Table of Contents

The global Pet Furniture industry serves consumers worldwide with diverse solutions.

1. Industry Overview

Americans will spend an estimated USD 2.59 billion on pet furniture in 2026 alone—a figure that underscores how deeply animal companionship has woven itself into household economics. This sector, once relegated to afterthoughts in hardware stores, now commands serious real estate in the home furnishings ecosystem, with dedicated aisles in major retailers and entire e-commerce categories devoted to pet-appropriate seating, shelter, and enrichment. The market's transformation from utilitarian crates to architecturally ambitious cat trees and orthopedic pet sofas reflects a fundamental shift in how humans view their animal charges: as family members deserving furniture designed for their comfort, not just containment. Manufacturers report that premium positioning—washable fabrics, multi-level configurations, and aesthetic matching with human décor—commands price premiums of 40-60% over baseline products, signaling that consumers increasingly view pet furniture as an extension of interior design rather than a disposable expense.

Industry Scope & Characteristics

Broad Product Portfolio

Products span pet beds, cat trees, dog crates, pet houses, pet carriers, feeding stations, pet toys, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

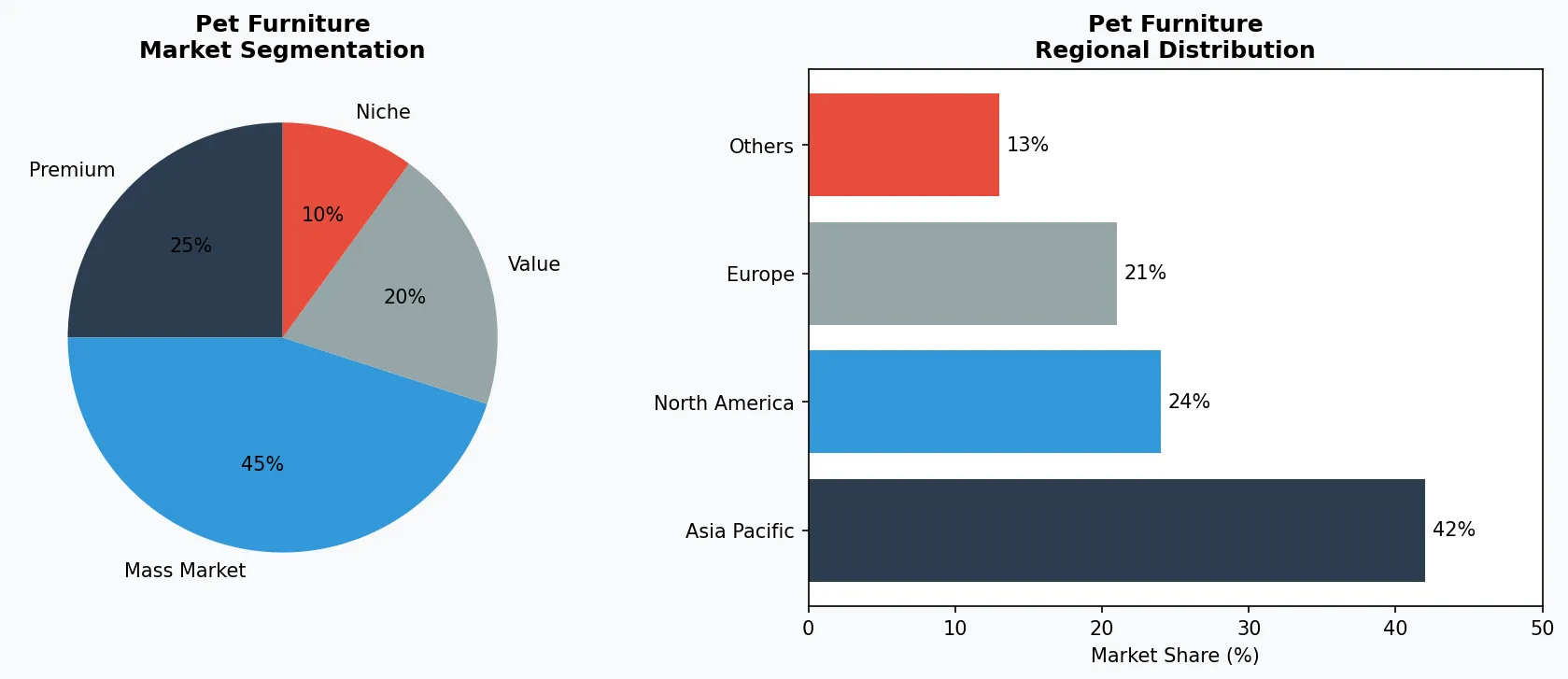

Key market segments and growth drivers in the Pet Furniture sector.

