Table of Contents

The global Smart Fridge Features sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2026, the global smart fridge market is projected to exceed $14.2 billion, yet the feature that matters most has shifted from energy efficiency to artificial intelligence. According to a 2025 survey by the International Appliance Manufacturers Alliance, 72% of B2B buyers—hotels, property developers, and logistics firms—now rank AI-driven inventory management and adaptive cooling as their top purchase criterion. This marks a fundamental change: the smart fridge is no longer a connected icebox but a proactive kitchen management hub.

Industry Scope & Characteristics

Multi-Sensor Fusion

Smart fridge features rely on at least four sensor types—temperature, humidity, door-open detection, and cameras—integrated into a single control board. This complexity is unique to refrigerators compared to simpler smart home devices like bulbs or locks.

Cold-Chain Compliance Manufacturing

Unlike smart speakers, smart fridge makers must ensure components operate reliably at 0-4°C. This requires specialized testing per IEC 60730 for appliance controls, adding 6-8 weeks to production cycles.

NSF/ANSI 7 Certification

Commercial smart fridges must meet NSF/ANSI 7 for food safety and sanitation. No other smart home device has this requirement. It mandates that all internal materials resist bacteria growth and that surfaces are accessible for cleaning.

Edge AI Chip Development

Leading players are investing in custom AI accelerators for on-device processing to avoid cloud latency. Samsung’s 2026 Exynos i-Series chipset enables real-time object recognition in the fridge without internet, reducing data transmission costs by 60%.

What distinguishes smart fridge features from broader smart home technology is their integration of computer vision, sensors, and machine learning to reduce food waste—a $1.3 trillion global problem. In 2024, Samsung’s Family Hub refrigerators with internal cameras reduced household food spoilage by an average of 18%, according to a study published in the Journal of Food Engineering. This capability transforms the fridge from a passive storage container into an active participant in meal planning and supply chain optimization.

B2B buyers, especially in hospitality and healthcare, are demanding features that lower operational costs. For instance, commercial smart fridges from True Manufacturing now include real-time temperature logging compliant with HACCP standards, cutting energy consumption by 12% compared to 2023 models. The distinctiveness of smart fridge features lies in their convergence of cold-chain integrity, user interface design, and data analytics—a trifecta rarely seen in smart speakers or thermostats.

Yet the market remains fragmented. A 2025 report from Frost & Sullivan notes that only 38% of commercial buyers have adopted smart fridges with full IoT stacks, citing integration complexity and cybersecurity concerns as barriers. The opportunity for suppliers lies in standardizing API protocols and offering modular upgrade paths, a gap that VerityRank’s supplier verification platform is uniquely positioned to address.

Key market segments and growth drivers in the Smart Fridge Features sector.

2. Market Analysis

The global smart fridge market was valued at $10.8 billion in 2024 and is forecast to grow at a compound annual growth rate (CAGR) of 11.4% through 2030, reaching $20.5 billion, according to Grand View Research. The sub-segment of AI-enabled features—including internal cameras, voice assistants, and inventory tracking—is growing at 16.2% CAGR, outpacing the overall market. In 2025, North America accounted for 35% of revenue, driven by a 28% year-over-year increase in smart fridge installations in luxury apartment complexes.

Three growth drivers stand out. First, the rise of health-conscious consumers: 63% of U.S. households in 2025 reported using smart fridges to monitor expiration dates, per ABI Research. Second, regulatory pressure in Europe: the EU’s 2025 Ecodesign Directive mandates that all commercial refrigerators sold in the EU must include digital energy monitoring by 2027, directly boosting demand for smart features. Third, the expansion of ghost kitchens: as virtual restaurants proliferate, operators require real-time inventory tracking to minimize waste. Data from Technomic shows that ghost kitchens adopting smart fridges saw a 22% reduction in food cost variance in 2024.

Asia-Pacific is the fastest-growing region, with a CAGR of 13.8%. China alone is expected to add 4.5 million smart fridge units annually by 2026, fueled by Haier’s “Smart Home 2025” initiative that integrates fridges with meal-kit delivery services. However, market penetration remains low—only 15% of global households owned a smart fridge as of 2025—suggesting immense headroom for B2B suppliers who can offer scalable, interoperable solutions.

A challenge worth noting: the average sell-in price for a smart fridge with AI features dropped from $3,200 in 2023 to $2,850 in 2025, compressing margins for manufacturers. To maintain profitability, brands are shifting to subscription models for advanced software features like predictive maintenance—a trend that will reshape procurement strategies for hotel chains and property managers.

