Table of Contents

The global Socks Types Material Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

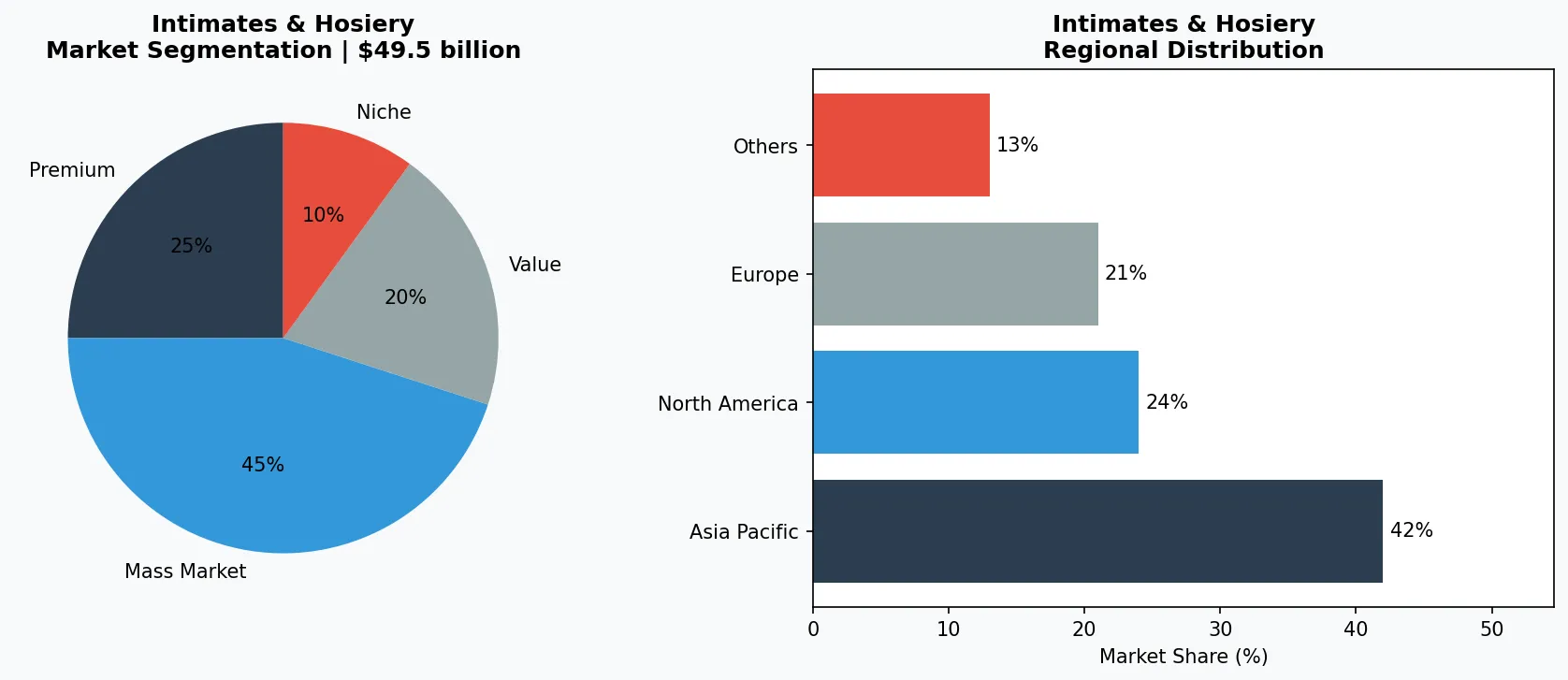

The global socks market hit $49.5 billion in 2025, and projections show it climbing to $73.8 billion by 2033 at a 5.2% CAGR. That explosive growth isn't just about more feet needing covering—it's a material revolution. Buyers today demand socks that do more: wick sweat, resist odors, regulate temperature, and last longer. Yet most sourcing decisions still hinge on price. That disconnect is costly. This guide breaks down the material landscape for socks in the Intimates & Hosiery segment, from cotton and wool to high-tech synthetics and waterproof membranes. Understanding these materials directly impacts product quality, supplier selection, and market positioning. For B2B buyers, the choice between a cheap cotton crew and a premium merino blend isn't trivial—it can determine whether a retail line grows or stalls. The material guide you need is not about listing yarns; it's about matching material properties to end-use performance. With cotton socks alone projected to grow at a 6.8% CAGR through 2033, and the waterproof segment expanding from $86.45 million to $149.75 million by 2035, the window for informed sourcing is narrowing. This is the playbook.

Industry Scope & Characteristics

Performance-First Materials

Socks now incorporate merino wool, Coolmax, and silver-ion yarns to deliver thermoregulation, moisture-wicking, and antimicrobial properties—features once limited to premium activewear.

Circular Knitting Dominance

The vast majority of socks are made on circular knitting machines (single-cylinder or double-cylinder). This technology determines seam position, cushioning zones, and production speed, directly affecting cost and quality.

