Table of Contents

The global Kitchen Furniture industry serves consumers worldwide with diverse solutions.

1. Industry Overview

What does a $182.7 billion kitchen look like? That's the projected global value of the kitchen furniture and fixture market in 2026, up from $177.15 billion in 2025. This steady growth underscores a fundamental shift: the kitchen is no longer just a utilitarian space but a central hub for living, entertaining, and expressing personal style. The industry, encompassing everything from cabinetry to islands, is a critical segment within the broader home furniture economy, directly fueled by consumer investment in home design and renovation.

Industry Scope & Characteristics

Broad Product Portfolio

Products span kitchen cabinets, kitchen islands, pantry cabinets, bar counters, kitchen benches, pot racks, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

The domestic kitchen furniture market is experiencing moderate but consistent expansion. This isn't driven by new housing alone; it's powered by a wave of remodeling and a heightened consumer focus on creating functional, beautiful living environments. The 2026 Kitchen Trends Report highlights how generational priorities are shaping demand, with Gen X and Boomers seeking durability and timeless design, while younger cohorts push for flexibility and tech integration.

Historically, kitchen furniture was about permanence. The recent shift, accelerated by changing work-life patterns and a focus on home-centricity, is toward adaptability. The market now thrives on solutions that can evolve with a family's needs, blending storage efficiency with aesthetic appeal. This evolution from static to dynamic spaces defines the modern industry's role and its growing economic footprint.

Key market segments and growth drivers in the Kitchen Furniture sector.

2. Market Analysis

The kitchen furniture and fixture market is on a clear growth trajectory, forecast to reach $182.70 billion in 2026. This increase represents a compound annual growth that reflects sustained consumer and commercial investment. The primary engine is increased consumer interest in home design and renovation, turning kitchens into high-value projects where furniture and storage solutions are paramount.

Several key drivers are accelerating this growth. First is the increasing demand for modular furniture designs, which offer customization and scalability for diverse kitchen layouts. Second is the rising adoption of ready-to-assemble (RTA) furniture, a segment championed by giants like IKEA, which appeals to cost-conscious and DIY-friendly consumers. Third is a growing preference for integrated, multi-functional pieces that maximize space in both large homes and compact urban apartments.

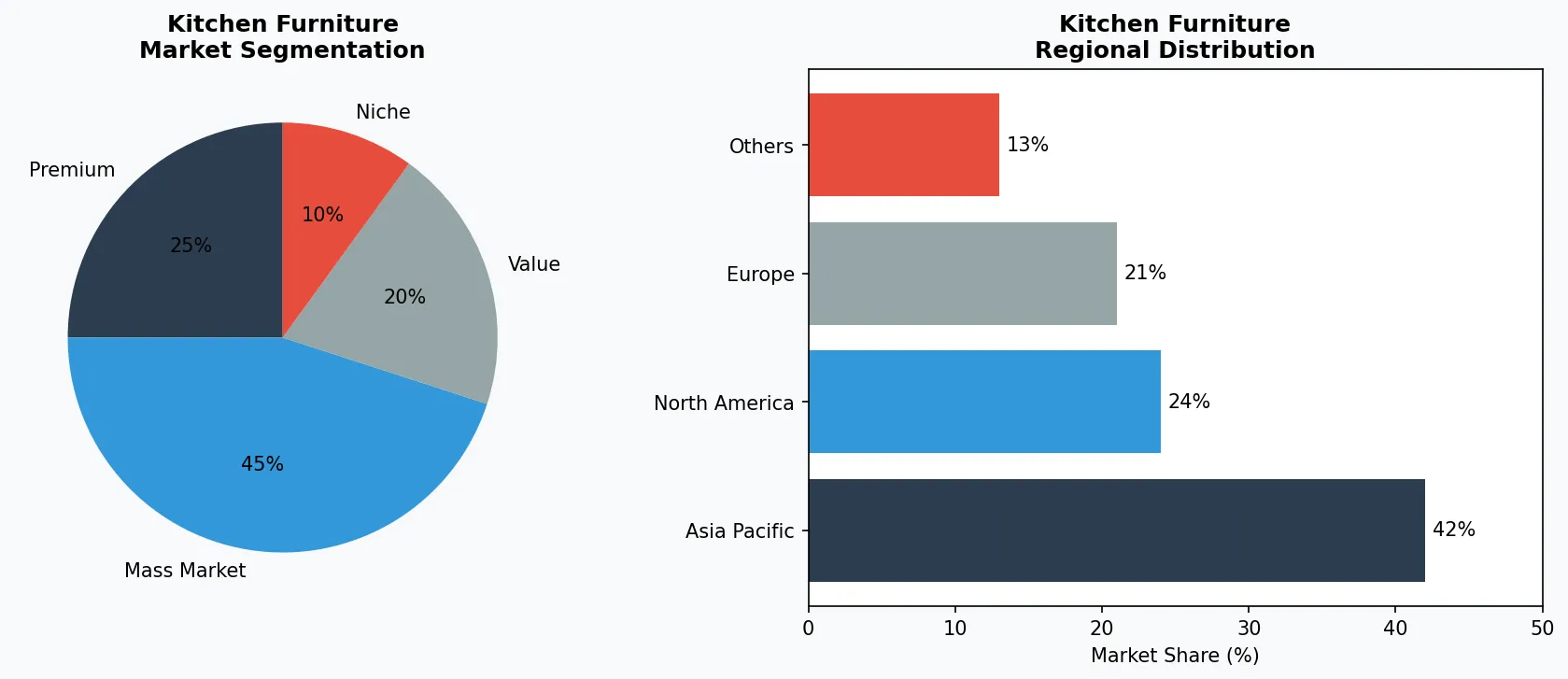

Geographically, the market is not uniform. A thorough investigation of the kitchen and dining furniture market at country and regional levels reveals distinct hotspots. North America remains a dominant force due to high remodeling rates and consumer spending power, while the Asia-Pacific region, led by manufacturing and design hubs in China and Southeast Asia, is a critical growth area driven by urbanization and a burgeoning middle class.

