Table of Contents

The global Smart Kitchen Technology Trends sector serves consumers worldwide with diverse solutions.

1. Industry Overview

By 2026, the global smart kitchen market will be worth $24.22 billion—and it’s not just about appliances. This transformation is rewriting the rules for kitchen furniture, where cabinets, islands, and pantry units are evolving from static storage into intelligent hubs. The convergence of AI-driven appliances, IoT connectivity, and sensor-laden hardware means that a kitchen island today can do more than hold a chopping board: it can track inventory, suggest recipes, and even adjust lighting based on usage patterns. For B2B buyers sourcing kitchen furniture, this shift demands a new lens—one that evaluates not just wood and finish, but embedded technology and ecosystem compatibility.

Industry Scope & Characteristics

Embedded Intelligence in Furniture

Smart kitchen technology products integrate sensors, displays, and connectivity into traditional furniture like cabinets and islands. For example, smart pantry cabinets use RFID tags and weight sensors to track inventory automatically.

Cross-Industry Supply Chain Demands

Manufacturing smart kitchen furniture requires collaboration between woodworkers, electronics engineers, and software developers. Supply chains must manage both timber sourcing and semiconductor procurement, often from different regions.

Safety and Certification Complexity

Smart furniture must comply with dual standards: furniture safety (e.g., ASTM F2057 for tip-over) and electrical safety (e.g., UL 962 for household furnishings with power). This adds layers of testing and certification.

AI and Sensor Fusion R&D

Current R&D focuses on fusing data from multiple sensors—weight, temperature, humidity, and motion—to create predictive kitchen assistants. For instance, a smart island can detect cooking patterns and suggest energy-saving modes.

What makes this sub-topic distinctive within the broader kitchen furniture industry is the fusion of hardware and software. Traditional cabinet makers now compete with tech-forward brands that embed touchscreens, weight sensors, and automated drawers into their designs. The kitchen bench is no longer a passive work surface; it can incorporate induction charging zones and smart scales. Pot racks, once purely decorative, now integrate RFID tags to log cookware usage. This is not incremental innovation—it is a structural redefinition of what kitchen furniture can be.

The growth trajectory is staggering. The smart kitchen appliances segment alone is projected to surge from $17.88 billion in 2024 to $94.98 billion by 2031, a compound annual growth rate (CAGR) of over 25%. Meanwhile, the broader smart kitchen systems market, valued at $57.39 billion in 2026, is expected to reach $141.78 billion by 2030. These numbers signal that the furniture layer of the smart kitchen—cabinets, islands, and storage—represents a fast-growing, high-value opportunity for suppliers and buyers alike.

Key market segments and growth drivers in the Smart Kitchen Technology Trends sector.