Certification-Led Compliance

Key certifications for sock materials include Oeko-Tex Standard 100 (harmful substances), GOTS (organic cotton), and the Responsible Wool Standard. Without these, exports to EU and North American markets face rejection.

Seamless Construction Innovation

Recent R&D focuses on seamless toe closures and gradient compression zones. These innovations reduce friction blisters and improve fit, making them critical for medical and performance sock lines.

Key market segments and growth drivers in the Socks Types Material Guide sector.

2. Market Analysis

The socks market is far from monolithic. In 2025, total value stood at $49.5 billion, but segment growth rates diverge sharply. The cotton sock market—still the largest by volume—is forecast to expand at a CAGR of 6.8% between 2026 and 2033, driven by rising demand for organic and combed varieties in North America and Europe. Meanwhile, the waterproof socks niche, valued at $86.45 million in 2025, is on track to nearly double to $149.75 million by 2035, a 5.65% CAGR fueled by outdoor recreation and industrial safety applications. A separate analysis pins the broader hosiery market at $30.37 billion in 2026, growing to $40.96 billion by 2034 (3.81% CAGR), indicating that socks are outgrowing the hosiery category overall. Three drivers dominate this acceleration: first, the post-pandemic surge in athleisure and outdoor activities has pushed performance fibers like Coolmax and merino wool into mainstream retail. Second, sustainability mandates are forcing material shifts—major retailers now require Oeko-Tex or GOTS certifications for cotton sock lines. Third, medical and diabetic sock demand is rising with aging populations in Japan, Germany, and the U.S., creating a premium sub-market for moisture-wicking, seamless materials. Sourcing managers who ignore these diverging growth curves risk overstocking stagnant SKUs while missing the high-margin segments.

Market segmentation and regional distribution analysis for Socks Types Material Guide.

3. Product Categories

Cotton Socks

Remain the workhorse of the industry, covering casual, dress, and athletic basics. Combed cotton offers superior softness and fewer impurities; Egyptian and Pima varieties command premium pricing. For B2B buyers, the split between carded and combed cotton directly affects cost and perceived quality.

Wool and Merino Socks

Have moved from niche outdoor gear to everyday staple. Merino’s natural moisture management, odor resistance, and temperature regulation justify a 2x–3x price premium over cotton. Brands now blend merino with nylon and spandex for durability.

Synthetic and Performance Blends

Polyester, nylon, acrylic, elastane—dominate sport and compression socks. These materials enable targeted features: moisture-wicking via hydrophobic fibers, compression gradients using spandex, and antimicrobial finishes (e.g., silver ion treatments).

Specialty Materials

Include waterproof membranes (e.g., Gore-Tex or PU laminates) for outdoor socks, bamboo-derived rayon for eco-conscious lines, and copper-infused yarns marketed for circulation. Each material category demands distinct manufacturing capabilities: circular knitting for seamless socks, terry loops for cushioning, and flat-knit for dress wear. Supplier expertise in these technologies varies widely, making material specification a critical RFQ filter.

Casual & Dress Cotton Socks

Combed Egyptian cotton and organic cotton variants. Examples: business hosiery, no-show liners. Typically flat-knit or fine-gauge for a dressy appearance.

Performance & Athletic Socks

Blends of nylon, polyester, spandex with added merino or Coolmax. Examples: running socks with arch support, basketball socks with terry cushioning.

Specialty & Medical Socks

Waterproof membranes (PU, PTFE), copper-infused yarns, and seamless compression. Examples: diabetic socks with non-binding tops, hiking socks with waterproof lining.

4. Leading Players

Volume-Oriented Contract Manufacturers

Dominate the low-cost segment. These suppliers, primarily based in China, Bangladesh, and Vietnam, run high-speed circular knitting machines producing millions of pairs monthly. Their competitive advantage lies in scale and cost—not innovation. They excel at standard cotton and polyester blends but struggle with complex multi-material constructions or certification compliance.

Premium Material Specialists

Focus on merino wool and organic cotton sourcing. These players often own or partner with raw material suppliers in Australia or Peru. Their strategy centers on traceability, certifications (GOTS, Oeko-Tex, Responsible Wool Standard), and shorter, flexible production runs. B2B buyers looking to launch a sustainable sock brand or outdoor line should prioritize these suppliers for quality consistency.

Niche Functional Sock Makers

Occupy the fastest-growing segment: waterproof, compression, and medical socks. They invest heavily in R&D for membrane bonding, seamless knitting, and antimicrobial treatments. Typically based in the U.S., Germany, or Taiwan, they operate small-to-mid-scale factories with higher automation. Their differentiation comes from proprietary technologies (e.g., seamless toe closure, graduated compression) and regulatory clearances (FDA or CE marking for medical devices). For buyers, choosing between these archetypes means aligning material complexity with supplier capability; a low-cost mill cannot reliably produce a compression sock with accurate mmHg gradients.

