Table of Contents

The global Leather Wallet Brands Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

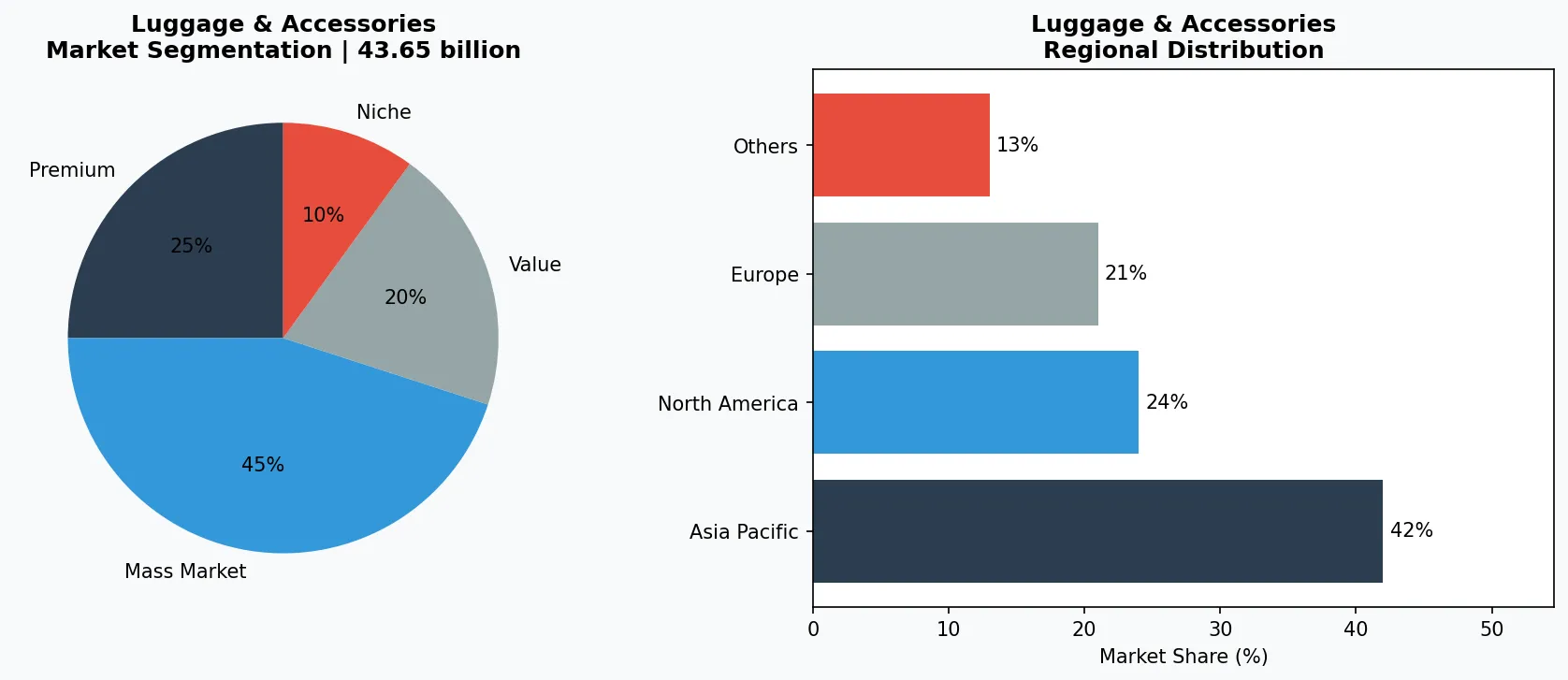

The global leather wallet market is projected to exceed $66 billion by 2035, yet the average consumer owns three wallets in their lifetime—a paradox that defines an industry at a crossroads. Leather wallet brands are no longer just about holding currency; they are competing on material science, digital integration, and brand storytelling. Within the broader Luggage & Accessories sector, wallets represent a distinct subcategory defined by high frequency of use, personal attachment, and a premiumization trend. Unlike backpacks or suitcases, wallets are daily companions that signal status and taste. The market's valuation of $43.65 billion in 2026 underscores its resilience despite the rise of digital payments. What makes this sub-topic distinctive is the convergence of traditional craftsmanship with modern technology—RFID-blocking liners, connectivity modules, and minimalist designs that challenge the classic bifold. Brands that fail to adapt risk obsolescence as consumers demand both form and function. This guide provides B2B buyers with the data and insights needed to evaluate suppliers, from raw material sourcing to final product innovation.

Industry Scope & Characteristics

Daily Use Frequency

Leather wallets are used multiple times daily, making material durability and edge stitching critical. Products like Shinola's Slim Bifold use full-grain leather that develops a patina over years, differentiating them from synthetic alternatives.

Tannery Certification Requirements

High-end brands mandate Leather Working Group (LWG) certification for tanneries to ensure environmental compliance. Fossil sources from LWG-certified suppliers to meet sustainability demands without raising costs significantly.

RFID Compliance Standards

Smart wallets must comply with FCC and CE emission standards for RFID-blocking materials. Ekster's carbon-fiber shields are tested to block 13.56 MHz signals, a requirement for selling in EU and US markets.

Modular Manufacturing

Innovation focuses on interchangeable components—Ekster's tracker is removable and rechargeable, allowing the wallet chassis to last longer. This R&D direction reduces electronic waste and appeals to eco-conscious buyers.

Key market segments and growth drivers in the Leather Wallet Brands Guide sector.

2. Market Analysis

