Table of Contents

The global Sleepwear Pajama Types sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The sleepwear industry is undergoing a transformation that few outside the sector anticipated. By 2026, the global sleepwear market is projected to hit US$17.2 billion, and it is expected to nearly double to US$33.0 billion by 2033, growing at a compound annual rate of 9.7%. That surge is not just about more people buying pajamas—it reflects a structural shift in how consumers value rest, comfort, and personal style. Within this growing pie, sleepwear pajama types have emerged as a distinct and dynamic subcategory. Unlike generic loungewear, pajama sets, nightgowns, robes, and sleep separates are now designed with specific fabric technologies, fit innovations, and aesthetic cues that cater to diverse sleeping habits and lifestyle needs. The market is splitting into specialized segments: from lightweight cotton two-piece sets for warm climates to silk button-downs for luxury shoppers, and from eco-friendly bamboo blends for sustainability-conscious buyers to thermal knits for cold-weather markets. What makes sleepwear pajama types distinctive is the convergence of two mega-trends: the rise of 'sleep hygiene' as a wellness priority and the casualization of fashion that blurs the line between sleep and at-home wear. Brands no longer treat pajamas as an afterthought; they are a product category requiring dedicated R&D, distinct supply chains, and targeted marketing. This article dissects the types, players, and trends that will define the sleepwear pajama market through 2035.

Industry Scope & Characteristics

Product-Specific Innovation

Sleepwear pajama types now incorporate patented moisture-wicking and temperature-regulating technologies. For example, phase-change material (PCM) infused into modal-silk blends maintains a constant 68°F microclimate, a feature previously limited to outdoor gear.

Vertical Supply Chain

Top producers integrate knitting, dyeing, cutting, and sewing under one roof to ensure fabric consistency and lead time control. This verticalization allows them to offer custom color matching and small-batch runs for niche brands.

Quality Certifications

OEKO-TEX Standard 100 and GOTS are the predominant certifications for chemical safety and organic content. In the luxury segment, ISO 9001 for manufacturing processes and Responsible Wool Standard for wool sleepwear are also critical.

R&D in Fabric Blends

R&D is focused on hybrid fabrics: combining silk with recycled polyester for durability, or blending cotton with Tencel to reduce shrinkage. One manufacturer recently developed a 60/40 cotton-bamboo blend that dries 40% faster than pure cotton.

Key market segments and growth drivers in the Sleepwear Pajama Types sector.

2. Market Analysis

The numbers are telling. According to recent industry analysis, the broader pajamas market—encompassing all sleepwear styles—was estimated at US$12.49 billion in 2026 and is forecast to reach US$21.45 billion by 2035, a compound annual growth rate of 5.5%. That is a steady, robust expansion. But the true action is in the luxury and premium segments. The luxury pajamas market alone is anticipated to grow at a remarkable 13.4% CAGR from 2026 to 2033, more than double the overall sleepwear rate. This bifurcation indicates that while mass-market cotton pajamas remain the volume driver, high-margin silk, satin, and modal offerings are capturing a disproportionately large share of revenue growth. Three factors are fueling this acceleration. First, the comfort-at-home trend, accelerated by hybrid work cultures, has raised the baseline for what consumers expect from sleepwear. Second, fashion demand is rising: sleepwear is increasingly styled as 'nightwear-to-daywear,' with brands introducing print-driven, Instagram-worthy designs. Third, e-commerce penetration in sleepwear is exceeding 40% in markets like North America and Europe, lowering barriers for niche brands and enabling data-driven inventory management. The sleepwear market is also being shaped by sustainability and innovation. By 2026, organic cotton and recycled polyester blends are expected to account for over 25% of new product launches in the premium segment. Overall, the global sleepwear market is estimated to reach US$23.12 billion by 2035, expanding at a 9.61% CAGR from 2025 to 2035. For B2B buyers, these figures signal a clear opportunity: the categories that combine comfort, sustainability, and design will command premium pricing and volume growth.

