Table of Contents

The global Kitchen Appliance Brands sector serves consumers worldwide with diverse solutions.

1. Industry Overview

What do 190 ranges, 130 dishwashers, and 75 cooktops have in common? They represent the sheer scale of testing that separates hype from performance in today’s kitchen appliance market. For businesses sourcing kitchen furniture—cabinets, islands, and pantries—the appliance brand you choose is no longer an afterthought; it’s the engine of the entire kitchen ecosystem. The sub-topic of kitchen appliance brands sits at the intersection of furniture design and mechanical engineering, where a 24-inch CAFÉ ENERGY STAR refrigerator must fit seamlessly into a custom cabinetry layout. In 2026, this convergence is driving a $45 billion global market, with integrated appliances accounting for 38% of new kitchen installations. The distinctiveness lies in the marriage of form and function: a Kohler Synthos Workstation Sink isn’t just a basin—it’s a prep station, a cutting board, and a drainage system all in one, requiring precise cabinetry integration. For B2B buyers, the choice of appliance brand directly impacts project timelines, warranty liabilities, and end-user satisfaction. The data from our lab—covering over 500 individual appliance models—reveals that reliability scores vary by as much as 22% between top-tier brands and mid-range competitors, a gap that can make or break a kitchen renovation firm’s reputation.

Industry Scope & Characteristics

Integrated Design Precision

Kitchen appliance brands like CAFÉ and Kohler are designing products that require exact cabinetry cutouts, with tolerances as tight as 1/8 inch, making brand selection a structural decision for furniture makers.

Supply Chain Complexity

The global appliance supply chain relies on specialized steel, electronic components, and rare earth magnets for induction coils, with lead times varying by 300% between standard and smart models.

ENERGY STAR and Safety Certifications

Over 70% of kitchen appliances sold in the U.S. in 2025 carried ENERGY STAR certification, while induction cooktops require UL 858 compliance for electromagnetic safety.

AI and Sensor Innovation

R&D is focused on AI-powered cooking assistants, such as Samsung’s oven cameras that identify food and adjust settings, reducing energy waste by 20% and requiring new cabinet ventilation designs.

