Table of Contents

The global Sustainable Fashion industry serves consumers worldwide with diverse solutions.

1. Industry Overview

The global fashion industry will post low single-digit growth in 2026, according to McKinsey analysis. Yet within this sluggish broader market, one segment is accelerating dramatically: sustainable fashion. The Sustainable Fashion Market is projected to cross USD 19,852.4 million by 2033, surging from USD 10,122.8 million in 2026 at a compound annual growth rate of 10.1%. This represents a near-doubling of market value in just seven years, signaling a fundamental shift in how consumers and investors view apparel production.

Industry Scope & Characteristics

Broad Product Portfolio

Products span recycled clothing, organic cotton apparel, vintage clothing, upcycled fashion, eco-friendly fabrics, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Sustainable fashion encompasses recycled clothing, organic cotton apparel, vintage clothing, upcycled fashion, and eco-friendly fabrics that minimize environmental harm throughout the production lifecycle. The industry distinguishes itself through measurable commitments: reduced water consumption, carbon neutrality pledges, biodegradable material adoption, and transparent supply chains. These aren't marketing abstractions but operational realities driving procurement decisions at scale.

Recent years have witnessed a historic shift as sustainability evolved from niche positioning to mainstream expectation. Major retailers now face investor pressure and regulatory scrutiny that would have been unthinkable a decade ago. The European Union's Green Claim Directive and expanding extended producer responsibility frameworks are compressing timelines for compliance. Brands that treat sustainability as optional are discovering competitive disadvantage accelerates with each passing quarter.

The textile and apparel sector accounts for approximately 10% of global carbon emissions and consumes vast quantities of water and chemicals. As stakeholders increasingly demand accountability, sustainable fashion is transitioning from alternative to imperative. The question confronting industry players is no longer whether to adapt but how rapidly transformation can be executed.

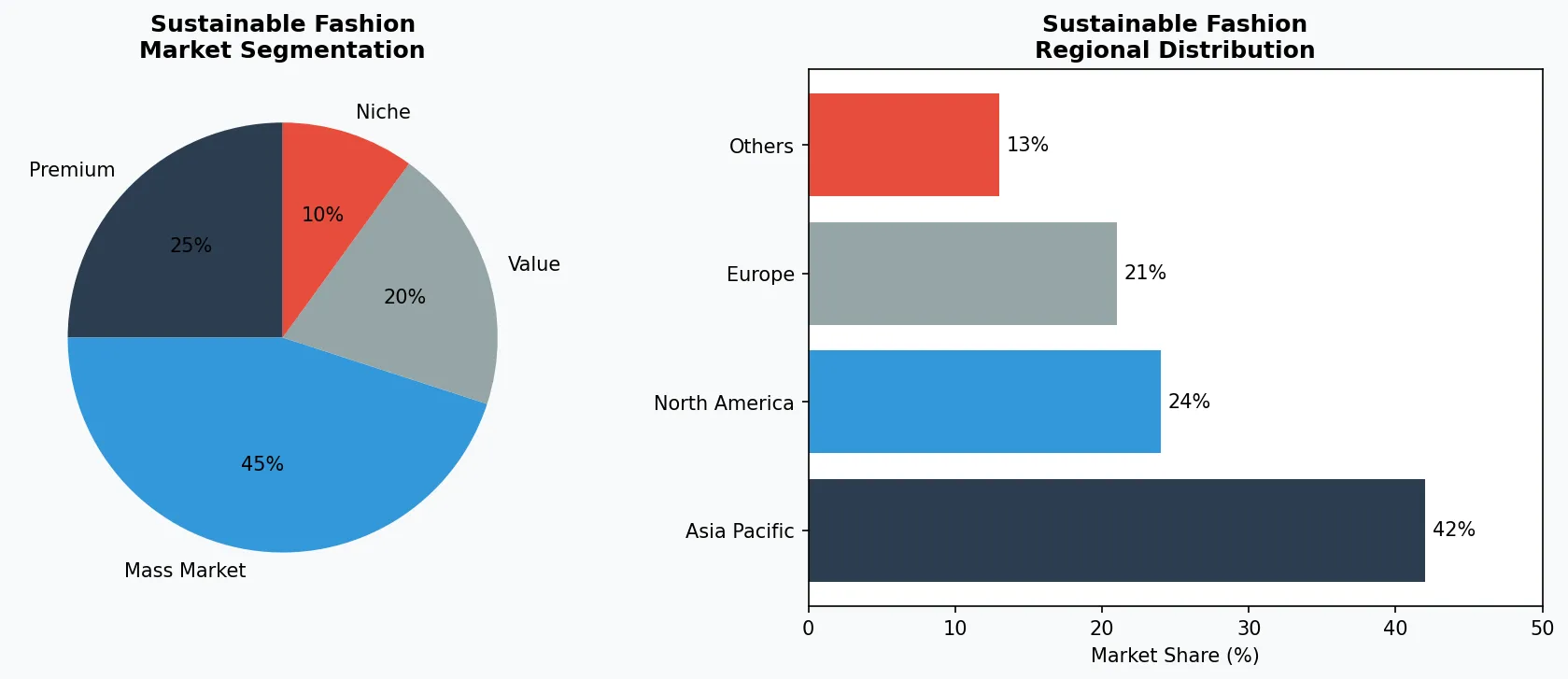

Key market segments and growth drivers in the Sustainable Fashion sector.

