Table of Contents

The global Seafood Snacks Collection sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Forget potato chips and candy bars; the next major shift in global snacking is swimming onto shelves. The Seafood Snacks Collection represents a disruptive niche within the broader Bakery Ingredients & Ready-to-Eat Snacks industry, defined by its fusion of convenience, high-protein nutrition, and oceanic flavors. This segment is distinct from traditional savory snacks, capitalizing on a fundamental consumer pivot away from empty carbohydrates toward functional, satiating ingredients. It’s not just about canned tuna anymore; it’s a diverse category encompassing shelf-stable, portable, and indulgent formats that appeal to health-conscious and adventurous eaters alike.

Industry Scope & Characteristics

Broad Product Portfolio

Products span dried shrimp, seaweed snacks, crispy squid, fish flakes, dried scallops, kelp noodles, seasoned seaweed, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Driving this surge is a powerful demographic force: Gen Z's interest in seafood snacks has jumped 23% year-over-year, according to Tastewise data. This isn't a fleeting trend but a recalibration of snack priorities, with tinned fish alone seeing a 14% annual increase on menus. The movement aligns with a broader dietary shift where consumers are actively cutting back on traditional salty snacks, liquor, soda, and bakery items to focus more on protein and fiber. Seafood snacks sit squarely at this intersection, offering a legitimate nutritional upgrade without sacrificing the convenience that defines modern snacking.

