Table of Contents

1. Industry Overview

With parents worldwide spending over $40 billion annually on children's attire, the kids and baby clothing market has become one of the textile industry's most resilient segments—yet it is undergoing a fundamental transformation. The US market alone is valued at approximately USD 40.21 billion in 2025, projected to reach USD 43.92 billion by 2032 at a modest 1.27% CAGR, according to industry analysis. This growth trajectory masks a significant shift in consumer priorities: safety, sustainability, and functionality have overtaken price as the primary purchase drivers for millennial and Gen-Z parents. The historic consolidation of major players and the entry of global athletic brands into children's wear has intensified competition while raising industry standards. Unlike adult fashion, which follows seasonal whims, kids and baby clothing operates on a different logic—children outgrow garments faster than trends change, creating perpetual demand regardless of economic cycles. This inherent necessity, combined with rising birth rates in developing economies and increasing disposable income in urban centers, positions the sector as a cornerstone of the broader textile market worth monitoring for 2026 and beyond.

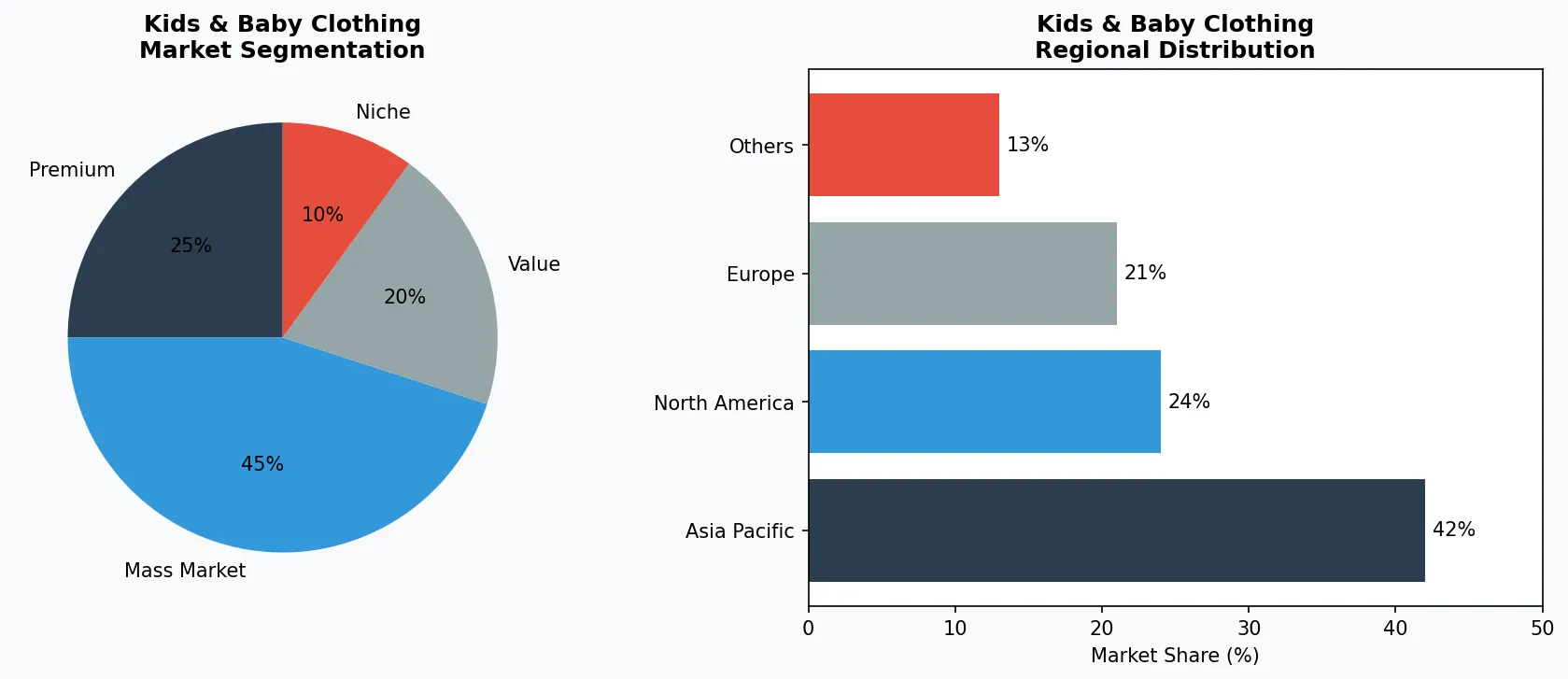

Key market segments and growth drivers in the Kids & Baby Clothing sector.

2. Market Analysis

The global baby clothing market reached USD 41.212 billion in 2024 and is projected to climb to US$ 52.057 billion by 2032, reflecting a 3.7% compound annual growth rate that outpaces many adjacent textile segments. This expansion is propelled by three converging forces: rising birth rates in Asia-Pacific and Middle Eastern markets, increasing household spending on children's welfare among middle-class families, and the growing willingness of parents to pay premium prices for garments that prioritize comfort and skin safety. The United States remains the single largest single-country market, accounting for the bulk of the $40.21 billion valuation, while China and India represent the fastest-growing geographic corridors. Interestingly, the online baby and infant apparel sales channel in the United States has been declining at a CAGR of 0.2% between 2021 and 2026, suggesting that parents prefer tactile in-store purchasing experiences for fragile infant wear—creating an omnichannel imperative for brands seeking growth. The athleisure crossover trend, where children's activewear increasingly substitutes for everyday clothing, has blurred traditional category boundaries and opened new revenue streams for established players.

