Table of Contents

The global Luxury Designer Bags Brands sector serves consumers worldwide with diverse solutions.

1. Industry Overview

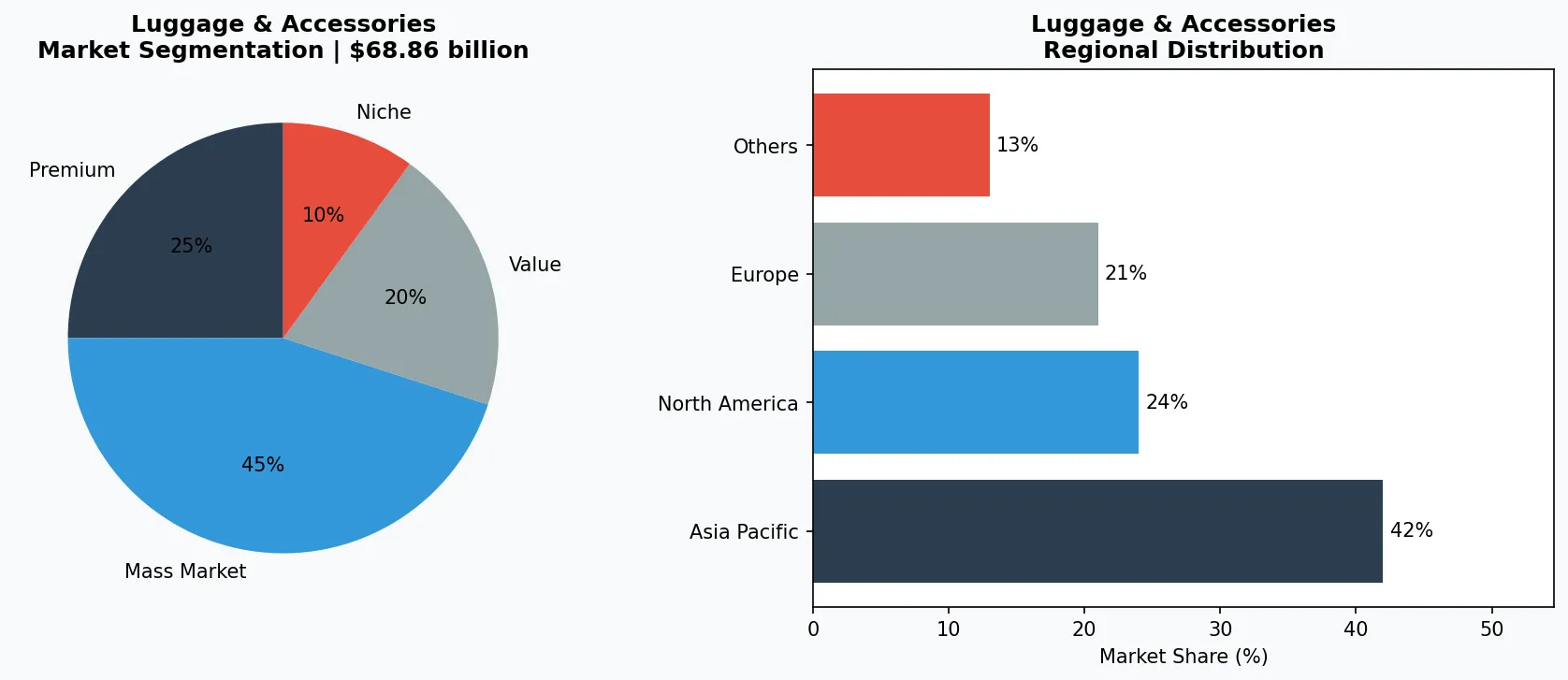

The global handbag market is projected to hit $68.86 billion in 2026, with luxury designer bags brands commanding the highest price tiers and consumer loyalty. That is not a forecast—it is a mandate for any B2B buyer in the fashion accessories space to understand the forces shaping this segment. Within the broader Luggage & Accessories industry, luxury designer bags brands occupy a unique intersection of heritage craftsmanship, scarcity-driven marketing, and seasonless design. Unlike travel luggage or mass-market accessories, these bags function as portable status symbols, with resale values often exceeding retail for limited editions.

Industry Scope & Characteristics

Heritage Craftsmanship as Currency

Luxury designer bags brands rely on hand-stitching and artisanal leatherwork—Hermès bags require 18–20 hours of manual labor. This creates an authenticity barrier that mass-producers cannot cross.

