Table of Contents

The global Shoe Care Products Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Shoe care products are no longer an afterthought in the fashion accessories ecosystem. With the global market valued at $4.47 billion in 2024 and forecast to reach $7.23 billion by 2032 (CAGR 6.20%), this segment is outpacing many traditional accessory categories like belts and scarves. The 2026 baseline of $5.56 billion, climbing to $8.51 billion by 2034 at a 5.46% CAGR, signals that footwear maintenance has become a non-negotiable consumer habit—driven by rising sneaker culture, premium leather investment, and sustainability mandates. What makes this sub-topic distinctive within fashion accessories is its dual role: protective consumable and style preservation tool. Unlike a watch or handbag that remains static after purchase, a shoe requires recurring care—creating repeat revenue streams for manufacturers and retailers alike. The shift from occasional polishing to routine cleaning, conditioning, and waterproofing has transformed shoe care from a commodity into a branded lifestyle category. Professional-grade products now command premium shelf space alongside luxury footwear, and B2B buyers must navigate a fragmented supply chain of chemical specialists, heritage brands, and fast-growing D2C disruptors. This guide dissects the market forces, product segments, and competitive dynamics that define this rapidly maturing industry.

Industry Scope & Characteristics

Recurring Consumption Model

Unlike most fashion accessories, shoe care products are consumables—conditioners, cleaners, and sprays get used up within 2–4 months, creating predictable repeat purchase cycles that B2B buyers can leverage for subscription or replenishment programs.

Chemical Formulation Complexity

Manufacturing requires specialized knowledge of surfactants, waxes, solvents, and bio-based polymers. Supply chain is concentrated among a few chemical raw material producers, with lead times often exceeding 8 weeks for specialty ingredients like natural carnauba wax.

Stringent Environmental & Safety Certifications

Products sold in the EU must comply with REACH, CLP, and the forthcoming PFAS ban. US-based brands often seek Green Seal or EPA Safer Choice certification. B2B buyers should verify supplier documentation for ISO 9001 (quality) and ISO 14001 (environmental management).

Packaging Innovation as Competitive Edge

Liquid shoe care products are heavy to ship, making packaging weight a key cost driver. Innovations like water-free wipes, concentrated powder refills, and lightweight spray bottles reduce freight costs by up to 30% while meeting sustainability targets.

Key market segments and growth drivers in the Shoe Care Products Guide sector.