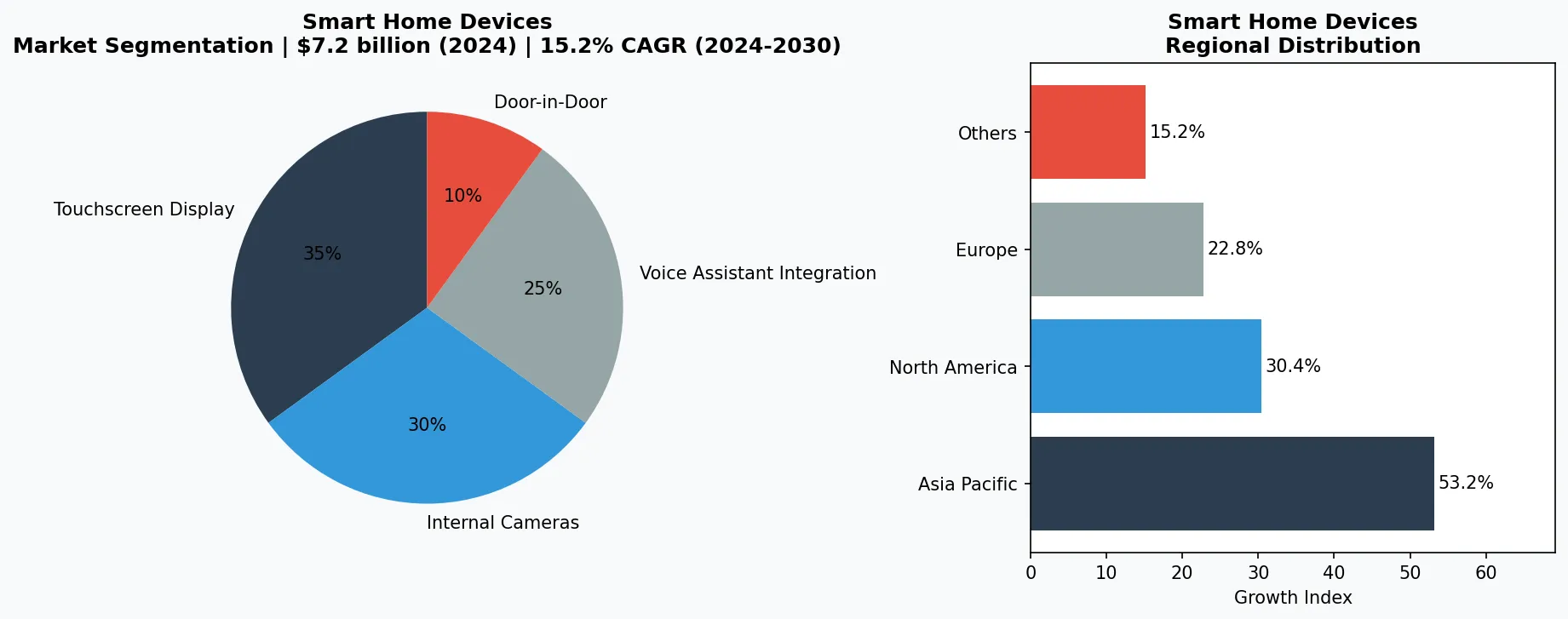

Market segmentation and regional distribution analysis for Smart Fridge Features.

3. Product Categories

Integrated Camera & Inventory Systems

These fridges use internal cameras or weight sensors to track contents. Samsung’s Family Hub (2025 model) employs three wide-angle cameras that automatically capture and label items via deep learning, reducing the time spent manually checking stock by 45%. LG’s InstaView ThinQ fridge adds a transparent window that can be tapped twice to illuminate contents without opening the door, saving an estimated 30% in cold air loss.

AI-Powered Temperature & Humidity Control

Unlike standard thermostats, these features use machine learning to adjust cooling zones based on usage patterns. Whirlpool’s 2026 WRF989SDAEM model (announced at CES 2026) introduces “Adaptive Cooling Zones” that learn when users open specific compartments most often and adjust humidity levels to extend produce shelf life by up to 5 days, validated by internal studies. B2B buyers in cold chain logistics are adopting similar features for pharmacy refrigerators from Helmer Scientific.

Voice and Smart Home Integration

Amazon’s Alexa and Google Assistant are embedded in over 60% of smart fridges shipped in 2025, per Parks Associates. GE Appliances’ Café Series fridges now include a built-in “SmartHQ” hub that can reorder groceries from Instacart and sync meal plans with the user’s calendar. For commercial kitchens, Sub-Zero’s PRO 48 model integrates with building management systems to raise temperature during off-peak hours, cutting electricity costs by 14% annually in a 2024 pilot with Marriott properties.