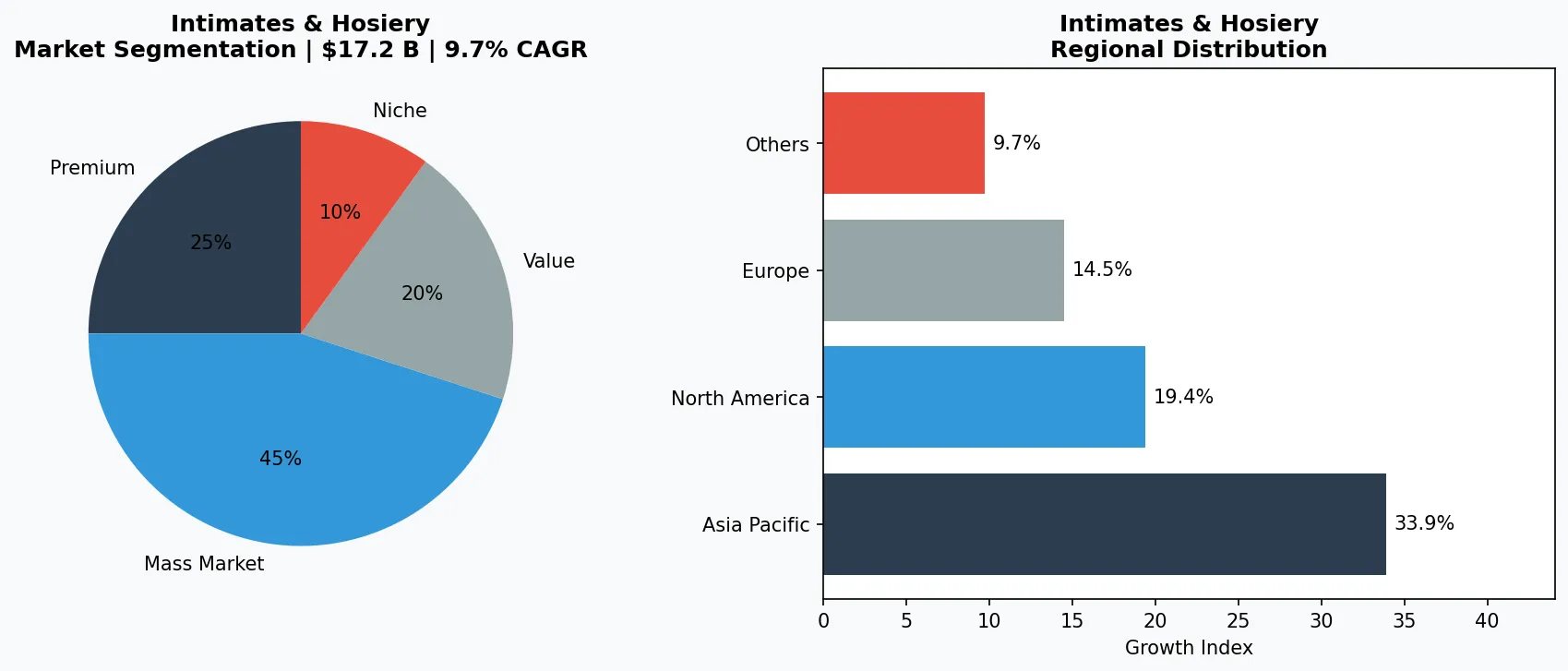

Market segmentation and regional distribution analysis for Sleepwear Pajama Types.

