Table of Contents

The global Smart Lighting System Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

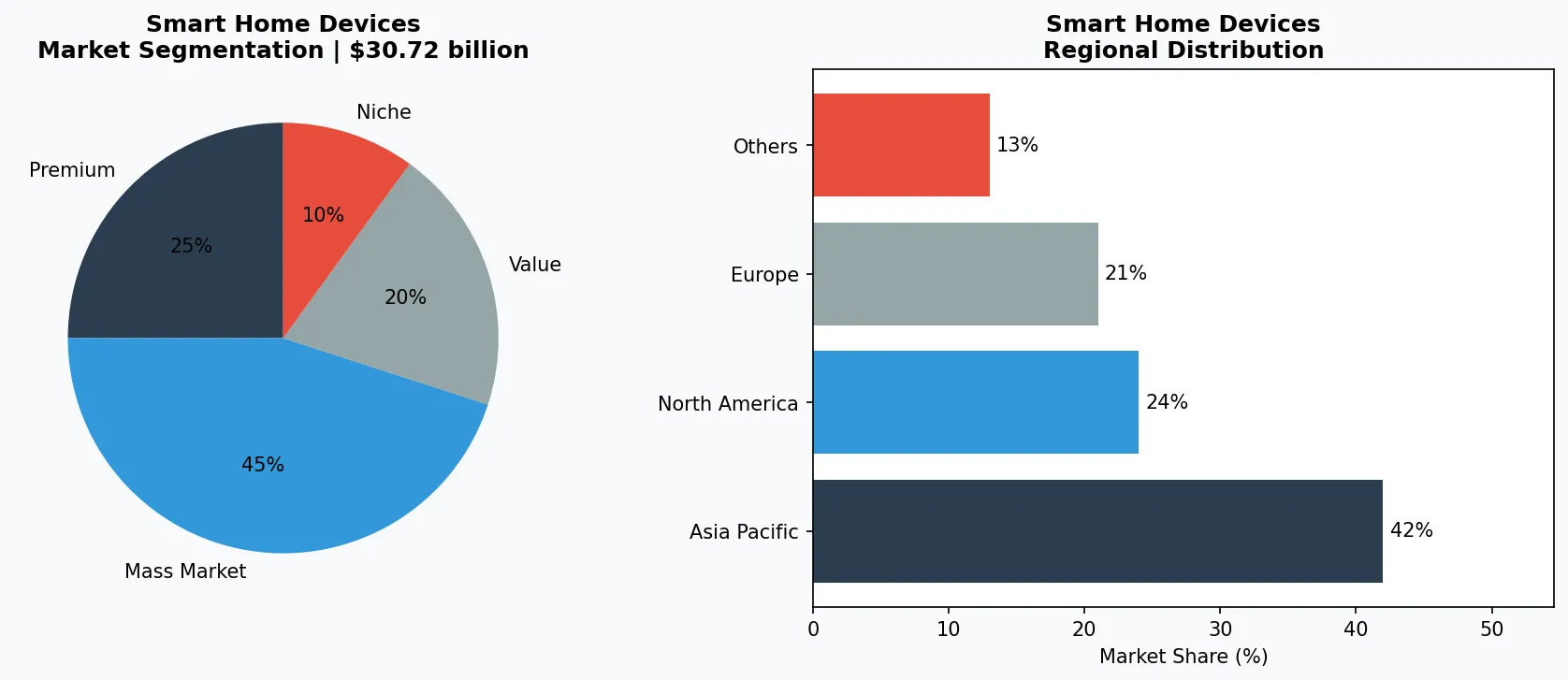

By 2026, the global smart lighting market is projected to reach $30.72 billion, and it's not slowing down. BloombergNEF estimates that by 2040, that figure will balloon to $221.59 billion — a compound annual growth rate of 15.16%. This isn't just about dimming bulbs from a phone. Smart lighting systems are now the nervous system of modern buildings, integrating sensors, data analytics, and AI to reduce energy consumption by up to 70% while enhancing occupant comfort. What makes smart lighting distinctive within the broader smart home ecosystem is its dual role: it's both an energy asset and a data platform. Unlike a smart speaker that only handles audio, a smart lighting system can detect occupancy, adjust color temperature based on circadian rhythms, and even feed occupancy data into HVAC and security systems. The LED revolution laid the groundwork — penetration hit 57% in 2021, according to MKL-21 — but the real value lies in the control layer. From PoE (Power over Ethernet) to DALI and Zigbee protocols, the competition is fierce. For B2B buyers, understanding the difference between a simple Wi-Fi bulb and a full-building management platform is critical. This guide cuts through the noise, offering a data-driven roadmap for procurement professionals navigating the smart lighting landscape in 2025 and beyond.

Industry Scope & Characteristics

Protocol Fragmentation

Smart lighting products rely on multiple wireless protocols (Zigbee, Thread, Bluetooth, Wi-Fi) and wired standards (DALI, PoE). The lack of universal interoperability remains a top procurement challenge for multi-vendor installations.