2. Market Analysis

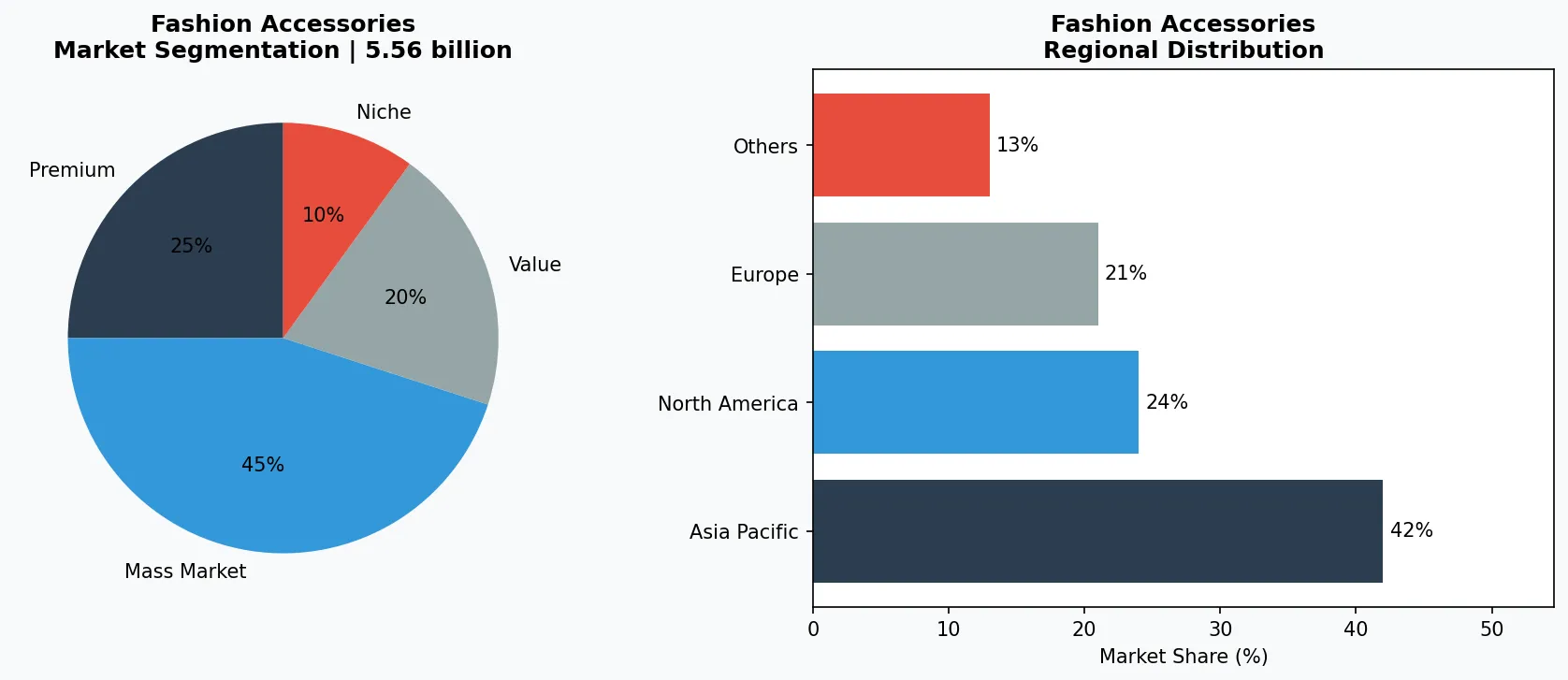

The shoe care products market is experiencing a structural growth phase that reflects deeper shifts in consumer spending and retail behavior. In 2024, the sector was valued at $4.47 billion, and projections estimate it will reach $7.23 billion by 2032 at a CAGR of 6.20%. Looking further ahead, another independent forecast pegs the market at $5.56 billion in 2026, expanding to $8.51 billion by 2034—a CAGR of 5.46%. A third analysis suggests a more conservative CAGR of 3.12% leading to $6.03 billion by 2034. The variance stems from differing scopes (e.g., inclusion of industrial shoe care vs. retail-only). The three biggest growth drivers are: (1) rising sneaker culture—limited-edition releases and collectible footwear have created a premium care niche where a $200 sneaker demands $30 in cleaning kits; (2) the premiumization of leather footwear, with consumers spending an average of $150–$300 per pair and expecting multi-season durability; and (3) the rapid penetration of online channels, which now account for over 40% of shoe care sales in North America and Europe. Regional dynamics are equally telling. Asia-Pacific is the fastest-growing market, led by China and India, where urbanization and rising disposable incomes are driving formal and casual footwear purchases—and the corresponding need for care products. Europe remains the largest regional market by revenue, thanks to a deep-rooted leather goods tradition and stringent environmental regulations that push innovation in water-based and biodegradable formulations.

Market segmentation and regional distribution analysis for Shoe Care Products Guide.

3. Product Categories

Leather Conditioners & Creams

The backbone of the premium shoe care segment. These products nourish and protect full-grain leather, patent leather, and suede. Key examples include top-grain leather balms and colored wax creams that restore original finish while adding a waterproof barrier. They typically contain lanolin, beeswax, or silicone-based compounds, and are sold in tins, tubes, or applicator bottles.

Sneaker & Fabric Cleaners

The fastest-growing sub-category. Formulated for mesh, canvas, and synthetic uppers, these foams, wipes, and sprays break down dirt without damaging delicate materials. Many now include deodorizing enzymes and are packaged in travel-friendly sizes. Major brands offer starter kits with brushes and microfiber towels.