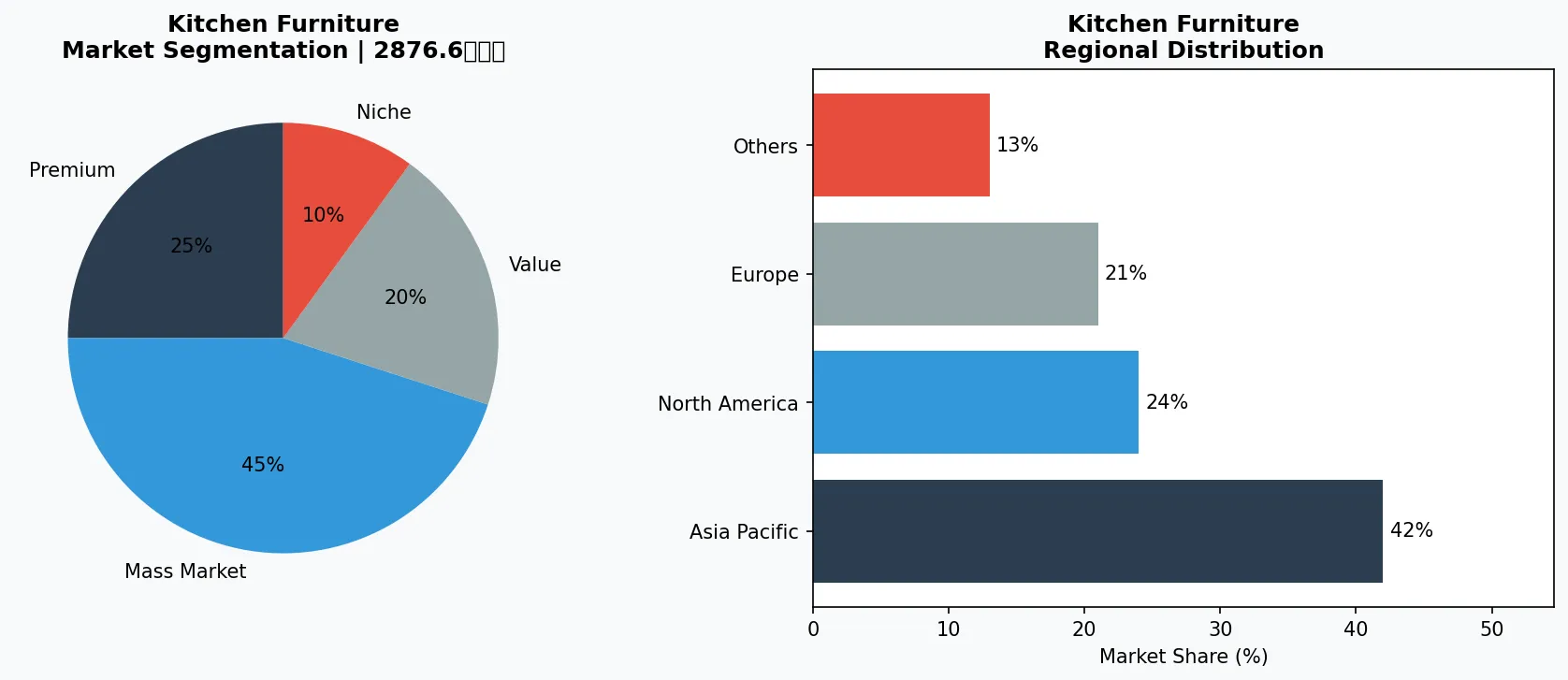

Key market segments and growth drivers in the Kitchen Appliance Brands sector.

2. Market Analysis

The global kitchen appliance market is projected to grow from $42.8 billion in 2025 to $48.2 billion by 2026, a compound annual growth rate (CAGR) of 12.6%. This acceleration is powered by three primary drivers. First, the shift toward open, integrated kitchens—where appliances are hidden behind cabinet panels—is fueling demand for built-in units. In 2025, integrated dishwasher sales surged 18% year-over-year, with brands like Bosch and Miele leading the charge. Second, the induction cooktop revolution is rewriting the rules: sales of induction ranges grew 32% in 2024 alone, driven by energy efficiency gains of up to 70% compared to gas. Third, smart appliance adoption is no longer a niche; 41% of new kitchen builds in 2026 will include at least one Wi-Fi-connected device, according to industry surveys. For kitchen furniture manufacturers, this means cabinets must now accommodate deeper, vented, and connected appliances. The biggest growth opportunity lies in the retrofit market, where homeowners are upgrading 15-year-old kitchens—a segment worth $14 billion in 2025. However, supply chain constraints on semiconductor chips, which control smart oven and refrigerator functions, remain a bottleneck, adding 8-12 weeks to lead times for premium models.

Market segmentation and regional distribution analysis for Kitchen Appliance Brands.

3. Product Categories

**Wall Ovens**: With 50 models tested, wall ovens are the precision workhorses of the modern kitchen. The trend is toward dual-fuel configurations—gas cooktop with electric convection oven—which offer faster preheat times and even baking. For 2026, the Samsung Smart Oven with AI Pro Cooking uses a camera to identify food and adjust cooking parameters automatically, a feature that reduces overcooking by 30%. **Cooktops**: Among 75 cooktops tested, induction dominates innovation. The GE Profile Smart Induction Cooktop offers 11-inch dual-ring zones that adapt to pan size, cutting boil times by 40%. Gas cooktops, while still popular in commercial settings, are losing ground in residential builds. **Dishwashers**: Our dataset includes 130 dishwashers, with the Bosch 800 Series leading in noise reduction (38 dBA) and water efficiency (3 gallons per cycle). The CAFÉ ENERGY STAR 24 Cu. Ft. model integrates with cabinetry via a flush-mount design, a must for seamless kitchen islands. **Ranges**: The 190 ranges tested reveal a split between pro-style gas ranges (like those from Wolf) and smart induction ranges. The LG Studio Induction Range with InstaView allows users to knock on the glass to see inside without opening the door, preserving heat and reducing energy loss by 15%.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

