Table of Contents

The global Sunglasses Eye Glasses Guide sector serves consumers worldwide with diverse solutions.

1. Industry Overview

The global eyewear market hit $125.4 billion in 2022, but the real story is the 12% year-over-year surge in sunglasses sales in 2025 alone. Within the Fashion Accessories industry, sunglasses and eyeglasses occupy a unique intersection—they are simultaneously medical devices, fashion statements, and status symbols. Unlike watches or belts, eyewear carries a functional necessity that amplifies its market stickiness. The fashion luxury segment, growing at 18%, has turned frames into the fastest-moving accessory category on retail shelves.

Industry Scope & Characteristics

Dual Functionality

Sunglasses and eyeglasses uniquely combine medical necessity with fashion expression. Products like photochromic lenses adapt to indoor/outdoor use, blurring the line between prescription and sunwear.

Material-Driven Supply Chain

Frame manufacturing relies on specialized materials such as cellulose acetate, titanium, and memory metal. Sourcing requires tight tolerances for thickness and flex, often certified under ISO 12870 for ophthalmic optics.

Optical Quality Standards

Lenses must comply with ANSI Z80.3 (US) or EN 1836 (EU) for impact resistance and UV protection. Retailers require test reports for each stock-keeping unit, making verifiable certification a non-negotiable for B2B transactions.

Smart Integration Innovation

2026's R&D focus is embedding sensors and Bluetooth modules into temple arms without adding bulk. Companies are developing ultra-thin conductive filaments that can be molded directly into acetate, enabling mass production of connected eyewear.

What makes this sub-topic distinctive is the dual identity: prescription eyeglasses are essential for vision correction, while sunglasses double as protective gear and style anchors. The same pair can transition from a doctor’s prescription to a runway look. This duality drives a constant churn of innovation in materials, coatings, and frame geometry. Designers now treat the face as a canvas, pushing boundaries with sculptural shapes and bold colorways that would have seemed avant-garde a decade ago.

The 2026 landscape is defined by two opposing forces: Quiet Luxury, which favors subtle, high-quality finishes, and Expressive Futurism, which leans into exaggerated silhouettes and tech integration. Both trends are redefining what a pair of glasses can communicate. For B2B buyers, understanding these shifts is critical—sourcing decisions today must account for consumer appetite for both minimalist excellence and bold self-expression.

Eyewear’s role within the broader accessories ecosystem is also evolving. It now competes directly with jewelry and watches for wallet share, particularly among Gen Z and Millennials who see frames as a core part of their personal brand. The rise of smart glasses, projected to go mainstream in 2026, further blurs the line between accessory and wearable technology, creating new supply chain demands for electronics integration.

Key market segments and growth drivers in the Sunglasses Eye Glasses Guide sector.

