Table of Contents

The global Men's Down Jacket Selection sector serves consumers worldwide with diverse solutions.

1. Industry Overview

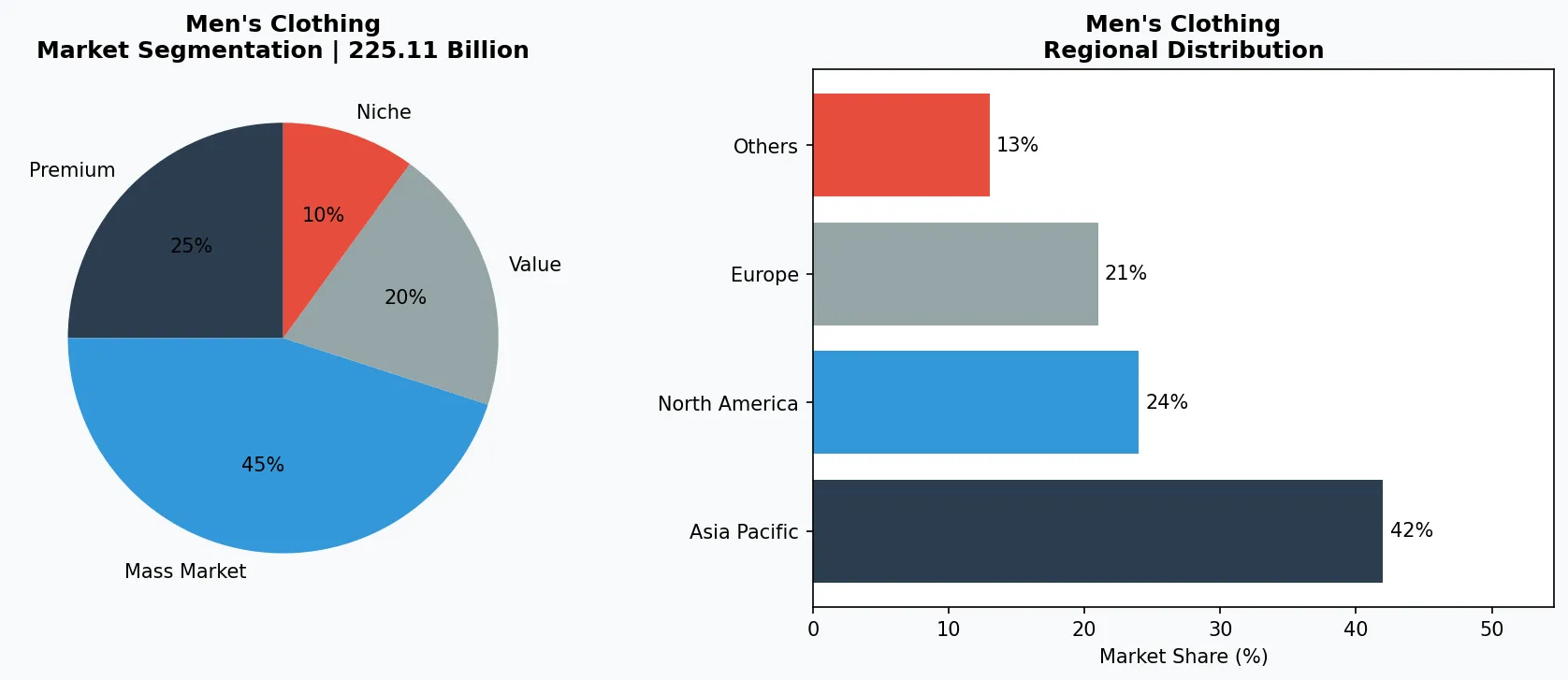

The numbers are staggering. By 2025, the global down jacket market was already valued at $225.11 billion. But the real story is the trajectory: analysts project the segment to hit $316.05 billion by 2032, fueled by a compound annual growth rate of 11.83%. Within this explosive landscape, men's down jackets command a dominant share—accounting for more than half of all down jacket revenue in 2024. For B2B buyers—retailers, procurement officers, and brand managers—understanding how to navigate this market is no longer a seasonal consideration; it is a strategic imperative. Men's down jacket selection has evolved from a simple warmth-versus-weight decision into a complex matrix of fill power, traceability certification, and consumer-driven innovation.

Industry Scope & Characteristics

Fill Power as a Quality Metric

Men's down jackets are graded by fill power—a measure of loft (cubic inches per ounce). Premium jackets use 700–850 fill power; 900+ is ultra-premium. B2B buyers should specify minimum fill power in supplier contracts to avoid underfilled products.

Globalized but Fragmented Supply Chain

Down sourcing spans farms in Hungary, Poland, and China, while garment assembly concentrates in China and Vietnam. Tier 2 suppliers (down processors) often have inconsistent traceability, making third-party certification verification critical.

RDS and ISO Standards Compliance

The Responsible Down Standard (RDS) and ISO 9237 (thermal resistance) are de facto requirements for retailers. Many importers also require Oeko-Tex Standard 100 for fabric safety. Non-compliance can block entry to EU and US markets.