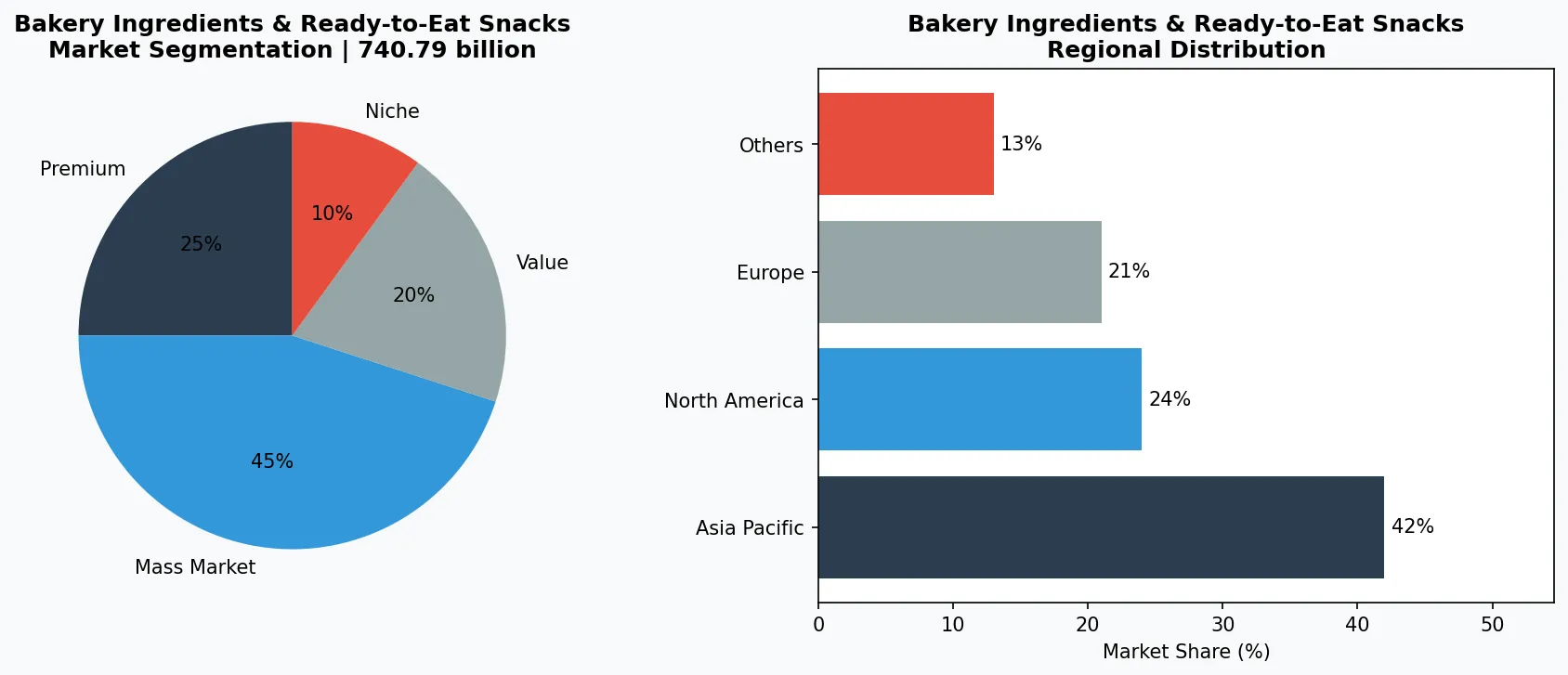

The financial scale of this opportunity is anchored in the massive underlying seafood market, estimated to reach USD 740.79 billion by 2026. The ready-to-eat seafood snacks segment is a high-growth vector within this vast ocean, projected to swell from USD 6.4 billion in 2025 to USD 11.0 billion by 2035. This growth trajectory signals that seafood is successfully transitioning from the center of the dinner plate to an anytime, anywhere protein source, creating a new and lucrative product category for suppliers and brands globally.

Industry application and market overview for Seafood Snacks Collection.

2. Market Analysis

The seafood snacks market is poised for significant expansion, with clear numerical boundaries defining its potential. The overarching seafood industry provides the foundational volume, growing from a 2025 value of USD 719.08 billion to an estimated USD 740.79 billion in 2026. Within this, the dedicated ready-to-eat seafood snacks niche is on a steeper climb, forecast to grow at a CAGR of 5.5% from USD 6.4 billion in 2025 to USD 11.0 billion by 2035. This disparity in growth rates highlights the snackification of seafood as a primary accelerator.

Three core drivers are fueling this growth. First is the relentless demand for healthy, protein-rich snack options. As consumers consciously reduce intake of traditional bakery snacks and salty chips, they are seeking alternatives that provide sustained energy and nutritional benefits. Seafood, naturally high in protein, omega-3 fatty acids, and essential minerals, perfectly fits this functional snacking bill. Second is the powerful influence of culinary trends permeating retail, evidenced by the 14% year-over-year rise of tinned fish on restaurant menus. This gourmet validation trickles down, educating palates and building comfort with seafood in casual formats.

Third is the critical element of convenience and format innovation. The success of this market hinges on moving beyond the canned goods aisle. Companies are winning by offering seafood in formats familiar to snackers—such as jerky, puffed crisps, and seasoned shelf-stable pouches—that require no preparation and are suitable for desks, gym bags, and on-the-go consumption. This fusion of health cred, trend credibility, and ultimate convenience creates a compelling market proposition with ample room for segmentation and premiumization.

Market segmentation and regional distribution for Bakery Ingredients & Ready-to-Eat Snacks - Seafood Snacks Collection.

3. Product Categories

The Seafood Snacks Collection can be organized into several distinct product types, each catering to different usage occasions and consumer preferences. The first and most established category is **Shelf-Stable Prepared Seafood**. This includes tinned or pouched fish like sardines, mackerel, salmon, and mussels, often packed in olive oil, sauces, or with seasonings. Brands like Fishwife and Season have elevated this segment with premium packaging and unique flavor profiles, transforming a pantry staple into a trendy, Instagram-worthy snack.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

The second category is **Seafood Jerky and Dried Strips**. Taking cues from the massive meat jerky market, this type involves drying fish like salmon, tuna, or squid into a chewy, protein-dense strip. It offers a long shelf life, high portability, and a savory, umami flavor. This format directly targets the health and fitness snack segment, competing with beef and turkey jerky on nutritional merits like lower saturated fat.

The third emerging category is **Puffed and Crisped Seafood Snacks**. This includes shrimp chips, fish skin crisps, and puffed snacks made with seafood meal or powder. These products compete directly with conventional potato chips and crackers, offering a crunchy texture and distinctive seafood taste. They often leverage alternative cooking methods like baking to enhance their health profile, appealing to those seeking a savory crunch without the nutritional guilt of traditional fried snacks.