2. Market Analysis

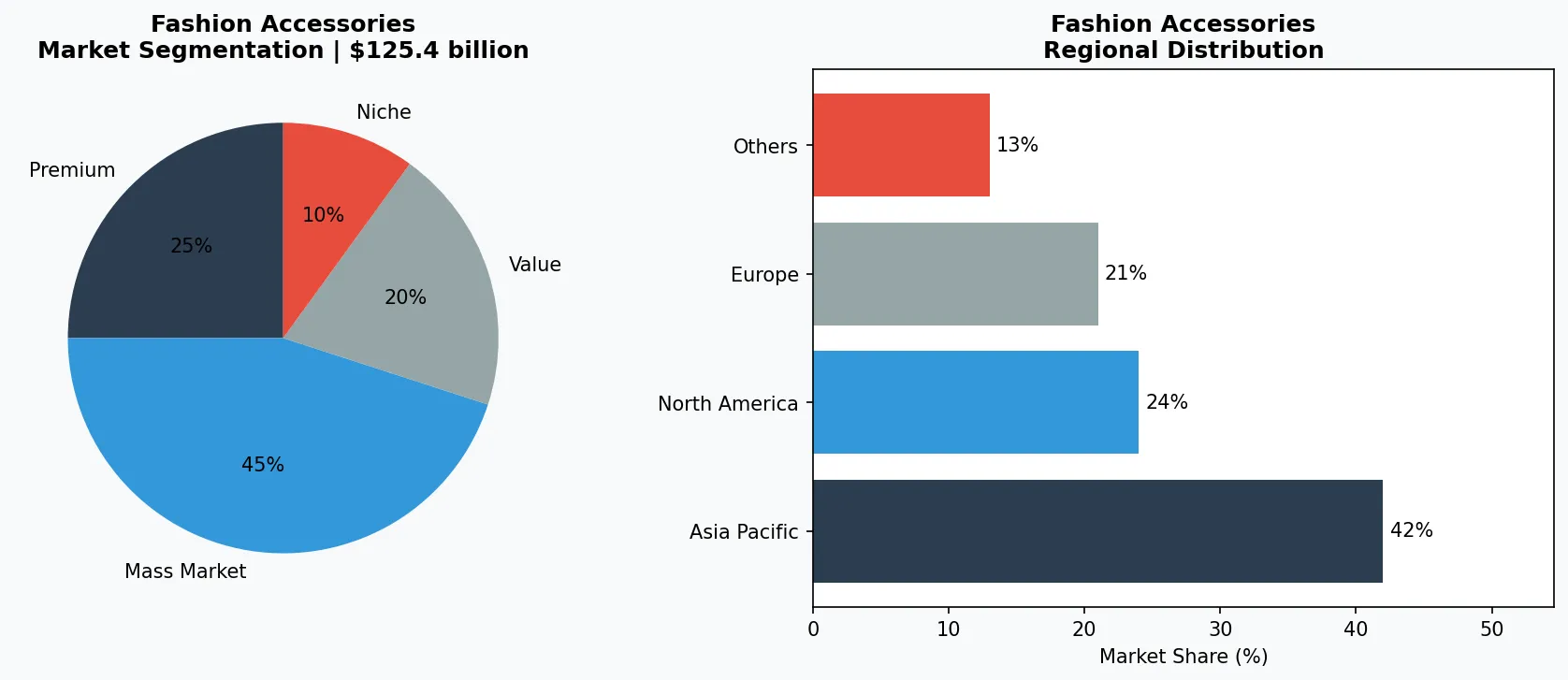

The global eyewear market was valued at approximately $125.4 billion as of 2022 and is expected to grow at a CAGR of around 6.7% through the next decade. Within this, sunglasses alone accounted for a significant share, driven by a 12% year-over-year growth in 2025, according to the Global Eyewear Report 2025. The fashion luxury segment outpaced the rest, rising 18%, as premium consumers treat designer frames as investment pieces.

Three growth drivers are propelling this expansion. First, the democratization of luxury: mid-range brands are offering premium aesthetics at accessible price points, pulling in younger buyers. Second, the clean beauty and UV awareness movement—consumers now prioritize certification like ISO 12312 for sunglass lenses, elevating quality standards. Third, the return of in-person events and travel post-pandemic has reignited demand for multiple frame wardrobes: one for work, one for weekends, one for the beach.

Regional dynamics vary sharply. North America and Europe remain the largest markets by value, but Asia-Pacific is the fastest-growing region, with a compound growth rate exceeding 8%. China and India are witnessing a surge in prescription eyewear adoption, fueled by rising screen time and myopia rates. Meanwhile, Latin America and the Middle East show strong appetite for luxury frames, driven by aspirational spending.

Supply chain pressures are reshaping the market. Frame materials—acetate, titanium, stainless steel—face price volatility. Manufacturers are investing in recycled bio-acetate and plant-based polymers to meet sustainability demands. The shift toward direct-to-consumer models, pioneered by online retailers, is squeezing margins for traditional wholesalers but rewarding those who can offer verified, traceable sourcing. B2B platforms like VerityRank are becoming essential for buyers to validate supplier claims on material quality and optical standards.

Market segmentation and regional distribution analysis for Sunglasses Eye Glasses Guide.