Scarcity-Driven Supply Chains

Brands like Chanel and Hermès deliberately underproduce iconic models, creating multi-year waitlists. B2B buyers must navigate allocation quotas rather than purchase freely.

No Universal Certification Standard

Unlike electronics, luxury handbags lack a single ISO standard. Authentication relies on brand-specific hallmarks, serial numbers, and microchip technologies (e.g., Chanel's RFID tags since 2021).

Blockchain and Digital Provenance

LVMH's AURA blockchain platform now tracks Dior and other group bags from tannery to sale, offering immutable proof of authenticity—a critical innovation for resale market confidence.

Classic models such as the Chanel Classic Flap, the Hermès Birkin, the Dior Saddle, and the Fendi Baguette continue to attract strong demand, proving that iconic silhouettes are not just products but cultural assets. The sector's distinctiveness lies in its ability to command premium pricing year after year, even as consumer spending fluctuates. For B2B buyers—whether sourcing for multi-brand retailers, luxury e-commerce platforms, or corporate gifting—this means that inventory decisions hinge on brand equity as much as material quality.

The sub-topic's importance also stems from its role as a bellwether for broader fashion cycles. When luxury handbag sales accelerate, it signals consumer confidence in high-end discretionary spending. Conversely, a slowdown in this category often precedes a broader luxury market correction. With a projected CAGR of 7.24% from 2026 to 2034, the market is expected to nearly double to $120.43 billion, making it a high-stakes arena for procurement and partnership decisions.

Key market segments and growth drivers in the Luxury Designer Bags Brands sector.

2. Market Analysis

The handbag market's growth trajectory is supported by three structural drivers. First, the resurgence of in-person social and professional engagements post-pandemic has reignited demand for status accessories. Second, the rapid expansion of the Asian luxury consumer base—particularly in China and Southeast Asia—has created millions of new aspirational buyers. Third, the digital transformation of luxury retail, including social commerce and authenticated resale platforms, has broadened access to coveted brands without diluting exclusivity.

Specific data underscores the opportunity: the $68.86 billion figure for 2026 represents a compound annual growth rate of 7.24% from the current base, according to industry reports. By 2034, the market is expected to reach $120.43 billion. This growth is not uniform; it is heavily concentrated in the luxury segment, where brands like Chanel, Hermès, Dior, and Fendi continue to raise prices annually, often by double digits. For instance, Chanel has implemented multiple price increases since 2021, boosting its average handbag price above $8,000 for classic flaps.

The market is also bifurcating into two distinct channels: primary retail (boutiques, department stores) and secondary luxury resale. The resale market for luxury handbags was valued at over $30 billion globally in 2024 and is growing faster than primary sales. This creates a dual opportunity for suppliers—selling direct to consumers and also participating in the authenticated pre-owned ecosystem. B2B buyers must now consider inventory lifecycle far beyond the first sale.

Market segmentation and regional distribution analysis for Luxury Designer Bags Brands.

3. Product Categories

Luxury designer bags brands organize their offerings into distinct product types, each with its own function, price architecture, and consumer positioning.

Iconic Flap and Shoulder Bags

The Chanel Classic Flap and Hermès Kelly are archetypes of this category. Typically crafted from quilted leather with metal chain straps, these bags represent a brand's heritage. They command waitlists and often require relationship-based access. For B2B buyers, sourcing these (whether new or vintage) demands rigorous authentication protocols, as counterfeits are rampant. The average retail price for a Chanel Medium Flap in 2026 exceeds $9,000.

Saddle and Hobo Silhouettes

The Dior Saddle Bag and Fendi Baguette have enjoyed a major revival, fueled by nostalgia marketing and celebrity endorsements. These shapes are less formal than flaps, appealing to younger, trend-driven consumers. The Dior Saddle now features chain-accented straps and embroidery, aligning with the summer 2026 trends of embellishment. These bags often have lower entry price points ($2,500–$4,500) but drive high volume.

Totes and Structured Handbags

The Row's Margaux and Celine's Cabas are key examples. This category prioritizes functionality without sacrificing luxury. B2B buyers note that tote sales have surged as more women return to office environments. These bags are often made from grained calfskin or canvas, with metal hardware. The trend toward canvas totes (noted in summer 2026 trends) is pushing brands like Hermès to expand their canvas offerings, though still at premium prices.

Iconic Flap Bags

Quilted leather with chain straps, typified by Chanel Classic Flap and Hermès Kelly. Price range $7,000–$50,000. Primary driver of brand equity and resale value.