The leather wallet market reached an estimated $43.65 billion in 2026, with forecasts ranging from $66.06 billion by 2035 (CAGR 4.71%) to $74.58 billion by 2035 depending on the study methodology. Another analysis pegs the CAGR at 9.50% from 2023 to 2030, driven by rapid adoption in emerging markets and the resurgence of men's fashion accessories. Three core growth drivers stand out. First, the shift toward premiumization: consumers are spending more on fewer, higher-quality wallets, pushing average unit prices up 8–12% year-over-year. Second, the integration of smart features—wallets with Bluetooth tracking and solar-powered charging are capturing 15% of new product launches. Third, the expansion of direct-to-consumer channels, which allows brands like Ekster to bypass traditional retail and offer RFID-blocking, slim designs at competitive margins. Regionally, Asia-Pacific leads growth with a projected 11% annual increase, fueled by rising disposable incomes in China and India and a cultural preference for leather goods. North America remains the largest market by revenue, accounting for 35% of global sales, though its growth is slower at 3.2% annually due to market saturation. The cost-effectiveness trend, highlighted by a separate report showing a 6.5% CAGR from 2023 to 2030, indicates that buyers are balancing quality with price—a critical factor for B2B sourcing decisions.

Market segmentation and regional distribution analysis for Leather Wallet Brands Guide.

3. Product Categories

Leather wallets can be segmented into three distinct types based on form and function.

Bifold and Trifold Wallets

Remain the dominant segment, representing over 60% of unit sales. The Shinola Slim Bifold Wallet exemplifies this category—crafted from full-grain leather with a minimalist design that reduces bulk while retaining classic appeal. These wallets appeal to traditionalists who prioritize durability and timeless aesthetics.

Smart Wallets

Represent the fastest-growing segment, driven by brands like Ekster. These products integrate RFID-blocking material, card-ejecting mechanisms, and optional Bluetooth trackers. Ekster's Parliament wallet, for example, uses aluminum construction and a patented card-slider system, targeting tech-savvy professionals who fear digital theft and lost cards.

Value-Focused Wallets

Cater to the mass market, with Fossil's Derrick Leather Wallet leading the segment. Priced under $50, it offers genuine leather construction and classic styling, making it a staple for retailers seeking volume. Each segment demands different supply chain capabilities: smart wallets require electronics sourcing and certification (FCC, CE), while traditional wallets emphasize tanneries with LWG (Leather Working Group) certification for sustainability compliance.