Baffle Sewing Automation

Leading manufacturers now use CNC-controlled baffle-stitching machines that achieve uniform down distribution within ±1.5g tolerance. This reduces cold spots and customer returns, making it a key capability for volume buyers.

What makes the men's down jacket subcategory distinctive within broader menswear is its dual identity: it sits at the intersection of technical performance apparel and everyday fashion. Unlike generic puffer jackets, men's down products must satisfy both the mountaineer demanding 800-fill goose down and the urban commuter seeking a sleek, packable silhouette. This bifurcation is driving product segmentation across price tiers and use cases, from insulated vests for mild climates to expedition-grade parkas rated to -40°F.

VerityRank’s analysis focuses on the B2B implications. For buyers, the critical question is not just which jacket to stock, but which supply chain partners can consistently deliver certified down, ethical sourcing, and scalable production. The market’s projected CAGR of 12.22% from 2026 onward means lead times, quality control, and compliance verification will become competitive differentiators—not back-office functions.

Key market segments and growth drivers in the Men's Down Jacket Selection sector.

2. Market Analysis

The men's down jacket market was valued at $115.54 billion in 2023 and is projected to reach $316.05 billion by 2032, according to the latest industry reports. This represents an 11.83% CAGR, outpacing the broader men's apparel segment by nearly 4 percentage points. Three forces are driving this growth. First, climate volatility: extreme winter events in North America and Europe have made insulated outerwear a non-negotiable wardrobe staple, expanding the addressable market beyond traditional cold-weather regions. Second, the athleisure trend has blurred the line between performance and lifestyle; men now wear down jackets for airport travel and coffee runs, not just ski trips. Third, rising disposable incomes in Asia-Pacific—particularly China and Japan—are fueling demand for premium down products.

From a revenue perspective, the total down jacket market (all genders) is expected to grow from $299 billion in 2026 to $529.5 billion in 2035 at a CAGR of 6.6%. The men’s subset will outpace this due to higher average selling prices (ASPs) in men’s technical outerwear. Another projection pegs the entire down jacket sector at $633.87 billion by 2033, with an annual growth rate of 12.7%. For B2B buyers, these numbers signal increasing competition for raw materials—particularly high-fill-power goose down—and the need to lock in supplier relationships early.

Geographically, North America contributed 38% of men’s down jacket revenue in 2024, but Asia-Pacific is the fastest-growing region with a projected 14.2% CAGR through 2030. This shift is driven by urbanization in China and South Korea, where lightweight down vests have become office attire. European demand remains strong, especially for sustainable and recycled-down products. The market’s fragmentation is notable: no single manufacturer holds more than 8% share, creating opportunities for nimble sourcing via platforms like VerityRank to identify vetted suppliers.

Market segmentation and regional distribution analysis for Men's Down Jacket Selection.

3. Product Categories

Men's down jacket selection broadly falls into three product segments: expedition-grade parkas, lightweight urban puffer jackets, and insulated vests. Expedition-grade parkas are designed for extreme cold, typically using 650- to 800-fill goose down with a waterproof breathable shell. Examples include the heavy-duty parkas used by Arctic expedition teams, featuring draft collars and fur-trimmed hoods. These jackets command premium price points ($500-$1,200) and require rigorous quality certifications such as RDS (Responsible Down Standard) and ISO 9237 for thermal resistance.

Lightweight urban puffers dominate the mid-market ($150-$400). These jackets prioritize packability and style over extreme warmth, often using 550- to 700-fill duck down with synthetic insulation blends. Brands like those sold through major outdoor retailers have popularized the “bubble jacket” silhouette, with baffle designs that prevent down migration. For B2B buyers, this segment offers the highest volume potential but requires careful supplier vetting to ensure consistent fill weight specifications across production batches.

Insulated vests—both sleeveless and hybrid—have exploded in popularity for layering. They use similar down fills but with reduced fabric weight, targeting temperatures between 40°F and 60°F. The key innovation here is the combination of down and synthetic fills in the same garment: down in the core for warmth, synthetic in the shoulders to manage moisture. Examples include vests with 800-fill power in the front panels and PrimaLoft in the arms. This hybrid approach minimizes bulk while maximizing versatility, a feature highly valued by B2B clients serving the corporate uniform or travel retail sectors.

Expedition-Grade Parkas

Built for extreme cold (rated to -40°F), using 800-fill goose down and waterproof/breathable membranes. Examples: heavy-duty parkas with fur-trimmed hoods and multiple pockets. Price range: $500–$1,200.

Lightweight Urban Puffer Jackets

Focus on packability and style, with 550–700 fill down and ultra-thin nylon shells. Ideal for commuting and travel. Price range: $150–$400. The highest-volume segment for B2B buyers.

Insulated Down Vests

Sleeveless or hybrid vests combining down in the core with synthetic insulation in the shoulders for moisture management. Popular for layering and corporate uniforms. Price range: $80–$250.

