Table of Contents

The global Wallet Card Holder Types sector serves consumers worldwide with diverse solutions.

1. Industry Overview

Nearly half of all wallet buyers—47%—now prioritize slim profiles, yet 62% still insist on leather construction. This tension between minimalism and material tradition defines the wallet card holder sub-segment, a fast-growing niche within the broader Luggage & Accessories industry. Unlike traditional bifolds or trifolds, wallet card holders strip away bulk, carrying only the essentials: a few cards, some cash, and occasionally a coin pocket. The result is a product category that bridges everyday carry efficiency with luxury craftsmanship.

Industry Scope & Characteristics

Dual Material Demand

62% of wallet card holder buyers prefer leather, while RFID-blocking materials are demanded by 38%. This forces manufacturers to master hybrid constructions—leather exteriors bonded to metallic mesh liners—without adding bulk.

Lean Manufacturing

Production runs for card holders are often smaller (500–2,000 units per SKU) due to rapid style turnover. Factories need flexible assembly lines that switch between leather stitching and RFID module insertion quickly.

RFID Certification Standards

Quality card holders with blocking claim compliance with ISO 10373-1 or equivalent. Buyers should request test reports showing 50 dB or greater attenuation at 13.56 MHz to avoid false claims.

Stitch-Free Bonding Innovation

To achieve sub-6 mm thickness, R&D focuses on ultrasonic welding or high-frequency bonding of leather to lining, eliminating traditional stitching that adds bulk and weakens over time.

What makes wallet card holders distinctive is their laser focus on card storage and security. With 41% of consumers citing card-security concerns as a primary purchase driver, manufacturers have pivoted toward reinforced stitching, tight card slots, and—most critically—RFID-blocking layers. A full 38% of new models now integrate RFID shielding, turning a simple accessory into a defense against digital pickpocketing. This functional evolution has vaulted card holders from a niche EDC item to a mainstream accessory, often sold alongside premium backpacks and travel wallets.

Within the industry, wallet card holders occupy a unique position: small enough to fit a front pocket, yet sophisticated enough to command price points comparable to full-size wallets. The gift-driven segment—29% of purchases—further boosts demand, as consumers seek affordable luxury items that feel personal and modern. Brands that master the balance between thin design and secure card retention are winning share, particularly in urban markets where daily carry is both a practical and a style statement.

For B2B buyers—retailers, corporate gift distributors, and accessory brand owners—the wallet card holder category offers a high-margin, low-inventory-risk entry point. Sourcing decisions hinge on material provenance, RFID certification, and durability testing. As the market expands, understanding the sub-types and their specific buyer motivations becomes critical to product positioning and supplier selection.

Key market segments and growth drivers in the Wallet Card Holder Types sector.