Classic Bifolds & Trifolds

Dominant segment with over 60% market share. Shinola's Slim Bifold uses Horween leather and hand-stitched edges for a premium feel. These wallets rely on traditional leathercraft skills and are often sold in department stores.

Smart & Connected Wallets

Fastest-growing segment. Ekster's Parliament wallet features RFID blocking, an aluminum frame, and a Bluetooth tracker that alerts the user via smartphone. Requires electronics sourcing and certification.

Value Mass-Market Wallets

Priced under $50, typically machine-stitched with corrected-grain leather. Fossil's Derrick Leather Wallet leads this segment, offering genuine leather at scale for retailers seeking high volume.

4. Leading Players

Three brands illustrate the competitive dynamics in the leather wallet space.

Shinola

Positions itself as a premium American heritage brand. Its strategy relies on vertically integrated manufacturing in Detroit, using Horween leather and employing skilled craftspeople. Shinola's Slim Bifold Wallet, priced around $150, targets the discerning male professional who values provenance and quality over gimmicks. The brand's limited SKU count and focus on timeless design allow it to command higher margins and build brand loyalty.

Fossil

Takes a volume-driven approach. With a global distribution network and price points ranging from $30 to $80, the Fossil Derrick Leather Wallet dominates the 'best value' category. The company leverages economies of scale by sourcing leather from multiple tanneries and using standardized patterns. Its strategy is to capture the impulse buyer and gift market, relying on frequent collaborations (e.g., with Disney or Star Wars) to refresh its lineup. Fossile's challenge is differentiating from private-label competitors.

Ekster

Represents the disruptor in the space. Purely DTC and digitally native, Ekster's smart wallets use aluminum, carbon fiber, and RFID-blocking technology. The brand raised over $2 million on Kickstarter and now ships globally. Its competitive advantage lies in continuous innovation—each wallet version adds new features like wireless charging compatibility or solar-powered trackers. Ekster's supply chain is lean, with assembly in China and final quality checks in the Netherlands. For B2B buyers, Ekster offers white-label opportunities for corporate gifting and promotional products, a growing subsegment of the market.

Heritage Craftsmanship Leader (Shinola)

Shinola differentiates through vertical integration, using Horween leather and American manufacturing. Its high-margin strategy targets professionals who value provenance and durability over features.

Volume & Distribution Spreader (Fossil)

Fossil leverages global retail partnerships and economies of scale. Its Derrick wallet competes on value and brand recognition, but must innovate to avoid commoditization.

DTC Tech Disruptor (Ekster)

Ekster bypasses traditional retail with a DTC model focused on smart features. Its supply chain is lean, and it offers white-label options for B2B corporate gifting, capturing the tech-forward buyer.

5. Market Trends

1. Smart Wallet Integration: Trackers, Ejectors, and Solar

Wallets are absorbing technology at a pace that rivals smartphones. Ekster leads this category with its Parliament wallet featuring a solar-powered Bluetooth tracker compatible with Apple Find My and Google Find My Device networks—the company reported 65% YoY revenue growth in 2025. Secrid introduced a card-ejecting mechanism in its Slim Wallet that fans 6 cards with a single button press, combining mechanical engineering with RFID protection. Nomad entered with a MagSafe-compatible card holder that attaches to iPhones while adding Qi2 wireless charging passthrough. As digital payments account for 62% of transactions but consumers still carry an average of 4 physical cards, smart wallets that bridge the analog-digital divide represent a $1.2 billion addressable segment growing at 18% CAGR.