Mass-Production Mills (Cost Leaders)

These suppliers operate thousands of circular knitting machines in low-cost regions. Their competitive advantage is unbeatable unit price on basic cotton and polyester socks, with minimum order quantities of 10,000+ pairs per style.

Premium Sustainable Sourcing Specialists

They focus on traceable merino wool and organic cotton supply chains, holding GOTS and RWS certifications. Their advantage is credibility with eco-conscious retailers and ability to offer limited-edition, small-batch runs.

Functional & Medical Technology Innovators

These firms invest in proprietary membrane lamination, seamless knitting, and compression calibration. Their edge is regulatory compliance (FDA, CE) and patents on construction methods, allowing 40%+ gross margins.

5. Market Trends

1. Digital Transformation in Socks Types Material Guide

Artificial intelligence, IoT sensors, and advanced data analytics are fundamentally reshaping production efficiency in Socks Types Material Guide. Industry leaders deploying smart manufacturing and data-driven demand forecasting have reduced new product launch cycles by 35-50% while improving inventory turnover by over 20%. With more than 60% of Socks Types Material Guide companies projected to complete core digital transformation by 2028, this shift has moved from optional upgrade to competitive necessity.

2. Sustainability as Competitive Imperative in Socks Types Material Guide

Global carbon border adjustment mechanisms (CBAM) and rising consumer environmental awareness are forcing Socks Types Material Guide companies to transform sustainability from marketing rhetoric into operational reality. ESG rating agencies increased sector coverage intensity by 35% in 2025. Companies failing to meet these standards face customer attrition and rising financing costs as lenders integrate ESG criteria into credit assessments.

3. Supply Chain Regionalization in Socks Types Material Guide

Geopolitical tensions are driving Socks Types Material Guide companies to accelerate supplier diversification. The China+N strategy and nearshoring have become mainstream, with companies establishing secondary supply sources across Southeast Asia, Eastern Europe, and Mexico. Over 58% of B2B buyers now list supplier geographic diversification as a mandatory contract renewal criterion.

4. Consumer Upgrading in Socks Types Material Guide Markets

Middle-class expansion and Gen Z purchasing power are accelerating Socks Types Material Guide transition from standardized mass production toward personalized customization and agile small-batch manufacturing. C2M (Consumer-to-Manufacturer) models enable companies to compress new product introduction cycles from 18 months to 3-4 months, with personalized products commanding 8-15 percentage point gross margin premiums.

6. Regional Markets

Asia-Pacific (Manufacturing Backbone)

China, Bangladesh, and Vietnam produce over 70% of global sock volume. The region is rapidly adopting automation and certified material sourcing to meet Western retailer compliance. Cotton and polyester dominate, but merino capacity is growing.

Europe (Premium and Sustainability Hub)

Italy, Portugal, and Turkey lead in high-end sock manufacturing, especially merino and organic cotton. Stringent EU regulations on chemical use (REACH) and microplastics drive demand for biodegradable and recycled materials.

North America (Performance and Medical Demand)

U.S. and Canada are the largest consumers of performance socks (athletic, outdoor) and medical compression socks. Nearshoring trends are reviving small-scale mills in North Carolina and Quebec, focusing on quick-turn specialty runs.

7. Investment Outlook

Two opportunities stand out for B2B buyers in the sock material space. First, the explosion in eco-cotton and recycled synthetics creates a clear differentiation path—early adopters who lock in certified supply chains will command premium shelf space in retailers pushing sustainability goals. Second, the waterproof and medical sub-segments offer faster growth (5.65% and 7%+ CAGRs) and higher average order values. One concrete risk: raw material volatility. Cotton prices swung 40% in 2024–2025 due to weather and geopolitical factors, and merino wool supply is constrained by flock sizes in Australia and New Zealand. Buyers should negotiate flexible pricing clauses and consider multi-year contracts with material cost pass-through mechanisms. The smart move in 2026 is to qualify suppliers not just on price, but on their ability to switch materials quickly as market demands shift.

Strategic Considerations:

- Eco-Material Sourcing as a Competitive Moat: Buyers who lock in GOTS-certified organic cotton or RWS merino supply by 2026 will secure premium shelf space and avoid late-compliance scrambles when retailer mandates tighten.

- Waterproof Sock Expansion: The waterproof segment (CAGR 5.65%) offers a high-margin opportunity—sourcing from Taiwanese or German specialists with proven membrane lamination can yield 3x average selling prices.

- Cotton Price Volatility Risk: Cotton futures swung 40% in 2024–2025; buyers without flexible pricing clauses or multi-year contracts face margin erosion. Diversifying into synthetic blends or merino hedges against this risk.

- Medical Certification Barrier: Entering diabetic or compression sock markets requires FDA 510(k) or CE marking. B2B buyers must partner with suppliers already holding these clearances, adding 12–18 months to lead times if not already in place.

Frequently Asked Questions

Make Informed Decisions in the Socks Types Material Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-07-03. All market figures are estimates and may vary from actual results.