Lifespan vs. Software Obsolescence

LED luminaires have a 50,000-hour lifespan (17+ years), but the embedded control chips and firmware often become obsolete within 5 years. Component traceability and firmware-update guarantees are critical for long-term asset management.

Energy Star and UL Certifications

Commercial buyers should only source fixtures with Energy Star 2.0 certification and UL 924 (emergency lighting) or UL 2108 (low-voltage lighting). These ensure safety and compliance with local building codes.

Edge Computing in Luminaires

New-generation smart sensors embed MCUs that process occupancy and ambient-light data locally, reducing cloud latency. Enlighted's IoT sensors now support 20 local analytics rules, enabling real-time HVAC/lighting coordination without internet dependency.

Key market segments and growth drivers in the Smart Lighting System Guide sector.

2. Market Analysis

The smart lighting market is accelerating on three powerful engines: energy regulation, IoT integration, and declining hardware costs. The Smart Lighting Management Platform segment alone was valued at $4.2 billion in 2024 and is projected to hit $4.8 billion in 2025 — a 14% year-over-year jump. By 2026, the total smart lighting market (including lamps, fixtures, and controls) is expected to reach $34.43 billion, with forecasts showing it climbing to $127.46 billion by 2033. That's a CAGR of roughly 20.5% over the period, outpacing many adjacent smart home categories. Why such aggressive growth? First, governments worldwide are mandating stricter energy-efficiency standards. The EU's Energy Performance of Buildings Directive and the U.S. Inflation Reduction Act both incentivize retrofits that include networked lighting controls. Second, the proliferation of IoT sensors in commercial buildings — 1.2 billion smart lighting nodes are expected to be installed globally by 2026 — creates a data-rich environment for facility managers to optimize energy use. Third, LED prices have dropped 85% since 2010, making the incremental cost of adding smart controls negligible. The result: a market where the smart lighting management platform (software + gateways) is growing faster than hardware. Major growth corridors include North America (35% market share), Europe (28%), and Asia-Pacific (27%), with China alone accounting for 60% of global LED production capacity.

Market segmentation and regional distribution analysis for Smart Lighting System Guide.

3. Product Categories

Smart lighting systems fall into three primary categories.

Smart Lamps & Fixtures

Are the most visible: retrofit bulbs (e.g., Philips Hue White and Color Ambiance) and integrated luminaires (e.g., Osram Lightify ceiling panels) that offer dimming, color tuning, and scheduling via Bluetooth or Wi-Fi. These are ideal for residential and small commercial retrofits.

Lighting Controls

Form the second category — wired and wireless dimmers, switches, occupancy sensors, and daylight sensors. Lutron's RadioRA 3 and Caséta systems exemplify how advanced controls can automate scenes and tie into third-party platforms like Apple HomeKit and Amazon Alexa. The use of DALI (Digital Addressable Lighting Interface) for large-scale commercial projects ensures interoperability across multiple manufacturers.

Lighting Management Platforms

Are the third, fastest-growing segment. These cloud-based software systems (like those from Enlighted or Acuity Brands) aggregate data from tens of thousands of light points, enabling real-time energy monitoring, predictive maintenance, and integration with building management systems. For B2B buyers, the choice hinges on scale: small installations can use off-the-shelf Zigbee bulbs, while enterprise-grade deployments require PoE or DALI-based systems with centralized orchestration.

LED Smart Lamps and Retrofit Bulbs

Plug-and-play bulbs with integrated wireless connectivity (Zigbee, Wi-Fi, Thread). Examples: Philips Hue White Ambiance (down to 2700K–6500K CCT), IKEA TRÅDFRI (budget-friendly Zigbee option). Ideal for residential and small office retrofits.

DALI and PoE Management Systems

Centralized control architecture using digital addressable (DALI-2) or Power over Ethernet (IEEE 802.3bt) wiring. Each luminaire has a unique address, enabling granular energy metering. Acuity Brands nLight system supports 4,000+ nodes per PoE switch.

Smart Lighting Management Software Platforms

Cloud-based dashboards that aggregate sensor data from thousands of luminaires. Features include real-time occupancy heatmaps, predictive maintenance alerts, and sustainability reporting. The market is growing from $4.2B (2024) to $4.8B (2025) driven by enterprise ESG mandates.

4. Leading Players

Three dominant archetypes define the competitive landscape.

Signify (Philips Hue)

Is the clear consumer leader, leveraging its brand and ecosystem to sell over 60 million connected bulbs globally. Its strategy is to expand beyond home into hospitality and office via the Interact platform, offering granular occupancy analytics.

Lutron Electronics

Dominates the high-end controls segment with its proprietary Clear Connect RF technology and deep partnerships with luxury lighting manufacturers. Lutron's vertical integration — it produces everything from keypads to occupancy sensors — gives it reliability advantages in multi-scene environments like boardrooms and penthouses.

Acuity Brands

(parent of Lithonia Lighting and SensorWise) focuses on the commercial and industrial middle market, where its nLight platform integrates directly with building automation systems from Honeywell and Siemens. Acuity's edge is its strong distribution channel and compliance with UL 924 for emergency lighting. A fourth player,

Osram (now ams OSRAM)

Is pivoting from hardware to sensor technology, supplying integrated gesture-sensing modules and VCSEL drivers for next-generation smart luminaires. Each player is investing heavily in AI-driven predictive maintenance and energy analytics — the real battleground is not the bulb, but the data it generates.