2. Market Analysis

The sustainable fashion market's headline figure demands attention: USD 19,852.4 million in projected value by 2033, representing explosive growth from USD 10,122.8 million in 2026. This 10.1% CAGR nearly doubles market size within seven years, outpacing conventional apparel growth by a factor of three to five depending on segment. The Sustainable and Eco-Friendly Clothing market specifically is tracking a 4.7% CAGR from 2026 to 2033, demonstrating that even the conservative estimates indicate robust expansion.

Three forces drive this growth trajectory. First, consumer preference is tilting decisively toward environmentally conscious purchasing, particularly among millennials and Gen Z consumers who represent growing purchasing power. Research indicates sustainability claims now influence buying decisions for a majority of apparel consumers under 40. Second, supply chain innovations are reducing cost premiums historically associated with eco-friendly production. Recycled fabric technologies and organic fiber scaling have narrowed price gaps that once limited market accessibility. Third, regulatory frameworks in Europe and increasingly North America are mandating transparency and environmental performance, removing the option for brands to maintain opaque practices.

Geographic distribution reveals uneven opportunity concentration. North America and Europe currently represent the largest sustainable fashion markets by revenue, driven by established eco-conscious consumer bases and stringent regulatory environments. However, Asia Pacific is emerging as the fastest-growing region, propelled by rising middle-class disposable incomes in China, India, and Southeast Asian markets combined with domestic sustainability awareness campaigns. Latin America shows nascent but promising growth, particularly in natural fiber and upcycling segments exploiting regional agricultural advantages.

Market segmentation and regional distribution analysis for Sustainable Fashion.

3. Product Categories

Organic cotton apparel leads sustainable fashion's product categories, commanding significant market share through mainstream accessibility. Brands including Pact and Eileen Fisher have built core collections around GOTS-certified organic cotton, eliminating toxic dyes and reducing water consumption by up to 91% compared to conventional cotton cultivation. These garments typically carry price premiums of 15-30% over conventional equivalents, a narrowing gap driving volume growth.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Recycled clothing and upcycled fashion represent the fastest-growing sub-category, innovation meeting environmental imperative. Patagonia's "Worn Wear" program exemplifies this space, taking returned garments and reselling them directly or transforming damaged items into new products. Reformation has pioneered luxury recycled面料, using deadstock materials and sustainable viscose to create premium-priced pieces that generate lower environmental footprints. Strike has built its entire brand identity around upcycled denim, diverting textile waste from landfills while creating distinctive, limited-production garments.

Eco-friendly fabrics extend beyond organic cotton to include Tencel, modal, hemp, and innovative materials like mushroom leather and ocean plastic textiles. Eileen Fisher's "Renew" program accepts old garments and transforms them into new pieces using proprietary recycling processes. This closed-loop approach addresses the linear "take-make-dispose" model that has defined fashion for decades. Accessories including sustainable jewelry and bags round out the category, with brands incorporating recycled metals, FSC-certified wood, and plant-based alternatives to conventional materials.

4. Leading Players

Patagonia remains the category standard-bearer, having built its entire brand identity around environmental activism since the 1970s. The company's 2022 conversion to a trust-owned entity, directing all profits to climate causes, represents the most radical corporate structure transformation in apparel history. Patagonia's strategy centers on durability-first design, repair services, and aggressive secondhand market development. The "Worn Wear" platform has normalized buying used from a premium brand, demonstrating that sustainability and profitability are complementary rather than conflicting objectives.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the sustainable fashion space.

Eileen Fisher commands a distinct position in sustainable luxury, targeting affluent consumers willing to pay premium prices for timeless design and environmental responsibility. The brand's "Renew" take-back program and "Visions" collection using deadstock fabrics exemplify circular economy implementation. Eileen Fisher's recent investments in regenerative agriculture sourcing demonstrate forward-thinking material strategy, anticipating regulatory requirements for supply chain transparency. The company's B Corp certification and women-focused ownership structure differentiate its sustainability narrative from competitors.

Reformation has disrupted sustainable fashion by proving that eco-friendly apparel can compete on aesthetic and trend-responsiveness terms previously associated with fast fashion. The direct-to-consumer brand's rapid inventory turnover and Instagram-native marketing demonstrate that sustainability need not compromise commercial velocity. Reformation's "RefScale" environmental impact dashboard, showing each garment's carbon footprint and water usage, set industry transparency standards. Everlane similarly combines sustainability messaging with aggressive pricing strategy, using its "Radical Transparency" platform to disclose factory locations and cost breakdowns for every product. Pact competes at accessible price points, proving that organic cotton basics can reach mass-market consumers without premium pricing.