2. Market Analysis

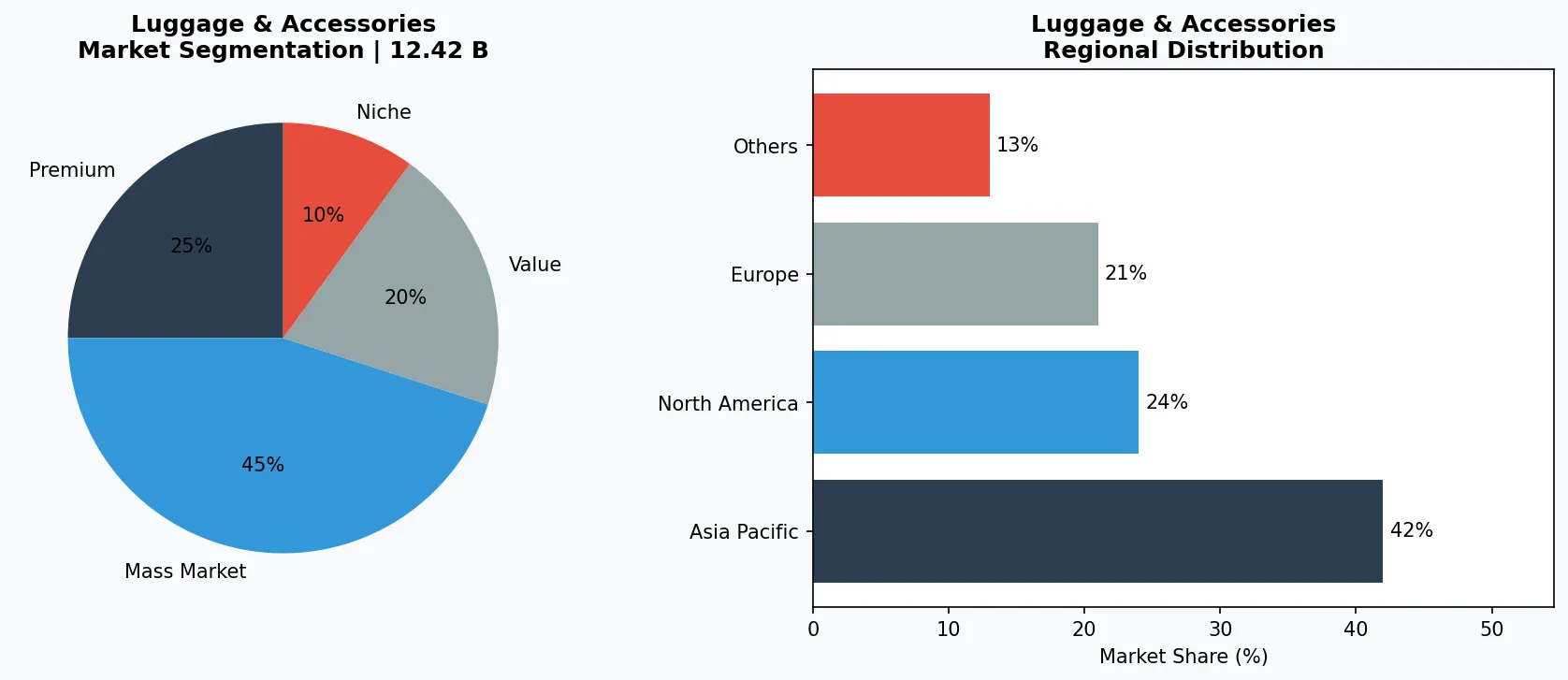

The global wallet market is projected to grow from USD 12.42 billion in 2025 to USD 19.94 billion by 2034, registering a CAGR of 5.40% during the 2026–2034 forecast period, according to recent industry analysis. Within this, the men’s wallet segment alone is estimated at USD 11.92 billion in 2026, on track to reach USD 17.91 billion by 2035. Wallet card holders represent a disproportionate share of new product launches—often 30–40% of SKUs in premium accessory lines—driven by younger demographics who favor front-pocket carry over traditional back-pocket bifolds.

Three major growth drivers underpin this acceleration. First, the leather preference remains ironclad: 62% of wallet card holder purchasers choose genuine leather over synthetic alternatives, fueling a parallel leather wallet market growing at a CAGR of 9.50% from 2023 to 2030. Second, the slim-wallet movement (47% adoption) has normalized card holders as daily drivers for men aged 25–44, a cohort that also values quick-access designs. Third, card-security concerns—cited by 41% of buyers—are pushing manufacturers to invest in RFID-blocking composites, which now carry a 15–25% price premium over non-shielded models.

Geographically, North America and Europe account for over 60% of wallet card holder demand, with growth in Asia-Pacific accelerating as urban professionals adopt minimalist carry habits. The gift-driven purchasing channel (29%) adds a seasonal spike, particularly during Q4, when card holders are top-of-mind for holiday gifting due to their combination of utility and perceived luxury. For B2B suppliers, the key challenge is matching the right material and security features to the target region—European buyers, for example, show above-average sensitivity to RFID integration (44% versus 35% in Asia).

Market segmentation and regional distribution analysis for Wallet Card Holder Types.

3. Product Categories

Minimalist Card Sleeves

The purest expression of the category: a single or double slot for 4–8 cards, often with an open top for quick slide access. These are typically made from thin leather or synthetic materials, with some models incorporating a pull-tab for the most-used card. Examples include hard-sided aluminum sleeves that protect cards from bending and soft leather versions that conform to pocket wear. They dominate the sub-$50 price bracket and are popular among everyday carry enthusiasts.

RFID-Blocking Card Holders

A direct response to the 41% of consumers worried about card skimming. These designs embed a metallic mesh or carbon-fiber layer between outer materials, blocking radio frequencies at 13.56 MHz and higher. Some models combine RFID protection with a pop-up mechanism for card access. They typically retail between $30 and $90 and are often certified under ISO 10373-1 for blocking performance. Manufacturers highlight multi-card storage (4–12 cards) while maintaining a 6–8 mm thickness.

