Table of Contents

The global Smart Door Lock Brands sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2026, the global smart door lock market is projected to reach $4.22 billion—but that’s just the beginning. With forecasts ranging from $7.41 billion by 2033 to $17.75 billion by 2034, the segment is expanding at a compound annual growth rate as high as 19.7%. This explosive growth reflects a fundamental shift in how homeowners and commercial property managers think about access control.

Industry Scope & Characteristics

Form Factor Diversity

Smart door locks come in deadbolt, lever, mortise, and padlock variants. Deadbolts dominate residential (39% share in 2026), while lever handle locks are preferred in commercial settings for ADA compliance.

Protocol Compatibility as a Differentiator

Z-Wave, Zigbee, Wi-Fi, Bluetooth, and Matter protocols require manufacturers to maintain multiple SKUs or universal firmware. Brands like Yale offer cross-platform compatibility to reduce channel complexity.

Security Certifications Matter

Top smart locks carry ANSI/BHMA Grade 1 or Grade 2 ratings for physical strength, plus UL 2900 cybersecurity certification. These standards are critical for commercial procurement and insurance compliance.

Edge AI for Predictive Maintenance

Leading brands embed machine learning to monitor battery degradation, latch alignment, and unlock frequency. Schlage’s latest firmware predicts battery failure 30 days in advance, alerting users via app.

Smart door locks are not merely digitized versions of traditional deadbolts; they are networked devices that integrate with broader smart home ecosystems, from voice assistants to security cameras. Unlike standard electronic locks, today’s smart locks offer multiple access mechanisms—keypad, smartphone app, fingerprint, and even voice commands—while providing real-time remote monitoring and guest access management. This convergence of convenience, security, and connectivity sets smart door locks apart as a gateway product in the smart home landscape.

The market’s acceleration is driven by three forces: declining component costs, rising security consciousness among consumers, and the growing ubiquity of home automation platforms. In North America alone, the smart door lock segment is expected to grow at a CAGR of 10.4% through the forecast period. The residential sector leads adoption, but commercial applications—hotels, offices, shared workspaces—are rapidly catching up, pushing product diversity beyond simple deadbolts into lever handles, mortise locks, and padlocks. Deadbolts alone are projected to hold a 39% share in 2026, underscoring their dominance as the preferred form factor.

Industry players are racing to differentiate through design, protocol support, and integration depth. The stakes are high: a smart lock is often the first physical touchpoint of a connected home, and brand loyalty formed here can extend to other smart devices. VerityRank’s analysis reveals that buyers increasingly prioritize cybersecurity certifications, ease of installation, and compatibility with Matter, the emerging interoperability standard. The brands that deliver on these fronts will capture the lion’s share of a market that could surpass $12 billion within a decade.

Key market segments and growth drivers in the Smart Door Lock Brands sector.

