Table of Contents

The global Kitchen Cabinet Materials sector serves consumers worldwide with diverse solutions.

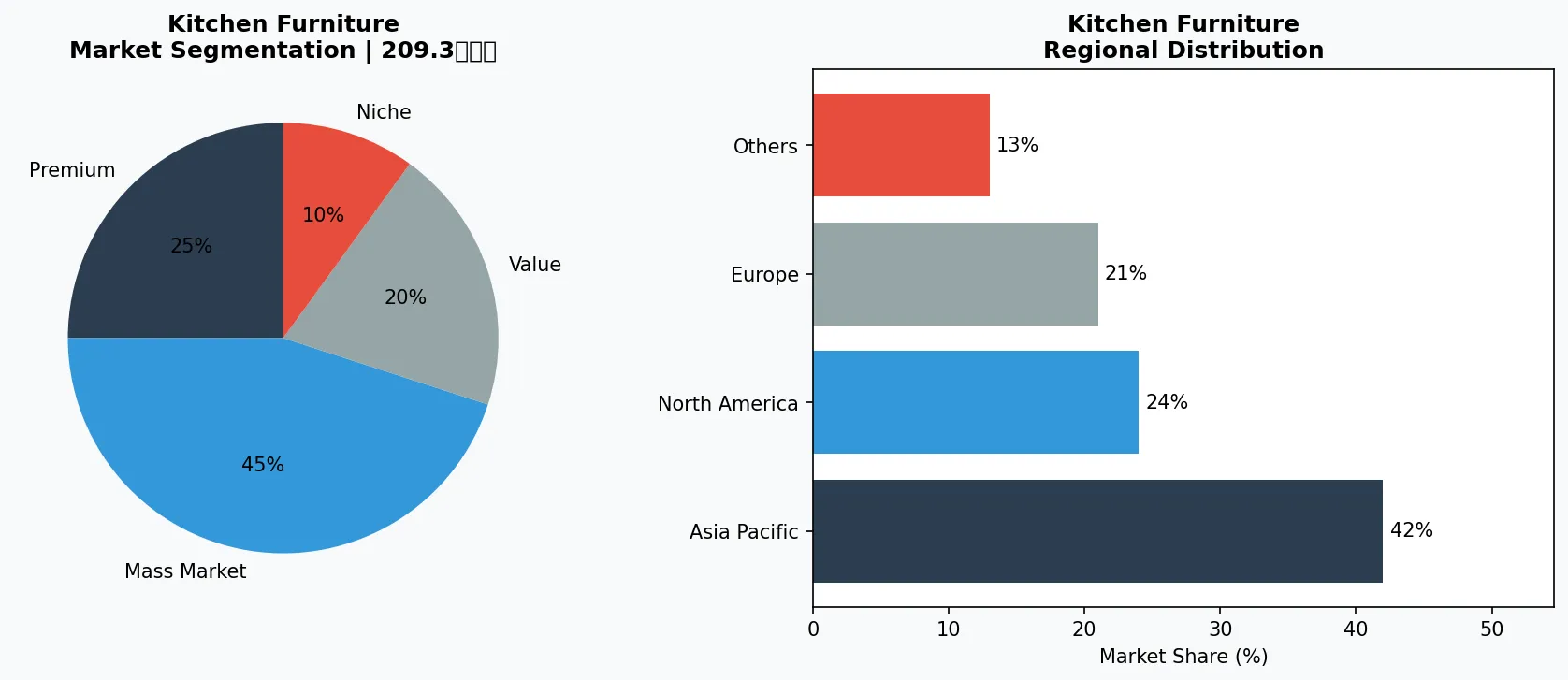

1. Industry Overview

When 96% of contractors favor warm neutrals and 59% report rising demand for dark wood, the message is unmistakable: kitchen cabinet materials have become the single most consequential decision in a kitchen remodel. Unlike hardware choices or appliance selections, cabinet materials dictate not just aesthetic appeal but resale value, durability, and long-term cost of ownership. A minor kitchen remodel averaging $23,000 prioritizes cabinet replacement precisely because material quality determines whether that investment retains value over a 10-15 year lifecycle.

Industry Scope & Characteristics

Material Composition Dictates Total Cost of Ownership

Cabinet material decisions extend far beyond initial purchase price. Solid hardwood options like white oak offer refinishing capability extending functional lifespan beyond 30 years, while engineered MDF cores may require replacement within 15 years in humid environments. The 45-55% premium for solid wood over engineered alternatives often reverses when calculated on annual cost basis for owner-occupied properties.

Regional Supply Chain Concentration Creates Vulnerability

North American cabinet manufacturing clusters in specific regions—Appalachian hardwood regions supply the majority of domestic white oak, while engineered wood production concentrates in the Pacific Northwest. This geographic specialization enables quality consistency and cost efficiency but creates supply risk when weather events, transportation disruptions, or regional economic downturns affect production capacity.