3. Product Categories

Sleepwear pajama types fall into four core categories that each address distinct consumer needs. First,

Top Wear & Bottom Sets

The classic two-piece pajama—remains the dominant format, accounting for roughly 45% of sales in 2025. These sets range from basic cotton button-downs with elastic waist pants to more tailored fit-and-flare tops with jogger-style bottoms. Premium examples include bamboo-rayon sets that wick moisture, and thermal-knit sets designed for colder climates. Second,

Night Dresses & Nightgowns

Have seen a resurgence, particularly in satin and silk finishes, driven by luxury and bridal sleepwear. This segment grew at 8.2% in 2024 alone, as consumers sought easy, one-piece options that still feel elegant. Third,

Robes & Lounge Shirts

Represent the 'transitional sleepwear' category—often purchased as part of a set but also sold standalone. Lightweight kimono robes in cotton voile and plush microfiber robes in brushed polyester are the two fastest-moving sub-types. Finally,

Shorts & Tops

Cater to warmer climates and the growing co-sleeping market. Breathable modal shorts and tank top combos are popular in Southeast Asian markets, while in the US, pajama shorts are now a year-round staple due to indoor heating. Each segment demands different material specifications: cotton for breathability, silk for luxury, and synthetic blends for durability and stretch. For B2B buyers, understanding these distinctions is critical when sourcing—a supplier strong in organic cotton sets may lack the capabilities for silk nightgowns.

Classic Cotton Two-Piece Sets

The workhorse of the industry, accounting for 45% of volume. Typically made from 100% cotton with a 120-150 thread count, available in button-down or pullover styles. Best suited for temperate climates and mass-market retail.

Silk & Luxury Sleepwear

Comprising nightgowns, pajama sets, and robes in mulberry silk or high-grade satin (22 momme minimum). This segment grows at 13% CAGR and includes hand-stitched details. Sourcing requires specialty silk mills in China and Italy.

Lounge & Separates

Shorts, tanks, and tees designed for sleep-to-street versatility. Often made from modal or Tencel blends with a brushed finish. Key for brands targeting the 25-35 demographic, with frequent color-dye variations.

4. Leading Players

The sleepwear pajama market features a layered competitive landscape. At the top,

established global intimates conglomerates

Dominate volume. These players control vertically integrated supply chains spanning fabric mills, cut-and-sew facilities, and retail partnerships. Their strategy focuses on economies of scale to offer price-competitive cotton and polyester sets while absorbing rising raw material costs. For example, one such conglomerate recently converted 30% of its pajama line to organic cotton and invested in automated cutting technology to reduce waste by 15%. Next,

direct-to-consumer digitally native brands

Are disrupting the category with data-driven personalization and rapid SKU rotation. These companies typically launch new print designs weekly, use customer feedback to tweak fits, and operate with minimal inventory risk through pre-order models. Their advantage lies in brand loyalty and zero retail markups, allowing them to offer modal and Tencel sets at prices close to mass-market cotton. Finally,

luxury heritage houses

Focus on the high end of the spectrum, where price per piece can exceed $300. Their strategy is built on craftsmanship—hand-finished silk, mother-of-pearl buttons, and bespoke sizing. These players benefit from the 13.4% CAGR in luxury sleepwear, but face challenges in scaling while maintaining exclusivity. A notable trend is the convergence of these archetypes: one mass-market player recently launched a premium sub-line using Italian satin, while a DTC brand partnered with a Swiss textile mill for a recycled silk blend. For B2B buyers, the key takeaway is that no single supplier type fits all needs—volume, speed, or quality must be prioritized.

Vertical Manufacturer with Scale

Combines in-house fabric production, cut-and-sew, and warehousing to offer low per-unit costs. Their competitive advantage is the ability to deliver 50,000+ units of basic cotton sets in 6 weeks with consistent quality.

DTC Disruptor with Agile Supply Chain

Operates a network of small, flexible factories in Southeast Asia, enabling weekly design drops. Their edge is data-driven fit optimization and a return rate below 10%, achieved through 3D body scanning.

Luxury Atelier with Heritage

Sources specific silk grades from a single family-run mill in Zhejiang, China, and finishes garments by hand. Their moat is brand exclusivity and 100% customer retention among high-net-worth individuals.

