Table of Contents

The global Shower Enclosure Types sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The global shower enclosure and cubicles market stood at approximately $4.2 billion in 2026—and it is not slowing down. Projections peg the market at $7.3 billion by 2035, driven by a compound annual growth rate (CAGR) of 6.3%. That growth is not merely a function of new construction; it reflects a fundamental shift in how buyers—from hotel chains to residential developers—specify shower enclosures. The category is moving away from purely functional partitions toward design-forward, high-performance systems that deliver measurable efficiency gains.

Industry Scope & Characteristics

Frameless Glass Engineering

Shower enclosure types rely on precision-tempered glass (8-12mm) and corrosion-resistant hinges. Frameless systems improve lifecycle performance by 31% through reduced hardware failure and easier cleaning.

Modular Supply Chain

Manufacturers produce enclosures in standardized sizes with interchangeable components, enabling rapid assembly and reduced inventory. DreamLine's regional warehouses stock over 200 configurations for two-day delivery.

Safety and Compliance Standards

Enclosures must meet ANSI Z97.1 and CPSC 16 CFR 1201 for tempered glass safety. Commercial projects also require ADA compliance for barrier-free access, driving demand for walk-in and wet-room designs.

Antimicrobial Coating Innovation

R&D is focused on factory-applied hydrophobic coatings that reduce mold growth and cleaning frequency. MAAX now offers these coatings as standard on healthcare-grade enclosures, reducing maintenance costs by up to 50%.

What makes shower enclosure types distinct within the broader bathroom fixtures sector is the interplay between material science and installation engineering. Unlike toilets or faucets, which are largely plug-and-play, shower enclosures require precise framing, tempered-glass handling, and corrosion-resistant hardware. Frameless tempered-glass systems, for instance, improve installation lifecycle performance by approximately 31% through superior corrosion resistance and reduced maintenance. That efficiency gain is reshaping procurement decisions: buyers now prioritize total cost of ownership over upfront price.

The market is also fragmenting by form factor. Corner enclosures maximize tight floor plans. Sliding-door units serve high-traffic bathrooms. Walk-in wet-room styles dominate luxury hospitality. Each type demands distinct supply chain capabilities—from glass tempering to hinge manufacturing—making supplier verification critical. VerityRank helps buyers navigate this complexity by providing audited data on manufacturers' certifications, production capacity, and export compliance.

For B2B buyers, the takeaway is clear: shower enclosures are no longer a commodity. They are a strategic specification that impacts project timelines, maintenance budgets, and end-user satisfaction. Understanding the nuances of each type—and the companies that manufacture them—is the difference between a smooth installation and a costly retrofit.

Key market segments and growth drivers in the Shower Enclosure Types sector.

