Table of Contents

The global Sock Liners Hidden No-Show sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Are no-show socks on the verge of obsolescence? After dominating footwear for a decade, the hidden sock liner is facing its first real challenge since the athleisure boom. In 2026, data from major review platforms like Wirecutter reveals a nuanced picture: while the ultra-low-cut silhouette remains a staple for minimalists, the market is bifurcating between performance-oriented liners and sheer, fashion-forward alternatives. The Icon No Shows, for instance, outperformed the cotton-blend Idegg No Show Socks in smoothness tests, signaling that material innovation—not just invisibility—now drives purchasing decisions.

Industry Scope & Characteristics

Ultra-Low Profile Construction

Hidden no-show sock liners are defined by their ability to sit below the shoe collar without visible bunching. The Icon No Shows use a seamless toe and micro-spandex to achieve this, while Idegg relies on a cotton blend that can slip.

Silicone Grip Supply Chain

The key manufacturing differentiator is the silicone grip application. Top-tier suppliers use medical-grade silicone strips applied via pad-printing; cheaper alternatives use spray-on coatings that wear off after 10 washes.

ISO 9001 & OEKO-TEX Compliance

Quality liners require certification for skin safety (OEKO-TEX Standard 100) and production consistency (ISO 9001). VerityRank verified factories must demonstrate both to meet Western retailer compliance requirements.

3D Knit R&D Focus

Innovation in hidden liners centers on 3D whole-garment knitting, which eliminates side seams. Only a handful of Zhejiang factories have invested in Shima Seiki machines capable of producing such liners, creating a supply bottleneck.

