Table of Contents

The global Smart Lighting Control Systems sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The smart lighting control market is on the verge of an extraordinary expansion, with projections indicating growth from $20.11 billion in 2025 to $73.73 billion by 2034, representing a compound annual growth rate of 15.53%. This trajectory positions smart lighting control systems as one of the most dynamic segments within the broader home lighting industry, fundamentally transforming how consumers interact with and benefit from artificial illumination in their living spaces.

Industry Scope & Characteristics

Broad Product Portfolio

Products span Smart Lighting Control Systems, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

At its core, a smart lighting control system comprises hardware and software components that enable users to manage lighting fixtures—including ceiling lights, pendant lights, floor lamps, and LED strips—through networked connectivity. Unlike conventional lighting that operates through simple on-off switches, these systems offer granular control over brightness, color temperature, scheduling, and场景 automation. The distinguishing factor is integration: smart lighting control connects individual fixtures into a unified ecosystem that responds to user preferences, environmental conditions, and broader smart home commands.

The technology has evolved beyond basic smartphone apps to encompass voice control through Amazon Alexa and Google Assistant, geofencing capabilities that trigger lights based on location, and circadian rhythm programming that adjusts color temperature throughout the day. For the home lighting industry, smart control systems represent a value-creation opportunity, enabling manufacturers to differentiate commodity fixtures through intelligent features and recurring software services.

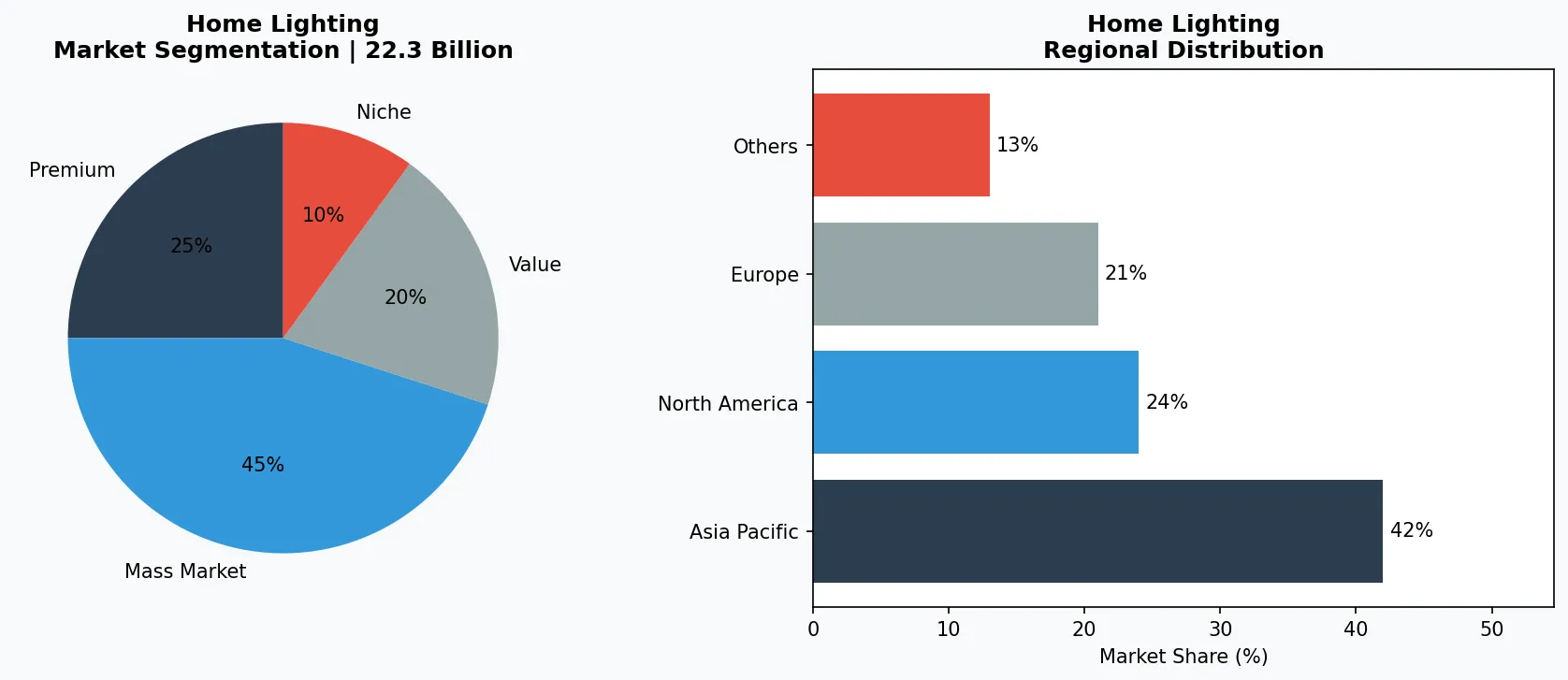

Key market segments and growth drivers in the Smart Lighting Control Systems sector.

