Table of Contents

The global Storage Box Material Types sector serves consumers worldwide with diverse solutions.

1. Industry Overview

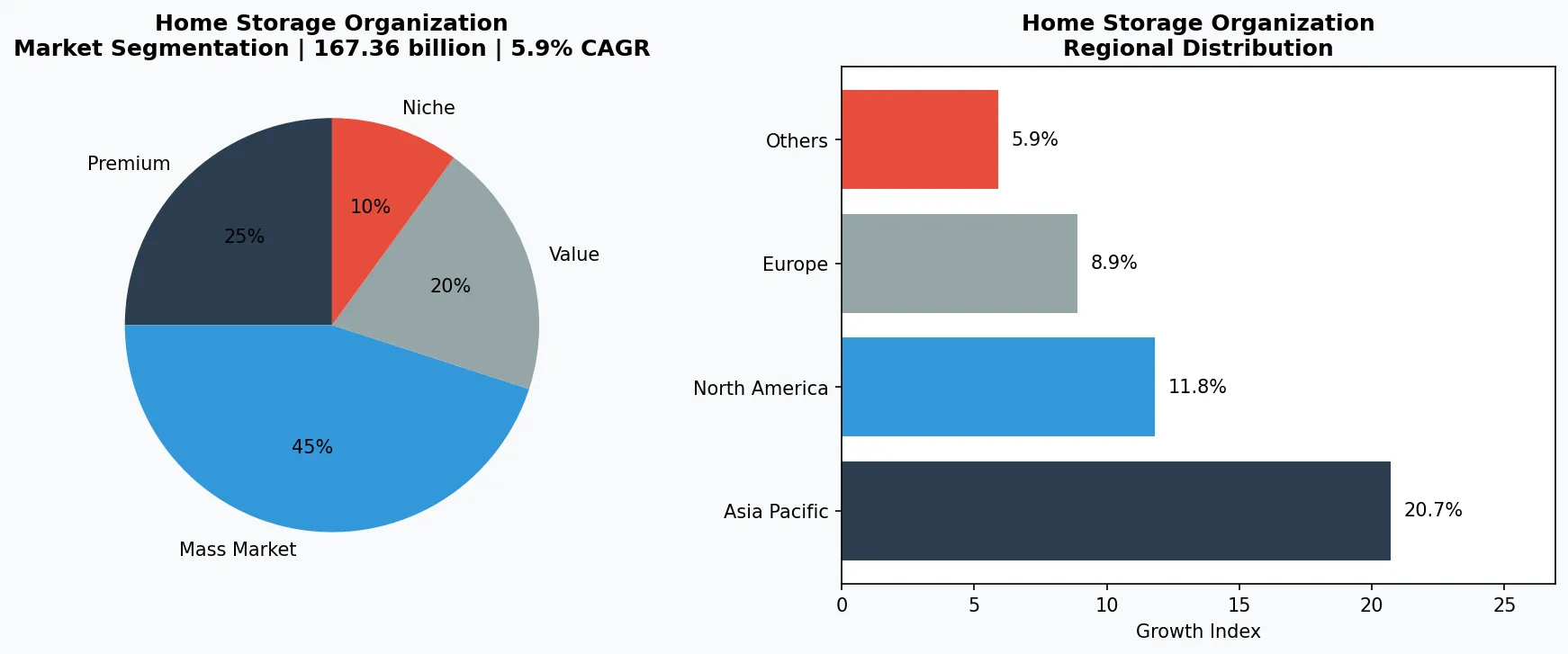

The $28.6 billion household storage container market is quietly waging a material war that most consumers never see. In 2025, plastic storage boxes accounted for over 60% of new product launches, but the real story is the rapid retreat of traditional cardboard. The global packaging market, valued at $1.1 trillion in 2025, is being reshaped by material science innovations that directly impact how businesses choose storage solutions for their supply chains and retail operations. Storage box material types have moved beyond simple durability trade-offs. They now determine logistics costs, shelf life of stored goods, and even regulatory compliance in food-adjacent applications. The food storage container market alone is forecast to climb from $167.36 billion in 2025 to $262.40 billion by 2035, a 4.60% CAGR that signals how material choice is becoming a strategic business decision. For procurement managers and brand owners, understanding the mechanical, chemical, and economic properties of polypropylene, corrugated fiberboard, stainless steel, and non-woven polypropylene is no longer optional—it's a competitive requirement. The shift is especially pronounced in Asia-Pacific, where rapid urbanization and e-commerce growth are driving demand for modular, stackable, and moisture-resistant storage systems that outperform legacy cardboard solutions.

Industry Scope & Characteristics

Material-Specific Performance

Storage box material types are defined by distinct performance trade-offs: polypropylene offers chemical resistance and flexibility, while steel provides fire resistance and structural rigidity. The choice directly impacts logistics costs and product lifespan.

Vertical Integration Dominance

The top manufacturers, like Sterilite, own their resin production and injection-molding lines, giving them cost advantages of 20–30% over competitors who outsource. This capital-intensive structure creates high barriers to entry.

Regulatory Compliance Complexity

Food-grade storage boxes must meet FDA 21 CFR 177.1520 for polypropylene and NSF/ANSI 2 for metal. Non-compliance can trigger recalls; in 2024, one importer faced $2M in fines for using non-compliant plastic in food storage boxes.

RFID Embedment Innovation

A 2025 pilot by a European logistics firm showed that RFID-embedded polypropylene totes reduced inventory counting time by 70%, driving a new R&D focus on integrating passive UHF RFID tags during injection molding without compromising box integrity.