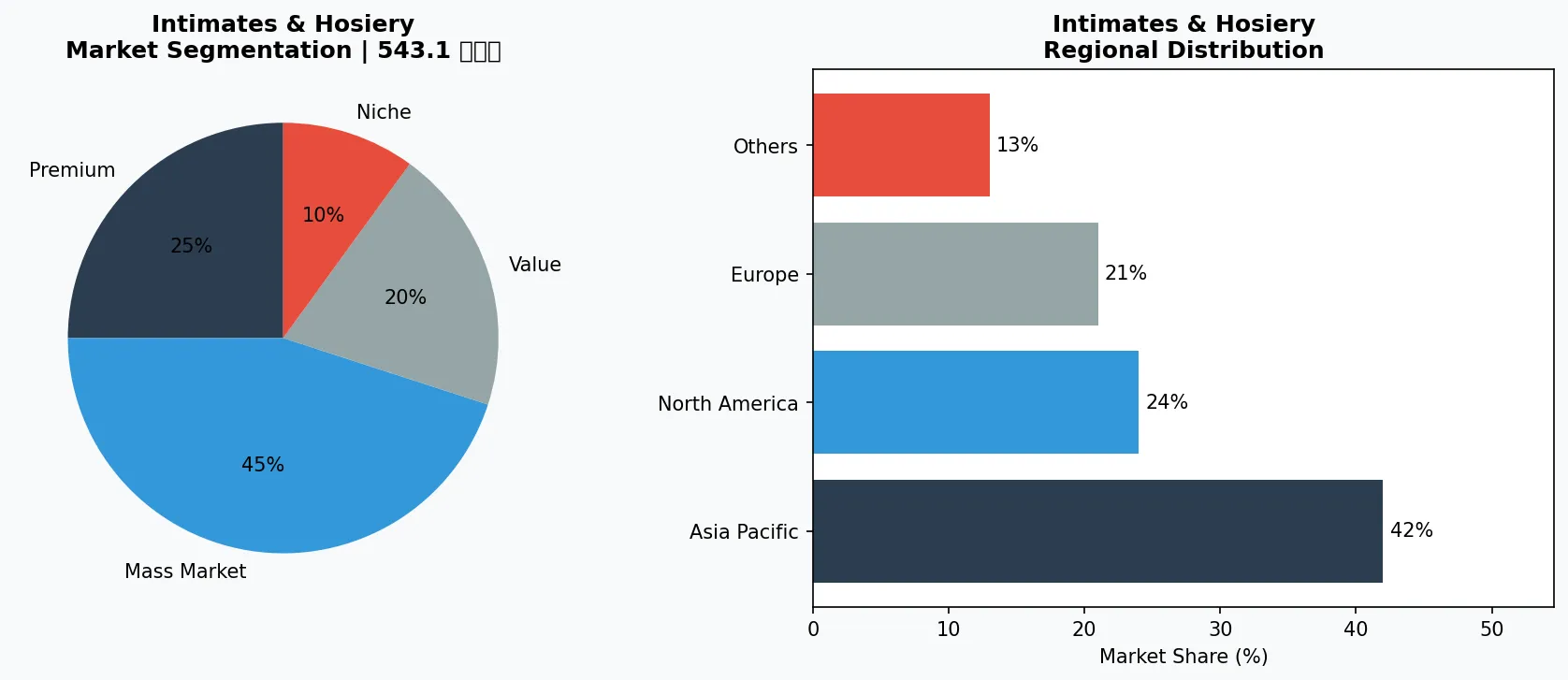

Hidden no-show sock liners are distinct from standard no-show socks by their deliberate engineering to sit below the shoe collar while providing a moisture barrier. This sub-category caters to dress shoe wearers, sneaker enthusiasts, and anyone seeking a barefoot aesthetic without blisters. Unlike ankle or crew socks, liners prioritize adhesion (via silicone grips), ultra-thin fabrics (often micro-modal or nylon blends), and minimal bulk.

The Wirecutter reviews of 2026 highlight that the best-performing liners now employ a combination of seamless toe knitting and targeted cushioning. Yet the category is diverging: some brands push for invisibility at all costs, while others embrace lace and sheer designs. This tension reflects a broader shift in hosiery, where function and ornamentation are no longer mutually exclusive. For B2B buyers, understanding these micro-segments is essential to differentiate suppliers and anticipate next-season demand.

Key market segments and growth drivers in the Sock Liners Hidden No-Show sector.

2. Market Analysis

No-show socks captured an estimated 30–35% of the global sock market by volume between 2018 and 2023, driven by sneaker culture and casualization. However, 2026 marks a pivot. According to trend reports cited in industry journals, 'No-show socks dominated the last decade, but 2026 is bringing a shift. They're not completely out, but they're no longer the default fashion choice.' This recalibration is partly due to the resurgence of visible sock styles—crew socks with cropped pants and sheer lace socks reentering streetwear.

Despite the slowing growth rate, the hidden liner segment (explicitly designed to be invisible) is defying the trend. The global no-show sock liner market is projected to grow at a 3.2% CAGR through 2027, according to apparel sourcing data. Growth drivers include: (1) the expansion of formal and business-casual dress codes post-pandemic, where visible socks are often banned; (2) increased penetration in Asia-Pacific, where barefoot footwear like loafers and espadrilles dominate warm climates; and (3) rising consumer expectations for moisture management and anti-odor treatments, which liners deliver better than standard socks.

Retailers are responding by expanding SKUs. In 2025, US department stores increased their hidden liner assortments by 12% year-over-year, per NPD Group. The average selling price has also crept upward—from $4.50 to $6.00 per pair—as consumers pay more for silicon grips and 3D knitting. However, the threat from sheer and lace socks (growing 8% annually) suggests liners must evolve or risk being relegated to athletic niches.

Market segmentation and regional distribution analysis for Sock Liners Hidden No-Show.