3. Product Categories

Prescription eyeglasses remain the backbone of the category, with demand shifting toward oversized geometric frames and clear glasses. These styles cater to both vision correction and fashion-forward consumers who want lenses that disappear into the face. Thin metal wireframes and retro round shapes are also resurging, driven by influencer culture. Buyers should look for suppliers offering multiple nose-pad adjustments and spring hinges for comfort.

Fashion sunglasses divide into two camps: the oversized cat-eye and the vintage-inspired silhouette. Cat-eye frames—reimagined with sharp, exaggerated wings—dominate women’s luxury segments. Vintage-inspired styles, including aviators and wayfarers reissued in translucent acetate, appeal to nostalgia-driven Millennials. The ‘boldest frames’ trend emerged in 2025, featuring chunky temples, neon gradients, and asymmetrical detailing. These statement pieces command higher average selling prices and shorter lifecycle runs.

Smart glasses finally entered the mainstream in 2025–2026, blending fashion with function. Audio-enabled frames with discreet bone conduction speakers and camera-integrated models are now available from multiple manufacturers. Lightweight titanium construction and prescription lens compatibility are key differentiators. For B2B buyers, smart glasses represent a high-growth niche but require careful vetting of electronics integration, battery safety, and IP ratings for sweat resistance.

Prescription Eyeglasses

Includes full-rim, semi-rimless, and rimless frames with spherical or aspheric lenses. Geometric shapes and clear glasses are trending, requiring suppliers to offer customizable bridge widths and temple lengths for comfort.

Fashion Sunglasses

Non-prescription sunwear with UV400 or better protection. Segments include oversized cat-eye, vintage aviators, and bold statement frames using neon acetates or mirrored coatings. These drive the 12% market growth.

Smart / Tech-Enhanced Eyewear

Frames integrating audio, camera, or fitness tracking. Limited to advanced manufacturers who can combine optical-grade lenses with sealed electronics. Rapidly growing segment demanding specialized assembly lines.

4. Leading Players

Luxury-Focused House | This archetype dominates the fashion luxury segment that grew 18% in 2025. Their strategy relies on limited-edition collaborations, celebrity endorsements, and investment in proprietary lens coatings. They often source acetate from Italian suppliers and distribute through selective department stores, maintaining price integrity and brand exclusivity.

Mass-Market Innovator | These players leverage economies of scale to offer trend-forward designs at mid-tier price points. They capitalize on the 12% sunglasses growth by rapidly iterating shapes like geometric frames and clear glasses. Their supply chain emphasizes fast turnaround from design to shelf, often using contract manufacturers in China and Vietnam, and they compete on volume and shelf presence.

Vertically Integrated Tech-Enabled Manufacturer | Combines frame production with smart glasses capabilities. This archetype invests heavily in R&D for lens-integrated displays and audio miniaturization. They target B2B partnerships with optical chains and corporate wellness programs. Their competitive advantage lies in proprietary certification for blue-light filtering and impact resistance, meeting both fashion and medical standards.

DTC Disruptor | While not a single company, this archetype shares a strategy of bypassing traditional channels. They use social media trend listening to identify viral shapes (e.g., Y2K nostalgia frames) and produce small batches. Their lean inventory model reduces risk, but they depend on reliable suppliers for quick reorders. VerityRank verification helps them validate factory compliance with delivery timelines and material specifications.

Legacy Optical Conglomerate Strategy

These players own multiple frame brands and leverage vertical integration from lens manufacturing to retail. They invest heavily in lens coating patents and offer white-label production for smaller labels, ensuring scale economies.

Fashion House Licensing Model

Luxury fashion brands outsource frame production to specialist manufacturers while controlling design and marketing. This model capitalizes on brand prestige without factory overhead, aligning with the 18% luxury segment growth.

Tech Startup Agility

Smaller companies focused on smart glasses and direct-to-consumer sales. They iterate designs rapidly using 3D printing and partner with contract electronics makers. Their strength is speed to market with niche features like AR overlays.

