Table of Contents

The global Smart Air Purifier Control sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2035, the smart air purifier market is projected to reach USD 23.41 billion, growing at a CAGR of 11.02%—but the real revolution lies not in filters, but in control. Smart air purifier control refers to the integration of connected sensors, machine learning algorithms, and voice or app-based interfaces that transform a passive appliance into an autonomous environmental manager. Unlike traditional air purifiers, these devices continuously monitor particulate matter, volatile organic compounds, and humidity, adjusting fan speed and purification intensity without human intervention. The year 2025 already saw the broader air purifier industry hit USD 18.09 billion, with the smart segment expanding at a faster clip of 14.18% CAGR toward USD 6.3 billion by 2031. This growth is fueled by consumer demand for real-time air quality data and seamless integration with smart home ecosystems. For B2B buyers, the shift means sourcing not just hardware but reliable connectivity modules, firmware stacks, and cloud platforms that ensure consistent performance across different regulatory markets.

Industry Scope & Characteristics

Multi‑Sensor Fusion Hardware

Smart air purifier control relies on arrays of optical particle counters, metal‑oxide gas sensors, and humidity detectors. Products must calibrate cross‑sensitivity between VOCs and PM2.5 for accurate auto‑mode decisions.

Supply Chain Specialization

Control modules often source MEMS sensors from specialized foundries in Germany or Japan, while Wi‑Fi chips come from Taiwanese semiconductor fabs. Lead times for certified sensor modules can exceed 16 weeks.

Certification Complexity

Smart purifiers must pass FCC/CE radio emissions, UL 867 safety, and CARB ozone limits. Control software additionally requires IEC 62368‑1 for cybersecurity and FDA clearance for medical‑grade air claims.

Edge AI & Firmware OTA

R&D focus is shifting to on‑device inferencing for fan speed prediction. Companies now ship units with secure enclaves for OTA updates, enabling post‑sale feature upgrades without hardware revision.

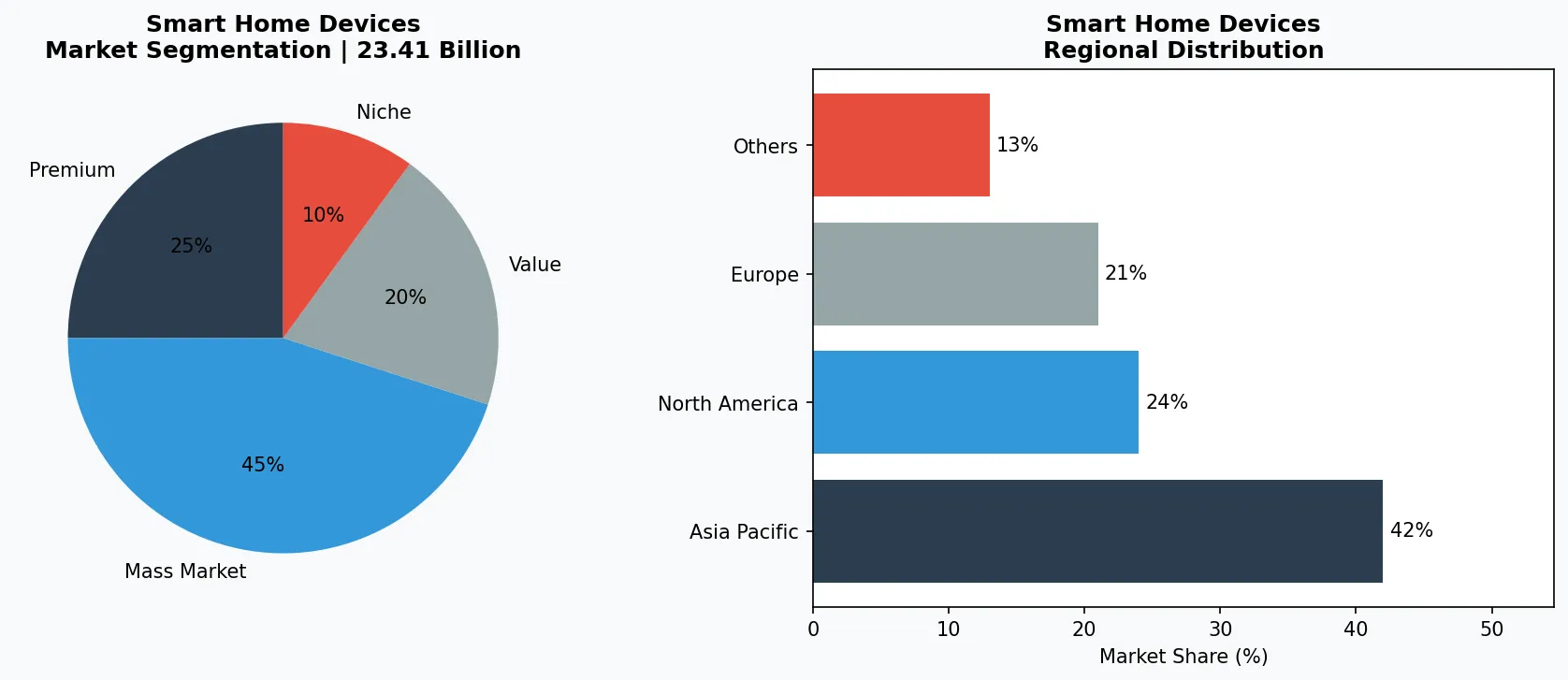

Key market segments and growth drivers in the Smart Air Purifier Control sector.