Environmental Certification Requirements Tightening

CARB Phase 2 formaldehyde emission limits now apply to all cabinet materials sold in California and states adopting California standards. FSC chain-of-custody certification has become mandatory for commercial projects exceeding $500,000 in environmental categories. These compliance requirements eliminate suppliers lacking documented quality management systems, creating barriers that favor established manufacturers over new market entrants.

Finish Technology Innovation Extends Material Performance

UV-cured finishes applied in controlled factory environments now achieve durability ratings exceeding site-applied coatings by 300% in scratch and chemical resistance testing. Low-VOC water-based UV systems have eliminated the environmental tradeoffs that previously limited factory finish quality. This finishing evolution enables engineered wood products to match solid hardwood performance in demanding applications like busy household kitchens.

The shift from painted cabinets to wood grain represents a fundamental taste evolution. According to 2026 data, 59% of respondents identified wood grain as growing in popularity, with white oak emerging as the dominant choice for homeowners seeking natural warmth without the visual heaviness of traditional dark hardwoods. This preference has forced manufacturers to reconsider their material sourcing, finishing processes, and price points. The kitchen cabinet materials market no longer rewards generic product lines—specialization in specific wood types and sustainable alternatives now defines competitive positioning.

Sustainability has transitioned from marketing buzzword to material selection criteria. Bamboo and reclaimed wood cabinet options have moved from boutique status to mainstream availability, driven by both consumer demand and regulatory pressures targeting formaldehyde emissions and deforestation concerns. Manufacturers that invested early in FSC-certified supply chains now enjoy structural advantages as environmental compliance requirements tighten across North American and European markets. The material composition of kitchen cabinets now carries the same weight as their visual design in purchasing decisions.

Key market segments and growth drivers in the Kitchen Cabinet Materials sector.

2. Market Analysis

The kitchen cabinet materials market represents a critical subsegment within the broader $300 billion global kitchen furniture industry, with cabinetry accounting for approximately 30-40% of total kitchen furniture expenditure in developed markets. North American kitchen remodel spending reached $87 billion in 2025, with cabinet materials representing the largest single expense category at 35-40% of total project costs. This concentration creates both opportunity and vulnerability—the material decision dominates budget allocation, making specification accuracy essential for contractors and homeowners alike.

Three growth drivers are reshaping material selection patterns. First, aging housing stock drives renovation urgency: homes built before 2000 contain cabinets averaging 20-25 years old, creating a massive replacement wave through 2030. Second, remote work adoption has elevated kitchen functionality requirements, pushing homeowners toward higher-quality materials that support intensive daily use rather than light entertaining purposes. Third, the "earthy vibrancy" aesthetic movement has validated premium material investments—wood tones at 29%, white at 28%, and off-white at 15% signal that material authenticity outweighs paint color novelty in 2026 purchasing decisions.

Regional market dynamics vary significantly. The Pacific Northwest and Mountain regions lead adoption of sustainable materials, with Portland and Denver showing 40% higher-than-average demand for bamboo and reclaimed wood options. Southern markets demonstrate stronger preference for painted finishes despite the wood grain trend, suggesting climate and architectural context influence material perception. Urban cores increasingly favor engineered materials offering consistent quality and faster installation, while suburban and rural markets sustain demand for solid wood construction with longer lead times.

Market segmentation and regional distribution analysis for Kitchen Cabinet Materials.

3. Product Categories

Solid hardwood cabinets remain the premium segment, commanding 45-55% price premiums over engineered alternatives. White oak dominates this category in 2026, favored for its light grain pattern and dimensional stability in varying humidity conditions. Hickory offers a more dramatic grain option for homeowners seeking visual impact, while cherry wood maintains its position for traditional and transitional kitchen designs requiring warm undertones. Solid hardwood's advantage lies in refinishing capability—a white oak cabinet can be sanded and restained multiple times, extending functional lifespan beyond 30 years.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Engineered wood cabinetry, including MDF and plywood core constructions, captured 40% of new construction cabinet installs in 2025. MDF (medium-density fiberboard) cores excel for painted finishes, providing uniformly smooth surfaces that highlight color depth. Plywood-core cabinets offer superior screw-holding strength and moisture resistance, making them the preferred choice for base cabinets near sinks and dishwashers. Manufacturers like American Woodmark have invested heavily in hybrid constructions combining engineered cores with hardwood veneers, reducing material costs while maintaining visual authenticity.

Sustainable alternatives are scaling rapidly. Bamboo cabinetry has achieved parity with mid-range hardwood options in both price and durability, withstrand-woven bamboo offering hardness ratings exceeding red oak. Reclaimed wood cabinets from companies specializing in salvaged barn timber and urban lumber programs command 60-80% premiums but eliminate new harvest concerns. Recycled polymer and composite materials serve the ultra-budget segment, offering water resistance and maintenance-free ownership at entry-level price points, though aesthetic limitations restrict their use to rental properties and utility applications.

Ready-to-assemble (RTA) cabinet materials have evolved to include higher-quality engineered wood options as manufacturers recognize that DIY installers cannot accommodate complex solid hardwood joinery. The RTA segment now represents 25% of cabinet sales by volume, with material specifications optimized for shipping durability and assembly tolerance rather than traditional furniture construction standards.

