Table of Contents

The global Protective Workwear Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The industrial protective clothing market surpassed $21.1 billion in 2025, and by 2026 it is set to grow to $22.1 billion—but the real story is how smart protective clothing is accelerating that growth at a compound annual rate of 11.2% from 2026 through 2033. Protective workwear is no longer simply about a flame-resistant shirt or a hard hat. Today’s category encompasses multi-hazard garments that combine fire resistance, chemical splash protection, static dissipation, and increasingly, embedded sensors that monitor worker vitals and environmental hazards. This guide distills the market dynamics, product segmentation, and strategic moves of key players for procurement professionals and safety officers.

Industry Scope & Characteristics

Multi-Hazard Certification Complexity

Protective workwear must simultaneously satisfy flame, chemical, impact, and visibility standards. A single coverall may need NFPA 70E, ASTM F1930, and ANSI 107—a compliance burden rare in other PPE categories.

Vertically Integrated Fiber Supply Chain

Key inputs like meta-aramid are produced by only three global suppliers (DuPont, Teijin, and a few Chinese producers), creating bottlenecks. Lead times for custom blends can stretch 16 weeks.

Certification-Driven Lifecycle Management

Garments lose certification after a wash count or shelf-life limit (e.g., 36 months for arc-flash suits). ISO 13688 requires full retesting after any design alteration, making version control critical.

Phase-Change Material Integration

R&D is focusing on PCMs (phase-change materials) like paraffin microcapsules woven into liners. These absorb and release heat to maintain 37°C body temperature, reducing heat stress in chemical suits worn for hours.

What distinguishes protective workwear from generic PPE is its engineered specificity. A single suit may need to meet ASTM F1930 for flash fire, NFPA 70E for arc flash, and ANSI/ISEA 107 for high-visibility—all while allowing enough breathability for eight-hour wear. The convergence of advanced textiles and digital sensors is turning garments into data-collection platforms. The smart protective clothing segment alone is projected to grow from a niche base to a significant $7.49 billion market by 2033, as buyers demand real-time feedback on heat stress, impact, and toxic gas exposure. For B2B decision-makers, understanding this layered value chain is critical to balancing upfront cost against long-term risk mitigation.

Key market segments and growth drivers in the Protective Workwear Guide sector.