Market segmentation and regional distribution analysis for Kitchen Furniture.

3. Product Categories

The kitchen furniture ecosystem is segmented into core functional categories. Kitchen cabinets form the foundational layer, accounting for the largest share of market revenue. This includes everything from base and wall cabinets to specialized pantry cabinets, with brands like Oppein and Boloni competing on materials, finish, and innovative internal storage systems.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Kitchen islands and peninsulas represent the statement category, transforming workflow and social interaction. These pieces have evolved from simple prep stations to multi-functional hubs incorporating seating, storage, and even appliances. High-end brands like Pioli often focus on bespoke, material-driven island designs that serve as a kitchen's centerpiece.

Auxiliary storage and furniture complete the space. This sub-category includes bar counters for entertainment zones, kitchen benches for casual dining, and organizational solutions like pot racks and trolleys. Companies like Vatti and Godi often play in this space, offering products that add final layers of functionality and style without the scale of full cabinetry installations.

4. Leading Players

IKEA dominates the global volume segment through its iconic ready-to-assemble model and democratic design philosophy. Its strategy hinges on affordability, modularity (exemplified by the METOD and SEKTION systems), and a seamless in-store/online experience, making functional kitchen furniture accessible worldwide. Its recent moves focus on circularity and space-saving solutions for urban dwellers.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the kitchen furniture space.

Oppein represents the strength of the integrated, full-service model, particularly in the Asia-Pacific market. As a major Chinese brand, Oppein competes on providing complete, customized kitchen solutions—from design to installation—often targeting the mid-to-high-end residential and commercial segments. Its strategy is built on vertical integration, controlling production from raw materials to finished, installed cabinetry.

Boloni, another key Chinese player, positions itself at the premium end of the custom kitchen spectrum. It emphasizes European-inspired design, high-quality materials like solid wood and quartz, and smart kitchen integrations. Boloni's market position relies on branding itself as a provider of luxury lifestyle solutions rather than mere furniture, often through exclusive showrooms and designer partnerships.

5. Market Trends

1. Modular & Customizable Designs

Modular & Customizable Designs — The shift toward modular cabinets and furniture allows for personalized layouts and easy future modifications. This matters as homeowners seek longevity and adaptability. IKEA's entire kitchen system is built on this trend, offering a framework consumers can configure and reconfigure.

2. Hidden & Integrated Storage

Hidden & Integrated Storage — The demand for clean, uncluttered aesthetics is driving innovation in concealed storage solutions like toe-kick drawers, appliance garages, and behind-panel compartments. This maximizes space and enhances visual flow. Oppein and high-end European brands excel in creating seamless, handle-less cabinets that prioritize this streamlined look.

3. Durable & Easy-Clean Surfaces

Durable & Easy-Clean Surfaces — Consumers prioritize low-maintenance materials that withstand heavy use, such as quartz countertops, laminate finishes, and stain-resistant laminates. This trend is critical for both longevity and hygiene. Brands like Boloni heavily market the durability and easy-care properties of their material selections as a key selling point.

6. Regional Markets

North America, particularly the United States, is a mature but robust market defined by high per-capita spending on home improvement. Growth here is less about new housing and more driven by renovation cycles, with homeowners investing in premium upgrades, smart storage, and open-plan kitchen furniture that blends with living areas. The demand for quality and brand reputation is pronounced.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

The Asia-Pacific region, with China at its core, is the engine of both manufacturing and consumption growth. Rapid urbanization, rising disposable incomes, and the development of large-scale residential projects fuel demand. Here, brands like Oppein and Boloni are household names, competing on full-service customization. The market is also a primary source for ready-to-assemble and export-oriented furniture.

Europe presents a diverse landscape, split between the value-driven, flat-pack dominance in Northern Europe led by IKEA, and the strong tradition of high-quality, bespoke craftsmanship in markets like Italy and Germany. Sustainability regulations and a focus on material provenance are particularly influential trends shaping product development and consumer choice in this region.

7. Investment Outlook

Two specific opportunities stand out for industry players. First, the technological integration of smart storage—think motorized lifts, sensor-activated lighting, and inventory-tracking pantries—presents a premium upgrade path. Second, tapping into the sustainability-driven renovation wave with certified, durable materials and circular business models (like take-back programs for old cabinets) can capture a growing segment of environmentally conscious consumers.

The primary concrete risk is economic sensitivity. The kitchen furniture market is closely tied to consumer confidence and disposable income. A sharp economic downturn or sustained inflation in 2024-2025 could quickly dampen discretionary spending on major renovations and high-ticket furniture items, stalling the projected growth toward the 2026 market size. Supply chain volatility for key materials remains an ongoing operational challenge.

Strategic Considerations:

- ('Technology & AI Integration:', 'Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.')

- ('Sustainability as Business Strategy:', 'Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.')

- ('Transparency & Traceability:', 'Consumers demand increasingly granular information about product origins, ingredients, and production methods.')

- ('Emerging Market Penetration:', 'Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.')

Make Informed Decisions in the Kitchen Furniture Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-16. All market figures are estimates and may vary from actual results.