Table of Contents

The global Men's Sweater Knitwear sector serves consumers worldwide with diverse solutions.

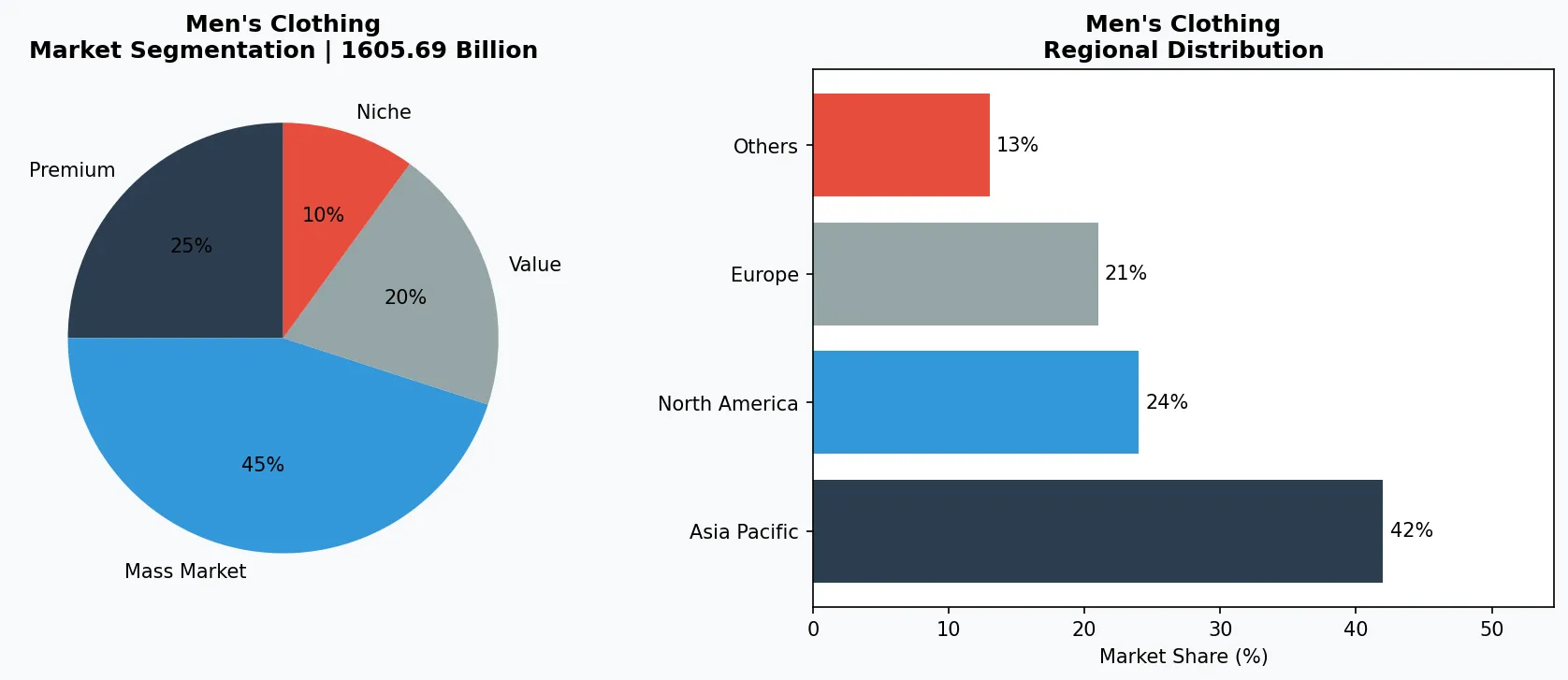

1. Industry Overview

The global knitwear market is on track to exceed $1.6 trillion by 2035, growing at a compound annual rate of 12.1%. Within that massive wave, men's sweater knitwear occupies a unique intersection of comfort and status. Unlike the broader men's clothing sector—where fast-fashion T-shirts and stiff dress shirts dominate—sweater knitwear marries technical craftsmanship with the quiet luxury trend that is redefining how men dress for both casual and formal settings.

Industry Scope & Characteristics

Gauge Precision Engineering

Men's sweater knitwear is defined by stitch density (gauge). Fine-gauge (12–14 G) cashmere sweaters offer a dress-shirt feel, while chunky cable-knits (3–5 G) provide structure. Each requires different machine setups and yarn tensions.

Vertical Production Control

Top mills own the full process from raw fiber washing to dyeing, spinning, and finishing. This control ensures consistent colorfastness (AATCC 61) and shrinkage limits (ASTM D4328) that B2B buyers demand.

ISO & Eco Certifications

Premium knitwear suppliers carry ISO 9001 (quality), ISO 14001 (environmental), Oeko-Tex Standard 100 (chemical safety), and often the Responsible Wool Standard (RWS) or Good Cashmere Standard.

Digital Knitting & Customization

Computerized flat-bed machines now allow fully fashioned knitting with minimal waste. Some manufacturers offer 3D sampling to reduce lead times, enabling brands to test 2026's 'relaxed tailoring' trends in weeks not months.