2. Market Analysis

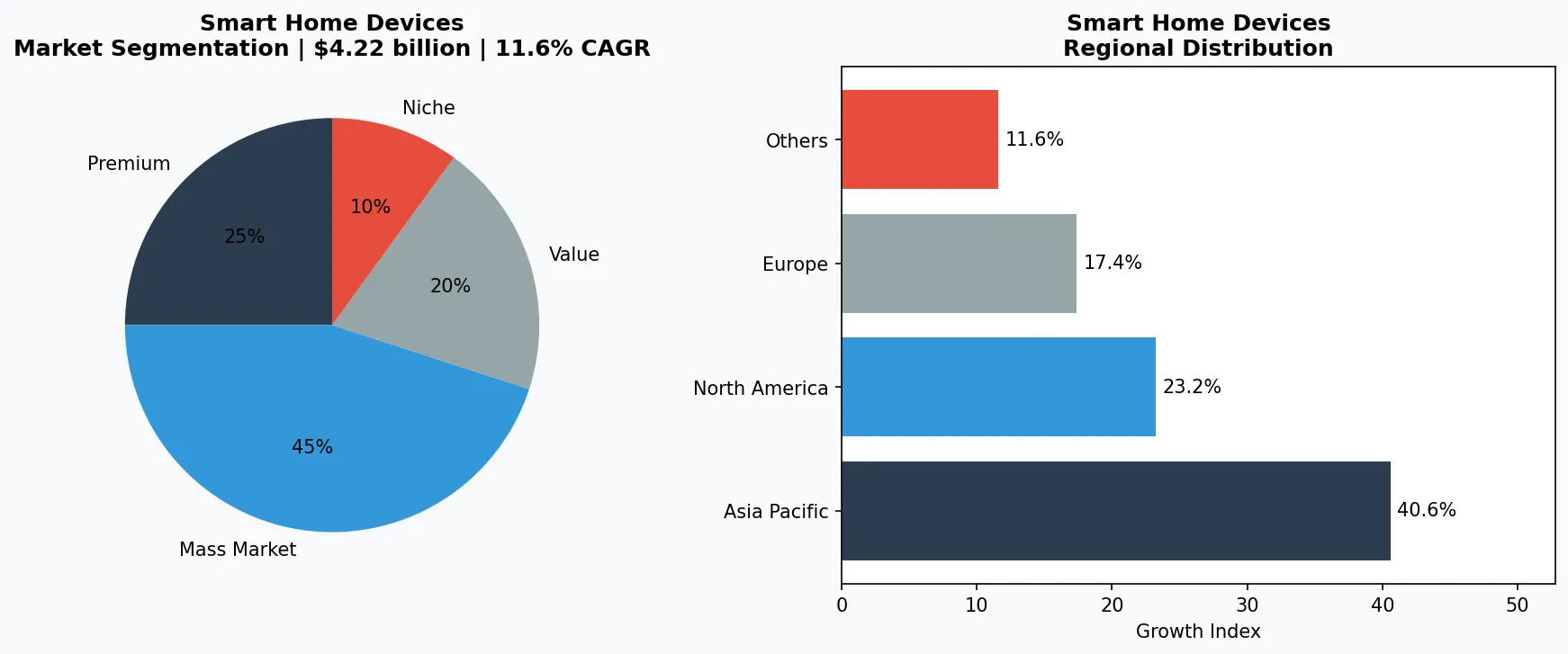

The smart door lock market is experiencing a sharp upward trajectory, with multiple reputable studies converging on strong double-digit growth. One projection values the market at $4.22 billion in 2026, climbing to $17.75 billion by 2034—a CAGR of 19.70%. Another analysis estimates $3.29 billion in 2026 surging to $7.41 billion by 2033 (CAGR 12.3%), while a third source pegs 2026 at $4.2 billion and forecasts $12.4 billion by 2033 (CAGR 16.7%). The variance in absolute numbers reflects different scopes and methodologies, but the consensus is clear: this is one of the fastest-growing segments in smart home technology.

Growth drivers are concentrated in three areas. First, residential adoption is accelerating as average selling prices fall below $200 for feature-rich models. In 2025, smart lock penetration in U.S. households is estimated to surpass 20%, up from under 10% in 2020. Second, the commercial sector is embracing smart locks for cost savings and operational efficiency. A single property manager can now remotely grant time-limited access to 50 units, eliminating physical key management. Third, the rapid expansion of smart home platforms—Amazon Alexa, Google Home, Apple HomeKit—has created a virtuous cycle: more smart lock compatibility drives more purchases, which in turn encourages manufacturers to deepen integration.

Regionally, North America holds the largest revenue share, buoyed by high consumer awareness and mature home automation infrastructure. Europe follows closely, with strong demand in Germany and the UK driven by strict building security norms. Asia Pacific is the fastest-growing region, fueled by urbanization and the proliferation of smartphone-based access in markets like China, Japan, and South Korea. Latin America and the Middle East are emerging markets, often leapfrogging to app-based locks. The deadbolt product type is expected to command a 39% share in 2026, but lever/knob locks are gaining ground in commercial settings where ADA compliance and ease of use matter.

Current events, including rising concerns about package theft and short-term rental management, are further boosting demand. The impact of artificial intelligence is becoming tangible: AI-powered facial recognition and behavioral analysis are being integrated into high-end models, while machine learning algorithms optimize battery life and detect tampering attempts. These innovations are not just features—they are creating new sub-categories and price tiers that expand the total addressable market.

Market segmentation and regional distribution analysis for Smart Door Lock Brands.

3. Product Categories

The smart door lock market can be organized into four principal product types, each serving distinct use cases and installation requirements.

Deadbolt Locks

Are the most common, projected to represent 39% of the market in 2026. They replace traditional single-cylinder deadbolts and offer keyless entry via keypad, fingerprint, or app. Leading examples include the Schlage Encode Plus (which supports Apple HomeKey) and the August Wi-Fi Smart Lock (designed to retrofit existing deadbolts). Deadbolts dominate residential applications because they fit standard door preparations and provide high security.

