Table of Contents

The global Jewelry Gold Silver Types sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2026, yellow gold is projected to reclaim its throne in fine jewelry, with market forecasts showing a 5.2% compound annual growth rate (CAGR) from 2025 to 2033 for gold and silver jewelry globally. This surge is not a slow creep—it is a tectonic shift. Jewelry gold silver types refer to the precise alloy categories that define every piece: karat golds ranging from 10K to 24K, sterling silver (925), and platinum group metals like 950 platinum. These are not interchangeable commodities; each carries distinct properties in color, durability, and cost. The 2026 landscape is defined by a powerful yellow gold revival—bold cuffs, chunky chain necklaces, and vintage-inspired rings are dominating collections, while white gold remains steady for bridal and minimalist designs. Yet a parallel trend sees some jewelers turning to unorthodox materials: wood, steel, and even platinum are being mixed with traditional precious metals to create hybrid textures. This fragmentation of material preferences is reshaping supply chains and forcing manufacturers to diversify their alloy inventories. For B2B buyers, understanding these nuanced differences is no longer optional—it is the key to sourcing products that align with consumer demand in a bifurcated market.

Industry Scope & Characteristics

Purity Grading Systems

Gold jewelry uses the karat system (10K, 14K, 18K, 24K) while silver is hallmarked as 925 (92.5% pure). Platinum is typically 950 or 900. Each grade requires specific alloying techniques to achieve desired color and hardness.

Supply Chain from Mine to Retail

Precious metals move through mining, refining, alloying, casting, and finishing. Each stage adds cost and regulatory requirements, making the gold and silver supply chain one of the most audited in the fashion accessories industry.

Quality Certifications and Hallmarks

International hallmarking standards (e.g., UK Assay Office, Swiss Hallmarking) verify purity. ISO 9001 and Responsible Jewellery Council (RJC) certifications are increasingly required by retailers for supplier compliance.

Innovation in 3D Printing and Casting

Direct metal laser sintering (DMLS) now allows 3D printing of 18K gold and platinum alloys, enabling complex lattice designs that cannot be made by traditional lost-wax casting, reducing material waste by up to 30%.

