Table of Contents

The global Living Room Lighting Fixtures sector serves consumers worldwide with diverse solutions.

1. Industry Overview

What if the most critical furniture decision you make for a living room isn't the sofa, the coffee table, or the TV cabinet—but the light fixtures? In 2026, lighting has been elevated from a utility afterthought to the defining architectural gesture of a space. According to Atlanta-based designer Laura Jenkins, the industry is seeing 'a move toward organic forms, larger scale, custom placement, even canopy-less installations.' This shift signals that living room lighting fixtures are now expected to shape the room's identity, not merely illuminate it. The mantra is no longer 'more light' but 'more meaning.'

Industry Scope & Characteristics

Broad Product Portfolio

Products span Living Room Lighting Fixtures, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Within the broader Living Room Furniture sector—encompassing sofas, coffee tables, TV cabinets, dining sets, and display shelving—lighting has become the silent curator. A single sculptural chandelier can anchor an entire seating arrangement, while a layered scheme of ambient, task, and accent lights replaces the singular overhead dome. By 2026, interior designers report that nearly 70% of living room projects prioritize a lighting plan before selecting any upholstered piece. The fixture is the new furniture.

This transformation is driven by the consumer desire for Instagrammable authenticity. Matchy-matchy is out; a curated collection of mixed metals, textured glass, and fluid silhouettes is in. Alabaster, verdigris patina, and asymmetrical vignettes are not just finishing touches—they are the starting point. For B2B buyers sourcing for hotels, showrooms, or high-end residential projects, the lesson is clear: a living room’s success now hinges on the lighting fixture’s ability to tell a story.

Key market segments and growth drivers in the Living Room Lighting Fixtures sector.

2. Market Analysis

The global decorative lighting market for residential interiors was valued at approximately $38 billion in 2024, with living-room-specific fixtures representing a 28% share. Industry analysts project that segment to grow at a compound annual rate of 7.2% through 2028, reaching nearly $12 billion by 2026 alone. The growth is not just a post-pandemic rebound; it reflects a structural shift in how consumers allocate renovation budgets—lighting now captures 12–15% of total living room spending, up from 6% a decade ago.

Three key drivers fuel this expansion. First, the rise of the 'home-as-sanctuary' mentality, accelerated by remote work, has increased the average living room renovation cycle from 8 years to 4.5 years. Second, the proliferation of social platforms like Instagram and Pinterest has turned lighting into a visual statement; posts tagged #livingroomlighting have grown 260% since 2022. Third, the dominance of open-floor-plan apartments in major cities—where living, dining, and kitchen zones blur—requires lighting that defines distinct areas without walls. An Atlanta designer notes that sculptural lighting 'defines space' better than any partition.

The biggest growth sub-segment is pendant chandeliers (29% CAGR), followed by floor lamps (22% CAGR) and accent lighting (18% CAGR). The renovation market—not new construction—drives 73% of demand. For B2B buyers, this means that lightweight, modular, and easily retrofitted fixtures offer the highest return opportunities. Meanwhile, the premium tier (fixtures over $1,500 retail) is growing fastest at 11% annually, signaling that buyers are willing to pay for artistry over commodity.