2. Market Analysis

The global pet furniture market is projected to grow from USD 2.4 billion in 2026 to USD 4.2 billion by 2036, registering a compound annual growth rate of 5.9%—a trajectory that outpaces many traditional furniture categories. In the United States specifically, the market is expected to expand at 6.2% CAGR, reaching USD 3.95 billion by 2033, driven by two intersecting forces: a 12% increase in pet ownership rates since 2020 and rising disposable incomes that enable households to allocate discretionary spending toward animal companions. The dog and cat furniture segment alone is projected to grow at 6.8% CAGR from 2023 through 2030, reflecting concentrated demand in these two pet categories. E-commerce channels now account for approximately 45% of sales, with Amazon, Chewy, and specialty platforms capturing consumers who research specifications like load capacity and material成分 before purchasing—a marked difference from the impulse-driven玩具 market that dominated pet retail a decade ago.

Market segmentation and regional distribution analysis for Pet Furniture.

3. Product Categories

Pet beds and sofas represent the largest revenue category, with orthopedic memory foam models driving margin expansion as aging pets and informed consumers seek therapeutic benefits. Furhaven has captured significant share in this segment with its removable cover designs and temperature-regulating fillers, while entry-level competitors like Ware continue serving price-sensitive buyers with basic cushioned options. Cat trees and scratching posts constitute the fastest-growing product sub-category, fueled by indoor cat populations that require environmental enrichment to prevent behavioral issues. Feandrea's multi-level models featuring sisal scratching surfaces and enclosed hideaways command premium positioning, while Petsfit offers collapsible alternatives for space-constrained urban apartments—a market segment expanding as metropolitan housing costs push renters toward smaller footprints. Pet houses and carriers round out the category, with hybrid designs that function as both indoor hideaways and portable transport containers gaining traction among frequent travelers who refuse to leave companion animals behind.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

4. Leading Players

Feandrea has distinguished itself through vertical integration, manufacturing directly in China while maintaining quality control standards that satisfy both Amazon's requirements and specialty retailer specifications. The company's strategy centers on rapid product iteration—launching 15-20 new SKUs annually—enabling rapid response to trending features like built-in storage compartments and modular expansion capabilities. Furhaven operates with a consumer-direct model that prioritizes review velocity and customer service response times, achieving above-average ratings on major platforms through consistent quality and proactive replacement policies for defective units. The brand's investment in therapeutic pet products, including heated beds and supportive ramps, positions it to capture demographic tailwinds as pet life expectancy increases alongside veterinary advances. Petsfit differentiates through space-efficient design philosophy, targeting apartment dwellers and frequent relocators who value furniture that adapts to changing living situations. Amy maintains a manufacturing-first approach, supplying private-label products to retailers while building its own branded portfolio, creating resilience against platform-specific sales disruptions that have crippled competitors dependent on single e-commerce channels.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the pet furniture space.

5. Market Trends & Innovations

1. Sustainability & Eco-Friendly Innovation

Sustainability has become a core competitive priority. Companies like Petco and PetSmart are investing in eco-friendly materials, carbon-neutral production, and circular economy initiatives to meet growing consumer demand for responsible products.

2. Digital Transformation & E-Commerce Growth

The shift to digital sales channels continues to accelerate. MidWest Homes for Pets and K&H Manufacturing are leveraging data analytics, AI-driven personalization, and omnichannel strategies to enhance customer engagement and streamline distribution.

3. Premiumization & Product Innovation

Rising consumer expectations are driving premiumization across the market. Frisco (Chewy) has introduced high-end product lines, while GoPet focuses on innovative features and superior quality to capture value-conscious yet quality-seeking customers.

4. Health, Wellness & Functional Benefits

Health-oriented consumer preferences are reshaping product development. Arf Pets and Molly Mutt are pioneering functional products with demonstrable benefits, commanding premium pricing and driving category expansion.

6. Regional Markets

The United States remains the largest single-country market, accounting for approximately 38% of North American pet furniture revenue. West Coast metropolitan areas—particularly San Francisco, Seattle, and Portland—drive disproportionate premium product demand, with consumers in these markets spending 2.3x the national average on individual pet furniture items. European markets, led by Germany, the United Kingdom, and France, emphasize design aesthetics and sustainability certifications, creating opportunities for brands that invest in environmental claims and minimalist styling. The Asia-Pacific region represents the highest-growth geography, with China's middle-class pet ownership expanding at 18% annually and Japan experiencing renewed cat-focused product demand as single-person households seek companionship without the space requirements of canine ownership. Urban density in cities like Tokyo and Shanghai drives demand for vertical cat furniture and multi-functional pieces that maximize limited square footage.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities define the sector's near-term trajectory: First, the integration of health monitoring sensors into pet furniture—weight scales embedded in beds, activity trackers in trees—positions manufacturers to capture share in the $4.2 billion pet wellness technology market. Second, rental-housing-compatible designs addressing lease restrictions on permanent pet modifications represent an underserved segment as housing costs push younger consumers toward flexible living arrangements. However, regulatory risk looms: proposed legislation in California and New York requiring flame retardant standards for pet products would force manufacturing overhauls, potentially adding $3-5 per unit in compliance costs at a moment when price sensitivity remains elevated among inflation-weary consumers. Brands that proactively adopt anticipated standards before mandates take effect will secure cost advantages and retailer relationships unavailable to reactive competitors.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Pet Furniture Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-18. All market figures are estimates and may vary from actual results.