4. Leading Players

The men’s down jacket market is populated by a mix of heritage outdoor brands, luxury houses, and private-label manufacturers. Outdoor specialist The North Face exemplifies a technology-led strategy, focusing on proprietary insulation like Thermoball Eco and down that meets the Responsible Down Standard. The company’s heavy investment in R&D—over $50 million annually—allows it to command premium pricing while maintaining supply chain transparency. For B2B buyers, The North Face offers a strong benchmark for quality but limited private-label flexibility.

Luxury house Moncler takes a fashion-forward approach, treating down jackets as seasonal statement pieces. With average retail prices above $1,200, Moncler’s strategy relies on limited-edition drops and collaborations with high-profile designers. The brand’s supply chain is vertically integrated, with down sourced from Hungarian and French farms. While not a typical B2B partner for mass-market buyers, Moncler’s success has validated the premium down jacket segment, encouraging retailers to allocate more shelf space to high-ASPs styles.

On the manufacturing side, Chinese OEMs like Tianyuan Garments (which produces for major global brands) represent the volume backbone of the market. These manufacturers have invested heavily in automation for down filling and baffle-stitching, achieving tolerances within ±2 grams of fill weight. They also offer flexible minimum order quantities (as low as 300 units for custom designs), making them ideal for mid-tier brands seeking to enter the down jacket segment without large upfront commitments. VerityRank’s supplier verification tools can help buyers assess these manufacturers’ RDS certifications and production capacity.

Technology-First Outdoor Brand

Invests $50M+ annually in insulation R&D; uses proprietary blends like Thermoball Eco. Strong on certification (RDS) and brand equity, but limited private-label flexibility for B2B partners.

Luxury Fashion House

Vertically integrated, sourcing down directly from European farms. Focuses on limited-edition drops and celebrity collaborations. Validates high-ASP segment but not suited for volume sourcing.

High-Volume OEM Manufacturer

Based in China, producing for multiple global brands. Offers MOQs as low as 300 units with automated down filling. Holds RDS and Oeko-Tex certifications. Ideal for mid-tier brands seeking cost-effective entry.

5. Market Trends

1. TRACEABILITY AND CERTIFICATION

Down jacket buyers increasingly demand full supply chain transparency, from farm to finished garment. The Responsible Down Standard (RDS) has become a baseline requirement for North American and European retailers. Brands like Patagonia now require Tier 1 and Tier 2 suppliers to submit annual audits. This trend matters because non-compliant down—product of live-plucking or force-feeding—can damage brand reputation and trigger import restrictions. B2B buyers should prioritize suppliers with third-party RDS accreditation.

2. HYBRID INSULATION SYSTEMS

The line between down and synthetic insulation is blurring. Jackets now combine down in the torso with synthetic fills (e.g., Primaloft, Thinsulate) in sleeves and hoods where moisture management is critical. This approach improves durability and washability while retaining down’s warmth-to-weight advantage. The North Face’s “Hybrid Down” collection is a market leader. For buyers, hybrid products extend the selling season beyond extreme cold climates.

3. LIGHTWEIGHT AND PACKABLE SILHOUETTES

Urban consumers want down jackets that compress into a pocket-sized stuff sack. This has driven demand for 800- to 900-fill goose down housed in ultra-light 10-denier nylon fabrics. Brands like Uniqlo’s Seamless Down series have popularized this form factor. The supply chain challenge: ultra-light fabrics require specialized sewing equipment to prevent down leakage. Buyers must verify that manufacturers have experience with micro-stitching and down-proof fabric lamination.

6. Regional Markets

North America: 38% Market Share

Highest ASP and strong demand for technical parkas. Buyers prioritize RDS and sustainability certifications. Growth driven by climate volatility and outdoor lifestyle trends.

Asia-Pacific: 14.2% CAGR Fastest Growth

Urbanization in China and South Korea boosts demand for lightweight down vests. Local manufacturers dominate supply but vary in certification rigor. Price sensitivity is high.

Europe: Regulatory-Led Market

EU regulations on down sourcing and microplastic shedding from synthetic fills push buyers toward certified natural down. Strong presence of heritage goose-down producers in Hungary and Poland.

7. Investment Outlook

Two opportunities stand out. First, the corporate gifts and uniform segment is underserved; companies are increasingly ordering custom-branded down vests for field staff and client giveaways. VerityRank can help buyers connect with suppliers offering short-run customization (500+ units) with RDS-certified down. Second, sustainable down alternatives—such as those using recycled down post-consumer waste—are gaining traction, with projected growth of 18% annually. Early movers can lock in exclusive supplier partnerships.

The primary risk is raw material volatility. Global goose-down prices fluctuated by 40% in 2024 due to avian influenza outbreaks in European farms. Buyers should negotiate fixed-price contracts with escalation clauses and maintain dual-supplier strategies across regions (e.g., China and Hungary). Ignoring these risks could lead to margin compression and order fulfilment delays.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Frequently Asked Questions

Make Informed Decisions in the Men's Down Jacket Selection Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-14. All market figures are estimates and may vary from actual results.