Full-Stack Ecosystem Developer (Signify)

Controls the entire value chain from LED chips to cloud software (Interact platform). Its key competitive advantage is brand trust: 60 million Philips Hue bulbs sold globally create a massive installed base, making it the default choice for multi-room residential retrofits.

Premium Controls Specialist (Lutron Electronics)

Lutron dominates high-end commercial and luxury residential with its proprietary Clear Connect RF and wired Grafik Eye systems. Its edge is reliability — the company has designed controls for 100+ years and offers a lifetime warranty on all keypads.

Commercial IoT Integrator (Acuity Brands)

Acuity owns the nLight platform and the SensorWise brand, focusing on large-scale commercial projects. Its competitive advantage is deep integration with BMS partners (Honeywell, Siemens) and compliance with Title 24 lighting controls standards in California.

5. Market Trends

1. AI-Driven Adaptive Lighting

Artificial intelligence is enabling luminaires that learn occupant preferences and automatically adjust color temperature and intensity throughout the day. Signify has deployed AI in its Interact system for retail environments, optimizing shelf lighting based on foot traffic patterns. This reduces energy waste by 30% while increasing dwell time.

2. Matter Protocol Standardization

The Connectivity Standards Alliance's Matter protocol (launched 2022, updated 2024) aims to end fragmentation between Zigbee, Thread, and Bluetooth. Lutron and Signify both announced Matter-compatible bridges in 2025, allowing a single app to control lighting from any brand. For B2B specifiers, Matter reduces integration risk and simplifies multi-vendor procurement.

3. Power over Ethernet (PoE) for Commercial Buildings

PoE lighting delivers both power and data over a single Cat6 cable, eliminating the need for line-voltage wiring. Cisco and Acuity Brands have partnered to offer PoE-enabled LED troffers with embedded occupancy and temperature sensors. Buildings using PoE report 40% lower installation costs and 25% energy savings compared to traditional AC-powered systems.

4. Circadian Lighting in Healthcare

Research from the American Medical Association shows that tunable white lighting can reduce patient recovery time by 12%. Major hospital systems like Kaiser Permanente are now specifying Zigbee-enabled fixtures that automatically shift from 6500K (daytime) to 2700K (evening) to align with natural circadian rhythms, improving staff alertness and patient sleep quality.

6. Regional Markets

North America (Energy Code Compliance)

Stringent building codes (California Title 24, ASHRAE 90.1) mandate occupancy sensing and daylight harvesting in all new commercial construction. This pushes demand for DALI-2 and PoE systems. The U.S. market is the largest, with 35% global share.

Europe (Circadian and Data Privacy Focus)

EU directives require GDPR-compliant data handling; lighting systems that collect occupancy data must obtain explicit consent. Germany and the Nordics lead in human-centric lighting adoption, with hospitals and schools deploying tunable-white systems at scale.

Asia-Pacific (Manufacturing Hub and Smart City Driver)

China produces 60% of global LEDs and is the fastest-growing smart lighting market due to government smart-city initiatives (e.g., 5G-connected streetlights). India's Energy Efficiency Services Ltd (EESL) has deployed 300 million smart LEDs, creating a secondary market for controls.

7. Investment Outlook

Two opportunities stand out. First, the commercial retrofit market: with 70% of existing commercial buildings still using fluorescent fixtures, the replacement cycle over 2025–2030 represents a $45 billion addressable market for smart LED systems. Second, the integration of lighting with renewable energy storage — smart luminaires can now act as grid-responsive assets, dimming automatically during peak demand and earning utility rebates. However, cybersecurity risk is the primary threat. A 2024 report from Claroty found that 60% of lighting-control IoT devices had unpatched vulnerabilities, potentially exposing building management networks to ransomware. B2B buyers must mandate that suppliers adhere to IEC 62443 security standards and require firmware encryption as a baseline procurement condition.

Strategic Considerations:

- Commercial Retrofits by 2030: Replace 70% of fluorescent troffers with PoE-enabled smart LED fixtures, capturing a $45B market. Prioritize projects in NYC, London, and Shanghai where energy codes are most aggressive.

- Lighting as a Grid Asset: Smart luminaires can participate in demand-response programs; early adopters in California are earning $2–$5 per fixture annually. Source controllers with OpenADR 2.0b certification.

- Cybersecurity Vulnerabilities in IoT Nodes: 60% of lighting-control devices have unpatched flaws. Mitigation: require IEC 62443-4-1 certification and mandate over-the-air firmware encryption in procurement contracts.

- Protocol Lock-In After Matter 1.3: Matter's 2025 update may force early adopters of proprietary Thread networks to replace bridges. Future-proof by selecting Matter-certified gateways from the CSA's certified products list.

Frequently Asked Questions

Make Informed Decisions in the Smart Lighting System Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-06. All market figures are estimates and may vary from actual results.