Waterproofing Sprays & Sealants

A critical protective layer for all footwear. Spray-on silicones or fluoropolymer treatments create a invisible barrier against moisture and stains. These products have become essential for outdoor and work footwear, but are increasingly adopted for casual and luxury shoes to extend wear life.

Shoe Deodorizers & Inserts

Often overlooked but high-margin. Natural charcoal-based inserts, UV-activated sprays, and activated carbon powders address odor without masking. This segment is growing due to the athleisure trend and closed-toe shoe usage.

Leather Care & Conditioning

Includes creams, waxes, balms, and polishes formulated for different leather types (full-grain, patent, suede). Examples: colored shoe polish tins, mink oil conditioners, and leather balm with UV protection.

Sneaker & Fabric Cleaning

Foaming cleansers, stain removers, and whole-shoe cleaning kits designed for mesh, knit, canvas, and synthetic uppers. Often sold as starter kits with soft brushes and microfiber cloths.

Waterproofing & Protection

Aerosol and trigger sprays, wax-based sealants, and wipe-on protectants that create a barrier against water, salt, and dirt. Emerging category includes eco-friendly, PFAS-free formulas.

4. Leading Players

The competitive landscape is split between legacy chemical companies and dedicated footwear-care specialists. The first archetype includes multinational conglomerates with broad consumer goods portfolios—companies that dominate the mass retail shelf through established distribution networks and economies of scale. Their strategy centers on brand trust, large-format packaging, and multipurpose claims (e.g., “cleaner + conditioner + waterproof”). A second archetype comprises heritage leather-care houses that have cultivated niche credibility over decades. These firms focus on premium ingredients (e.g., mink oil, Japanese waxes) and authentic craftsmanship narratives, often commanding price premiums of 2–3x over mainstream products. Their advantage lies in deep retailer relationships with luxury department stores and independent shoe repair shops. The third archetype is the direct-to-consumer disruptor, usually born from the sneaker community. These brands launch on Instagram and TikTok, leverage influencer partnerships, and use subscription models for recurring revenue. They compete on convenience (all-in-one kits, phone-based support) and aesthetic packaging. The key challenge for all players is raw material volatility—waxes, solvents, and bio-based polymers face supply disruptions and regulatory shifts, particularly in the EU under REACH and CLP regulations.

Chemical Conglomerates (Mass-Market Titans)

Leverage enormous R&D budgets and global distribution to dominate retail shelves with multipurpose products (e.g., 3-in-1 cleaner+conditioner+waterproofer). Their competitive advantage is scale and brand trust, but they often lack authenticity with sneakerhead communities.

Heritage Leather Specialists (Premium Niche)

Family-run or century-old companies that source high-quality waxes and emollients from specific regions (e.g., Norwegian cod oil, Japanese carnauba). Their edge is craftsmanship storytelling and loyalty from luxury shoe retailers; they resist price competition and maintain 50%+ gross margins.

Digital-Native Sneaker Care Brands (D2C Disruptors)

Born on social media, these brands focus on convenience, aesthetic packaging, and influencer marketing. Their advantage is real-time customer feedback loops and subscription models. A typical kit costs $30–$45 and includes a cleaner, brush, and towel, with monthly refill subscriptions.

5. Market Trends

1. ECO-FRIENDLY FORMULATIONS

Rising consumer demand and regulatory pressure (EU Green Deal, California Prop 65) are forcing manufacturers to replace petroleum-based solvents with plant-derived alternatives. Brands are launching biodegradable bottles and water-based polishes that eliminate VOCs. For example, a leading European heritage brand reformulated its entire polish line to be 95% bio-based by 2025, reducing carbon footprint by 40%. The challenge remains performance parity—natural ingredients often require longer drying times.