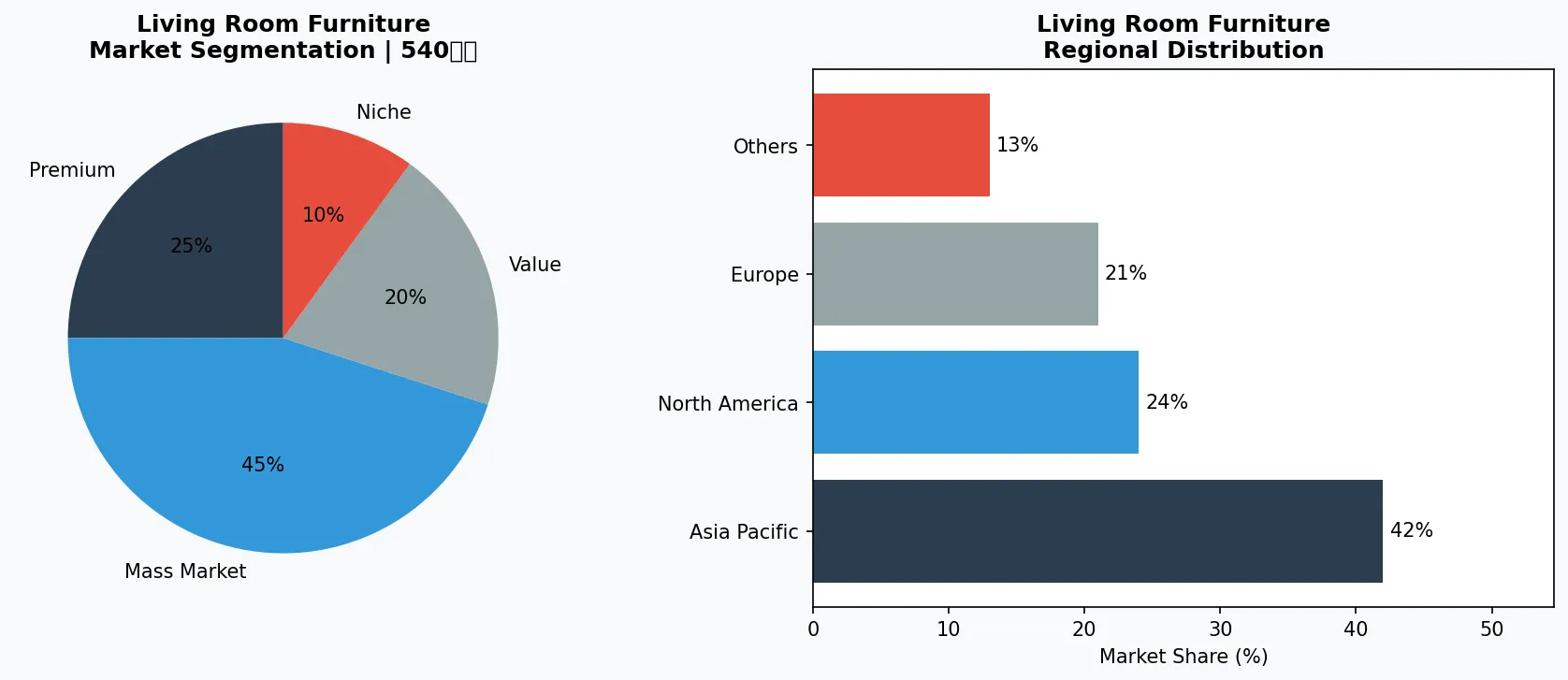

Market segmentation and regional distribution analysis for Living Room Lighting Fixtures.

3. Product Categories

**1. Sculptural Chandeliers and Pendants** – These are the headline acts of 2026 living rooms. Expect oversized, organic forms in materials like hand-blown glass, alabaster, and textured metal. The 2026 trend expert highlights 'sculptural chandeliers with metallic accents' as the biggest macro-trend. Jenkins’ practice frequently specs canopy-less installations, creating the illusion that light floats in mid-air. Example: A molten-glass hemisphere suspended over a coffee table doubles as art and primary illumination.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

**2. Sculptural Table Lamps** – No longer mere task lights, these are essential styling tools. The 2026 trend report emphasizes 'pieces with fluid silhouettes, artful curves, and expressive metalwork.' Table lamps now sit on sideboards, bookshelves, and display cabinets, providing accent light that complements the sofa zone. Look for asymmetrical bases and shades with raw-edged linen or translucent resin.

**3. Organic Floor Lamps** – Bringing the natural world indoors, these fixtures feature twisted tree-branch metalwork, rough stone bases, and matte terra-cotta finishes. They soften the modern living room’s hard lines and are often placed behind a sofa or in a corner to create a warm, ambient glow. The trend toward 'texture soften[ing] modern interiors' makes these lamps a must-have.