2. Market Analysis

The global smart air purifier market is riding a powerful wave of technological convergence. In 2025, the overall air purifier market was valued at approximately USD 18.09 billion, with projections to reach USD 30.08 billion by 2033 at a CAGR of 6.4%. The smart subset, however, is accelerating much faster: a separate forecast pegs the smart air purifier market at USD 6.3 billion by 2031, expanding at a CAGR of 14.18%. Three primary drivers are pushing this divergence. First, the integration of advanced multi‑sensor arrays that detect PM1.0, PM2.5, PM10, CO2, TVOCs, and humidity in real time, enabling precise control. Second, tightening indoor air quality regulations, especially in commercial buildings and healthcare facilities, are mandating automated ventilation and purification. Third, the proliferation of smart home hubs (smart speakers, thermostats, locks) has created an ecosystem where users expect all devices to respond to voice commands or geofencing triggers. Germany exemplifies the regional variance: its smart air purifier market is forecast to grow at an 8.2% CAGR from 2026 to 2033, reflecting stricter EU air quality directives and higher adoption of building automation systems.

Market segmentation and regional distribution analysis for Smart Air Purifier Control.

3. Product Categories

The smart air purifier control landscape can be segmented into three product categories. First, app‑controlled purifiers with multi‑modal sensors form the baseline. These devices stream live air quality metrics to a smartphone app and allow manual override of fan speeds, timers, and modes. Examples include models with Wi‑Fi, Bluetooth, and Zigbee connectivity that display PM2.5 readings and filter life. Second, voice‑integrated purifiers that work with Amazon Alexa, Google Assistant, and Apple HomeKit are gaining traction. Users can say 'set the purifier to auto mode' or 'increase fan speed' without touching a button. The control logic here is embedded in cloud‑based skills, requiring robust API partnerships. Third, autonomous zone‑based purification systems use multiple indoor sensors and machine learning to predict pollution spikes. For instance, a purifier in a kitchen may detect cooking fumes and automatically ramp up extraction, then revert to silent mode when air clears. Some advanced units incorporate HVAC integration, allowing the purifier to communicate with a smart thermostat to coordinate air circulation and filtration across multiple rooms. These products require rigorous testing for latency, sensor accuracy, and interoperability with different smart home protocols.

App‑Controlled Multi‑Sensor Purifiers

Baseline smart products with Wi‑Fi, Bluetooth, and Zigbee. They display real‑time PM2.5, CO2, and temperature via app, and allow manual override of fan speeds. Typical CADR range: 200–400 CFM.

Voice‑Integrated Autonomous Units

Embedded microphones and ML processors for hands‑free control via Alexa, Google Assistant, or Siri. Auto‑mode adjusts fan based on indoor/outdoor pollution differentials. Must pass voice‑activation latency <2 seconds.

Zone‑Based HVAC‑Integrated Systems

Multiple units communicate via mesh network to create purification zones. They interface with smart thermostats and duct sensors to coordinate air exchange. Used in open‑plan offices and multi‑room residential setups.

4. Leading Players

Competitive dynamics in smart air purifier control are shaped by three distinct strategic archetypes. The first archetype, Sensor Integration Pioneers, focuses on proprietary multi‑spectral sensor fusion. These companies invest heavily in R&D to reduce cross‑sensitivity between gas sensors and particulates, achieving detection thresholds below 1 µg/m³. Their competitive advantage lies in providing raw data accuracy that third‑party calibration labs certify. The second archetype, Ecosystem Enablers, builds open platforms that allow the purifier to act as a central node in larger building management systems. They offer APIs and SDKs for custom integration with HVAC controllers, occupancy sensors, and even wearable health monitors. Their value proposition is interoperability: a single SDK can connect a purifier to hundreds of smart home brands. The third archetype, Data‑Driven Service Providers, monetizes control data beyond the device. They offer subscription services that include predictive filter replacement, personalized air quality reports, and insurance discounts for maintaining healthy indoor air. Each archetype targets different B2B customer segments—from residential OEMs to commercial facility managers—and faces distinct certification barriers (e.g., ENERGY STAR, CARB, CE, FCC) that vary by region. Suppliers verified on VerityRank often demonstrate strength in one of these three strategies, making archetype identification a critical sourcing criterion.