Lever Handle Locks

Are popular in commercial and multi-unit residential buildings where lever handles are required for ADA compliance. These locks typically integrate with electronic access control systems and feature PIN code or RFID card access. The Assa Abloy Yale Assure Lever is a prominent example, offering Z-Wave and Wi-Fi connectivity. Lever handle smart locks are also gaining traction in premium apartment complexes and office suites.

Mortise Locks

Are a traditional European design adapted for smart features. They are common in high-end commercial settings and luxury residential properties where the door already has a mortise pocket. Brands like Baldwin and Kwikset offer smart mortise locks that combine heavy-duty hardware with Bluetooth or Zigbee modules. While representing a smaller volume segment, mortise locks command higher margins due to their robust construction and customization options.

Padlocks and Specialty Locks

Cover portable use cases like gates, locker rooms, and shared bike storage. The Master Lock Bluetooth Padlock and the Tapplock Wi-Fi Padlock exemplify this category. They offer app-based unlocking and shareable access codes, making them ideal for temporary or transient security needs. As the sharing economy expands, these niche products are growing at a faster percentage rate, albeit from a small base.

Deadbolt Smart Locks

The most popular segment, covering keypad, touchscreen, and fingerprint-enabled models. Examples: Schlage Encode Plus, August Wi-Fi Smart Lock. These fit standard 2-3/8" backset doors and offer Grade 1 or 2 security ratings.

Lever Handle Smart Locks

Designed for commercial and multi-tenant buildings, these integrate with access control software. Notable: Yale Assure Lever, which supports both Z-Wave and Matter. Often feature key-override for emergency egress.

Portable & Specialty Locks

Includes Bluetooth padlocks for gates and lockers. Master Lock Bluetooth Padlock and Tapplock Wi-Fi Padlock exemplify this niche. Target markets: gyms, shared offices, and bike storage.

4. Leading Players

Brand competition in the smart door lock space is intense, with established lock manufacturers vying against tech-first startups. Three distinct archetypes dominate.

The Heritage Lock Giant: Schlage (Allegion)

Schlage leverages decades of mechanical lock distribution and brand trust. Its Encode Plus line integrates Apple HomeKey, allowing users to unlock with an iPhone or Apple Watch, while maintaining ANSI Grade 1 security ratings. Schlage’s strategy is to bridge traditional security expectations with modern smart features, targeting homeowners upgrading from conventional locks. The company also offers commercial-grade solutions like the Schlage AD-400, which works with existing access control systems. This dual-channel approach gives it a strong foothold in both retail and security dealer networks.

The Retrofit Innovator: August (Assa Abloy)

August disrupted the market with a lock that fits over existing deadbolts, requiring no rekeying or door modification. Its Wi-Fi Smart Lock Pro and Smart Lock Gen 4 feature DoorSense™ technology that confirms door open/closed status. August’s strategy is to minimize installation friction, appealing to renters and DIY homeowners. By integrating with Amazon Key and Airbnb, the brand has carved out a leadership position in the short-term rental and delivery-access verticals. Its parent company, Assa Abloy, provides scale while preserving August’s product agility.

The Full-Building Ecosystem Player: Yale (Assa Abloy)

Yale offers the broadest product range, from the low-cost Yale Real Living to the premium Yale Linus. The brand’s key differentiator is its compatibility with nearly every major smart home platform—Z-Wave, Zigbee, Wi-Fi, HomeKit, and Matter. Yale also provides integrated access control for multi-tenant buildings through the Yale Access ecosystem, which includes controllers, keypads, and remote management software. This positions Yale as a one-stop solution for property managers looking to standardize across units without locking into a single protocol.

The Security-First Specialist: Kwikset

A subsidiary of Spectrum Brands, Kwikset is known for its SmartKey re-key technology, which allows homeowners to change keys instantly. Its smart locks, like the Kwikset Halo, emphasize ease of installation (no hub required) and strong AES-256 encryption. Kwikset’s strategy targets price-conscious consumers who want reliable, no-fuss smart security. The brand also offers the Kevo series with Bluetooth touch-to-open, appealing to users who prioritize speed over full IoT integration.

Heritage Lock Integrator

Schlage (Allegion) leverages its century-old door hardware reputation to offer high-security smart locks with Apple HomeKey integration, capturing homeowners who demand both trust and modern tech.