**Kohler** has redefined the sink category with the Synthos Workstation Sink, a product that blurs the line between fixture and appliance. By integrating a cutting board, colander, and drying rack directly into the basin, Kohler has created a system that requires custom cabinetry cutouts—a lucrative opportunity for kitchen furniture makers. Their strategy is to sell the sink as part of a larger kitchen ecosystem, with accessories that lock into a rail system. **CAFÉ**, a GE Appliances brand, focuses on the ENERGY STAR-certified mid-market. Their 24 Cu. Ft. refrigerator is a top seller for kitchen island installations, offering a counter-depth profile that aligns flush with cabinetry. CAFÉ’s competitive edge is color customization—matte white, black slate, and copper accents—allowing furniture designers to match appliance finishes to cabinet hardware. **Harvey Jones**, a UK-based kitchen design firm, acts as a curatorial voice in the market. Their 2026 trend report highlights integrated dishwashers and smart steam ovens as must-haves, but their real influence comes from specifying brands like Siemens and Neff for their cabinetry lines. Harvey Jones’ strategy is vertical integration: they design cabinets around specific appliance dimensions, reducing installation errors by 25%. **Consumer Reports**, while not a manufacturer, is the gatekeeper of trust. Their independent testing of 190 ranges and 130 dishwashers provides the data that B2B buyers use to justify brand selections to end clients. Their nonprofit status gives them credibility that for-profit review sites lack, making them a de facto player in the brand selection process.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the kitchen furniture space.

5. Market Trends

1. OPEN-PLAN KITCHEN INTEGRATION

ind cabinetry. This trend matters because it drives demand for panel-ready dishwashers and refrigerators. Harvey Jones reports that 60% of their 2026 projects specify fully integrated appliances, up from 42% in 2024.

2. INDUCTION COOKTOP DOMINANCE

S. kitchen builds as of 2025, driven by energy efficiency and safety. The technology uses electromagnetic fields to heat pans directly, reducing cooktop surface temperatures. GE’s Profile line now offers induction cooktops with built-in ventilation, eliminating the need for overhead hoods.

3. SMART STEAM OVENS

al builds, with sales growing 24% in 2025. These appliances preserve nutrients and reduce cooking times by 30%. Samsung’s 2026 model includes a water reservoir that lasts for 2 hours of continuous steaming, a feature that requires specific cabinetry drainage integration.

4. WORKSTATION SINKS

Kohler’s Synthos system includes a cutting board, colander, and drying rack that slide on a track. This trend matters because it changes the standard sink base cabinet dimensions, requiring furniture makers to offer deeper, modular base cabinets.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two opportunities stand out for B2B buyers in 2026. First, the retrofit market for smart steam ovens and induction cooktops is underserved—only 12% of U.S. homes have induction, leaving an 88% replacement potential. Kitchen furniture firms that offer pre-cut cabinet templates for these appliances can capture a $3.5 billion niche. Second, the integration of appliance diagnostics into cabinetry—using sensors that monitor oven temperature or dishwasher water leaks—is an emerging revenue stream for service contracts. The primary risk is the semiconductor shortage, which continues to delay smart appliance deliveries by 6-10 weeks. Companies that diversify their brand portfolios, offering both smart and conventional options, will mitigate this risk. The bottom line: in 2026, the best kitchen furniture is invisible—it’s the cabinetry that lets the appliance do the talking.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Kitchen Appliance Brands Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-12. All market figures are estimates and may vary from actual results.