2. ONLINE RETAIL CHANNEL EXPANSION

E-commerce now represents over 40% of shoe care product sales in developed markets, up from 25% in 2020. Amazon, specialty footwear e-tailers, and brand-owned D2C sites are the primary growth engines. This shift enables smaller brands to gain national distribution without retailer listings, but also intensifies price competition. A North American sneaker care startup reported that 70% of its sales came through its own website and social commerce in 2024.

3. SUSTAINABLE PACKAGING INNOVATION

Single-use plastics are being phased out in favor of refillable systems, aluminum containers, and post-consumer recycled (PCR) materials. One industry leader introduced a “zero-waste shoe care” line where pouches replace rigid bottles, cutting plastic use by 80%. This trend matters because packaging constitutes 20–30% of product cost in this segment.

4. SNEAKER CULTURE MAINSTREAMING

The global resale sneaker market exceeded $20 billion in 2025, driving demand for specialized cleaning kits that can restore limited-edition pairs to mint condition. This has created a premium sub-segment with price points $25–$60 per kit, often sold in exclusive collabs with sneaker release events.

6. Regional Markets

Europe – Highest Per-Capita Spend & Regulatory Driver

With a deep leather heritage and strict environmental laws (EU Green Deal, REACH), Europe leads in premium product adoption. Brands here are forced to innovate with water-based and biodegradable formulas, making the region a benchmark for sustainable shoe care.

North America – Sneaker Culture Epicenter

The U.S. accounts for the largest share of sneaker cleaning products, driven by the resale market. Online channels dominate, and startups use TikTok to launch viral cleaning solutions. Cross-border logistics from Mexico is a key sourcing route for generic products.

Asia-Pacific – Fastest-Growing Frontier

Rapid urbanization in China, India, and Southeast Asia is expanding the middle class and formal footwear usage. Local manufacturers produce lower-cost alternatives but are increasingly adding premium lines. Japan remains a distinct market with a preference for minimalist, high-quality balms.

7. Investment Outlook

Two concrete opportunities emerge for B2B buyers in the shoe care space. First, the refillable/subscription model is underpenetrated in professional settings—shoe repair shops, hotel valets, and premium retailers need bulk refills of conditioners and cleaners. Developing institutional-grade refill pouches with EAN codes for automated reordering could secure long-term contracts. Second, the integration of smart sensors (e.g., UV dosimeters in waterproofing sprays that indicate reapplication time) is an untapped differentiation. However, a significant risk looms: regulatory crackdown on certain chemical preservatives and surfactants under the EU’s PFAS ban and similar regulations globally. Products containing perfluorinated compounds for water repellency may be phased out entirely by 2028, forcing massive reformulation costs. Buyers should prioritize suppliers that already offer PFAS-free waterproofing alternatives and have ISO 14001 certified production facilities to future-proof their sourcing.

Strategic Considerations:

- Bulk Refill Systems for Commercial Clients: Hotels, shoe repair chains, and retail valet services need cost-effective refill pouches for detergents and conditioners. B2B suppliers that offer 5-liter refills with automated replenishment APIs can secure multi-year contracts with 20–30% margin premiums.

- Smart Packaging with Reapplication Reminders: Integrating NFC tags or QR codes on waterproofing sprays that sync with a mobile app to alert users when to reapply could create a premium SKU. Early adopters could patent this utility and charge up to 2x the standard price.

- PFAS Ban Impact on Waterproofing Segment: EU’s proposed PFAS restriction (expected 2028) would eliminate most fluoropolymer-based waterproof sprays. Suppliers without ready alternatives in silicone or nano-wax will lose shelf access. B2B buyers must audit suppliers for PFAS-free options now to avoid supply disruption.

- Raw Material Price Volatility: Natural waxes (candelilla, carnauba) and surfactants have seen 15–25% price swings in 2024–2025 due to climate events and geopolitical tensions. Long-term contracts with price index clauses are essential to manage procurement costs.

Frequently Asked Questions

Make Informed Decisions in the Shoe Care Products Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-24. All market figures are estimates and may vary from actual results.