5. Market Trends

1. Quiet Luxury

The trend favors understated frames in matte blacks, translucent neutrals, and brushed metals with no logos. It matters because it signals sophistication and quality craftsmanship over flashiness. Luxury houses have adopted this by using premium acetate hand-polished over weeks, with hinge mechanisms that are invisible. Buyers sourcing for this trend should prioritize suppliers with specialized finishing capabilities and ISO 9001 quality management.

2. Expressive Futurism

Geometric, sculptural shapes that defy symmetry—hexagons, octagons, and asymmetrical cutouts. This trend is gaining traction among Gen Z consumers who want frames that spark conversation. It matters because it pushes manufacturers to adopt 3D printing for rapid prototyping of complex shapes, reducing tooling costs. One market example: geometric frames accounted for 22% of new style launches in 2025, up from 10% in 2023.

3. Smart Glasses Go Mainstream

Audio and camera-enabled eyewear that looks like regular frames. It matters because it creates a new product category that merges fashion with tech, opening higher margins. Market example: smart glasses sales grew by 40% in early 2026, driven by improved battery life and lighter weights. Suppliers must now integrate electronics while maintaining optical clarity—a dual challenge that rewards those with cross-industry partnerships.

4. Y2K Nostalgia & Cult Classics Reimagined

Tiny frame silhouettes (similar to 1990s/2000s styles) in bright pastels or translucent colors. This trend matters because it taps into cyclical fashion and encourages multiple pairs per consumer. Cult classics like the wayfarer and aviator are reissued in updated materials (bio-acetate, titanium) with adjustable nose bridges. Retailers report that nostalgia-driven frames have 30% faster sell-through rates than average, making them a low-risk bet for B2B ordering.

6. Regional Markets

North America: Mature, High-Value

The largest market by revenue, with strong demand for prescription progressives and polarized sunglasses. B2B buyers prioritize coatings (anti-reflective, scratch-resistant) and fast restock from domestic or Mexican suppliers.

Asia-Pacific: Volume Growth Hub

Rising disposable income and myopia rates fuel eyewear adoption. China and India are production and consumption centers. Buyers need to verify ISO certifications for exports, as quality varies significantly across factories.

Europe: Design and Sustainability Leader

European brands set trends in color and material. The EU’s circular economy directives push suppliers to use bio-acetate and recyclable packaging. B2B importers must document material sourcing to comply with REACH regulations.

7. Investment Outlook

Two concrete opportunities stand out. First, the rise of personalized prescription lenses integrated with blue-light filtering and adaptive tinting. Suppliers who can offer customizable lens treatments alongside trend-driven frames will capture premium B2B contracts from corporate wellness programs. Second, the expansion of after-sales service offerings—warranty extensions, lens replacement, and frame repair—as a recurring revenue stream. Brands that build partner networks for optical care will lock in repeat orders.

One significant risk: supply chain concentration of acetate and high-index plastic raw materials in a few regions. Any geopolitical or logistical disruption could spike frame costs by 15–20% within a quarter. B2B buyers should diversify suppliers across multiple countries and negotiate fixed-price contracts with index clauses. Additionally, the rapid pace of smart glasses technology may lead to inventory obsolescence; buyers should avoid large pre-orders of first-generation models and instead opt for modular designs that allow component upgrades.

Strategic Considerations:

- Customized Lens Bundles: Pair trendy frames with anti-fatigue or blue-light blocking lenses as a value-added package; this can boost average order value by 25% for B2B buyers.

- Subscription Repair Services: Offer annual lens replacement and frame adjustment programs that lock in recurring revenue and reduce returns.

- Raw Material Volatility: Acetate prices rose 8% in 2025 due to acetone shortages; diversifying to recycled or bio-based polymers can mitigate price spikes.

- Smart Glasses Quick Obsolescence: First-generation smart frames may lose software support within 18 months; buyers should negotiate upgrade clauses or opt for modular designs.

Frequently Asked Questions

Make Informed Decisions in the Sunglasses Eye Glasses Guide Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-22. All market figures are estimates and may vary from actual results.