2. Market Analysis

The smart lighting market demonstrates robust expansion across multiple measurement methodologies, reinforcing confidence in its growth trajectory. Market sizing estimates show values ranging from $15.2 billion in 2024 to projected figures between $32.4 billion and $127.4 billion by 2033, depending on scope and forecasting approach. Notably, the market is expected to grow by $139.36 billion from 2026 to 2030 alone, expanding at an 18.8% CAGR during this period. The Global Smart Lighting Market specifically is estimated at USD 34.4 billion in 2026, reflecting the immediate-term growth trajectory.

Three primary drivers fuel this expansion. First, stringent energy efficiency regulations worldwide are compelling residential and commercial consumers to replace incandescent fixtures with intelligent LED-based alternatives that smart control systems optimize. Second, the declining cost of LED components and wireless connectivity modules has narrowed the price gap between traditional and smart fixtures, accelerating mainstream adoption. Third, the proliferation of smart home ecosystems—smart speakers, home hubs, and connected appliances—creates natural demand for lighting integration, as consumers seek unified control interfaces.

The residential segment currently drives the majority of smart lighting adoption in home applications. Homeowners installing smart bulbs and switches typically pair them with existing smart speakers for voice control, creating a frictionless user experience that encourages expanded deployment. The commercial sector, however, is emerging as a high-growth opportunity, with the Smart Industrial Illumination Market projected to surpass USD 20.5 billion by 2036 as factories and facilities transition from basic LED retrofits to fully integrated intelligent lighting networks that deliver operational insights alongside illumination.

Market segmentation and regional distribution analysis for Smart Lighting Control Systems.

3. Product Categories

Smart Bulbs and Tunable Fixtures represent the most accessible entry point for consumers adopting smart lighting control. These replacement bulbs integrate directly into standard fixtures like ceiling lights and pendant lights, adding connectivity without requiring fixture replacement. Leading examples include Philips Hue White and Color Ambiance bulbs, which offer 16 million colors and seamless integration with major smart home platforms, and LIFX smart bulbs featuring native Wi-Fi connectivity without requiring a separate hub.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Centralized Control Hubs and Controllers serve as the brain of more sophisticated smart lighting installations. Systems like Lutron's Caseta bridge connect multiple dimmers, switches, and smart shades, providing reliable whole-home control even when internet connectivity fluctuates. These controllers often support both wireless protocols like Zigbee and proprietary RF technologies, enabling compatibility with diverse fixture types from chandeliers to recessed ceiling lights.

LED Strip Controllers and Drivers have emerged as a popular category for ambient and accent lighting applications. These devices transform conventional LED strips into addressable lighting capable of color-changing effects, zone-based control, and synchronization with music or media. Manufacturers like Govee and Nanoleaf offer controllers that enable consumers to install cove lighting, under-cabinet illumination, and decorative floor lamp installations with theatrical color effects.

Integrated Fixture Systems combine smart control electronics directly into lighting fixture designs, eliminating the need for aftermarket smart bulbs. Contemporary chandeliers, wall lamps, and pendant lights increasingly ship with built-in Wi-Fi connectivity, app control, and voice assistant compatibility as standard features. This integration appeals to consumers seeking aesthetically cohesive smart lighting solutions without visible smart bulb adapters or external controllers.

4. Leading Players

Signify (formerly Philips Lighting) maintains the industry's most recognized smart lighting brand through its Philips Hue ecosystem, which has become synonymous with residential smart lighting. The company's strategy centers on ecosystem completeness and interoperability, offering over 700 compatible products and extensive third-party integrations. Signify has expanded beyond consumer residential applications into professional lighting, acquiring related companies to offer smart lighting solutions for commercial buildings and outdoor municipal lighting networks. The company leverages its lighting expertise to differentiate through product quality and color accuracy while building recurring revenue through its Hue app subscriptions and partnerships.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the home lighting space.