2. Market Analysis

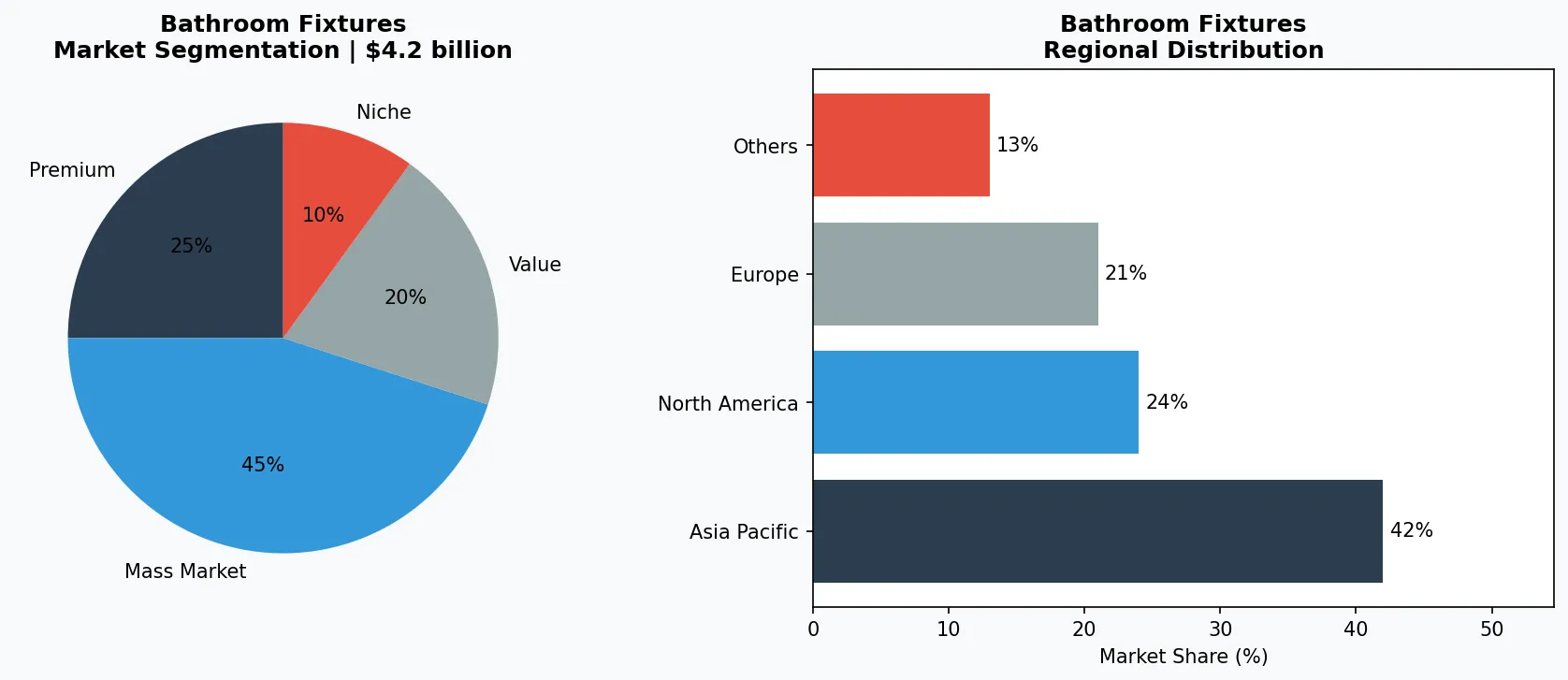

The shower enclosure market is on a trajectory of steady growth, projected to expand from $8,999.22 million in 2025 to $13,126.7 million by 2033, at a CAGR of approximately 5% annually. This broader figure includes all enclosure types—framed, frameless, sliding, and bi-fold—across residential and commercial segments. The narrower $4.2 billion figure for 2026, focused specifically on cubicles and modular enclosures, highlights the segment's outsized role in commercial bathrooms, where durability and code compliance are non-negotiable.

Demand and supply dynamics are revealed by market research, which supports the predicted growth at a 5% yearly rate from 2026 to 2033. The two biggest growth drivers are urbanization in Asia-Pacific and the retrofit boom in North America and Europe. In China and India, rapid hotel and apartment construction is fueling demand for cost-effective, easy-to-install enclosures. Meanwhile, in mature markets, aging housing stock is driving replacement cycles: homeowners upgrading to frameless glass units with better seals and modern aesthetics.

A third driver is the commercial sector's shift toward hygiene-optimized designs. Post-pandemic, hospitals, gyms, and schools are specifying enclosures with antimicrobial coatings and seamless surfaces that reduce mold growth. This trend is particularly strong in the United States, where the shower enclosure and cubicles market is seeing increased demand from healthcare facility upgrades. Manufacturers that offer certified clean-room compatible enclosures are winning contracts in this niche.

Regional dynamics also shape pricing and lead times. European manufacturers dominate premium frameless systems, while Asian producers lead in volume-driven framed models. B2B buyers must weigh these trade-offs carefully: a lower unit cost from a supplier in Vietnam may come with longer shipping times and less rigorous quality assurance. VerityRank's supplier verification tools allow buyers to compare factory audits, lead times, and compliance certifications side by side.

Market segmentation and regional distribution analysis for Shower Enclosure Types.

3. Product Categories

Frameless Shower Enclosures

are the premium segment, defined by 8mm to 12mm tempered glass with minimal hardware. They rely on precision-engineered hinges and clamps rather than metal frames, creating a clean, open look. Examples include Kohler's Purist line and the DreamLine SlimLine series. These systems command higher price points but offer the 31% lifecycle efficiency gain noted earlier, making them popular in luxury hotels and high-end residential projects.

