Table of Contents

The global Smart Bed Systems sector serves consumers worldwide with diverse solutions.

1. Industry Overview

A $2.91 billion market in 2025 is rewriting how humans interact with their bedrooms. Smart bed systems—beds integrated with sensors, actuators, and connectivity features—have evolved from novelty gadgets into serious sleep optimization tools valued by consumers and healthcare providers alike. Unlike traditional bedroom furniture, these systems actively monitor vital signs, adjust firmness in real-time, and sync with broader home automation ecosystems.

Industry Scope & Characteristics

Integrated Sensor Technology

Smart bed systems embed biometric sensors directly into sleep surfaces, measuring heart rate, breathing patterns, and movement without wearable devices. The Sleep Number 360 bed uses pneumatic sensors to detect呼吸 rate and body movement across 16 measurement points.

Specialized Manufacturing Supply Chain

Smart bed production requires assembly combining traditional mattress manufacturing with electronics integration. Components including sensors, motors, control modules, and connectivity chips must be sourced from distinct supplier categories not typically serving conventional furniture manufacturers.

Medical Device Compliance Requirements

Beds making health claims—particularly those monitoring heart rate or detecting sleep apnea indicators—may require FDA registration or medical device compliance. UL electrical safety certification and FCC electromagnetic emissions compliance represent minimum standards for North American market access.

AI-Powered Sleep Optimization

R&D investment centers on machine learning algorithms that analyze multi-month sleep data to generate personalized recommendations. Eight Sleep's latest Pod generation reportedly processes over 100 data points per sleep session to optimize temperature and firmness adjustments automatically.

The distinction between smart beds and conventional mattresses represents a fundamental shift in furniture's role. A smart bed system does not merely provide a surface to sleep on; it collects data, responds to body position, and generates insights that can improve sleep quality over time. This data-driven approach explains why hospitals, wellness clinics, and premium residential markets are all increasing procurement of these systems.

Technology integration in bedroom furniture has accelerated dramatically since 2022. What once required separate devices—sleep trackers, white noise machines, temperature controllers—now embeds directly into the sleep surface itself. Manufacturers report that consumers increasingly view smart beds as health investment rather than furniture purchase, a perception shift that commands premium pricing and drives category expansion.

Key market segments and growth drivers in the Smart Bed Systems sector.

2. Market Analysis

The smart bed market is projected to grow from $2.91 billion in 2025 to $5.41 billion by 2033, representing a compound annual growth rate of 6.3% through 2033. This trajectory mirrors broader smart home adoption, with bedroom technology following kitchen and living room automation into mainstream households. Market analysts attribute growth to three primary drivers: aging populations prioritizing sleep health, corporate wellness programs demanding employee sleep tracking data, and direct-to-consumer brands cutting traditional retail margins.

Regional dynamics reveal North America maintaining leadership through 2026, driven by high consumer awareness and established distribution through specialty mattress retailers. However, Asia-Pacific is emerging as the fastest-growing region, with Chinese and Japanese manufacturers rapidly scaling production of mid-tier smart beds targeting mass market adoption. European growth remains steady, supported by stringent energy efficiency regulations that favor smart thermostats integrated into bed heating systems.

The specialty mattress retail channel—including brands like Sleep Number and Tempur-Pedic—remains critical for premium smart bed sales, while direct-to-consumer manufacturers capture price-sensitive segments. This dual-channel structure indicates market maturation, with both luxury and accessible price points expanding simultaneously.