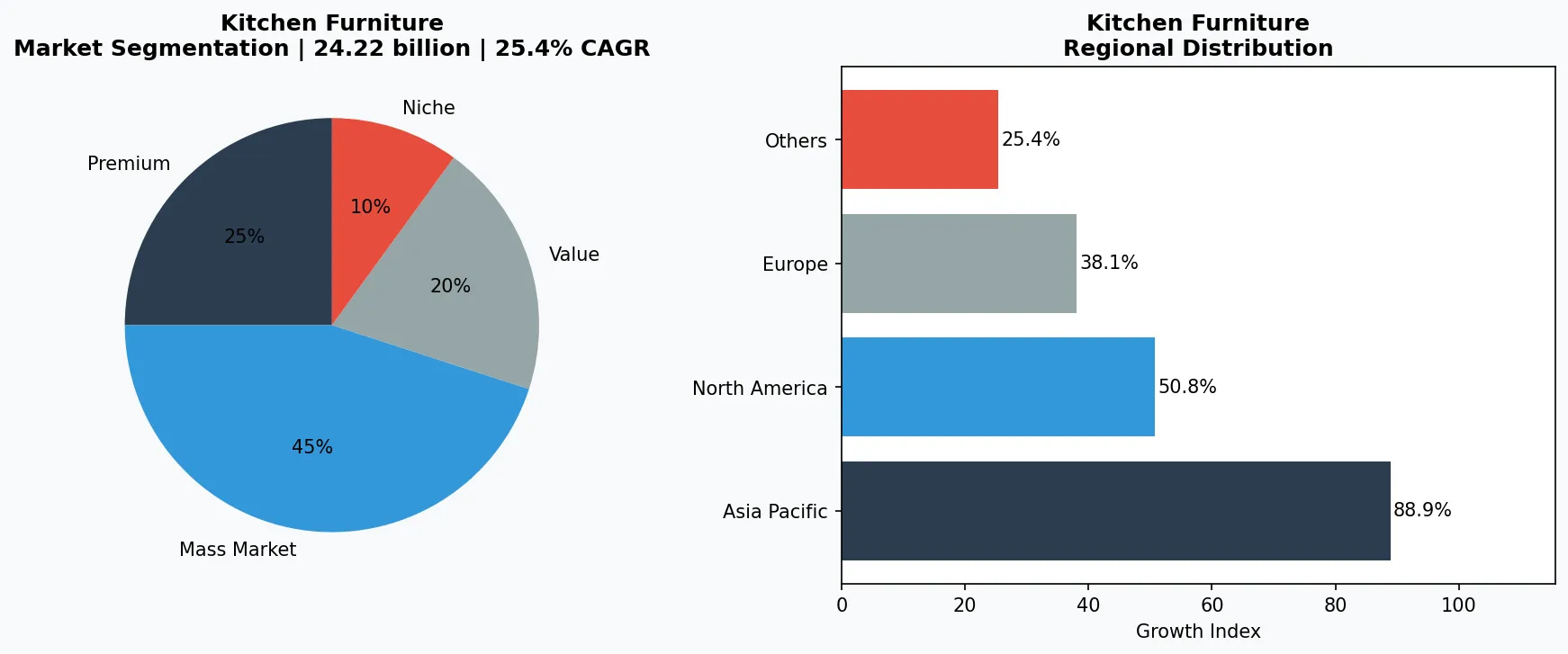

2. Market Analysis

The smart kitchen market is not a monolith; it is composed of distinct segments where investment is flowing unevenly. According to competitor research, the global smart kitchen market was valued at $24.22 billion in 2026, growing at a CAGR of 11.09% to reach $40.98 billion by 2031. However, the smart kitchen appliances sub-segment is expanding far faster, with a CAGR exceeding 25%, from $17.88 billion in 2024 to $94.98 billion by 2031. This divergence highlights a critical trend: the hardware layer—appliances, sensors, and connectivity modules—is attracting the lion’s share of R&D capital, while furniture manufacturers must adapt to integrate these components.

Three growth drivers dominate. First, the rise of connected kitchen appliances, which now communicate via common protocols like Matter and Thread, creates demand for furniture that can house and conceal wiring, screens, and sensors. Second, the shift toward hands-free kitchens—fueled by voice assistants and gesture controls—requires surfaces and storage that support touchless operation. Third, health and wellness trends are pushing for smart pantries that track expiration dates and nutritional content, driving demand for cabinets with embedded scanners and digital displays.

Geographically, North America leads in smart kitchen adoption, accounting for over 35% of global revenue in 2025, according to Mordor Intelligence. Europe follows, driven by energy-efficiency regulations, while Asia-Pacific is the fastest-growing region, with China and India investing heavily in smart home ecosystems. For B2B buyers, this means sourcing strategies must account for regional standards—UL certification in the U.S., CE marking in Europe, and CCC in China—especially when integrating electronics into furniture.

Market segmentation and regional distribution analysis for Smart Kitchen Technology Trends.

3. Product Categories

Smart kitchen technology is manifesting in four distinct product categories within kitchen furniture. First, smart cabinets and pantry units are the new frontier. These units integrate weight sensors in shelves to track inventory, automated lighting that adjusts to time of day, and even built-in RFID scanners that log every item placed inside. For example, IKEA’s RÖNNINGE series has experimented with modular smart storage that syncs with recipe apps. Second, intelligent kitchen islands are evolving into command centers. They now incorporate pop-up touchscreens, wireless charging pads, and retractable power outlets. High-end models from manufacturers like SieMatic include built-in induction hobs and refrigerated drawers, blurring the line between furniture and appliance.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Third, smart bar counters and kitchen benches are being redesigned for connectivity. These surfaces can include integrated scales for precision cooking, temperature-controlled zones for wine or cheese, and even embedded displays for video recipes. The key innovation is the use of tempered glass or ceramic tops that are both durable and touch-interactive. Fourth, pot racks and hanging storage are becoming part of the IoT ecosystem. Smart pot racks use RFID tags to identify cookware and suggest compatible recipes, while some models include built-in timers and heat sensors to prevent overcooking.