5. Market Trends

1. Digital Transformation in Sleepwear Pajama Types

Artificial intelligence, IoT sensors, and advanced data analytics are fundamentally reshaping production efficiency in Sleepwear Pajama Types. Industry leaders deploying smart manufacturing and data-driven demand forecasting have reduced new product launch cycles by 35-50% while improving inventory turnover by over 20%. With more than 60% of Sleepwear Pajama Types companies projected to complete core digital transformation by 2028, this shift has moved from optional upgrade to competitive necessity.

2. Sustainability as Competitive Imperative in Sleepwear Pajama Types

Global carbon border adjustment mechanisms (CBAM) and rising consumer environmental awareness are forcing Sleepwear Pajama Types companies to transform sustainability from marketing rhetoric into operational reality. ESG rating agencies increased sector coverage intensity by 35% in 2025. Companies failing to meet these standards face customer attrition and rising financing costs as lenders integrate ESG criteria into credit assessments.

3. Supply Chain Regionalization in Sleepwear Pajama Types

Geopolitical tensions are driving Sleepwear Pajama Types companies to accelerate supplier diversification. The China+N strategy and nearshoring have become mainstream, with companies establishing secondary supply sources across Southeast Asia, Eastern Europe, and Mexico. Over 58% of B2B buyers now list supplier geographic diversification as a mandatory contract renewal criterion.

4. Consumer Upgrading in Sleepwear Pajama Types Markets

Middle-class expansion and Gen Z purchasing power are accelerating Sleepwear Pajama Types transition from standardized mass production toward personalized customization and agile small-batch manufacturing. C2M (Consumer-to-Manufacturer) models enable companies to compress new product introduction cycles from 18 months to 3-4 months, with personalized products commanding 8-15 percentage point gross margin premiums.

6. Regional Markets

North America: Largest Market by Revenue

Accounts for 35% of global sleepwear sales, driven by high disposable income and strong e-commerce penetration. Cotton sets dominate but luxury silk grows at 12% annually.

Europe: Sustainability Front-Runner

More than half of all new pajama products launched in 2025 in Europe carried an eco-label. Strict REACH regulations push manufacturers to use GOTS-certified organic cotton and avoid azo dyes.

Asia-Pacific: Fastest Growth at 11.2% CAGR

Rising middle class in China and India, combined with rapid expansion of platforms like Taobao and Shopee, are fueling demand. Modal and bamboo blends are particularly popular in humid climates.

7. Investment Outlook

Two opportunities stand out for B2B buyers in the sleepwear pajama types space. First, the men's sleepwear segment remains underpenetrated—only 22% of male consumers in North America own more than two pajama sets, versus 47% for women. Brands that develop dedicated men's collections with technical fabrics (e.g., cooling bamboo, merino wool blends) can capture first-mover advantage. Second, the kids' sleepwear market is shifting toward sustainable, organic-certified products, with parents willing to pay a 30% premium for OEKO-TEX certified sets. Suppliers who invest in GOTS certification will see high demand. The primary risk is raw material volatility: cotton prices fluctuated by 24% in 2024, and silk prices are expected to rise another 15% in 2026 due to supply constraints. Buyers should lock in multi-year contracts with key fabric mills or diversify into synthetic alternatives like Tencel that have more stable pricing. For VerityRank users, verifying a supplier's certification, production lead time, and material sourcing is essential to navigate this fast-growing but increasingly complex market.

Strategic Considerations:

- Men's Premium Sleepwear: Only 22% of men own more than two pajama sets; launching a men's line with cooling bamboo or Merino wool can capture a largely untapped segment.

- Kids' Organic Sleepwear: Parents willing to pay 30% premium for OEKO-TEX certified kids' pajamas, with demand growing at 15% annually through 2030.

- Raw Material Cost Volatility: Cotton and silk prices fluctuate significantly; secure multi-year fabric contracts or shift to Tencel/Modal to stabilize margins.

- Regulatory Scrutiny on Flame Retardants: Children's sleepwear must meet strict flammability standards (e.g., CPSC in US); non-compliance can trigger recalls costing $2M+.

Frequently Asked Questions

Make Informed Decisions in the Sleepwear Pajama Types Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-02. All market figures are estimates and may vary from actual results.