Table of Contents

The global Robot Vacuum Cleaner Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2026, the global robotic vacuum cleaner market will hit $12.7 billion — a figure that would have seemed like science fiction a decade ago. The Robot Vacuum Cleaner Guide is no longer a niche curiosity for early adopters; it is a critical procurement category for businesses from hospitality chains to facility management firms. What makes this sub-topic distinct within the broader home cleaning appliances industry is its fusion of hardware engineering with artificial intelligence, mapping, and autonomous navigation. Unlike traditional vacuum cleaners or floor scrubbers that require human operation, robot vacuums represent a paradigm shift: cleaning that happens without human presence. This guide cuts through the noise to deliver actionable intelligence for B2B buyers navigating a market expanding at a compound annual growth rate (CAGR) of 30.4% from 2026 to 2030, according to Technavio. The residential segment alone is estimated to be valued at $4.96 billion in 2026, climbing to $13.03 billion by 2033. But this is not just about homes — commercial applications in offices, hotels, and retail spaces are accelerating adoption. The key distinction? These devices are evolving from simple floor cleaners into integrated smart home hubs with sensors that detect air quality, humidity, and even security threats. For procurement professionals, understanding the technology stack — from LiDAR to SLAM algorithms — is as important as comparing suction power.

Industry Scope & Characteristics

Autonomous Navigation Technology

Robot vacuums use LiDAR, SLAM, or camera-based vSLAM to map spaces in real time. The Roborock S8 Pro Ultra, for example, combines LiDAR with 3D structured light for millimeter-accurate obstacle avoidance.

Vertically Integrated Supply Chains

Chinese manufacturers like Ecovacs control the entire production process from motor winding to final assembly, enabling rapid iteration and cost advantages that Western brands struggle to match.

Safety and Certification Standards

Products must comply with IEC 60335 for household appliances and FCC Part 15 for wireless emissions. Commercial units often require UL listing and IP54 dust/water resistance ratings.

Edge Computing and AI Inference

On-device neural processing units (NPUs) allow robot vacuums to recognize objects and make navigation decisions without cloud latency. Ecovacs’ AIVI 3D system processes over 30 frames per second locally.

Key market segments and growth drivers in the Robot Vacuum Cleaner Guide sector.