Retrofit Specialist

August (Assa Abloy) focuses on DIY installation over existing deadbolts, targeting renters and homeowners who can't replace the entire lock. Its DoorSense technology and Airbnb integration drive adoption in the sharing economy.

Cross-Protocol Platform Player

Yale (Assa Abloy) offers the widest protocol support (Z-Wave, Zigbee, Wi-Fi, Matter, HomeKit), positioning itself as the vendor-agnostic choice for property managers standardizing smart access across diverse buildings.

5. Market Trends

1. TREND: AI-Powered Risk Detection

Smart locks are embedding on-device AI to analyze unlock patterns and detect anomalies—such as repeated failed attempts or unusual unlock times. This enables proactive alerts rather than passive logs. Yale’s latest firmware uses machine learning to differentiate between normal family behavior and potential break-in attempts, sending immediate notifications. As edge AI hardware costs drop, this capability is moving from premium models to mid-range products by 2026.

2. TREND: Matter Protocol Universal Adoption

The Matter smart home standard, backed by Apple, Google, Amazon, and Samsung, is unifying smart lock connectivity. By 2026, most new smart locks will ship with Matter support, eliminating the need for proprietary hubs. Schlage and August have already released Matter-compatible firmware updates. This trend lowers compatibility friction for buyers and reduces inventory complexity for distributors, accelerating market growth.

3. TREND: Biometric Access Goes Mainstream

Fingerprint and facial recognition are moving from high-end office doors to residential smart locks. The cost of capacitive fingerprint sensors has fallen below $5 per unit, enabling sub-$150 models with biometric unlock. Kwikset’s Obsidian uses a fingerprint sensor embedded in the deadbolt face, while several Chinese OEMs are testing 3D facial recognition locks for the Asian market. This trend addresses a perennial consumer pain point: carrying keys or remembering codes.

6. Regional Markets

North America: Platform-Led Growth

High penetration of Amazon Alexa and Apple HomeKit drives demand for compatible smart locks. The region's CAGR of 10.4% is fueled by package theft concerns and short-term rental management needs.

Europe: Security Compliance First

Stringent building codes and GDPR restrictions push brands toward offline-capable locks with local data processing. Germany and the UK lead adoption, with a preference for mortise and lever handle formats.

Asia Pacific: Mobile-First Adoption

Smartphone ubiquity and rapid urbanization make China and South Korea the fastest-growing markets. Fingerprint and facial recognition locks are common, with brands like Tencent-backed HiKeep emerging.

7. Investment Outlook

Two specific opportunities stand out for industry players. First, the new construction channel offers a massive growth runway. Homebuilders are increasingly offering smart locks as standard features in mid- to high-end projects. By partnering with builders to pre-install compliant locks that integrate with their preferred home automation platform, lock brands can lock in multi-year revenue. Second, the retrofit market remains underserved: over 80% of U.S. homes still have traditional deadbolts. Retrofittable models like August’s could capture this base with aggressive marketing and easy installation kits.

The single biggest risk is cybersecurity. A high-profile breach of a major brand’s smart lock would erode consumer trust across the entire category. As locks become more connected, attack surfaces expand—cloud APIs, Bluetooth pairing, firmware updates. Brands that invest in independent security audits and publish transparent vulnerability disclosure programs will build long-term advantage. The market’s CAGR of 16–20% is achievable, but only if manufacturers treat security as a non-negotiable pillar of product development, not a marketing checkbox.

Strategic Considerations:

- New Construction Integration: Homebuilders are standardizing smart locks as included features. Lock brands that pre-certify with popular home automation platforms (e.g., Control4, Crestron) can secure multi-project contracts.

- Retrofit Upsell Potential: Over 80% of global doors still use mechanical locks. Retrofittable smart locks with no-wiring installation can capture this massive installed base through retail and e-commerce channels.

- Cybersecurity Breach Liability: A single massive-scale vulnerability exploit could halt market growth. Brands must invest in OWASP-compliant testing and bug bounty programs to maintain buyer confidence.

- Battery Life Innovation: Frequent battery changes are a top consumer complaint. Companies achieving 12+ months of real-world usage via low-power chips (e.g., Nordic nRF52 series) will gain clear competitive advantage.

Frequently Asked Questions

Make Informed Decisions in the Smart Door Lock Brands Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-06. All market figures are estimates and may vary from actual results.