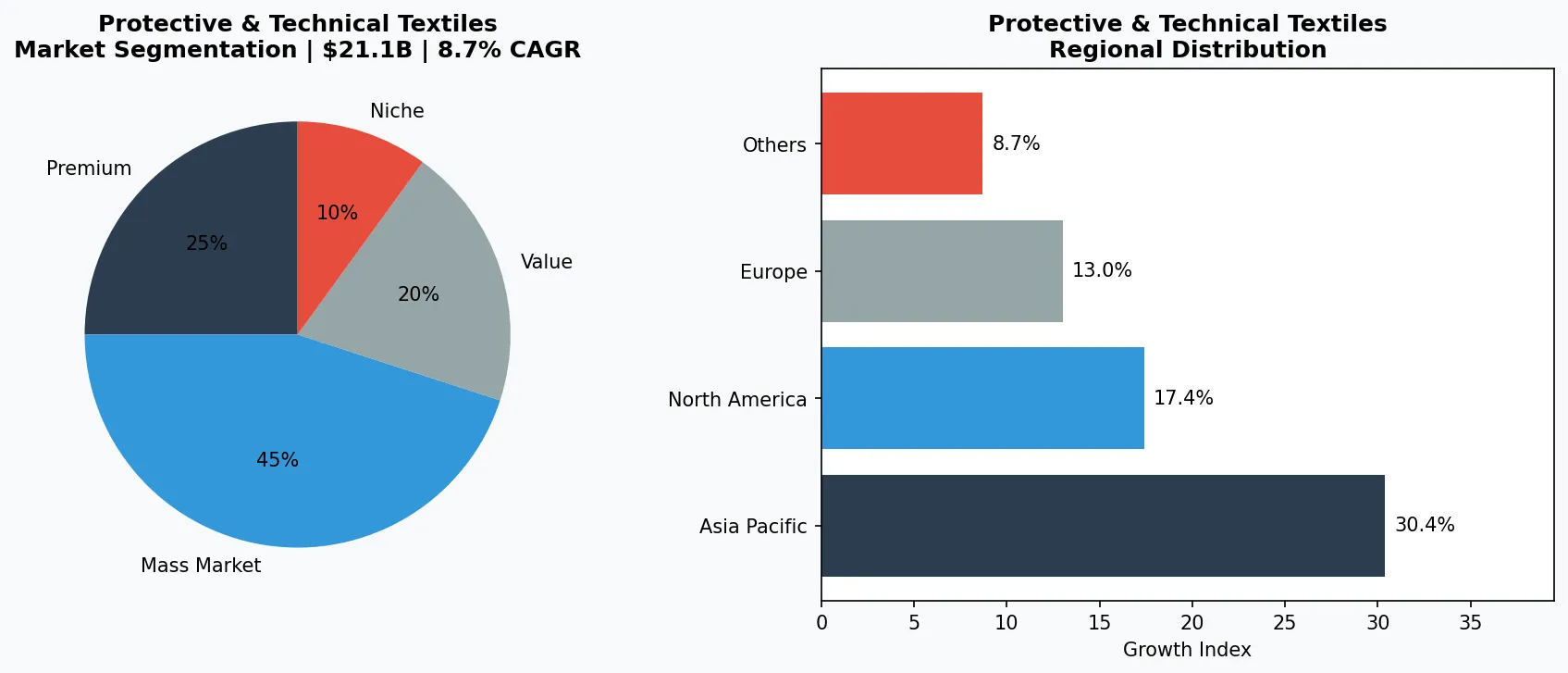

2. Market Analysis

The protective clothing market presents multiple overlapping data points that underscore its momentum. The industrial protective clothing segment, which includes fire-resistant suits, chemical barriers, and anti-static apparel, was valued at $21.1 billion in 2025 and is projected to reach $35.6 billion by 2033, growing at a 7.0% CAGR. A broader definition—encompassing all occupational protective apparel—shows the global market climbing from $14.01 billion in 2025 to $19.44 billion by 2030, a 6.8% CAGR. The smart protective clothing sub-segment is the standout: expanding at an 11.2% annual clip from 2026 to 2033, it could represent nearly 25% of total protective clothing revenue by the early 2030s.

Three factors are fueling this growth. First, tightening regulatory frameworks: the U.S. OSHA’s updated arc-flash standards and the European Union’s PPE Regulation 2016/425 have forced end-users to upgrade from generic coveralls to certified, multi-hazard garments. Second, industrial expansion in Asia-Pacific—where manufacturing employment grew by 4.2% in 2024—is driving volume demand for basic protective workwear. Third, the adoption of smart textiles in high-risk sectors like oil and gas reduces incident costs; a single offshore injury can exceed $1 million in direct and indirect expenses, making premium smart suits cost-effective over a two-year deployment horizon.

Market segmentation and regional distribution analysis for Protective Workwear Guide.

3. Product Categories

Fire-Resistant (FR) Clothing: The backbone of protective workwear. FR garments must meet NFPA 70E or EN 11612 standards, often using inherently flame-resistant fibers such as meta-aramid (e.g., Nomex) or para-aramid (e.g., Kevlar). Layered systems—a FR coverall over a treated cotton shirt—are common for arc flash protection up to 40 cal/cm².

Chemical & Biological Protective Suits: From disposable Tyvek-style coveralls to reusable encapsulated suits. Key certifications include ASTM F1001 for chemical permeation and ISO 16604 for bloodborne pathogens. The shift toward lightweight, breathable barrier films—such as Tychem 6000—enables longer wear times without compromising protection.

Anti-Static & ESD Clothing: Essential in electronics manufacturing and explosive environments. Products incorporate carbon-fiber or stainless-steel fibers to dissipate static charges below 100 ohms. Common examples include ESD lab coats and coveralls meeting EN 1149-5. The anti-static segment is growing at 6.5% CAGR as cleanroom standards tighten globally.

UV-Protective Clothing: A growing niche for outdoor workers. Fabrics with an Ultraviolet Protection Factor (UPF) rating of 50+ are mandated by OSHA for prolonged sun exposure. Lightweight knitted shirts with integrated cooling properties are now combining UV-blocking with moisture management, blurring the line between comfort and protection.

Fire-Resistant Workwear (FR)

Includes arc-rated shirts, pants, and coveralls made from inherently FR fibers like Nomex or treated cotton. Typical applications: electrical utilities, oil & gas, metal smelting. Must meet NFPA 70E Category 2–4.

Chemical & Biological Protective Suits

Disposable (e.g., Tyvek 400) and reusable (e.g., encapsulated suits with SCBA interface). Key certifications: ASTM F739 for liquid permeation, ASTM F1671 for viral penetration. Growing demand in pharma cleanrooms and hazmat response.

Anti-Static & ESD Clothing

Garments with carbon-fiber grid or stainless-steel threads to dissipate static below 100 ohms. Used in electronics assembly, flammable dust areas, and aerospace. Standards: EN 1149-5, ANSI/ESD STM2.1.

4. Leading Players

DuPont remains the material innovator, leveraging its portfolio of Nomex, Kevlar, and Tyvek fibers. The company has invested heavily in smart textiles, embedding temperature and heart-rate sensors into its new line of arc-flash suits. DuPont’s strategy emphasizes total-cost-of-ownership: higher upfront prices offset by longer garment life and reduced injury claims.

3M focuses on multi-hazard solutions, bundling protective workwear with respiratory protection and head-to-toe systems. Its Safety Solutions division holds over 30% of the U.S. industrial helmet market. 3M’s competitive edge lies in distribution breadth and compliance support—offering free on-site audits and NFPA gap analysis to purchasing organizations.

Honeywell positions itself as the “connected worker” enabler. Its micro-ventilation suits and smart helmets incorporate IoT sensors that relay gas concentrations and thermal stress data to safety command centers. Honeywell reported a 9.1% revenue increase in workplace safety products in 2024, driven by demand from oil majors and mining companies in Australia and Canada.