For B2B buyers, the critical takeaway is that smart furniture requires careful specification of power, data, and thermal management. A smart cabinet is only as reliable as its wiring and cooling system. Suppliers must ensure that all electronic components are certified for kitchen environments—resistant to heat, moisture, and grease—and that software updates are supported over the product’s lifecycle.

4. Leading Players

The competitive landscape in smart kitchen technology is fragmented but converging. IKEA, the global furniture giant, is leveraging its scale to democratize smart storage. Through its partnership with Sonos and integration with Apple HomeKit, IKEA’s smart cabinets and lighting systems offer an accessible entry point for consumers. The company’s strategy is ecosystem-driven: every smart furniture piece connects via the IKEA Home smart app, creating a low-cost, modular platform that appeals to both residential and small commercial buyers.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the kitchen furniture space.

SieMatic, a German luxury kitchen furniture manufacturer, targets the high end with fully integrated smart islands. Their S2 series features a central island with a built-in touchscreen, automated height adjustment, and connectivity to smart appliances. SieMatic’s competitive advantage lies in bespoke design combined with seamless tech integration—a model that commands premium pricing and long lead times. For B2B buyers seeking differentiation, SieMatic represents a benchmark in quality, though at a cost that suits luxury hospitality and high-end residential projects.

Miele, while primarily an appliance maker, is increasingly influencing furniture design. Their Dialog oven and smart refrigerator lines require cabinetry that accommodates specific ventilation, power, and data ports. Miele’s strategy is to co-develop furniture specifications with cabinet makers, ensuring that their appliances fit seamlessly into smart kitchen ecosystems. This creates an opportunity for furniture suppliers to partner with appliance brands, offering certified compatibility as a value-add. For Verity Rank users, verifying a supplier’s partnership with major appliance brands is a key quality indicator.

5. Market Trends

1. RISE OF CONNECTED KITCHEN APPLIANCES |

Rise of Connected Kitchen Appliances | This trend refers to the proliferation of appliances that communicate with each other and with users via Wi-Fi, Bluetooth, or Zigbee. It matters because it transforms the kitchen from a collection of standalone devices into a coordinated system. IKEA’s smart kitchen line, for instance, allows a smart fridge to alert a smart cabinet when milk is running low.

2. AI-DRIVEN PREDICTIVE FUNCTIONALITY | AI ENABLES

AI-Driven Predictive Functionality | AI enables appliances and furniture to learn user habits and anticipate needs. For example, smart pantries can suggest meals based on inventory, while intelligent islands can adjust lighting and temperature based on cooking activity. This trend is driving demand for furniture with embedded sensors and processors. SieMatic’s S2 island uses AI to learn a chef’s preferred counter height and lighting levels.

3. HANDS-FREE AND VOICE-CONTROLLED KITCHENS | VOICE

Hands-Free and Voice-Controlled Kitchens | Voice assistants like Amazon Alexa and Google Assistant are being integrated into kitchen furniture, allowing users to control cabinets, lighting, and appliances without touching surfaces. This is especially important for hygiene and accessibility. Miele’s Dialog oven, for example, can be voice-activated, and its cabinetry is designed to house microphones and speakers without compromising aesthetics.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

Two specific opportunities stand out for B2B buyers in smart kitchen furniture. First, the modular smart cabinet segment is underpenetrated—few suppliers offer standardized, certified smart storage units that can be easily retrofitted. Early movers who develop UL-listed, plug-and-play smart cabinets will capture significant market share. Second, the hospitality sector is ripe for disruption: hotels and restaurants need durable, connected kitchen furniture that can withstand heavy use while providing data on inventory and energy consumption. Suppliers who offer commercial-grade smart islands with integrated point-of-sale and inventory tracking will find a ready market.

One concrete risk is obsolescence. Smart kitchen technology evolves rapidly, and furniture with embedded electronics may become outdated within five years. Buyers must demand modular designs that allow component upgrades—such as swappable sensor modules or software-updatable control units—to extend product lifespan. Additionally, reliance on proprietary ecosystems (e.g., Apple HomeKit vs. Amazon Alexa) can lock buyers into single-vendor paths, increasing switching costs. Verity Rank recommends that buyers prioritize suppliers offering multi-protocol compatibility and open APIs to future-proof their investments.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Smart Kitchen Technology Trends Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-12. All market figures are estimates and may vary from actual results.