What makes this segment distinctive is its reliance on fiber engineering and gauge precision. A single Merino wool sweater can require over 1,200 meters of yarn, knitted at densities that affect drape, warmth, and durability. The shift toward relaxed tailoring in 2026 has only accelerated demand: consumers now expect sweaters that feel like loungewear but look like investment pieces.

The data backs this up. While the overall men's apparel market grows at roughly 2–3% annually, knitwear is outpacing it by multiples. The sweaters sub-segment alone is projected to expand at a 3.1% CAGR from 2025 to 2035, driven by rising disposable incomes in Asia and a Western pivot toward wardrobe minimalism that prioritizes versatile, high-quality knits over disposable fashion.

Key market segments and growth drivers in the Men's Sweater Knitwear sector.

2. Market Analysis

The numbers tell a clear story: the global knitwear market was valued at approximately $667.65 billion in 2024 and is expected to reach $5.32 trillion by 2034, implying a CAGR of 3.15% over that period. However, other analysts peg an even more aggressive trajectory—$1.6 trillion by 2035 at a 12.1% CAGR—suggesting that the segment is being redefined by premiumization and technical innovation.

Two primary drivers are fueling this growth. First, the rise of 'quiet luxury' has made understated sweaters a status signal. Instead of logos, consumers invest in fabric provenance and construction—think Scottish cashmere, Italian merino, or Japanese denier-fine cottons. Second, the athleisure spillover into knitwear has created a new hybrid category: performance sweaters that wick moisture, resist pilling, and maintain shape through machine washing.

Regionally, Asia-Pacific dominates both production and consumption. China alone accounts for roughly 40% of global knitwear output, while India and Bangladesh are rapidly upgrading their spinning and finishing capabilities. In contrast, Europe remains the epicenter of high-end knitwear, with Italy and Scotland supplying the finest yarns and finishing techniques. North America, driven by direct-to-consumer brands that emphasize transparency and sustainability, is the fastest-growing import market.

Importantly, the sweaters sub-segment within knitwear benefits from an aging demographic in developed markets—older consumers buy fewer but better quality pieces—and a younger cohort in emerging markets that sees sweaters as a year-round layering essential, not just a winter item.

Market segmentation and regional distribution analysis for Men's Sweater Knitwear.

3. Product Categories

Men's sweater knitwear breaks down into three distinct product categories, each with its own supply chain and consumer base.

1. Fine-Gauge Cashmere Sweaters

These are the ultra-luxury end of the market, typically knit at 12 to 14 gauge using pure cashmere from Inner Mongolia or Scotland. They command retail prices above $300 and are prized for softness, drape, and warmth-to-weight ratio. Leading mills produce cashmere sweaters with ISO 9001-certified quality management systems, ensuring consistent fiber diameter (under 16 microns) and low pilling ratings.

2. Mid-Weight Merino & Wool Blends

This is the volume driver. Merino wool sweaters (often machine-washable) dominate the premium casual segment, with brands offering garments that feel like cotton but regulate body temperature. Blends with nylon or elastane add stretch and durability, making them suitable for active lifestyles. The best-performing products use Super 150s grade wool and are finished with anti-shrinkage treatments.

3. Statement Cable-Knits & Textured Sweaters

These are the fashion-forward segment, often featuring chunky cable patterns, fisherman ribs, or artful intarsia. They leverage traditional knitting techniques (e.g., Fair Isle, Aran) but are produced on modern computerized flat-bed machines for scalability. A zippy cable-knit from a heritage Scottish mill might retail for $250–$500 and serve as a wardrobe anchor piece for the 'cozy luxury' trend highlighted in 2026 winter roundups.

Luxury Cashmere Sweaters

Pure cashmere pullovers and cardigans in fine-gauge knits, often with hand-finished details. Example: 2-ply cashmere crewnecks from Inner Mongolian mills, sold at $350+ retail.

Performance Merino Knits

Machine-washable Merino wool sweaters with anti-pilling and moisture-wicking treatments. Example: 150s Superfine Merino with Teflon coating for stain resistance.

Statement Textured Sweaters

Cable-knit, fisherman rib, and intarsia designs using blended wool or cotton. Example: Aran-style sweaters from Irish mills with traditional patterns updated for modern fits.

4. Leading Players

The men's sweater knitwear market is fragmented but dominated by three strategic archetypes.

1. Heritage European Mills

These are family-owned operations in Scotland, Italy, and Ireland that have been perfecting knitwear for generations. They control the entire value chain from raw fiber sourcing to final finishing. Their competitive advantage lies in proprietary yarn blends and certification (e.g., Woolmark, Oeko-Tex Standard 100) that command premium wholesale prices. They supply the world's top luxury houses and direct-to-consumer cult labels.

2. Asian Contract Manufacturers

Large-scale producers in China, Bangladesh, and Vietnam account for the bulk of global volume. Their edge is cost efficiency and scale, with the ability to turn around orders of 10,000+ units in 4–6 weeks. They are increasingly investing in sustainable production methods (e.g., waterless dyeing, recycled wool content) to meet Western buyer ESG requirements. Many hold ISO 14001 for environmental management.