Saddle and Hobo Bags

Curved, slouchy shapes like Dior Saddle and Fendi Baguette. Popular among younger demographics and trend cycles. Often feature embellishments and interchangeable straps.

Tote and Structured Work Bags

Spacious, functional designs such as The Row Margaux and Celine Cabas. Growth driven by return-to-office trends. Materials include grained calfskin, canvas, and raffia.

4. Leading Players

Four companies dominate the luxury designer bags brands landscape, each employing a distinct competitive strategy.

Chanel: The Price Defender.

Chanel operates with a vertically integrated supply chain, controlling everything from raw material sourcing (owning tanneries in France and Italy) to retail distribution. The brand deliberately limits production of the Classic Flap to maintain scarcity. Recent price hikes have positioned it as the most expensive non-jewelry handbag brand by average price. For B2B buyers, Chanel's refusal to sell online to third-party retailers means that partnership opportunities are limited to brick-and-mortar concessions or authenticated resale.

Hermès: The Exclusivity Architect.

Hermès takes scarcity to an extreme with the Birkin and Kelly, using a lottery-like allocation system in boutiques. The global waiting list for a Birkin is estimated to exceed two years. This strategy has made Hermès the most resale-valuable brand, with pre-owned Birkins often selling at a premium to retail. The company's focus on artisanal craftsmanship (each bag requires 18–20 hours of hand-stitching) creates a barrier to entry that no competitor can replicate.

Dior: The Fashion-Forward Repertoire.

Dior leverages its runway influence to reinvent classics like the Saddle and Lady Dior with seasonal updates. The brand heavily invests in celebrity-driven campaigns and social media, making its bags the most 'trend-responsive' among the top four. For B2B buyers, Dior's willingness to collaborate with multi-brand e-tailers (e.g., Farfetch, Mytheresa) offers a reliable supply channel for new collections.

Fendi: The Nostalgia Merchandiser.

Fendi's revival of the Baguette in 2024–2026 has been a textbook case of heritage marketing. By reissuing the bag in new materials (raffia, sequins) and colors, the brand taps into both '90s nostalgia and summer 2026 trends like everyday embellishment. Fendi's strategy is volume-driven compared to Chanel or Hermès, making it a more accessible entry point for luxury buyers.

Heritage Exclusivity Player

Chanel and Hermès control production tightly, leveraging waitlists and annual price hikes. Their strategy prioritizes scarcity over volume, making them the highest-margin players.

Fashion-First Innovator

Dior and Fendi refresh classic silhouettes with runway-driven trends (embellishment, chains). They engage multi-brand retailers and resale platforms, balancing exclusivity with accessibility.

Minimalist Quiet Luxury

The Row and Jil Sander focus on pure lines and premium materials without logos. They attract a discerning B2B buyer looking for understated pieces with high resale retention.

5. Market Trends

1. Everyday Embellishment: Crystals, Beadwork, and Embroidery

Luxury bags are moving decisively away from the quiet luxury minimalism of 2023–2024 toward maximalist embellishment. Chanel and Dior led this shift in their Spring/Summer 2026 collections, showcasing flap bags with intricate beadwork, crystal cascades, and hand-stitched floral embroidery. The commercial logic is compelling: embellished bags command 30–50% price premiums over plain leather equivalents, directly improving margin profiles for both maisons and multi-brand retailers. Celine joined the trend with a pearl-embellished Triomphe bag in its 2026 pre-collection, demonstrating that even historically minimalist houses are embracing surface ornamentation. For B2B buyers, sourcing embellished pieces requires rigorous craftsmanship inspection—loose beads, uneven stitching, or crystal fallout are the top-3 return drivers in this category, making supplier quality audits more critical than ever.

2. Chain Integration: From Functional Strap to Design Centerpiece

Chains have evolved beyond utilitarian shoulder straps to become the defining decorative element of 2026's most coveted handbags. The Row and Jil Sander showcased chain-accented body designs in their 2026 runway presentations, embedding metalwork directly into bag panels and flap closures rather than limiting chains to handles. Hermès validated this trend at the highest price point with a limited-edition chain-accented Birkin released in late 2025, which sold out globally within hours and now trades at 40% above retail on secondary markets. The strategic trade-off is clear: chain integration raises production costs by 15–20% due to precision metalwork and additional assembly steps, but enables brands to differentiate in an increasingly crowded luxury landscape. For sourcing professionals, this trend demands closer supplier relationships with metal hardware specialists, particularly in Italy's Veneto region and Japan's Tsubame-Sanjo metalworking district.