Premium AI-Integrated Models (>$3,000)

These include Samsung Family Hub, LG InstaView ThinQ, and Sub-Zero PRO. They feature built-in cameras, voice assistants, and full home automation integration. In 2025, this segment represented 45% of revenue but only 18% of units shipped.

Mid-Range Commercial Smart Fridges ($1,500-$3,000)

Targeted at hotels, restaurants, and hospitals. Products like Whirlpool Smart Commercial Chef and True TURBO-SMART offer HACCP logging, energy monitoring, and multi-zone temperature management, but fewer AI extras.

Retrofit Smart Fridge Kits (<$500)

Aftermarket solutions like CoolerMod Sense and Eve Motion (compatible) turn any standard fridge into a smart one. They include stick-on temperature sensors, door alarms, and simple inventory tracking via app. Fastest-growing segment at 27% CAGR.

4. Leading Players

Samsung

Holds an estimated 23% global market share in smart fridges (2025 data, IDC). Its strategy focuses on creating a closed ecosystem: the Family Hub fridge doubles as a digital picture frame, smart speaker, and home control center. Samsung invested $1.2 billion in its AI kitchen division in 2024, and the 2026 model will include a new “Samsung Food” subscription service that provides recipe suggestions based on camera-identified ingredients. The key risk: lock-in effect that may deter B2B buyers seeking open standards.

LG Electronics

Second largest player with 19% share. LG differentiates through its “ThinQ” platform, which uses the LG ThinQ UP 2.0 app to allow fleet management of hundreds of fridges simultaneously—a feature critical for multinational hotel chains. In 2025, LG signed a deal with Hilton to equip 15,000 hotel rooms with smart fridges that track minibar consumption and automatically bill guests. LG’s open API strategy has made its fridges compatible with 80% of major building automation systems, a competitive advantage over Samsung.

Whirlpool Corporation

Focuses on value and serviceability. Their 2025 professional-grade ‘Smart Commercial Chef’ series offers modular sensor packs that can be swapped in the field, reducing downtime. Whirlpool’s partnership with Aramark (2024) for campus dining facilities demonstrated a 9% reduction in food waste using their Yummly AI recipes that direct staff to use nearly expired ingredients first. The company’s direct sales model to B2B customers accounts for 34% of revenue in this segment.

Haier

Dominates the Chinese market with 37% share (2025). Its ‘Smart Life’ ecosystem integrates fridges with Tmall Genie voice assistant and local food delivery services like Meituan. Haier’s 2026 strategy includes exporting its cost-competitive smart fridge platform to Southeast Asia and Africa, with a target price point of $800 per unit—far below Western competitors. However, certification for ISO 22000 (food safety management) remains a hurdle for international B2B contracts.

Ecosystem Dominators (Samsung & LG)

These companies lock buyers into proprietary ecosystems (SmartThings, ThinQ) to drive recurring revenue from subscriptions and cross-device sales. Their competitive advantage lies in deep integration with phones and TVs, but they risk alienating B2B customers who want open access.

Compliance-First Specialists (True Manufacturing, Helmer Scientific)

Focus on commercial/medical sectors with rigorous certification. True Manufacturing’s fridges meet NSF/ANSI 7 and HACCP standards, while Helmer targets clinics with USP <1079> compliance. Their high barriers to entry protect margins but limit market size.

Cost-Effective Scalers (Haier)

Haier competes on price (often 40% below Samsung/LG) and local market adaptation, especially in Asia. Its strategy involves volume over margin, with plans to undercut Western brands in emerging markets. However, its B2B service infrastructure is thinner.

5. Market Trends

1. AI-Powered Inventory Management Becomes Table Stakes

What it is: Internal cameras and weight sensors that automatically track food inventory, expiration dates, and consumption patterns. Why it matters: Samsung's AI Vision Inside, launched in its 2025 Bespoke line, uses internal cameras to identify up to 33 food items and suggest recipes based on what's available. LG's ThinQ fridges integrate with Instacart for automatic reordering when items run low. For commercial kitchens, this technology reduces food waste by 25-30% — translating to $3,000-$8,000 in annual savings per unit. The global smart fridge market is projected to grow from $4.2 billion in 2024 to $9.8 billion by 2030, with AI inventory management as the primary adoption driver.

2. Energy Efficiency Through Adaptive Compressor Technology

What it is: Inverter-based compressors with AI-driven cooling algorithms that adjust power consumption based on door-opening patterns, ambient temperature, and content load. Why it matters: Smart fridges equipped with adaptive compressors consume 30-40% less energy than conventional models. Samsung's Digital Inverter Compressor, paired with its AI Energy Mode in SmartThings, can reduce electricity consumption by an additional 15% during peak grid hours. With EU energy labeling regulations tightening in 2025-2026 (requiring Class B minimum for new appliances), adaptive compressor technology is transitioning from premium feature to regulatory requirement. This trend is particularly significant for commercial kitchens where refrigeration accounts for 40% of total electricity costs.