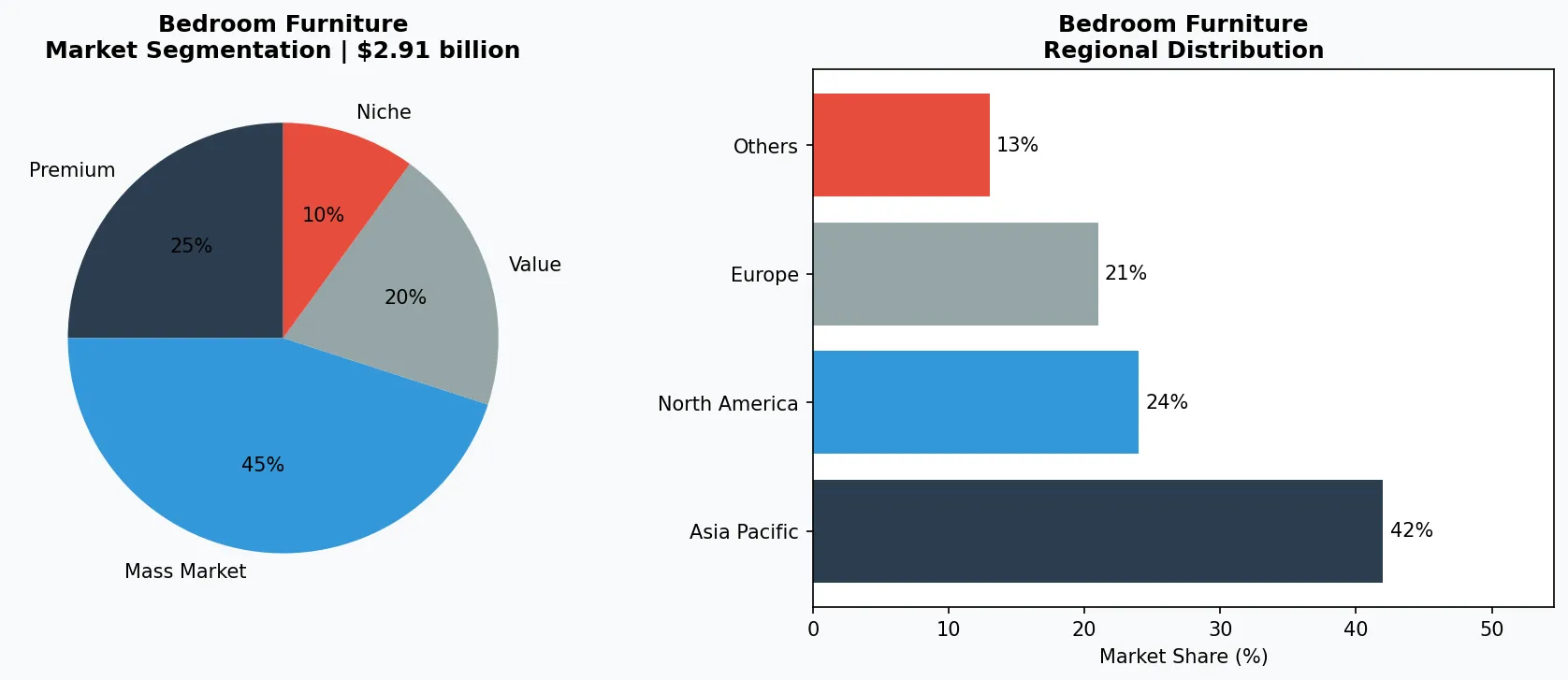

Market segmentation and regional distribution analysis for Smart Bed Systems.

3. Product Categories

Adjustable Firmness Mattresses represent the largest product category within smart bed systems. These beds use air chambers or motorized coils to allow users to customize firmness levels by zone—firmer under the lower back, softer under the shoulders. Leading models feature memory presets for different users and automatic adjustment based on detected sleep positions. Prices range from $1,500 for basic models to $5,000+ for full-body smart systems.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Sleep Tracking Integration Beds embed biometric sensors directly into the mattress surface, measuring heart rate, respiratory rate, and movement patterns throughout the night. Unlike wearable sleep trackers, these systems require no device to wear or charge. Data syncs to smartphone applications, generating nightly sleep scores and trend analysis. Some models integrate with smart home systems to adjust room lighting or temperature based on detected sleep stages.

Climate-Controlled Sleep Surfaces address temperature regulation through built-in heating and cooling channels. Dual-zone systems allow couples to maintain separate temperature preferences without compromising the shared mattress surface. Advanced models use predictive algorithms to warm the bed before the owner's typical bedtime and gradually cool as the night progresses. Power consumption remains a development focus, with manufacturers targeting 50% energy reduction compared to 2023 models.

Integrated Sleep Environment Systems represent the most comprehensive category, combining firmness adjustment, biometric monitoring, climate control, and white noise generation in unified platforms. These systems often include voice assistants, sunrise simulation lighting, and smart alarm features that wake users during optimal sleep phases.