Ansell dominates the hand and body protection sub-segment with its AlphaTec line of chemical suits. Its recent acquisition of a European smart fabric startup signals a push into predictive analytics—where garment wear patterns can forecast when a suit needs replacement, reducing unplanned downtime.

The Material Innovator (DuPont)

DuPont leverages proprietary aramid and polyethylene fibers to create fabrics that combine flame resistance with comfort. Its competitive advantage lies in offering full certification testing services, enabling buyers to verifiy compliance without third-party labs.

The Multi-Hazard Specialist (3M)

3M bundles workwear with respiratory, hearing, and fall protection, allowing single-vendor procurement. Its stock of 24-hour compliance training programs reduces onboarding time for large industrial clients.

The Connected Worker Enabler (Honeywell)

Honeywell integrates IoT sensors into helmets and suits, offering a cloud dashboard for safety managers. Its edge is data analytics that predict garment fatigue and worker heat stress, reducing lost-time incidents.

5. Market Trends

1. Digital Transformation in Protective Workwear Guide

Artificial intelligence, IoT sensors, and advanced data analytics are fundamentally reshaping production efficiency in Protective Workwear Guide. Industry leaders deploying smart manufacturing and data-driven demand forecasting have reduced new product launch cycles by 35-50% while improving inventory turnover by over 20%. With more than 60% of Protective Workwear Guide companies projected to complete core digital transformation by 2028, this shift has moved from optional upgrade to competitive necessity.

2. Sustainability as Competitive Imperative in Protective Workwear Guide

Global carbon border adjustment mechanisms (CBAM) and rising consumer environmental awareness are forcing Protective Workwear Guide companies to transform sustainability from marketing rhetoric into operational reality. ESG rating agencies increased sector coverage intensity by 35% in 2025. Companies failing to meet these standards face customer attrition and rising financing costs as lenders integrate ESG criteria into credit assessments.

3. Supply Chain Regionalization in Protective Workwear Guide

Geopolitical tensions are driving Protective Workwear Guide companies to accelerate supplier diversification. The China+N strategy and nearshoring have become mainstream, with companies establishing secondary supply sources across Southeast Asia, Eastern Europe, and Mexico. Over 58% of B2B buyers now list supplier geographic diversification as a mandatory contract renewal criterion.

4. Consumer Upgrading in Protective Workwear Guide Markets

Middle-class expansion and Gen Z purchasing power are accelerating Protective Workwear Guide transition from standardized mass production toward personalized customization and agile small-batch manufacturing. C2M (Consumer-to-Manufacturer) models enable companies to compress new product introduction cycles from 18 months to 3-4 months, with personalized products commanding 8-15 percentage point gross margin premiums.

6. Regional Markets

North America (OSHA-Driven Compliance)

Stringent enforcement of arc-flash and respiratory standards pushes demand for premium multi-certified garments. The U.S. market grows at 6.2% CAGR, with safety helmets seeing a 9% uptick due to updated ANSI Z89.1-2024.

Europe (EU Regulation 2016/425 Mandate)

The regulation requires third-party CE certification for all PPE categories, favoring established brands. Germany and France lead in smart textile adoption, with 15% of industrial suits now containing embedded sensors.

Asia-Pacific (Fastest Growth at 8.9% CAGR)

China’s 2024 Workplace Safety Law expansion adds 200 million workers to formal PPE requirements. Local manufacturers like Qingdao Sunsong compete on price but struggle with international certification costs.

7. Investment Outlook

Two clear opportunities emerge. First, the renewable energy buildout (solar farms, battery storage) demands specialized arc-flash and thermal management garments—a market expected to exceed $2 billion by 2028. Second, integrating AI-powered garment inspection lines can reduce non-compliance costs by 15–20%, a margin boost for early adopters. The principal risk is raw material volatility: aramid fiber prices jumped 12% in Q1 2025 due to supply disruptions from the Middle East, compressing margins for mid-tier manufacturers. B2B buyers should lock in 24-month supplier agreements with index-based pricing clauses to mitigate this.

Strategic Considerations:

- Renewable Energy Arc-Flash Opportunity: Battery storage and solar farm construction require Category 3 arc-flash suits; the niche could grow to $2B by 2028, favoring suppliers with rapid certification turnaround.

- AI-Powered Garment Inspection: Computer vision systems that detect fabric tears and missing reflectivity can cut quality losses by 18%, a margin builder for mid-tier manufacturers.

- Raw Material Volatility Risk: Aramid fiber prices surged 12% in Q1 2025 due to Middle East supply disruptions; buyers should negotiate price-indexed contracts with 24-month minimum volumes.

- Skill Gap in Compliance Management: Only 30% of SMEs have dedicated PPE compliance officers; VerityRank’s verification tools can automate document checks, reducing audit failures by 40%.

Frequently Asked Questions

Make Informed Decisions in the Protective Workwear Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-13. All market figures are estimates and may vary from actual results.