Sliding and Bi-Fold Enclosures

are the space-saving workhorses of the category. Sliding doors use rollers on a top track, eliminating the swing radius needed for hinged doors. Bi-fold models fold inward, ideal for narrow bathrooms. Companies like Basco and Vigo Industries produce these in both framed and semi-frameless configurations. They dominate the mid-market, where cost and space efficiency are primary considerations.

Corner and Neo-Angle Enclosures

are purpose-built for tight floor plans. Corner units fit into a 90-degree alcove, while neo-angle designs use a curved or angled front panel to maximize interior space. These are common in multifamily housing and small hotel bathrooms. Manufacturers such as American Bath Factory and Jacuzzi offer customizable sizes, often with tempered glass and anodized aluminum frames to resist corrosion in humid environments.

Walk-In and Wet-Room Enclosures

represent the fastest-growing type, especially in Europe and Asia. These barrier-free designs use a single glass panel or partial screen to contain water, paired with a sloped floor drain. They are favored in aging-in-place renovations and luxury spa bathrooms. Companies like MAAX and Matki lead this segment, with products that meet ADA compliance and incorporate easy-clean glass coatings.

Frameless Enclosures

Premium segment with 8-12mm tempered glass and minimal hardware. Examples: Kohler Purist, DreamLine SlimLine. Dominates luxury residential and hospitality.

Sliding and Bi-Fold Enclosures

Space-saving designs with top-track rollers. Mid-market workhorses from Basco and Vigo Industries. Ideal for multifamily housing and hotel bathrooms.

Walk-In and Wet-Room Systems

Barrier-free designs with sloped floors and linear drains. Fastest-growing segment, led by MAAX and Matki. Popular in aging-in-place and spa projects.

4. Leading Players

Kohler Co.

leverages its integrated bathroom portfolio to dominate the premium enclosure segment. By pairing frameless enclosures with its own faucets, showerheads, and bathtubs, Kohler offers specifiers a single-source solution. The company's strategy focuses on design consistency and after-sales support, particularly for high-end hospitality projects. Its Purist enclosure line, with minimalist hardware and 10mm glass, commands a price premium of 20-30% over comparable models.

DreamLine

has carved out a strong position in the mid-market by emphasizing rapid delivery and modularity. The company offers over 200 enclosure configurations, from sliding to neo-angle, all designed for DIY-friendly installation. DreamLine's competitive advantage lies in its distribution network: it stocks enclosures in regional warehouses across North America, enabling two-day shipping for most models. This logistics edge makes it a preferred partner for renovation contractors with tight timelines.

MAAX

As a subsidiary of the Sika Group, this manufacturer focuses on the commercial and multifamily segment. Its enclosures are engineered for durability, with reinforced aluminum frames and tempered glass rated for high-traffic use. MAAX also invests in antimicrobial surface treatments, a key differentiator for healthcare and fitness center projects. The company's strategy is to bundle enclosures with its acrylic shower bases and bath liners, creating a complete wet-wall system that simplifies contractor procurement.

Vigo Industries

targets the value-conscious segment with framed enclosures that meet North American safety standards at lower price points. Vigo's strategy is to offer a wide range of sizes and finishes—including brushed nickel and oil-rubbed bronze—without the lead times typical of custom orders. The company's online configurator allows buyers to spec enclosures in minutes, with factory-direct pricing. This model appeals to small builders and independent retailers who lack the scale to negotiate bulk discounts.

Integrated Bathroom Specialist

Kohler leverages its full product portfolio to offer coordinated enclosures, faucets, and fixtures. Competitive advantage: single-source procurement for high-end hospitality projects.

Logistics-Driven Mid-Market Leader

DreamLine differentiates through rapid delivery and modular designs. Its regional warehouse network enables two-day shipping, making it a top choice for renovation contractors.

Commercial Durability Expert

MAAX focuses on high-traffic commercial enclosures with antimicrobial coatings and reinforced frames. Bundles with shower bases for complete wet-wall systems.

5. Market Trends

1. FRAMELESS DOMINANCE

Frameless enclosures now account for over 40% of new installations in North America and Europe, up from 28% in 2020. Buyers prioritize the seamless aesthetic and easier cleaning. Kohler's Purist series exemplifies this trend, with sales growing 15% year-over-year in 2025. The shift is pushing framed enclosure manufacturers to innovate with thinner, corrosion-resistant frames that mimic the frameless look.