4. Leading Players

Tempur-Pedic has positioned itself as the premium segment leader through its TEMPUR-Adapt series, which combines proprietary memory foam formulations with embedded sensors tracking sleep metrics. The company's strategy emphasizes material science credibility—leveraging decades of aerospace foam research—to justify premium pricing. Tempur-Pedic distributes through both its own retail locations and authorized dealer networks, maintaining price integrity that lesser brands cannot match.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the bedroom furniture space.

Sleep Number Corporation dominates the adjustable air bed segment with its 360 smart bed line, which has shipped over 100,000 units since 2022. The company's direct-to-consumer model, combined with its零售 partnerships, creates omnichannel reach that pure-play manufacturers lack. Sleep Number's proprietary SleepIQ technology platform generates proprietary data on aggregate sleep patterns across its user base—a significant competitive moat for future product development.

Eight Sleep has disrupted traditional market entry by positioning its products as technology platforms rather than furniture. The company's Pod series integrates all major smart bed features—adjustable firmness, temperature control, sleep tracking—in monthly subscription bundles that lower upfront costs while creating recurring revenue. This model appeals to younger consumers resistant to large furniture purchases and generates lifetime customer value exceeding single-transaction competitors.

Traditional furniture manufacturers including Ashley Furniture and IKEA have entered adjacent categories through partnerships with sleep tech providers. Rather than developing proprietary systems, these companies integrate third-party smart mattress components into conventional bed frames, creating hybrid products that appeal to existing customer bases unfamiliar with dedicated sleep technology brands.

5. Market Trends

1. BIOMETRIC MONITORING EXPANSION

Sleep tracking has evolved beyond basic movement detection to continuous cardiovascular and respiratory monitoring. Smart beds now detect irregular heart rhythms, breathing disruptions, and temperature fluctuations that may indicate emerging health issues. Major manufacturers report that medical-grade monitoring accuracy has improved 40% since 2022, driven by advances in pressure-sensitive sensors and machine learning algorithms. Why it matters: Insurers and employers are beginning to subsidize smart bed purchases for high-risk employees, creating new B2B revenue channels beyond consumer retail. Mayo Clinic's recent partnership with a leading smart bed manufacturer demonstrates clinical validation of home sleep monitoring data.

2. AI-DRIVEN SLEEP OPTIMIZATION

Machine learning algorithms now analyze months of sleep data to generate personalized recommendations and automatically adjust bed settings for optimal rest. These systems learn user patterns—preferred temperatures, ideal firmness levels, optimal wake times—and proactively configure the sleep environment. Why it matters: First-generation smart beds required manual adjustment; AI-driven systems remove user friction, making advanced features accessible to non-technical consumers. Select Comfort's latest platform claims 23% improvement in user sleep scores through automated optimization versus manual configuration.

3. SUSTAINABILITY INTEGRATION

Manufacturers are addressing environmental concerns through recyclable materials, extended warranties reducing landfill waste, and energy-efficient climate control systems. Some brands now offer mattress recycling programs when upgrading to newer models. Why it matters: Conscious consumerism is influencing premium furniture purchases, with surveys indicating 67% of smart bed shoppers consider manufacturer sustainability practices. The trend pressures both established brands and new entrants to demonstrate environmental responsibility beyond marketing claims.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two concrete opportunities define the near-term outlook for smart bed systems. First, corporate wellness programs represent an underserved B2B market where employers increasingly recognize sleep quality as productivity driver. Manufacturers developing enterprise sales channels and volume pricing structures can capture contracts with major employers seeking employee health improvements. Second, the aging population creates sustained demand for beds with health monitoring features—particularly systems detecting fall risk indicators and sleep apnea symptoms. Manufacturers combining medical monitoring accuracy with consumer-friendly interfaces will capture market share in this high-growth demographic.

One significant risk demands attention: data privacy concerns may suppress adoption among privacy-conscious consumers. Smart beds collect intimate health data continuously, creating vulnerability to breaches and potential regulatory scrutiny as governments expand health data protection requirements. Manufacturers lacking robust security architectures and transparent data policies risk both legal liability and consumer backlash that could damage category reputation. Companies must invest in security infrastructure proportional to the sensitivity of data collected—failure to do so threatens both individual brands and the broader smart bed category.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Smart Bed Systems Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-09. All market figures are estimates and may vary from actual results.