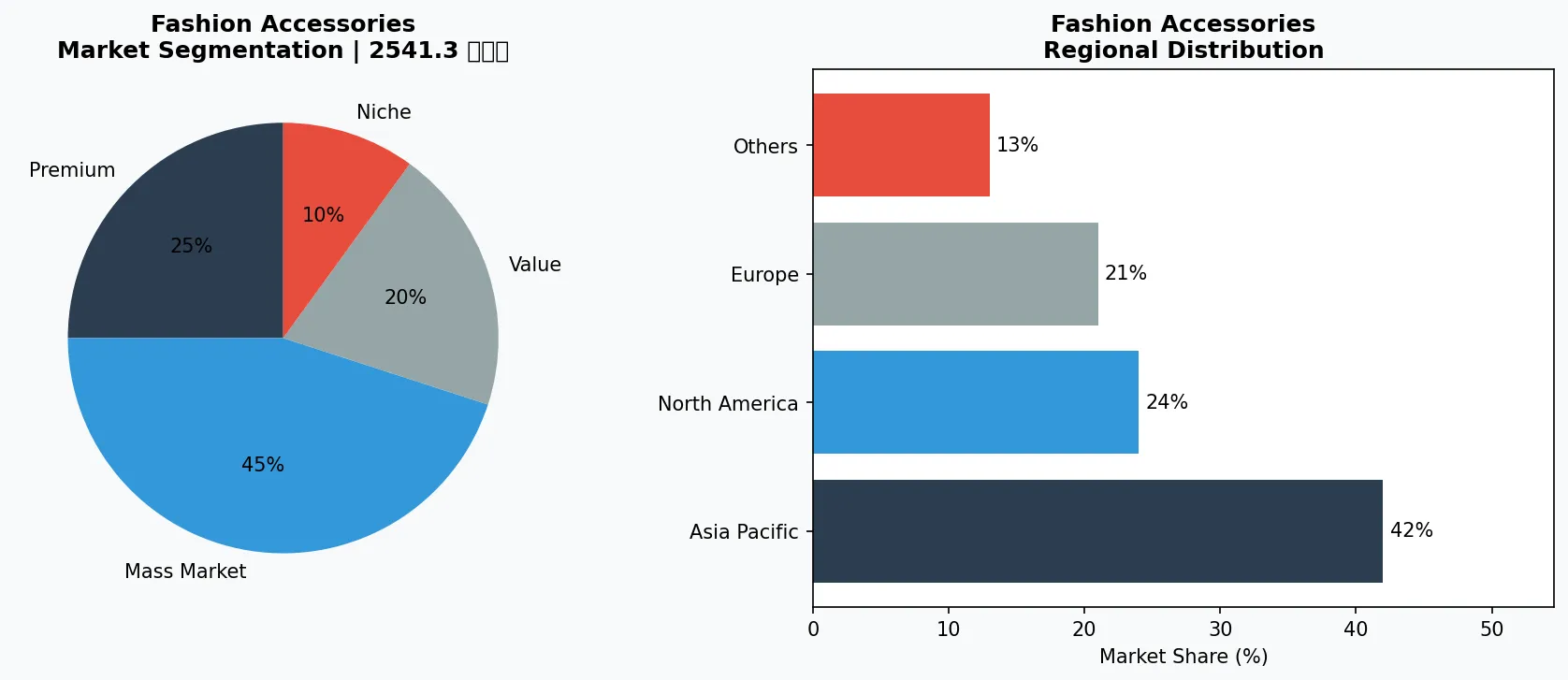

Key market segments and growth drivers in the Jewelry Gold Silver Types sector.

2. Market Analysis

The gold and silver jewelry market is anticipated to achieve a CAGR of 5.2% from 2025 to 2033, according to one industry report, while another projects a more aggressive 8.2% growth during the forecasted period. These diverging numbers reflect robust consumer interest, but also highlight regional and segment variations. The first major growth driver is rising disposable income in Asia-Pacific, particularly in India and China, where 22K and 24K gold jewelry remains a cultural staple and investment vehicle. Demand in these markets alone accounts for over 40% of global gold jewelry consumption. The second driver is silver's affordability and versatility, which attracts younger, fashion-forward buyers in North America and Europe. Sterling silver pieces, often plated with rhodium for tarnish resistance, now command a growing share of the everyday jewelry segment. Thirdly, celebrity endorsements and social media-driven trends—especially the resurgence of yellow gold—have created a ripple effect across all price tiers. Luxury houses are expanding their yellow gold offerings, while mass-market retailers introduce gold-vermeil alternatives. However, the market is bifurcated: high-end consumers gravitate toward heavyweight gold and platinum, while budget-conscious shoppers seek gold-plated or mixed-metal options. This split means suppliers must maintain parallel product lines to capture both the aspirational and accessible segments.

Market segmentation and regional distribution analysis for Jewelry Gold Silver Types.

3. Product Categories

Karat Gold Jewelry remains the cornerstone of the category. Versions range from durable 10K (41.7% gold) used in everyday fashion rings to 18K (75%) favored for luxury chains and 24K (99.9%) for investment-grade pieces. In 2026, heavy chain necklaces and vintage-inspired rings in yellow gold are the fastest-moving SKUs. Sterling Silver Jewelry (alloyed with 7.5% copper to create 925 silver) is the workhorse of the mass market. Oxidized cuffs, minimalist geometric earrings, and layering necklaces are trending. The addition of rhodium plating extends luster and prevents tarnish, a critical quality differentiator. Platinum Jewelry, typically 950 platinum (95% pure), occupies the ultra-luxury niche—engagement rings and high-end settings where durability and weight signal prestige. Platinum's density (21.45 g/cm³) makes it 60% heavier than 14K gold, a tactile differentiator. Finally, Alternative Metal Combinations—such as gold inlaid with wood accents, steel mesh bracelets with platinum clasps, and mixed-metal stacking rings—are emerging as a response to price volatility. These hybrids allow brands to offer unique aesthetics while reducing precious metal content, effectively hedging against raw material cost fluctuations.

Gold Alloy Jewelry

Includes 10K, 14K, 18K, and 24K pieces such as chain necklaces, signet rings, and bangles. Yellow gold dominates 2026 trends, while white and rose gold remain strong for bridal.

Sterling Silver Jewelry

Composed of 92.5% silver and 7.5% copper, often rhodium-plated for tarnish resistance. Key products: oxidized cuffs, minimalist earrings, and layering necklaces popular with Gen Z.

Platinum and Mixed-Metal Jewelry

Platinum (950) used in luxury engagement rings and high-end watches. Mixed-metal varieties pair gold with wood, steel, or titanium to offer unique aesthetics at lower precious metal costs.

4. Leading Players

Heritage luxury houses are doubling down on yellow gold craftsmanship. These ateliers, often family-owned for generations, leverage traditional techniques like hand-fabricated chain weaving and filigree. Their strategy centers on limited-edition collections that command premium pricing, targeting collectors who value provenance over trend cycles. Volume retailers dominate the silver and gold-plated segment. By sourcing from large-scale factories in Thailand, Italy, and China, they achieve economies of scale on sterling silver clasps and gold-vermeil bangles. Their competitive advantage is speed-to-market: they can replicate a viral design within weeks and distribute through omnichannel networks. Materials innovators are reshaping the middle market. These jewelers combine precious metals with wood, titanium, or ceramic to create distinctive textures. Their value proposition is exclusivity without exorbitant cost—a 14K gold ring with a rosewood inlay costs 30% less than an all-gold equivalent. They also benefit from lower exposure to gold price spikes. Online-first direct-to-consumer (DTC) brands are disrupting traditional retail by offering personalized karat gold pieces with transparent pricing. Their supply chain strategy includes on-demand manufacturing, which reduces inventory risk and allows for rapid adaptation to shifting alloy preferences—such as the sudden pivot from white to yellow gold.