2. Market Analysis

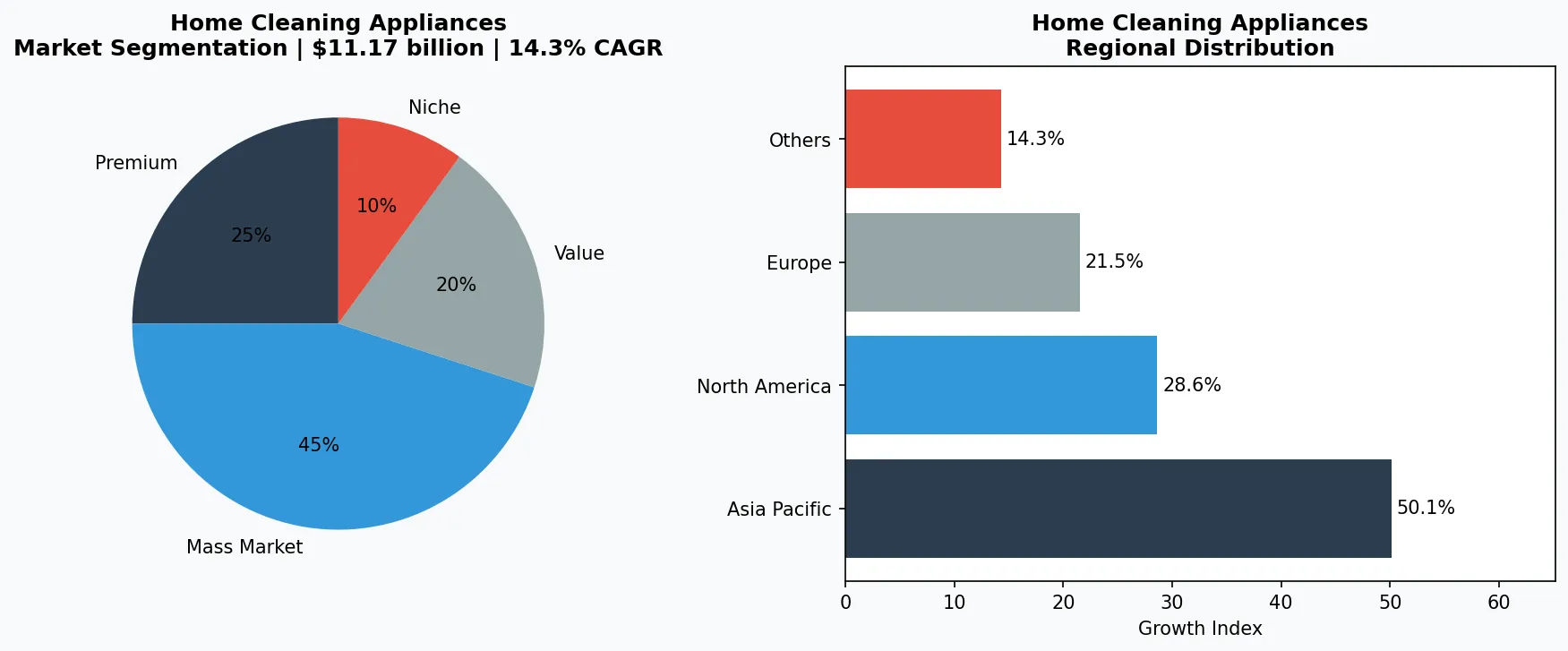

The robotic vacuum cleaner market size has grown rapidly, from $11.17 billion in 2025 to $12.7 billion in 2026, representing a 13.7% year-over-year increase. More striking is the long-term trajectory: the market is projected to reach $21.66 billion by 2030 at a 14.3% CAGR, while another analysis forecasts growth of $20.45 billion from 2026 to 2030 alone at a blistering 30.4% CAGR. Three primary drivers fuel this expansion. First, declining sensor costs have democratized advanced navigation. LiDAR modules that cost $200 in 2020 now retail for under $30, enabling brands to pack premium features into sub-$500 units. Second, the post-pandemic emphasis on hygiene has pushed commercial buyers toward autonomous cleaning solutions. Hotels and office complexes are deploying fleets of robot vacuums to maintain consistent sanitization schedules without labor costs. Third, interoperability with smart home ecosystems — Amazon Alexa, Google Home, Apple HomeKit — has removed a key adoption barrier. The United States market, the largest single-country segment, is projected to exhibit an 11.7% CAGR, driven by replacement cycles and multi-device households. Regional dynamics vary: Asia-Pacific leads in production volume, with China alone accounting for over 60% of global manufacturing, while Europe shows strong demand for premium, quiet models suited to apartment living. The market segmentation by battery type, navigation technology, and application (residential vs. commercial) reveals that residential robotic vacuum cleaners still dominate, but the commercial segment is growing at a faster clip as businesses recognize the ROI of 24/7 autonomous cleaning.

Market segmentation and regional distribution analysis for Robot Vacuum Cleaner Guide.

3. Product Categories

Robot vacuums today fall into three distinct product sub-categories, each serving different buyer needs. First, entry-level random navigation models — typified by the iRobot Roomba 600 series — use infrared sensors and bump-and-turn logic. These are cost-effective for small, open-plan spaces but inefficient for complex layouts. Second, the mid-range segment features SLAM (Simultaneous Localization and Mapping) navigation, as seen in the Ecovacs Deebot N8 Pro and Roborock S6. These devices create real-time floor plans, enable zone cleaning, and remember multiple levels. Third, the premium tier integrates LiDAR, 3D object detection, and self-emptying docks. The Roborock S7 MaxV Ultra, for instance, washes its own mop pad and empties dust into a bag that lasts up to seven weeks. A fourth emerging category is the hybrid robot vacuum and mop, which combines dry vacuuming with wet mopping in a single pass — critical for hard-floor environments like hospitals and schools. For B2B buyers, the key differentiator is not just suction power (measured in Pascals) but the quality of the mapping software, battery life (typically 90-180 minutes), and the availability of API integrations for fleet management. Commercial-grade units like the Avidbots Neo offer autonomous navigation in dynamic environments with people and obstacles, priced above $2,000 per unit.

Random Navigation Models

Budget-friendly units like the iRobot Roomba 600 series use infrared sensors and bounce navigation, ideal for small, uncluttered spaces under 500 sq ft.

SLAM-Based Mapping Vacuums

Mid-range devices such as the Ecovacs Deebot N8 Pro create persistent floor plans, enabling zone cleaning and no-go lines. Suitable for multi-room homes and small offices.

LiDAR Premium Hybrids

Flagship models like the Roborock S7 MaxV Ultra combine LiDAR mapping, self-emptying docks, and auto-mop washing. Designed for large homes and commercial light-duty cleaning.