3. Vertical Retailers with In-House Knit Capabilities

A growing number of brands now own or co-own knitting facilities to control quality and lead times. These players bypass traditional intermediaries, offering competitive pricing on mid-range products while maintaining technical specs like seam strength and colorfastness. Their strategy centers on data-driven inventory—producing small batches of trending styles (like the 2026 'clean fit' silhouette) based on real-time demand signals.

Heritage European Mills

These family-owned producers control premium fiber sources and have generational expertise in twist and finishing techniques. Their competitive advantage is brand cachet and certification portfolios that luxury houses require.

Scale-Focused Asian Manufacturers

They dominate volume with cost-efficient production of mid-range wool, cotton, and acrylic sweaters. Their edge is speed-to-market and capacity for private-label programs under buyer-owned brands.

Direct-to-Brand Knit Specialists

Mid-size manufacturers that operate their own knitting floors and offer design-to-delivery services. They specialize in small-batch, data-driven runs for emerging direct-to-consumer brands.

5. Market Trends

1. Technology-Driven Transformation

Artificial intelligence, IoT sensors, and advanced data analytics are fundamentally reshaping production efficiency, quality control, and demand forecasting in Men's Sweater Knitwear. Leading manufacturers deploying smart sensors and automated production lines have reduced operational costs by 12-18% while maintaining defect rates below 0.5%. With over 60% of industry participants projected to complete initial digital transformation by 2028, this shift represents a competitive imperative rather than an option.

2. Sustainability and Regulatory Compliance

Global carbon border adjustment mechanisms (CBAM) and rising consumer environmental awareness are forcing Men's Sweater Knitwear companies to elevate sustainability from marketing rhetoric to core business strategy. Carbon footprint tracking, recycled material substitution, and zero-waste production systems have become baseline requirements for winning large-scale B2B contracts. ESG rating agencies increased their sector coverage intensity by 35% year-over-year in 2025.

3. Supply Chain Resilience and Regionalization

Geopolitical tensions and post-pandemic supply chain disruption lessons are driving Men's Sweater Knitwear companies to accelerate supply base diversification. The China+N strategy and nearshoring are becoming mainstream, with companies establishing secondary supply sources in Southeast Asia, Eastern Europe, and Mexico to reduce single-source dependency from 75% to below 40%. This structural shift significantly enhances risk resilience and buyer confidence.

4. Consumer Demand Upgrading and Personalization

Middle-class expansion and Gen Z purchasing power are driving Men's Sweater Knitwear from standardized mass production toward personalized customization and small-batch agile manufacturing. C2M (Consumer-to-Manufacturer) models and flexible production lines enable companies to compress new product launch cycles from 18 months to 3-4 months. This trend is particularly pronounced in premium market segments, where personalized products typically command gross margins 8-15 percentage points above standard offerings.

6. Regional Markets

Asia-Pacific (Production Hub)

China, Bangladesh, and Vietnam produce over 70% of global sweater volume. Supply chain advantages include low labor costs and integrated fiber mills, but rising wages are shifting premium work to South Asia.

Europe (Premium & Innovation)

Italy, Scotland, and Ireland lead in high-end cashmere and wool sweaters. They invest heavily in R&D for sustainable fibers and digital knitting, setting trends for the global market.

North America (Import & Demand)

The US is the largest importer of men's sweaters, with a growing preference for traceable, eco-certified products. Canadian brands are also emerging as champions of ethical knitwear sourcing.

7. Investment Outlook

Two opportunities stand out. First, the B2B sourcing shift toward verified ethical production creates a premium for suppliers that can provide traceability—especially for cashmere and Merino wool. Second, the 'year-round layering' trend in moderate climates opens a new product category: lightweight, breathable sweaters (18–21 gauge) that compete with shirts and hoodies.

The primary risk is raw material volatility. Cashmere prices have swung 30% in the past two years due to climate-driven yield drops in Inner Mongolia. Buyers should lock in multi-year contracts with mills that have diversified fiber sources and hedging strategies. Another risk is overcapacity in basic synthetic knits—commodity sweaters made from acrylic or polyester will face margin compression as consumers trade up to natural fibers.

Strategic Considerations:

- Ethical Cashmere Premium: Brands willing to pay for certified, traceable cashmere (RWS or Good Cashmere Standard) will capture the quiet-luxury consumer willing to spend $400+ per sweater.

- Year-Round Lightweight Knits: Developing 18–21 gauge merino and linen-blend sweaters for spring/summer layering can open new revenue streams outside the traditional winter season.

- Raw Material Volatility: Cashmere and high-grade wool prices fluctuate sharply due to climate events. Lock long-term contracts with hedging clauses or diversify into certified recycled fibers.

- Commodity Margin Compression: Basic acrylic or polyester sweaters face intense price competition from fast-fashion giants. B2B buyers should shift away from commodity SKUs toward differentiated natural-fiber products.

Frequently Asked Questions

Make Informed Decisions in the Men's Sweater Knitwear Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-12. All market figures are estimates and may vary from actual results.