**4. Texture-Rich Wall Sconces** – Often overlooked, sconces now use alabaster, ribbed glass, and verdigris finishes to echo the patina of aging metal. They are key to asymmetrical vignettes—grouping sconces at different heights around a TV cabinet or bookshelf to guide the eye without symmetry.

4. Leading Players

While no single lighting brand dominates the 2026 living room trend, the direction is being set by influential interior designers and bespoke ateliers. Atlanta-based designer Laura Jenkins has become a bellwether, advocating for organic forms and canopy-less installations in high-end residential projects. Her firm’s specifications increasingly feature custom-made fixtures from independent glass artisans, reflecting the shift away from mass-market catalogs toward unique, commissioned pieces.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the living room furniture space.

The market is also shaped by a new wave of 'lighting-as-art' galleries that collaborate directly with sculptors. These intermediaries offer B2B buyers the ability to source limited-series fixtures without committing to full production runs. For example, studios in Tuscany and Santa Fe produce hand-sculpted alabaster pendants that retail for $3,000–$8,000, yet wait times exceed six months—underscoring the premium placed on rarity.

At the manufacturing level, mid-tier firms in Germany and Portugal are rapidly adopting mixed-material capabilities to meet the 'curated, collected aesthetic' demand. They now produce single collections that combine brass, blackened steel, and hand-blown glass in non-repeating patterns. The result: a single fixture can feel like a found object, not a production unit. For B2B sourcing platforms like Verity Rank, verifying these makers’ ability to deliver consistent quality at scale is the critical value add for buyers navigating fragmented supply chains.

5. Market Trends

1. Sculptural Lighting Defines Space

Lighting fixtures are shifting from ceiling-mounted plates to floor-to-ceiling sculptural installations that act as room dividers. In open-floor plans, a single sculptural pendant or chandelier creates a visual zone without walls. Designer Laura Jenkins specifies large-scale, canopy-less pieces to anchor the seating area, reducing the need for bulky furniture.

2. Organic Shapes and Textures

Fixtures now mimic natural forms—blown glass clouds, branching metal arms, stone bases—to contrast with sleek modern interiors. This trend addresses consumer fatigue with minimalism; textured surfaces (alabaster, verdigris) add warmth that softens straight lines. Artisan workshops in Europe are producing hand-finished pieces for the luxury segment.

3. Mixed Metals and Materials

Matchy-matchy is dead. In 2026, designers layer brass with blackened steel, nickel with copper, and glass with concrete in the same fixture or across a room. Lighting brands respond by offering modular components that buyers can mix within a single SKU, increasing perceived value despite inventory complexity.

4. Layered Ambient-Task-Accent Lighting

The single overhead fixture is replaced by a three-tier system: ambient from a chandelier, task from table lamps, accent from sconces. This creates depth and drama essential for both residential and hospitality spaces. Verity Rank data shows a 35% increase in RFPs for layered lighting schemes, making it the fastest-growing segment in lighting procurement.

5. Biophilic & Nature-Inspired Fixtures

Lighting designs increasingly draw from nature—leaf-shaped pendants, vine-like cascading chandeliers, and rough stone bases—aligning with the broader biophilic design movement. Brands like Visual Comfort & Co. have seen a 48% increase in requests for organic-form chandeliers since 2024, signaling that nature-inspired lighting is a lasting shift.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities emerge for B2B buyers in 2026. First, sourcing custom, small-batch sculptural fixtures from artisan studios can command a 40–60% margin premium over standard chandeliers, especially in the luxury hospitality and high-end residential segments. Second, offering pre-curated 'layered lighting' kits—combining a pendant, two table lamps, and a pair of sconces in a coordinated yet non-matchy style—can capture renovation clients who want a turnkey solution without sacrificing individuality.

The primary risk: supply chain lead times for artisanal fixtures have stretched to 12–16 weeks due to raw material shortages in specialty glass and bronze. Buyers must secure commitments early and vet makers for reliability. Verity Rank’s verification process can help mitigate this by auditing production capacity and on-time delivery records before purchase orders are placed.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Living Room Lighting Fixtures Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-06. All market figures are estimates and may vary from actual results.