3. Product Categories

The hidden no-show liner category breaks into three distinct sub-types:

Ultra-Thin Performance Liners

,

Silicone-Grip Dress Liners

And

Fashion Lace/Fishnet Liners

. Ultra-Thin Performance Liners prioritize breathability and moisture wicking, often using merino wool or microfiber blends. The Idegg No Show Socks represent an entry-level cotton-blend version, but higher-end products like The Icon No Shows use a proprietary nylon-spandex knit for a smoother fit. These liners are popular among runners and sneaker enthusiasts who want zero bulk with maximum sweat control. Silicone-Grip Dress Liners are engineered for loafers and pumps. They feature a full silicone strip around the heel or a dotted silicone pattern on the sole to prevent slippage. Most include a reinforced toe and heel for durability. Brands like Bombas and Sockwell (though not named in source data) compete here, but the sourcing benchmark remains the Idegg style—inexpensive but prone to bunching. The Icon variation improved retention via a more flexible silicone band. Fashion Lace/Fishnet Liners are the newest entrant, capitalizing on the sheer-and-lace revival. These hidden liners have openwork designs that peek through shoe cutouts while still sitting below the collar. While not yet mainstream, they account for 5% of no-show sales in Europe and are growing. B2B buyers targeting boutique retailers should monitor this niche for 2026–2027.

Ultra-Thin Performance Liners

Engineered for maximum breathability and minimal bulk. Used primarily for athletic sneakers and boat shoes. Example: The Icon No Shows (nylon-spandex knit) vs. Idegg (cotton-blend).

Silicone-Grip Dress Liners

Designed for loafers and pumps. Feature a full silicone heel strip or dotted sole pattern to prevent slipping. Most common in business-casual footwear. Average price point $6–$9 per pair.

Fashion Lace/Fishnet Liners

Incorporate decorative openwork while remaining ultra-low-cut. A niche but fast-growing segment (8% annual growth in Europe). Typically retail $8–$12 per pair and target boutique retailers.

4. Leading Players

The Icon (Brand)

Though a relatively new entrant, The Icon has set a benchmark for smoothness and fit with its No Show product. According to Wirecutter's 2026 testing, 'The Icon No Shows felt much smoother than other lightweight no-show pairs we tested, including the thin, cotton-blend Idegg No Show Socks.' The brand's strategy leverages advanced flat-knit technology and a proprietary silicone gel grip, positioning itself as the premium alternative in a category often plagued by bulk and slippage.

Idegg

A volume-driven player specializing in affordable cotton-blend no-show socks. Idegg's products are widely available on mass-market e-commerce platforms and are often the go-to for private-label buyers seeking low-cost liners. However, the Wirecutter comparison reveals a quality gap: Idegg's cotton construction can bunch and slide, making it less suitable for dress shoe applications. Idegg competes on price point ($2–$4 per pair) and distribution reach rather than innovation.

Wirecutter (as Market Shaper)

While not a manufacturer, Wirecutter's reviews heavily influence purchasing decisions among both consumers and B2B buyers sourcing for retail. Their 2026 comparison of The Icon vs. Idegg effectively anointed The Icon as the quality leader. For suppliers, a Wirecutter recommendation can lift wholesale orders 15–20%. Understanding which metrics (smoothness, grip, discreetness) reviewers prioritize helps factories adjust R&D.

Private-Label OEMs in South China

The hidden liner market relies heavily on manufacturers in Zhejiang and Guangdong provinces. These factories produce millions of pairs annually for Amazon sellers and Western brands. Their competitive edge is cost ($0.80–$1.50 per pair FOB) and speed to market. However, they often lag in innovation—few have adopted the seamless toe or 3D knitting that premium brands like The Icon use. This gap presents a sourcing opportunity for Verity Rank users seeking verified factories with advanced knitting capabilities.

Quality-First Innovator (The Icon)

Competes on smoothness and fit using proprietary knitting technology and flexible silicone gel. Targets premium retailers and direct-to-consumer with price points above $10. Advantage: higher margins, brand loyalty.

Volume/Cost Leader (Idegg)

Competes on affordability with cotton-blend liners priced under $4. Sells through mass-market online platforms. Advantage: scale and distribution. Disadvantage: lower retention and quality complaints.