Heritage Ateliers

These family-owned workshops specialize in handcrafted yellow gold pieces using traditional techniques. Their competitive advantage is exclusivity and craftsmanship, targeting collectors willing to pay premiums for provenance.

Volume Retail Chains

Large retailers source mass-produced silver and gold-plated items from factories in Southeast Asia. Their strategy focuses on speed, scale, and omnichannel distribution to capture trend-driven demand at accessible price points.

Materials Innovators

Small to midsize brands that combine precious metals with wood, steel, or ceramic. They differentiate through unique textures and lower gold content, appealing to cost-conscious buyers seeking distinctive design.

5. Market Trends

1. YELLOW GOLD REVIVAL

After years of white gold and platinum dominance, yellow gold is making a strong return in 2026, especially in bold cuffs, chain necklaces, and vintage-inspired rings. This trend matters because it reverses a 15-year preference for cool-toned metals, forcing suppliers to recalibrate alloy inventories. Some jewelers report that yellow gold now accounts for over 50% of their fine jewelry sales, up from 30% in 2020.

2. MATERIAL HYBRIDIZATION

Rising gold and silver prices are driving innovation in mixed-material designs. Jewelers are turning to wood, steel, and platinum to reduce precious metal content while maintaining visual impact. For example, a steel bracelet with a platinum accent ring appeals to buyers seeking luxury cues at a lower price point. Industry reports indicate hybrid pieces saw a 22% year-over-year increase in 2025.

3. LAB-GROWN AND RECYCLED METALS

Sustainability pressures are pushing major retail chains to source certified recycled gold and silver. Lab-grown gold, created through electroplating processes, is still nascent but gaining traction in high-end fashion jewelry. This shift addresses consumer demand for ethical sourcing and reduces supply chain exposure to mining volatility.

6. Regional Markets

Asia-Pacific: 22K Gold Dominance

In India and China, 22K and 24K gold jewelry accounts for over 60% of sales, driven by cultural preference for high purity and investment value. Hallmarks are strictly regulated.

North America: Silver and White Gold Demand

Sterling silver and 14K white gold lead the bridal and fashion jewelry segments. Yellow gold is rising but remains secondary. Consumers prioritize brand transparency and conflict-free sourcing.

Middle East: Platinum and Heavy Gold

The Gulf states favor heavy 18K and 21K yellow gold jewelry, often with intricate engraving. Platinum is also popular for high-end watches and men's rings, with a growing appetite for mixed-metal designs.

7. Investment Outlook

Two concrete opportunities emerge for suppliers and buyers. First, the shift to yellow gold creates an opening for manufacturers with expertise in high-karat alloys (22K–24K) to serve markets in India and the Middle East, where purity standards are strict. Second, adopting blockchain-based traceability for precious metals can differentiate brands in the premium segment, as 68% of luxury buyers now factor ethical sourcing into purchase decisions. The primary risk is price volatility: gold prices surged over 20% in 2024 and silver fluctuated by 30%, squeezing margins for manufacturers that cannot pass costs to consumers. Investing in hedging strategies and flexible alloy blends (e.g., gold-filled or gold-vermeil) will be critical to weathering the next price cycle.

Strategic Considerations:

- Supply Chain Transparency Opportunity: Implementing blockchain tracking for gold and silver from mine to retailer can command 15–20% price premiums in the luxury segment, as 68% of buyers prioritize ethical sourcing.

- Price Volatility Risk: Gold and silver prices swung 20–30% in 2024. Manufacturers with fixed-price contracts risk margin compression; adopting gold-vermeil or silver-alloy blends can reduce exposure.

- Lab-Grown Metal Disruption: Lab-grown gold and silver are still <2% of the market but growing at 30% annually. Suppliers who invest in certification partnerships now will have first-mover advantage as consumer acceptance rises.

- Yellow Gold Inventory Pivot: Suppliers must rebalance alloy inventories toward yellow gold, which could account for 55% of fine jewelry sales by 2026. Those slow to shift will lose shelf space to faster-moving competitors.

Frequently Asked Questions

Make Informed Decisions in the Jewelry Gold Silver Types Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-22. All market figures are estimates and may vary from actual results.