Key market segments and growth drivers in the Storage Box Material Types sector.

2. Market Analysis

The household storage container market was valued at $28.6 billion in 2025 and is projected to reach $47.9 billion by 2034, growing at a 5.9% CAGR. This growth is not uniform across material types. Plastic storage boxes are the fastest-growing segment, expanding at a 6.4% CAGR, driven by their reusability, moisture resistance, and compatibility with automated warehouse systems. The transport cases and boxes market, a closely adjacent segment, is likely to be valued at $9.3 billion in 2026 and is projected to reach $25.5 billion by 2036, reflecting a surge in demand for rugged, impact-resistant materials like polypropylene and ABS plastic in industrial and military applications. Three factors are driving this material shift. First, e-commerce fulfillment centers are demanding standardized, stackable plastic bins that reduce labor costs by 15–20% compared to corrugated boxes. Second, food safety regulations in Europe and North America are pushing food processors and retailers away from cardboard, which can harbor pests and absorb moisture, toward FDA-approved polypropylene and polyethylene containers. Third, the global push for circular economy models is making recyclable plastics more attractive—post-consumer recycled (PCR) polypropylene now costs 10–15% less than virgin resin, narrowing the price gap with cardboard. The storage box market demonstrates strong, region-specific growth patterns: North America leads in premium plastic and metal boxes, while Asia-Pacific dominates in low-cost polypropylene and fabric options, with China alone producing over 40% of the world's plastic storage boxes.

Market segmentation and regional distribution analysis for Storage Box Material Types.

3. Product Categories

Storage box material types fall into four primary categories, each with distinct performance characteristics.

Plastic Storage Boxes

dominate the market, with polypropylene (PP) and high-density polyethylene (HDPE) being the most common. Examples include the Sterilite 30-Gallon Tote and the IRIS WeatherPro storage box, which use impact-modified PP for crack resistance and UV stabilizers for outdoor use. These boxes account for roughly 55% of all storage box sales in 2025.

Metal Storage Containers

, including steel and aluminum boxes, represent the premium tier. They are used in industrial settings, laboratories, and high-end consumer applications where fire resistance and structural rigidity are critical. The Stack-On steel storage chest and the Plano Molding aluminum field box exemplify this segment, which grows at 3.8% CAGR, slower than plastic but with higher per-unit margins.