5. Market Trends

1. CIRCULAR FASHION

CIRCULAR FASHION — Circular fashion represents the industry's most comprehensive structural shift, designing products for unlimited lifecycles through repair, resale, and recycling. Patagonia, Eileen Fisher, and Reformation have all built operational infrastructure supporting garment return, resale, and recycling programs. The trend matters because linear production models generate unsustainable waste volumes—approximately 92 million tons annually. Circular approaches decouple revenue growth from resource consumption. Patagonia's repair program processes over 40,000 garments annually, extending product lifecycles by years.

2. CARBON NEUTRAL OPERATIONS

CARBON NEUTRAL OPERATIONS — Carbon neutrality commitments are accelerating from marketing language to operational reality as measurement standards mature. Brands including Everlane and Reformation have achieved carbon-neutral certification for specific product lines, with broader organizational commitments targeting 2030 timelines. This trend matters because fashion's carbon footprint rivals aviation, and voluntary pledges are increasingly backed by regulatory requirements in key markets like the EU. Supply chain electrification and renewable energy procurement are primary implementation pathways.

3. INDUSTRY 4.0 DIGITALIZATION

INDUSTRY 4.0 DIGITALIZATION — Digitalization and Industry 4.0 technologies are becoming survival prerequisites rather than competitive advantages. AI-powered demand forecasting reduces overproduction waste, while blockchain-enabled supply chain tracking meets emerging transparency regulations. Strike and Reformation have implemented digital fitting tools reducing return rates, addressing both customer experience and logistics emissions. Digital product passports are emerging as regulatory requirements in EU markets, requiring comprehensive material and production data attached to each garment.

4. PRICE-VALUE ALIGNMENT

PRICE-VALUE ALIGNMENT — The historical tension between price premium and sustainability is resolving as production scaling reduces eco-friendly manufacturing costs. Pact's organic cotton basics demonstrate that accessible price points are achievable, while premium brands justify higher prices through durability and transparency. Consumer research indicates willingness to pay 10-15% premiums for verified sustainable credentials, supporting margin structures that fund continued innovation. This trend matters because mass-market adoption determines whether sustainable fashion remains niche or achieves transformational scale.

6. Regional Markets

North America represents the most mature sustainable fashion market, with the United States commanding the largest regional share. American consumers demonstrate high willingness-to-pay premiums for sustainability claims, driving brand investment in eco-positioning. The absence of federal sustainability mandates has accelerated private sector initiatives, with California particularly active in textile waste regulation. Major brands including Patagonia and Everlane are headquartered in the region, shaping industry norms globally. However, market saturation concerns are emerging, with growth increasingly dependent on category expansion rather than consumer base expansion.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

Europe dominates regulatory-driven sustainability transformation, with the EU Green Claim Directive and Extended Producer Responsibility schemes setting global standards. Germany, France, and the Netherlands lead in sustainable apparel consumption per capita, while Scandinavian countries including Sweden and Denmark have built internationally recognized eco-fashion ecosystems around brands like H&M's conscious collections and local innovators. The EU's Digital Product Passport requirements, effective 2027 for textiles, are forcing supply chain transparency investments across the region and globally for brands serving European markets.

Asia Pacific emerges as the pivotal growth region, combining rising middle-class purchasing power with substantial manufacturing base. China represents both the largest apparel producer globally and an increasingly significant sustainable fashion consumer market, driven by urban consumers facing domestic pollution concerns. India presents distinct opportunities in natural fiber production and traditional textile techniques compatible with contemporary sustainability narratives. Southeast Asian markets including Indonesia and Vietnam show accelerating consumer interest alongside production sector investments in eco-friendly manufacturing capacity to serve export markets.

7. Investment Outlook

Two specific opportunities define sustainable fashion's near-term trajectory. First, AI-powered textile recycling technology is approaching commercial viability at scale, potentially solving the mechanical recycling limitations that currently constrain circular fashion economics. Companies including H&M's innovation lab and startups like Evrnu are developing chemical recycling processes that can separate blended fabrics into reusable components. Second, the EU's Digital Product Passport mandate creates immediate compliance market opportunities for supply chain traceability platforms, with companies including TextileGenesis and Provenance positioned to capture significant enterprise software spending as the 2027 implementation deadline approaches.

One concrete risk demands attention: greenwashing backlash threatens brand credibility across the sector. Regulatory enforcement is intensifying, with the EU greenwashing monitor reporting that 40% of sustainability claims in fashion lack substantiation. As litigation and regulatory fines increase, brands that made aspirational but vague commitments face reputational damage that could slow overall market growth. The risk concentrates among large incumbents attempting to retrofit sustainability narratives onto conventional operations rather than authentic transformation. Companies demonstrating verifiable, specific progress on measurable metrics will consolidate market trust, while those relying on marketing language over operational substance face accelerating competitive disadvantage.

Strategic Considerations:

- ('Technology & AI Integration:', 'Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.')

- ('Sustainability as Business Strategy:', 'Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.')

- ('Transparency & Traceability:', 'Consumers demand increasingly granular information about product origins, ingredients, and production methods.')

- ('Emerging Market Penetration:', 'Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.')

Make Informed Decisions in the Sustainable Fashion Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-15. All market figures are estimates and may vary from actual results.