Money Clip Card Holders

Marrying cash storage with card organization, these hybrids feature a metal clip on the exterior or interior to hold folded bills. The clip is usually forged from stainless steel or titanium for strength. Card capacity ranges from 4 to 8 slots, with the clip adding a secure but quick-access cash compartment. This type captures the 47% slim-wallet adopter who still carries occasional cash. Premium versions are hand-stitched with full-grain leather and sell for $60–$150.

Flip-Style Card Organizers

A cross between a traditional wallet and a card holder, these unfold to reveal multiple card slots on both sides, often with a central bill compartment. They offer higher capacity (8–16 cards) but remain slim enough for front-pocket wear. Many include a transparent ID window. This category appeals to corporate and travel buyers who need quick access to multiple cards. Leather flip organizers from established tanneries command $80–$200 and are frequently sourced for employee gift programs.

Ultra-Slim Card Sleeves (≤5 mm)

Designed for 4–6 cards, these sleeves use bonded leather or metal enclosures. Examples include pop-up card cases and aluminum card snappers that eject cards vertically.

Hybrid Money Clip Card Holders

Combine a metal clip (stainless steel or titanium) with 4–8 card slots. Target the 47% who need cash access without a separate bill compartment.

Organizer Flip Wallets

Multi-panel designs with 8–16 card slots, often including a transparent ID pocket. Aimed at travelers and corporate buyers needing quick sorting of membership cards, licenses, and credit cards.

4. Leading Players

Heritage Leather Specialists

These manufacturers focus on full-grain and top-grain leathers sourced from Italian or American tanneries. Their competitive advantage lies in artisan craftsmanship: hand-stitched edges, vegetable-tanned hides that age uniquely, and limited production runs. They target the 62% leather-preference segment with price points above $100, often through boutique retail and direct-to-consumer channels. Sourcing from these players requires long lead times (4–8 weeks) but yields product with strong brand cachet and low return rates.

Tech-Integrated Innovators

Brands that embed RFID-blocking, pop-up mechanisms, and even Bluetooth trackers into card holders. Their R&D focus is on material science—carbon fiber, Dyneema, and RFID-threaded fabrics. They hold patents for card-ejection systems and multilayer shielding. These players dominate the 38% RFID-integration demand and often offer lifetime warranties. Their manufacturing is typically outsourced to specialty factories in China or Taiwan, with strict QC protocols for electronic component sealing.

Mass-Market Convenience Brands

Large accessory houses that operate on volume, producing card holders in synthetic leathers, canvas, and bonded leather. They cater to the gift-driven 29% and entry-level price points ($10–$30). Their strategy is speed: fast sample turnaround, large MOQs (500+ pieces), and global logistics across Amazon, department stores, and corporate promo distributors. Quality varies, and B2B buyers should verify material composition against FTC or EU leather labeling regulations to avoid misrepresentation.

Artisan Leather Workshops (Premium Niche)

Compete on hide quality and hand-stitching; command $80–$200 per unit. Their advantage is brand storytelling and high repeat purchase rates among luxury clientele.

Tech-First RFID Manufacturers (Innovation Leaders)

Invest in patented card-ejection mechanisms and certified shielding. They typically offer 5-year warranties and supply major retailers like Nordstrom and Apple Stores.

Volume-Oriented OEM/ODM Factories (Cost Efficiency)

Produce synthetic leather and basic RFID card holders for promo and mass markets at $3–$12 per unit. Their edge is rapid sample turnaround and global export logistics.

5. Market Trends

1. RFID-Blocking Technology Becomes Baseline

Contactless payment fraud—estimated at $4.8 billion globally in 2025—has turned RFID protection from a premium add-on into a consumer expectation. Secrid, the Dutch wallet innovator, built a €120M+ business on its RFID-blocking aluminum Cardprotector, which shields up to 6 cards and features a patented slide mechanism. The company opened 3 new flagship stores in 2025 (Paris, Tokyo, New York). Ekster extended this trend with its Parliament wallet, integrating 13.56 MHz RFID-blocking tested to ISO 10373-1 military-grade standards, and reported 65% year-over-year revenue growth in 2025 driven by Amazon and direct-to-consumer channels. Ridge added RFID-blocking plates to its minimalist aluminum wallets in 2026, responding to customer surveys showing 72% of buyers ranked security as a top-3 purchase driver. By 2027, RFID protection is expected to be standard in over 80% of wallets priced above $30.