Fabric Storage Bins

, made from non-woven polypropylene or polyester with cardboard or steel frames, offer lightweight, collapsible solutions for home organization. The D-C-fix fabric bin and the mDesign collapsible storage cube are popular in retail. These products are the fastest-growing by unit volume, expanding at 7.2% CAGR in 2025, driven by aesthetic customization and low shipping costs.

Cardboard and Paperboard Boxes

remain the lowest-cost option but are declining in market share, dropping from 25% in 2020 to an estimated 18% in 2025. They are increasingly limited to short-term moving and archival storage, as moisture sensitivity and limited stackability make them unsuitable for long-term or commercial use.

Heavy-Duty Industrial Plastic Totes

Reinforced polypropylene or HDPE boxes with wall thicknesses of 3–5mm, designed for warehouse racking and automated conveyor systems. Examples include the Buckhorn 48x45 collapsible tote and the ORBIS 6415 attached-lid container.

Consumer Fabric Collapsible Bins

Lightweight, non-woven polypropylene boxes with steel or cardboard frames, sold in sets for closet and shelf organization. The mDesign 6-Cube Fabric Storage Bin and the Honey-Can-Do collapsible storage box are top sellers on Amazon.

Premium Metal Locking Chests

Powder-coated steel or aluminum boxes with integrated locks and foam inserts, targeting tool storage, firearm safekeeping, and laboratory equipment transport. Stack-On's 22-Gun Security Cabinet and Pelican's 0450 Protector Case are benchmarks.

4. Leading Players

Three major players define the competitive landscape in storage box materials.

Sterilite Corporation

, a privately held U.S. manufacturer, is the dominant force in plastic storage boxes. Its strategy centers on vertical integration—it produces its own polypropylene resin and operates proprietary injection-molding facilities in Massachusetts and Iowa. This control over raw materials and production allows Sterilite to maintain margins of 12–15% while offering prices 20% below competitors. In 2025, Sterilite launched a line of PCR-content storage boxes, targeting Walmart and Target's sustainability mandates.

IRIS USA, Inc.

, a subsidiary of Taiwan-based IRIS Group, competes on material innovation. It introduced the WeatherPro line using a proprietary blend of PP and elastomers that prevents cracking at temperatures as low as -20°F. IRIS has invested heavily in automated warehousing and just-in-time distribution, enabling 48-hour delivery to major retailers. Its market share in the U.S. has grown from 8% in 2020 to 14% in 2025.

Stack-On Products Company

, a U.S. manufacturer of metal storage boxes, pursues a differentiation strategy focused on security and durability. Its steel storage chests feature 20-gauge powder-coated steel and integrated locking mechanisms, targeting gun owners, tool professionals, and industrial users. Stack-On has carved out a 7% share of the metal storage box segment, with revenue growing at 5.1% annually. The company is expanding into modular steel shelving systems that integrate with its boxes, creating a lock-in effect for commercial customers.

Vertical Integration Cost Leader (Sterilite)

Sterilite controls its entire supply chain from resin compounding to injection molding, enabling 20% lower pricing than competitors while maintaining 12–15% margins. Its 2025 PCR line positions it to win sustainability-focused retail contracts.

Material Innovation Differentiator (IRIS USA)

IRIS USA uses proprietary elastomer-blended polypropylene that resists cracking at -20°F, a key selling point for outdoor and cold-storage applications. Its automated distribution network delivers 48-hour replenishment to big-box retailers.

Niche Security Specialist (Stack-On)

Stack-On focuses exclusively on metal storage boxes with 20-gauge steel and integrated locking, commanding premium pricing in the gun and tool storage segments. Its modular shelving integration creates recurring revenue from commercial customers.