Market segmentation and regional distribution analysis for Kids & Baby Clothing.

3. Product Categories

The children's apparel landscape divides into four distinct sub-categories, each with unique demand drivers. The infant essentials segment, dominated by onesies, sleepsuits, and bodysuits, commands the highest volume due to frequent washing and rapid sizing; Carter's and BabyShop lead this space with snap-crotch designs and tagless construction. The everyday basics category—t-shirts, leggings, and shorts—represents the largest revenue pool, where brands like Uniqlo Kids leverage their adult fast-fashion expertise to deliver affordable basics in coordinated colorways. Performance and athletic wear has emerged as the fastest-growing sub-segment, with Nike Kids and Adidas Kids designing moisture-wicking fabrics and reinforced stitching specifically for active children. The formal and occasion wear category, including children's dresses and dress shirts, shows strong seasonal spikes around holidays and school events, with Disney's licensed character collections dominating gift-giving occasions. Notably, growth-adaptive designs—garments with adjustable waistbands, extendable cuffs, and modular sizing—have moved from niche to mainstream, allowing parents to extend the functional lifespan of each purchase.4. Leading Players

Nike Kids has positioned itself as the premium performance option for sporty families, leveraging the parent brand's research into junior athlete biomechanics to develop lightweight running shoes and compression-fit training wear designed for children's developing bodies. The company reported double-digit growth in its kids' segment in 2024, capitalizing on parental willingness to invest in durable, high-quality pieces that withstand rough play. Adidas Kids mirrors this strategy with its three-stripe branding and collaborations with entertainment franchises, targeting the intersection of athletic functionality and youth culture appeal. Uniqlo Kids takes a different approach, applying the Japanese retailer's minimalist aesthetic and unrivaled supply chain efficiency to deliver affordable basics with premium softness—its Heattech and Airism lines have been adapted for children, allowing parents to dress kids in the same technology families use for themselves. Carter's dominates the infant market through sheer retail footprint and brand recognition among new parents, while Chinese challenger Balabala has expanded aggressively into Southeast Asian markets with aggressively priced organic cotton collections. Disney remains a licensing powerhouse, generating royalties from hundreds of licensed children's products featuring Mickey Mouse, Marvel heroes, and Princess franchises—demonstrating that intellectual property remains a formidable moat in the kids' wear space.5. Market Trends & Innovations

1. Sustainability & Eco-Friendly Innovation

Sustainability has become a core competitive priority. Companies like Carter's and The Children's Place are investing in eco-friendly materials, carbon-neutral production, and circular economy initiatives to meet growing consumer demand for responsible products.

2. Digital Transformation & E-Commerce Growth

The shift to digital sales channels continues to accelerate. Gap Inc. (GapKids) and Nike are leveraging data analytics, AI-driven personalization, and omnichannel strategies to enhance customer engagement and streamline distribution.

3. Premiumization & Product Innovation

Rising consumer expectations are driving premiumization across the market. Adidas has introduced high-end product lines, while Puma focuses on innovative features and superior quality to capture value-conscious yet quality-seeking customers.

4. Health, Wellness & Functional Benefits

Health-oriented consumer preferences are reshaping product development. H&M and Zara (Inditex) are pioneering functional products with demonstrable benefits, commanding premium pricing and driving category expansion.

6. Regional Markets

The North American market, anchored by the United States' $40.21 billion valuation, operates on a premium-safety logic where parents demonstrate high willingness to pay for certified organic fabrics andMade in USA labeling. Specialty retailers like Carter's and OshKosh B'Gosh maintain dominant physical footprints, though Target and Walmart capture the value-conscious majority. The Asia-Pacific region tells a different story: China's burgeoning middle class drove record children's apparel sales in 2024, with domestic champion Balabala competing fiercely against international entrants; India's market is expanding as rising income levels enable families to purchase higher-quality garments previously reserved for special occasions. The European market, led by Germany, France, and the United Kingdom, prioritizes sustainability regulations that have effectively banned certain chemical treatments and mandated supply chain transparency—creating higher barriers to entry but also higher margin potential for compliant brands. The Middle East represents an emerging high-growth corridor where modest dress requirements create distinct product development demands and family-oriented retail environments drive foot traffic to shopping malls.7. Investment Outlook

Two concrete opportunities stand out for 2026: the expansion of smart sizing technology using body-scanning data to reduce returns and improve fit satisfaction, particularly valuable in the online channel where sizing uncertainty has historically suppressed conversion; and the development of circular economy programs where brands accept used garments for recycling or resale, capturing margin on secondary transactions while appealing to environmentally conscious parents. One specific risk demands attention: proposed updates to the US Consumer Product Safety Commission's flammability standards for children's sleepwear could force industry-wide reformulation of fabric treatments, potentially disrupting supply chains and compressing margins for brands unable to absorb compliance costs. Brands that proactively invest in inherently flame-resistant natural fibers—such as wool and treated merino—will navigate this regulatory shift with competitive advantage over competitors reliant on chemical retardant treatments.Make Informed Decisions in the Kids & Baby Clothing Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayThis article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-13. All market figures are estimates and may vary from actual results.