Sensor Fusion Specialists

They own proprietary calibration algorithms for multi‑gas and particulate sensors, achieving accuracy within ±5% of reference monitors. Their advantage is reducing false positives that waste fan energy.

Ecosystem Orchestrators

They provide SDKs and cloud APIs that let any smart purifier talk to over 200 smart home platforms. Their control module is the middleware that handles protocol translation (Matter, Zigbee, Wi‑Fi).

Data Monetization Leaders

They offer predictive filter replacement subscriptions and air quality insurance discounts. Their control logic tracks usage patterns and sends pre‑emptive alerts to avoid peak pollution events.

5. Market Trends

1. Technology-Driven Transformation

Artificial intelligence, IoT sensors, and advanced data analytics are fundamentally reshaping production efficiency, quality control, and demand forecasting in Smart Air Purifier Control. Leading manufacturers deploying smart sensors and automated production lines have reduced operational costs by 12-18% while maintaining defect rates below 0.5%. With over 60% of industry participants projected to complete initial digital transformation by 2028, this shift represents a competitive imperative rather than an option.

2. Sustainability and Regulatory Compliance

Global carbon border adjustment mechanisms (CBAM) and rising consumer environmental awareness are forcing Smart Air Purifier Control companies to elevate sustainability from marketing rhetoric to core business strategy. Carbon footprint tracking, recycled material substitution, and zero-waste production systems have become baseline requirements for winning large-scale B2B contracts. ESG rating agencies increased their sector coverage intensity by 35% year-over-year in 2025.

3. Supply Chain Resilience and Regionalization

Geopolitical tensions and post-pandemic supply chain disruption lessons are driving Smart Air Purifier Control companies to accelerate supply base diversification. The China+N strategy and nearshoring are becoming mainstream, with companies establishing secondary supply sources in Southeast Asia, Eastern Europe, and Mexico to reduce single-source dependency from 75% to below 40%. This structural shift significantly enhances risk resilience and buyer confidence.

4. Consumer Demand Upgrading and Personalization

Middle-class expansion and Gen Z purchasing power are driving Smart Air Purifier Control from standardized mass production toward personalized customization and small-batch agile manufacturing. C2M (Consumer-to-Manufacturer) models and flexible production lines enable companies to compress new product launch cycles from 18 months to 3-4 months. This trend is particularly pronounced in premium market segments, where personalized products typically command gross margins 8-15 percentage points above standard offerings.

6. Regional Markets

Germany: Stricter EU Norms Drive Automation

Growing at 8.2% CAGR (2026‑2033), Germany demands purifiers with auto‑mode that meets EN 16798‑3 for building ventilation. Local buyers require bilingual voice control (German/English) and TÜV certification for sensor accuracy.

North America: Voice Integration Dominance

Over 70% of smart purifiers sold in the US are compatible with Amazon Alexa or Google Assistant. Control latency and interoperability with existing smart thermostats (e.g., Nest) are key purchase criteria for hospitality buyers.

Asia Pacific: Cost‑Sensitive IoT Mass Market

High volume but low ASP drives demand for compact control modules with integrated Wi‑Fi/Bluetooth SOCs. Chinese manufacturers prioritize high‑sensitivity PM2.5 sensors and WeChat mini‑program integration for fast app adoption.

7. Investment Outlook

Two opportunities stand out for smart air purifier control in 2026‑2035. First, the convergence with smart thermostats and HRV systems opens a new revenue stream for control‑as‑a‑service: building owners pay a monthly fee for automated air quality management that reduces HVAC energy consumption by up to 20%. Second, the integration of biometric feedback (heart rate, sleep quality) from wearables can drive predictive purification before users even sense poor air. One concrete risk: cybersecurity vulnerabilities in cloud‑connected purifiers could lead to remote manipulation of fan speeds or sensor data spoofing, potentially triggering regulatory fines under emerging IoT security laws (EU Cyber Resilience Act). B2B buyers must prioritize suppliers with proven firmware encryption and over‑the‑air update capabilities. VerityRank’s verification process now includes a security readiness assessment for smart home control modules.

Strategic Considerations:

- HVAC‑Purifier Convergence as a Service: Offer control‑as‑a‑service for commercial buildings: automated air management that cuts HVAC energy use by 20% while maintaining IAQ compliance.

- Biometric‑Triggered Purification: Integrate wearable health data (heart rate, sleep stage) to pre‑activate purifier before occupant enters a zone, boosting premium product margins.

- Cybersecurity Vulnerabilities in Cloud Control: Remote exploitation of cloud APIs could falsify sensor readings or disable purification; upcoming EU Cyber Resilience Act may require mandatory security certifications.

- Supply Chain Bottlenecks for MEMS Sensors: German‑made optical particle counters have 16‑week lead times; diversifying to Taiwanese or Korean sensor suppliers may reduce cost but risks calibration drift.

Frequently Asked Questions

Make Informed Decisions in the Smart Air Purifier Control Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-09. All market figures are estimates and may vary from actual results.