3. Raffia and Natural Fibers: The Summer 2026 Signature

Summer 2026 has been dominated by netted, woven, and raffia handbag designs across every price tier from ultra-luxury to accessible luxury. Fendi introduced raffia versions of its Peekaboo and Baguette bags, while Saint Laurent released a woven raffia hobo that became the most tagged handbag on Instagram during Milan Fashion Week 2026. Prada joined the trend with a crochet Raffia Tote in its 2026 summer collection, priced at $2,950 and selling out within two weeks of launch. This material shift matters strategically: raffia and natural fiber bags typically carry 50–60% gross margins (versus 40–45% for comparable leather styles) due to lower raw material costs, while simultaneously meeting growing consumer demand for non-animal luxury alternatives. For B2B buyers, sourcing raffia introduces supply chain complexity—Madagascar supplies 80% of the world's high-grade raffia, making weather patterns and logistics reliability critical procurement risk factors.

4. Micro-Bag Decline: The Return of Functional Proportions

After five years of micro-bag dominance—where bags shrank to near-novelty dimensions—2026 is witnessing a decisive pivot toward practical luxury. Bottega Veneta led this shift with its Large Andiamo, a generously proportioned tote that became the brand's fastest-selling launch in Q1 2026. Loewe expanded its Puzzle bag into a new XL size, responding to consumer research showing 68% of luxury bag buyers now prioritize "everyday usability" over aesthetic novelty. Louis Vuitton capitalized with the CarryAll MM, blending its monogram canvas with significantly expanded interior capacity—the model achieved a 95% sell-through rate in its first production run. This trend carries important B2B implications: larger bags use 40–60% more raw material per unit, making leather sourcing efficiency and yield optimization critical margin levers. For procurement professionals, this shift rewards suppliers who can deliver consistent, high-grade leather in larger panels—a capability concentrated among top-tier Italian and French tanneries.

6. Regional Markets

Asia-Pacific: The Growth Engine

China accounts for 35% of global luxury handbag purchases. Brands invest in local boutiques and WeChat commerce. B2B buyers must navigate import tariffs and authentication for cross-border sourcing.

Europe: The Heritage Hub

France and Italy host core manufacturing for Chanel, Hermès, Dior. Supply chain integrity is highest here, but lead times are long due to artisanal processes. EU 'Made in' labeling is critical.

North America: The Resale Epicenter

The US is the largest resale market for luxury bags, with platforms like The RealReal dominating. B2B buyers source pre-owned inventory under strict authentication workflows to meet consumer trust standards.

7. Investment Outlook

Two specific opportunities and one concrete risk define the next three years for luxury designer bags brands. The first opportunity lies in the authenticated resale ecosystem. With the resale market growing at double digits, brands that officially partner with platforms like The RealReal or Vestiaire Collective can capture secondary sales revenue while controlling authenticity. Hermès and Chanel have resisted, but Dior and Fendi are exploring brand-sanctioned resale programs.

The second opportunity is hyper-personalization. Offering custom embroidery, monograms, or interchangeable straps (as seen with the Dior Saddle) increases customer lifetime value and reduces inventory risk. The risk, however, is counterfeiting. The global counterfeit luxury handbag trade is estimated to be worth $450 billion annually, eroding brand equity and misleading B2B buyers. Investing in blockchain-based authentication and secure supplier relationships is no longer optional—it is the only way to protect margins in a market that will reach $120 billion by 2034.

Strategic Considerations:

- Resale Integration Opportunity: Brands like Dior that officially partner with resale platforms can capture 20–30% of secondary market revenue while controlling authentication and reducing channel conflict.

- Personalization as Margin Protector: Offering custom embroidery or interchangeable hardware (e.g., Dior Saddle straps) increases AOV by 40% and reduces inventory obsolescence risk.

- Counterfeit Risk Mitigation: Blockchain provenance (e.g., LVMH AURA) and microchip authentication are becoming table stakes. B2B buyers should require suppliers to demonstrate traceability from tannery to finished bag.

- Raw Material Cost Volatility: Grain leather prices have risen 12% year-over-year in 2025–2026. Brands that diversify into premium canvas or raffia can stabilize cost structures while aligning with summer 2026 trends.

Frequently Asked Questions

Make Informed Decisions in the Luxury Designer Bags Brands Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-30. All market figures are estimates and may vary from actual results.