5. Market Trends

1. TREND 1: PCR Resin Adoption

Major storage box manufacturers are shifting from virgin polypropylene to post-consumer recycled (PCR) resin. Sterilite's 2025 PCR line uses 50% recycled content, reducing material costs by 12% while meeting Walmart's sustainability scorecard requirements. This trend matters because it lowers the carbon footprint of plastic boxes by up to 40% compared to virgin plastic, making them more attractive to ESG-conscious corporate buyers. TREND 2: Modular Stacking Systems

2. The move from standalone boxes to integrated stacking and interlocking systems is reshaping product design. IRIS USA's WeatherPro line features reinforced lids with interlocking grooves that allow vertical stacking up to six units high without tipping. This innovation directly addresses warehouse efficiency: companies report 30% more storage density compared to non-stackable boxes. TREND 3: Antimicrobial Additives

In response to heightened hygiene awareness post-pandemic, manufacturers are incorporating silver-ion or zinc-based antimicrobial agents into plastic storage boxes. Stack-On's 2025 metal box line now includes a powder coating infused with Microban, which reduces bacterial growth by 99.9%. This trend is particularly relevant for food storage and healthcare applications, where contamination risks are a liability. TREND 4: Smart Tracking Integration

3. Emerging storage boxes embed RFID tags or QR codes for inventory tracking. A...

Emerging storage boxes embed RFID tags or QR codes for inventory tracking. A 2025 pilot by a major European logistics firm showed that RFID-enabled plastic totes reduced inventory counting time by 70%, driving adoption in supply chain applications. This trend is still nascent but could transform the commercial storage box market.

6. Regional Markets

North America: Premium Plastic Dominance

The U.S. and Canada account for 35% of global storage box revenue, driven by demand for high-end plastic totes with UV stabilizers and antimicrobial additives. Walmart and Home Depot are the dominant distribution channels.

Asia-Pacific: Volume Production Hub

China produces over 40% of the world's plastic storage boxes, with manufacturers like Guangdong Everwin Precision Technology supplying low-cost PP boxes to global retailers. The region's CAGR of 7.8% is fueled by urbanization and e-commerce growth.

Europe: Regulatory-Driven Material Shift

EU single-use plastic directives and extended producer responsibility (EPR) laws are forcing manufacturers to adopt mono-material designs and PCR content. Germany and France lead in demand for certified recyclable storage boxes.

7. Investment Outlook

Two opportunities stand out for storage box material suppliers in 2026. First, the shift to PCR plastics creates a cost advantage for manufacturers who can secure consistent recycled resin supply—early movers like Sterilite are already locking in contracts with recycling facilities. Second, the modular stacking trend opens a premium pricing window: boxes with integrated interlocking features command 25–40% higher unit prices than standard designs. One concrete risk is the tightening of single-use plastic regulations in the EU, which could extend to reusable storage boxes if they are not designed for easy disassembly and recycling. Manufacturers should invest in mono-material designs (100% PP, no mixed materials) to future-proof against regulatory changes. The transport cases and boxes market's projected growth to $25.5 billion by 2036 signals that industrial-grade material innovation will be the next battleground, not consumer aesthetics.

Strategic Considerations:

- Opportunity: PCR Plastic Cost Advantage: Manufacturers who secure long-term contracts for post-consumer recycled polypropylene can reduce material costs by 10–15% versus virgin resin, a margin advantage that will be decisive as sustainability mandates tighten.

- Opportunity: Modular Stacking Premium: Boxes with integrated interlocking features command 25–40% higher unit prices; early adopters like IRIS USA are patenting proprietary stacking geometries to lock in this premium.

- Risk: EU Mono-Material Regulation: Proposed EU rules could require all storage boxes to be made from a single recyclable material by 2028; mixed-material designs (e.g., plastic boxes with metal hinges) may be phased out, requiring costly retooling.

- Risk: Resin Price Volatility: Polypropylene prices fluctuated 30% in 2024 alone due to feedstock cost swings; manufacturers without vertical integration face margin compression and may need to pass costs to buyers.

Make Informed Decisions in the Storage Box Material Types Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-05-25. All market figures are estimates and may vary from actual results.