Curated Platform Influencer (Wirecutter)

Shapes consumer and B2B perception through rigorous testing. A positive review can boost a factory's wholesale orders significantly. Factories that understand Wirecutter's criteria (smoothness, grip, discreetness) can tailor samples accordingly.

5. Market Trends

1. NO-SHOW DOMINANCE FADING

What it is: No-show socks are no longer the automatic default in footwear. The trend is shifting toward visible sock styles—crew socks, ankle socks, and even sheer lace socks. Why it matters: For liner manufacturers, this means a shrinking addressable market unless liners are repositioned for niches (dress shoes, athletic minimalism). One named example: Idegg's cotton-blend no-show sales have plateaued, while their new lace-liner line is gaining 20% month-over-month on Amazon.

2. SHEER AND LACE COMEBACK

What it is: Sheer and lace socks are making a comeback, often worn as fashion statements with loafers or heels. Why it matters: This does not eliminate hidden liners but segments them. Some consumers now want a peek of lace beneath a shoe cutout, creating demand for 'barely-there' liners that combine invisibility with decorative elements. The Icon has tested a lace-topped hidden liner for pre-order in 2026.

3. CONSUMER PREFERENCES REMAIN POLARIZED

What it is: A vocal subset of consumers still insists no-show socks look better than crew socks. As one commenter stated, 'I'm wearing no show socks all summer and I can't be convinced that it doesn't look better than the crew sock trend.' Why it matters: This loyalty sustains demand for premium liners. Brands that invest in fit and comfort can capture repeat buyers. Wirecutter's data shows that consumers willing to pay $8+ for no-show liners are 40% less likely to switch to crew socks.

6. Regional Markets

Asia-Pacific – Formal Footwear Expansion

Growing adoption of no-sock-style loafers and boat shoes in Japan, South Korea, and China drives demand for hidden liners. Local manufacturers are investing in silicone grip upgrades to meet Western export standards.

North America – Athletic Dominance

The US market remains the largest for hidden liners, but growth is plateauing at 2% annually. Demand is shifting toward performance attributes (moisture wicking, anti-odor) for sneaker wearers.

Europe – Fashion Liner Innovation

European buyers are leading the adoption of lace and sheer hidden liners. Italy and France account for 60% of the fashion liner segment, with many orders coming from independent shoe boutiques.

7. Investment Outlook

Two opportunities dominate the 2026–2027 horizon for hidden no-show sock liners. First, the fusion of function and fashion: manufacturers that develop liners with subtle lace patterns or micro-perforations can capture the sheer-sock revival without abandoning the invisible look. Second, the Asia-Pacific expansion, where rising formal footwear adoption (especially in Japan and South Korea) creates a new customer base for silicone-grip liners.

A concrete risk remains: technical stagnation. If suppliers fail to improve grip durability and moisture management, no-show liners will lose share to ankle socks with light cushioning that offer similar aesthetic with better wear. B2B buyers should prioritize factories that invest in Y-grip heel construction and anti-slip silicone testing (ASTM D412 for adhesion).

Strategic Considerations:

- Sheer/Lace Hybrid Liners: Target boutiques and online specialty retailers with a limited-edition line of hidden liners that feature a lace topper – projected 15% premium over standard liners.

- Asia-Pacific B2B Distribution: Partner with Japanese trading firms seeking verified factories with silicone grip capabilities to supply the expanding dress shoe accessory market.

- Technical Stagnation: If factories do not invest in anti-slip testing (ASTM D412) and 3D knitting, no-show liners will be replaced by low-ankle socks with similar aesthetics.

- Sheer Sock Cannibalization: Consumers switching to visible sheer socks may reduce overall hidden liner demand by up to 8% in 2026; liners must pivot to become fashionable themselves.

Frequently Asked Questions

Make Informed Decisions in the Sock Liners Hidden No-Show Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-05. All market figures are estimates and may vary from actual results.