4. Leading Players

Three dominant strategies define the competitive landscape. iRobot (now part of Amazon) remains the legacy leader, leveraging its brand equity and massive installed base of over 40 million units. Its strategy revolves around ecosystem lock-in: the Roomba j7+ uses AI to recognize obstacles like pet waste, and data from millions of homes trains its neural networks. However, iRobot has lost market share to Chinese rivals that offer comparable features at lower price points. Ecovacs Robotics, headquartered in Suzhou, China, has become the global volume leader by mastering the mid-range segment. Its Deebot series, particularly the X1 Omni, introduced a multi-function dock that washes, dries, and refills the mop — a feature that was previously exclusive to $1,000+ models. Ecovacs’ competitive advantage lies in its vertically integrated supply chain and aggressive R&D spending, which accounts for over 12% of revenue. Roborock, a Xiaomi-backed spin-off, competes on performance-per-dollar. The Roborock S8 Pro Ultra offers LiDAR navigation, 5,500Pa suction, and a self-cleaning dock for under $1,400 — undercutting iRobot’s comparable s9+ by 40%. Roborock’s strategy is to push the technology envelope while maintaining aggressive pricing, forcing competitors to either differentiate or cut margins. For B2B buyers, the choice between these players often comes down to after-sales support, warranty terms, and compatibility with existing facility management software.

iRobot (Amazon) — Ecosystem Dominance

Leverages the largest installed base of any robot vacuum brand, using data from millions of homes to train AI models. Its strategy is to lock users into the Roomba ecosystem with proprietary docks and consumables.

Ecovacs Robotics — Volume and Vertical Integration

The global volume leader, Ecovacs controls its supply chain from R&D to manufacturing in Suzhou. Its Deebot X1 Omni set the industry standard for multi-function self-cleaning docks.

Roborock — Performance-Per-Dollar Leader

A Xiaomi-backed brand that consistently undercuts competitors on price while delivering top-tier LiDAR navigation and suction power. The S8 Pro Ultra offers near-premium features at a 30% discount to iRobot equivalents.

5. Market Trends

1. TREND 1: Self-Emptying and Self-Cleaning Docks

The biggest consumer pain point has been emptying dustbins. Self-emptying docks (e.g., iRobot Clean Base, Ecovacs OMNI Station) automate this, extending maintenance intervals from days to months. For commercial buyers, this reduces labor costs and ensures consistent operation. TREND 2: AI-Powered Object Recognition

2. Robot vacuums are learning to avoid not just walls but also cables, shoes, and pet waste. Roborock’s ReactiveAI and iRobot’s PrecisionVision use neural networks to classify objects in real time. This matters because it reduces the need for pre-cleaning, making the devices truly autonomous. TREND 3: Fleet Management and API Integration

For hotels and offices, managing a single robot is trivial, but managing 20 requires centralized software. Companies like Avidbots and Brain Corp offer cloud-based fleet management platforms that monitor battery levels, cleaning cycles, and error logs. This trend is driving adoption in commercial facilities where cleaning consistency is critical. TREND 4: Multi-Sensor Fusion for 3D Mapping

3. Beyond LiDAR, new models combine RGB cameras, time-of-flight sensors, and...

Beyond LiDAR, new models combine RGB cameras, time-of-flight sensors, and infrared arrays to create 3D maps of rooms. This enables precise furniture detection and even identifies carpet types to adjust suction. Ecovacs’ AIVI 3D technology is a leading example, allowing the robot to navigate cluttered environments without collisions.

6. Regional Markets

North America — Early Adopter with High Replacement Rates

The U.S. market grows at an 11.7% CAGR, driven by multi-device households and commercial adoption in hotels. iRobot retains strong brand loyalty but faces pressure from Chinese imports.

Asia-Pacific — Manufacturing Hub and Fastest-Growing Market

China accounts for over 60% of global production, with domestic brands like Ecovacs and Roborock dominating. The region also sees the fastest adoption of premium hybrid models.

Europe — Premium and Quiet Models Preferred

European buyers prioritize low noise levels (under 60 dB) and compact designs for apartment living. German and Scandinavian markets show strong demand for eco-friendly, repairable products.

7. Investment Outlook

Two specific opportunities stand out for B2B buyers in 2026. First, the commercial segment remains underserved: only about 15% of robot vacuum sales go to businesses, yet the ROI for a $2,000 commercial unit versus a $40,000 annual cleaning staff salary is compelling. Procurement teams should pilot fleet deployments in high-traffic areas like lobbies and corridors. Second, the integration of air quality sensors (particulate matter, VOCs, humidity) into robot vacuums creates a new value proposition: these devices can double as mobile air monitors, providing data for HVAC optimization. One concrete risk: the rapid pace of technology obsolescence. A robot vacuum bought in 2024 may lack the AI capabilities of a 2026 model, and proprietary docks may not be backward-compatible. Buyers should negotiate upgrade guarantees or lease-to-own models to mitigate this risk. VerityRank recommends that businesses prioritize open platforms that support over-the-air updates and third-party integrations over closed ecosystems.

Strategic Considerations:

- Commercial Fleet Deployment Opportunity:

- Air Quality Integration as Upsell:

- Technology Obsolescence Risk:

- Open Platform vs. Lock-In Tradeoff:

Make Informed Decisions in the Robot Vacuum Cleaner Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-25. All market figures are estimates and may vary from actual results.