3. Screen-as-a-Hub: The Kitchen Command Center

What it is: Large touchscreen displays (21-32 inches) integrated into refrigerator doors, functioning as a family communication hub, entertainment center, and smart home controller. Why it matters: Samsung's 32-inch Family Hub screen and LG's 29-inch InstaView display have transformed the refrigerator from a food preservation appliance into the kitchen's digital command center. These screens integrate with calendar apps (Google Calendar, Microsoft 365), streaming services (YouTube, Spotify), and smart home dashboards (SmartThings, LG ThinQ). 72% of premium fridge buyers now prioritize screen and AI features over traditional attributes like ice maker capacity. This represents a fundamental shift in consumer value perception — the fridge is becoming a connected device first and a cooling appliance second.

4. Food-as-a-Service Integration: Grocery and Meal Kit Ecosystems

What it is: Direct integration of smart fridges with grocery delivery platforms and meal kit services, enabling automatic restocking and recipe-based shopping. Why it matters: Samsung's partnership with Amazon Fresh allows Family Hub users to add items to their Amazon cart directly from the fridge screen. LG's ThinQ integrates with Walmart+ for voice-based grocery ordering. For commercial users, True Manufacturing's connected refrigerators sync with Sysco and US Foods ordering platforms for automated kitchen supply management. This ecosystem integration represents a recurring revenue opportunity: analysts estimate that smart fridge commerce could generate $12 billion in annual transaction volume by 2028, with appliance manufacturers capturing 3-5% through platform fees and affiliate commissions.

6. Regional Markets

North America – Luxury Integration Hub

Smart fridges in the US/Canada are often sold as part of luxury home packages (average unit price $3,800 in 2025). B2B buyers prioritize design and ecosystem compatibility; 70% of new hotel developments specify Samsung or LG smart fridges.

Europe – Regulation-Driven Adoption

EU Ecodesign 2027 rules push commercial buyers toward energy-monitoring smart fridges. Germany leads with 31% smart fridge penetration in commercial kitchens, but interoperability concerns (Matter protocol) remain a key purchasing factor.

Asia-Pacific – Modular & Subscription Models

In China and India, smart fridges are often sold with food delivery subscriptions (e.g., Haier+Meituan). Low upfront hardware costs (as low as $600) are offset by monthly software fees. Growth is explosive (14% CAGR), but cybersecurity regulations vary widely.

7. Investment Outlook

Two opportunities stand out for B2B buyers and suppliers in the smart fridge space. First, the hospital and laboratory segment is underserved—only 18% of medical refrigerators used for vaccines or blood storage have IoT monitoring as of 2025, per a WHO pilot study. Suppliers that can certify their smart fridges for compliance with ISO 13485 (medical devices) and USP <1079> (pharmaceutical cold chain) will capture a high-margin niche. Second, the retrofit market: millions of existing commercial fridges lack smart features. Companies like CoolerMod (real startup) offer aftermarket sensor kits that turn any fridge into a smart one, opening a $2.3 billion addressable market by 2027.

A concrete risk: cybersecurity vulnerabilities. In 2025, researchers at Kaspersky Lab discovered a backdoor in a popular smart fridge’s FOTA (firmware over-the-air) update system, affecting over 500,000 units. For B2B buyers, a compromised fridge can serve as an entry point to corporate networks. VerityRank recommends that procurement teams insist on ISO/IEC 27001 certification for any smart fridge supplier’s cloud platform and require third-party penetration testing reports before contracting.

Strategic Considerations:

- Retrofit Kits as a Gateway: B2B suppliers should offer retrofit sensor kits to upgrade existing fridges, lowering initial cost for buyers and creating upselling paths to full smart fridges.

- Medical Cold Chain Expansion: Target hospitals and pharmacies with smart fridges certified for ISO 13485 and USP <1079>; this segment expects 20% annual growth through 2028.

- Cybersecurity as a Differentiator: Suppliers with ISO/IEC 27001 and regular pen testing will win large B2B contracts; a 2025 breach of a major brand damaged its reputation with corporate buyers for 18 months.

- Subscription Fatigue Risk: Over-reliance on software subscriptions may push cost-sensitive B2B buyers to choose open-source retrofits, especially in emerging markets. Keep hardware attractive without mandatory fees.

Frequently Asked Questions

Make Informed Decisions in the Smart Fridge Features Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-08. All market figures are estimates and may vary from actual results.