4. Leading Players

Masco Corporation operates the largest cabinet manufacturing network in North America through brands including KraftMaid, Merillat, and QualityCabinets. The company's 2024 strategic shift toward regional production facilities reduced lead times by 40% while enabling material customization at scale. Masco's position as a preferred supplier to major homebuilders ensures volume stability, while their dealer network supports custom order fulfillment for renovation projects requiring specific material specifications. Their recent investment in UV-cured finishing technology addresses environmental compliance while improving finish durability on wood veneer products.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the kitchen furniture space.

MasterBrand, Inc. generates over $3 billion in annual cabinet revenue through brands including Diamond Cabinets, Schrock, and Home Decorators Collection. The company's acquisition strategy has consolidated regional manufacturers into a national supply network capable of matching materials to regional aesthetic preferences—offering knotty alder configurations in the Southwest while maintaining white oak-focused inventory for Northeast specifications. MasterBrand's 2025 launch of a reclaimed wood product line under the NatureMark brand demonstrates responsiveness to sustainability certification requirements from commercial and institutional buyers.

American Woodmark Corporation serves the mid-market through branded and private-label programs, with IKEA and Lowe's partnerships representing significant volume channels. The company's 2026 material strategy emphasizes engineered wood innovations, including their proprietary engineered particleboard core with enhanced moisture resistance. American Woodmark's Just-In-Time delivery system accommodates job-site material scheduling, reducing on-site storage requirements for contractors managing multiple simultaneous projects. Their 2024 capacity expansion in West Virginia added 200,000 square feet dedicated to premium solid wood production, signaling confidence in continued demand for higher-end materials.

For buyers seeking supplier verification and competitive positioning, Verity Rank's B2B platform provides material specification databases and supplier capability assessments. The platform's supplier verification services address quality consistency concerns that plague large-scale material procurement, where batch-to-batch wood moisture content variation and finish thickness inconsistencies represent recurring pain points for contractors and specification writers.

5. Market Trends

1. EARTHY VIBRANCY DOMINANCE

Wood tones captured 29% of kitchen color/finish preferences in 2026, surpassing white (28%) for the first time since 2018. This shift validates premium material investments—paint finishes cannot replicate the grain depth and light interaction of natural wood. Companies responding include Masco's expanded white oak finish options and MasterBrand's Knotty Alamo Alder introduction targeting Southwest markets where rustic-modern aesthetics drive specification.

2. DARK WOOD RESURGENCE

Dark wood finishes rose 59% in contractor preference according to NKBA data, reversing the light-tone dominance of 2020-2024. Walnut and espresso-stained maple cabinets now specify at rates matching white painted cabinets in luxury segments. American Woodmark reported 35% year-over-year growth in dark finish options, with installation volume concentrated in high-end residential and boutique commercial projects where budget constraints yield to aesthetic impact.

3. SUSTAINABLE MATERIAL CERTIFICATION

FSC (Forest Stewardship Council) certification has transitioned from differentiator to requirement for commercial and institutional specification. California Buy Clean requirements and similar state-level regulations are extending certified material requirements to residential projects exceeding valuation thresholds. Manufacturers lacking certified supply chains face restricted access to public projects and environmentally conscious national builders, creating structural competitive disadvantages that compound annually until addressed.

4. HYBRID CONSTRUCTION EVOLUTION

The most significant material innovation in 2026 involves combining material types within single cabinet constructions—plywood cores with hardwood edge banding, MDF interiors with wood veneer exteriors, and engineered wood drawer boxes with solid wood face frames. These hybrid approaches optimize cost-performance ratios, reducing solid wood content to high-visibility components while engineering stability into structural elements. The trend challenges traditional "solid wood" marketing claims, as consumers increasingly accept engineered cores when properly specified and finished.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities define the market outlook for kitchen cabinet materials through 2028. First, the aging housing stock renovation wave creates sustained demand for replacement cabinets through 2035, with baby boomers and Gen X homeowners controlling the majority of home equity driving renovation spending. Suppliers positioning capacity for mid-range solid wood and premium engineered options will capture volume growth without competing on price with commodity imports. Second, the continued rise of DIY home improvement, where 60% of homeowners now attempt cabinet projects without contractors, creates demand for RTA products with improved assembly documentation and material consistency—reducing the expertise gap between professional and homeowner installation.

One concrete risk demands strategic attention: import competition from European and Asian manufacturers offering engineered wood cabinets at 25-40% below domestic manufacturing costs. These products increasingly meet technical specifications for North American certification while undercutting on price, threatening domestic production capacity for mid-market segments. Manufacturers that cannot achieve cost parity through automation and regional production will face difficult decisions between margin erosion and volume loss. The risk extends beyond pricing—domestic suppliers losing mid-market volume also lose scale advantages in material purchasing and overhead absorption, creating cascading competitive disadvantages that compound over multiple years. Supplier diversification strategies, including qualified import partnerships and domestic capacity maintenance, represent the pragmatic response to this structural challenge.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Kitchen Cabinet Materials Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-10. All market figures are estimates and may vary from actual results.