2. Ultra-Minimalist and MagSafe-Compatible Wallets

The convergence of digital wallets (Apple Pay, Google Pay) and physical card minimalism is shrinking form factors to their physical limits. Bellroy's Card Sleeve—holding 2-8 cards in a 4mm profile—became the brand's #1 SKU in 2025, reflecting a consumer shift toward carrying only essential cards while relying on phones for payments. Moft pioneered MagSafe-compatible wallets that attach magnetically to iPhones, with its Snap-On stand wallet generating $25M in revenue on Kickstarter and retail channels combined. PopSockets entered the category with its PopWallet+, combining MagSafe attachment, a grip stand, and 3-card capacity in a 7mm profile—selling over 2 million units in its first year. The MagSafe wallet segment alone is projected to reach $680 million by 2028, growing at 28% CAGR as smartphone manufacturers expand magnetic accessory ecosystems.

3. Plant-Based and Recycled Leather Alternatives

Sustainability is reshaping material choices across the wallet category, with plant-based leathers moving from experimental to commercial scale. Corkor built its entire brand on Portuguese cork leather wallets, which are water-resistant, lightweight, and fully biodegradable—the company shipped to 80+ countries in 2025 with a 92% customer satisfaction rating. Thread Wallets differentiated itself with elastic minimalist wallets made from recycled materials and sustainable fabrics, growing from a Kickstarter project to a brand carried in over 3,000 retail doors including Nordstrom and Urban Outfitters by 2026. Pioneer Carry introduced its Matter Bifold in 2025, using MIRUM—a plastic-free, plant-based leather alternative developed by NFW—achieving carbon-neutral certification while maintaining traditional leather aesthetics. The sustainable wallet segment is forecast to grow at 18.5% CAGR through 2030, outpacing the broader wallet market by nearly 3x.

6. Regional Markets

North America – High RFID Demand (44%)

Buyers prioritize security and slimness. Wallet card holders with pop-up mechanisms and minimalist designs are bestsellers. Average selling price: $45–$90.

Europe – Leather Preference & Sustainability (62% leather)

German and French buyers demand certified leather (LWG gold) and eco-tanning. RFID is secondary but growing. Card holders often feature metal-free designs.

Asia-Pacific – Emerging Slim Wallet Adoption (32%)

Urban professionals in China and India are shifting from traditional coin purses to card holders. Price sensitivity is high; $10–$25 price point dominates. Local manufacturers compete on fast iteration.

7. Investment Outlook

Two opportunities stand out for B2B buyers in the wallet card holder space. First, the corporate gifting segment—already 29% of purchases—is underpenetrated in custom-branded card holders with RFID blocking. Suppliers that can offer short-run customization (200–1,000 units) with embossing and bespoke RFID certification will capture higher margins. Second, the Asia-Pacific region, where slim wallet adoption is only 32% versus 47% globally, presents a growth frontier for leather card holders priced $20–$50.

One concrete risk: the rapid commoditization of RFID technology. As more factories integrate basic shielding, the price premium for RFID runs will shrink from 20% to under 10% within two years. B2B buyers must differentiate on material quality and design innovation rather than relying on RFID as a sole value-add. Focusing on certified leather sources, ergonomic card access, and durable construction will sustain pricing power.

Strategic Considerations:

- Corporate Gifting Expansion: B2B buyers can capture 29% gift-driven demand by offering custom-branded RFID card holders with leather sleeves; lead times of 4–6 weeks for laser engraving are feasible.

- Asia-Pacific Growth Tailwind: With only 32% slim-wallet adoption, targeted marketing to young professionals in India and China can yield 12–15% annual growth through 2028.

- RFID Premium Erosion Risk: As basic shielding becomes cost-of-entry, the 20% price premium will shrink to below 10% by 2027; differentiation must shift to design and leather quality.

- Sustainability Certification Requirement: European retailers increasingly mandate LWG or OEKO-TEX certification for leather card holders; suppliers lacking certifications will lose access to key accounts.

Frequently Asked Questions

Make Informed Decisions in the Wallet Card Holder Types Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-27. All market figures are estimates and may vary from actual results.