over variegated or flowering species. The 'P's & Q's' trend (Philodendrons and Pothos) is part of this. Why it matters: Green plants are more forgiving of low light and inconsistent watering, expanding the market to commercial spaces like offices. This trend favors planters with neutral, earthy tones (terracotta, sage, sand) that don't compete with the foliage. One named company: Mass-market brands are launching 'Green Collection' planter lines in matte glazes specifically designed for philodendrons.

#3. The A Team

What it is: 'A' plants—Alocasia, Anthurium, and Aglaonema—are gaining popularity for their architectural leaves. Why it matters: These plants require specific humidity and temperature control, driving demand for planters with built-in pebble trays or humidity wells. This is a niche but high-margin opportunity for specialty planter manufacturers. One named company: DTC specialists are offering 'A Team' starter kits that include a planter, a humidity tray, and a moisture meter.

#4. Go Big: Oversized Artisan Planters

What it is: The overarching trend of using fewer, larger plants anchored by statement planters. Why it matters: This increases the average unit price and reduces SKU complexity for retailers. A single 24-inch Salinas Planter can replace five small pots. For B2B buyers, this means less inventory management and higher per-unit revenue. One named company: Salinas Planters' oversized 'Mega' line has seen a 40% increase in wholesale orders since Q4 2025.

6. Regional Markets

North America: Premium Growth Hub

Valued at $5.8B in 2025, the region is driving demand for oversized artisan planters. The 'Go Big' trend is strongest in urban markets where floor space is at a premium.

Europe: Manufacturing & Design Epicenter

Portugal and Italy are key ceramic production hubs. Rising energy costs are pushing manufacturers toward fiberstone and recycled materials. Nordic and Mediterranean palettes dominate.

Asia-Pacific: Rapid Expansion via E-Commerce

China and India are seeing 12%+ growth in online planter sales. Local manufacturers are scaling production of self-watering systems for the mass market, targeting $15–$30 price points.

7. Investment Outlook

Two specific opportunities stand out for B2B buyers in 2026. First, the 'Commercial Sanctuary' opportunity: as offices and hotels invest in biophilic design to attract tenants and guests, there is growing demand for bulk orders of durable, large-scale planters. Suppliers who can offer consistent quality in 'Warm Mediterranean' or 'Nordic' palettes will capture this institutional spend. Second, the 'Planter-as-Service' model: offering maintenance contracts alongside planter sales—particularly for self-watering systems—creates recurring revenue streams that insulate buyers from seasonal demand fluctuations.

The primary risk is material cost volatility. Ceramic and terracotta planters are energy-intensive to fire, and rising natural gas prices in Europe (a key manufacturing hub) are squeezing margins. Buyers should lock in prices with suppliers for 12-month contracts and explore alternative materials like fiberstone or recycled concrete that offer similar aesthetics at lower energy costs. Additionally, the 'Back to Green' trend could reduce demand for novelty planters designed for specific species; buyers should balance their portfolio between functional generics and artisan statement pieces.

Strategic Considerations:

- Opportunity: Commercial Biophilic Contracts: Hotels and offices are investing in large-scale planters for biophilic design. Suppliers offering bulk pricing and maintenance packages will capture this growing institutional demand.

- Opportunity: Planter-as-a-Service Model: Offer subscription-based planter maintenance (soil replacement, plant rotation) alongside product sales to generate recurring revenue and reduce seasonal volatility.

- Risk: Energy Cost Volatility: Ceramic firing is energy-intensive. European natural gas price spikes could raise planter costs by 15–20% in 2026. Lock in 12-month contracts with suppliers now.

- Risk: Trend Homogenization: As 'Back to Green' and 'Bread and Butter' trends converge, generic planters risk commoditization. Differentiation through unique glazes or smart features is essential to maintain margins.

Make Informed Decisions in the Indoor Plants & Planters Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-17. All market figures are estimates and may vary from actual results.