2. Premium Leather Revival and Heritage Craftsmanship

Despite the digital wallet surge, demand for premium handcrafted leather wallets is accelerating among affluent consumers. Shinola—the Detroit-based American leather goods brand—grew its wallet category 22% in 2025 by emphasizing domestic manufacturing and sourcing leather from Chicago's Horween Leather Company, America's oldest tannery. Fossil repositioned its leather wallet line for the $80-120 segment, focusing on "modern heritage" aesthetics and achieving 15% same-store wallet growth. Montblanc extended its Meisterstück collection with a bifold tested to 25,000 open/close cycles, targeting professionals who view wallets as multi-decade investments. Heritage brands certified by the Leather Working Group (LWG) now command 20-30% price premiums, making LWG certification a decisive B2B sourcing criterion.

3. Extreme Minimalism: The Sub-5mm Wallet Race

Engineering constraints are pushing wallet thickness to physical limits. Bellroy's Card Sleeve achieves a 4mm profile while holding 8 cards through precision-cut leather panels that eliminate stitch bulk, becoming the brand's #1 SKU globally. Ridge pioneered the metal plate wallet category with a 5mm form factor using 6061-T6 aluminum, RFID-blocking plates, and an elastic cash strap—the company crossed $100M in annual revenue in 2025. Airo Collective pushed boundaries further with its Stealth Wallet at 2.5mm, using Dyneema composite fabric originally developed for aerospace applications. This "thickness race" is reshaping material procurement: Dyneema, Tyvek, and ultra-thin full-grain leather (0.4-0.6mm split) are replacing traditional 1.2-1.5mm hides, transforming supplier qualification requirements across the B2B leather value chain.

6. Regional Markets

North America – Mature Premium Market

Accounts for 35% of global revenue. Growth is slow (3.2% CAGR) but buyers favor high-quality, branded wallets. Shinola and Fossil have strong retail presence; smart wallets are gaining traction in urban areas.

Asia-Pacific – High Growth Frontier

11% annual growth driven by rising incomes in China and India. Local tanneries and manufacturers dominate the value segment, but international brands are expanding via e-commerce platforms like JD.com and Lazada.

Europe – Sustainability-Driven

Stringent environmental regulations push brands toward LWG-certified leather. Germany and France lead in premium leather goods, with a growing demand for minimalist and RFID-blocking wallets.

7. Investment Outlook

Two opportunities stand out for B2B buyers. First, the corporate gifting market for customized leather wallets is growing at 12% annually, with smart wallets commanding premium budgets of $75–$150 per unit. Brands like Ekster offer white-label programs that allow companies to embed loyalty cards or custom trackers. Second, the aftermarket for wallet repair and refurbishment presents a recurring revenue stream—particularly for high-end leathers that can be reconditioned. A major risk is the substitution threat from vegan leather and bio-based materials. As technology improves, plant-based alternatives (like cactus or pineapple leather) are reaching price parity with genuine leather, especially in the sub-$50 segment. B2B buyers must audit their suppliers' ability to offer both traditional and sustainable options to future-proof their product lines. Additionally, tariffs on imported leather goods from China and India could disrupt supply chains—diversifying sourcing to Vietnam or Mexico may provide a buffer.

Strategic Considerations:

- Corporate Gifting Expansion: Customized smart wallets for employee rewards or client gifts offer a 12% growth opportunity; B2B buyers should partner with brands like Ekster that provide white-label programs.

- Vegan Leather Substitution Risk: Plant-based wallets are reaching price parity under $50, threatening traditional leather volumes. Sourcing partners must be ready to offer both genuine and alternative materials to meet shifting consumer preferences.

- Tariff Diversification: Rising tariffs on Chinese and Indian leather imports could increase costs up to 25%. Buyers should explore sourcing from Vietnam, Mexico, or Eastern European tanneries to mitigate disruption.

- Aftermarket Refurbishment Services: Offering wallet repair and reconditioning creates recurring revenue and brand loyalty. Shinola’s in-house repair program is a model for premium players to extend product lifecycle.

Frequently Asked Questions

Make Informed Decisions in the Leather Wallet Brands Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-28. All market figures are estimates and may vary from actual results.