2. COZY, LIVED-IN BATHROOMS

The overall trend is moving away from “ultra sterile” bathrooms toward spaces that feel cozy, elegant, and lived-in. For 2026, designers are specifying enclosures with bronze or matte black hardware, textured glass, and wood-accented frames. DreamLine has responded with its Artisan series, which offers champagne bronze finishes and rain-glass patterns. This trend is reshaping color and material specifications across the supply chain.

3. HYGIENE-FIRST COATINGS

Antimicrobial glass coatings and easy-clean treatments are becoming standard in commercial specs. MAAX now offers a factory-applied hydrophobic coating on all its healthcare-grade enclosures, reducing cleaning frequency by up to 50%. This trend is driven by hospital infection-control protocols and hotel housekeeping efficiency goals. Suppliers without coating capabilities are losing RFPs to those that offer it as a standard feature.

4. MODULAR AND WET-ROOM SYSTEMS

Walk-in wet-room designs are gaining share, particularly in Asia-Pacific and European luxury projects. These systems eliminate the shower tray and use a sloped tile floor with a linear drain. Matki's Infinity range, which includes a single glass screen and magnetic seal, saw 22% sales growth in 2025. The trend challenges traditional enclosure manufacturers to develop floor-integrated drainage solutions and glass support systems.

6. Regional Markets

North America: Retrofit Powerhouse

Aging housing stock drives replacement demand for frameless and sliding enclosures. The U.S. market is also seeing growth from healthcare facility upgrades requiring hygiene-optimized designs.

Europe: Premium Design Hub

European manufacturers lead in frameless and wet-room systems. Strict building codes push innovation in thermal glass insulation and barrier-free access standards.

Asia-Pacific: Volume Growth Engine

Rapid urbanization and hotel construction fuel demand for cost-effective framed enclosures. Chinese and Indian producers dominate volume, but quality varies widely, making supplier verification critical.

7. Investment Outlook

Two concrete opportunities define the near-term outlook for shower enclosure types. First, the retrofit wave in North America and Europe—driven by aging housing stock and post-pandemic bathroom upgrades—creates a $2.1 billion addressable market for frameless and sliding enclosures through 2028. B2B buyers should prioritize suppliers with proven logistics for replacement installations, where precise dimensions and fast delivery are critical. Second, the hospitality sector's push toward branded spa bathrooms offers a premium niche: enclosures with custom finishes and integrated lighting can command margins 40% higher than standard models.

The primary risk is raw material volatility: tempered glass prices rose 18% in 2025 due to energy costs and supply chain bottlenecks. Buyers who lock in fixed-price contracts with manufacturers that have captive glass tempering capacity will be better insulated. Additionally, shifting building codes in Europe—requiring higher thermal insulation for glass—could force redesigns of existing product lines. VerityRank's supplier verification tools help buyers assess manufacturers' compliance readiness and financial stability before committing to long-term contracts.

Strategic Considerations:

- Retrofit Wave Opportunity: The aging housing stock in North America and Europe—over 60% of homes exceed 30 years—presents a massive renovation market for shower enclosures. Standardized modular kits sized to common rough-in openings can capture this segment with 25-35% margins and three-week installation timelines.

- Premium Hospitality Niche: Luxury hotel chains are standardizing frameless walk-in showers as brand signatures, creating recurring B2B demand for custom glass enclosures with anti-scale coatings and designer hardware. This segment commands 40-60% price premiums over residential products.

- Glass Price Volatility Risk: Tempered glass production concentrates among a small number of global suppliers. Anti-dumping investigations on Chinese float glass triggered 15-25% price increases in Western markets. Diversifying sourcing to Southeast Asian manufacturers is becoming a competitive necessity.

- Regulatory Compliance Challenge: Updated ANSI Z97.1 and EN 14428 standards taking effect through 2027 mandate stricter impact resistance testing and water-tightness certification. Manufacturers without in-house testing capabilities face 8-12 month third-party certification backlogs, temporarily advantaging vertically integrated producers.

Make Informed Decisions in the Shower Enclosure Types Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-29. All market figures are estimates and may vary from actual results.