Lutron Electronics dominates the premium smart lighting control segment with its sophisticated ecosystem of smart dimmers, switches, and motorized shading solutions. The company's strategy targets homeowners willing to invest in premium whole-home solutions rather than individual smart bulbs, emphasizing reliability, installation quality, and integration with high-end home automation platforms. Lutron's proprietary Clear Connect wireless technology ensures consistent communication without interference from Wi-Fi networks, a key differentiator for mission-critical installations. The company's recent Aurora smart bulb dimmer demonstrates its willingness to adapt strategies to accommodate changing market preferences.

Acuity Brands positions itself at the intersection of smart lighting and building data analytics through its Atrius platform, targeting commercial and industrial customers rather than residential consumers. This B2B focus differentiates Acuity from consumer-focused competitors, serving offices, retail environments, and healthcare facilities with lighting systems that generate occupancy data and energy analytics. Schneider Electric similarly emphasizes integrated building management, incorporating smart lighting control into its broader EcoStruxure platform for smart building applications. Both companies recognize that the industrial illumination market projected to exceed $20.5 billion by 2036 represents substantial growth opportunity beyond consumer smart home applications.

5. Market Trends

1. VOICE CONTROL INTEGRATION

VOICE CONTROL INTEGRATION — Smart lighting control systems increasingly prioritize native voice assistant compatibility as a core feature rather than an add-on capability. With platforms like Amazon Alexa and Google Assistant now standard in most smart home environments, lighting manufacturers ensure seamless voice activation, scene triggering, and multi-room control through natural language commands. This trend matters because voice control reduces friction in daily lighting use, making smart features accessible to all household members without requiring smartphone interaction. Philips Hue recently enhanced its voice control capabilities by expanding native Alexa skill functionality, enabling more sophisticated voice commands for color adjustments and场景 programming.

2. AI-DRIVEN AUTOMATION

AI-DRIVEN AUTOMATION — Machine learning algorithms now power smart lighting systems that learn occupant preferences and automatically adjust settings without explicit programming. These systems analyze usage patterns, time of day, and environmental factors to optimize lighting conditions proactively. The trend matters because it transforms smart lighting from requiring active user management to functioning as a truly automated experience that improves over time. Companies like Signify are incorporating predictive algorithms into their Hue app that anticipate user needs based on historical behavior, while startups like Tossed Robotics integrate AI directly into smart switches to enable local processing without cloud dependency.

3. HUMAN-CENTRIC LIGHTING

HUMAN-CENTRIC LIGHTING — Circadian lighting systems that adjust color temperature and intensity to support natural sleep-wake cycles are gaining traction in both residential and commercial applications. These systems shift from cool blue-white light in morning hours to warmer tones in evening periods, mimicking natural daylight patterns. This trend matters because growing research demonstrates connections between light exposure and human health, productivity, and sleep quality. Sensity Systems offers human-centric lighting solutions for commercial offices demonstrating measurable improvements in occupant well-being, while residential manufacturers increasingly offer tunable-white fixtures that support circadian programming through dedicated scenes and automatic schedules.

6. Regional Markets

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

7. Investment Outlook

The outlook for smart lighting control systems presents substantial opportunities alongside notable challenges. First, voice control technology is becoming standard in new installations, with industry projections indicating that over 60% of residential smart lighting systems will feature voice assistant integration by 2026. Manufacturers that prioritize seamless voice interaction and multi-assistant compatibility will capture market share from competitors with limited platform support. Second, the commercial and industrial segments represent significant untapped opportunity as businesses seek lighting solutions that deliver energy savings while generating operational data. Companies that successfully position smart lighting as an intelligent building infrastructure component rather than merely illumination will unlock enterprise customers beyond traditional consumer channels.

The primary risk confronting the market is interoperability fragmentation, which could slow adoption if consumers encounter difficulty integrating products from different manufacturers. The coexistence of competing wireless protocols—Zigbee, Z-Wave, Thread, and Matter—creates consumer confusion and potential installation complexity. Should the industry fail to deliver reliable plug-and-play experiences across brands, purchase hesitation may increase, particularly among mainstream consumers less tolerant of technical troubleshooting. However, the Matter protocol's industry backing suggests the market will likely converge toward standardization, potentially resolving this challenge by 2027 and enabling faster growth thereafter.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Smart Lighting Control Systems Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-14. All market figures are estimates and may vary from actual results.