4. Leading Players

Several companies are strategically positioning themselves to capitalize on this growth. **Fishwife**, a direct-to-consumer brand, has become a poster child for the premium tinned fish movement. Their strategy revolves around exceptional design, ethical sourcing, and chef-driven flavor combinations, successfully rebranding canned seafood as a luxury pantry item for millennials and Gen Z. They are not just selling tuna; they are selling a lifestyle and aesthetic aligned with modern food values.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the bakery ingredients & ready-to-eat snacks space.

**Thai Union Group**, a global seafood powerhouse behind brands like Chicken of the Sea, represents the large-scale manufacturing approach. Their strategy involves leveraging existing supply chains and brand recognition to introduce convenient, ready-to-eat seafood snack formats, such as tuna salad kits and flavored pouch products, into mainstream grocery channels. They compete on scale, affordability, and widespread distribution.

**Ocean's Halo** exemplifies innovation at the intersection of seafood and other snack formats. While known for seaweed snacks, their strategic move into products like Salmon Jerky demonstrates how companies are expanding their portfolios to capture the protein snack seeker. Their strategy focuses on clean labels, simple ingredients, and crossing category boundaries to attract health-focused consumers who may be new to seafood snacks.

**General Mills**, through its venture arm, has invested in brands like **Tio Gazpacho** and others, indicating major food conglomerates' interest in adjacent, better-for-you categories. While not a pure-play seafood snack company, its activity signals strategic attention to the portable, nutritious snack space where seafood is gaining prominence, potentially foreshadowing future acquisitions or internal product development.

5. Market Trends

1. Premiumization & Ethical Sourcing

Premiumization & Ethical Sourcing — Consumers are willing to pay more for seafood snacks with transparent, sustainable sourcing and gourmet positioning. This matters as it builds brand trust and justifies higher price points. Fishwife executes this by partnering with specific fisheries and highlighting story-driven provenance.

2. Snackification of Fine Dining Ingredients

Snackification of Fine Dining Ingredients — Luxe seafood items like smoked salmon, trout roe, and ceviche-style preparations are moving into shelf-stable snack formats. This matters because it democratizes gourmet experiences and drives trial. Companies are creating pâtés, spreads, and marinated shellfish in single-serve packages.

3. Flavor Fusion & Global Inspiration

Flavor Fusion & Global Inspiration — Snack brands are incorporating global flavors like gochujang, yuzu, and chimichurri into seafood products. This matters for attracting adventurous eaters and expanding usage beyond traditional preparations. Season brand tinned fish uses flavors like Jalapeño & Olive Oil and Lemon & Black Pepper.

4. Hybrid Format Innovation

Hybrid Format Innovation — Blending seafood with other snack bases, such as seafood-based protein bars, crackers with integrated fish powder, or trail mixes with dried shrimp. This matters as it reduces the 'fishiness' barrier for new consumers and integrates seafood into established snack routines. Startups are experimenting with salmon protein bars and seaweed-infused cracker blends.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

The outlook for the Seafood Snacks Collection is robust, with two specific opportunities standing out. First is the untapped potential in **personalized nutrition**. As consumers seek snacks tailored to dietary goals—high protein for fitness, omega-3 for cognitive health—seafood snacks can be positioned with precise functional benefits, creating subscription boxes or targeted product lines. Second is **expansion into new retail channels** beyond grocery, including gyms, office provisioning services, travel hubs, and specialty vending machines, meeting consumers at their point of need.

The primary concrete risk is **supply chain volatility and sustainability scrutiny**. Climate change, overfishing concerns, and fluctuating ocean harvests can disrupt ingredient costs and availability. A single sustainability scandal or misstep in sourcing can severely damage a brand built on ethical credentials. Companies must invest in transparent, resilient supply chains and credible certifications to mitigate this existential risk.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Seafood Snacks Collection Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-23. All market figures are estimates and may vary from actual results.