Table of Contents

The global Whole-Home Smart Ecosystem sector serves consumers worldwide with diverse solutions.

1. Industry Overview

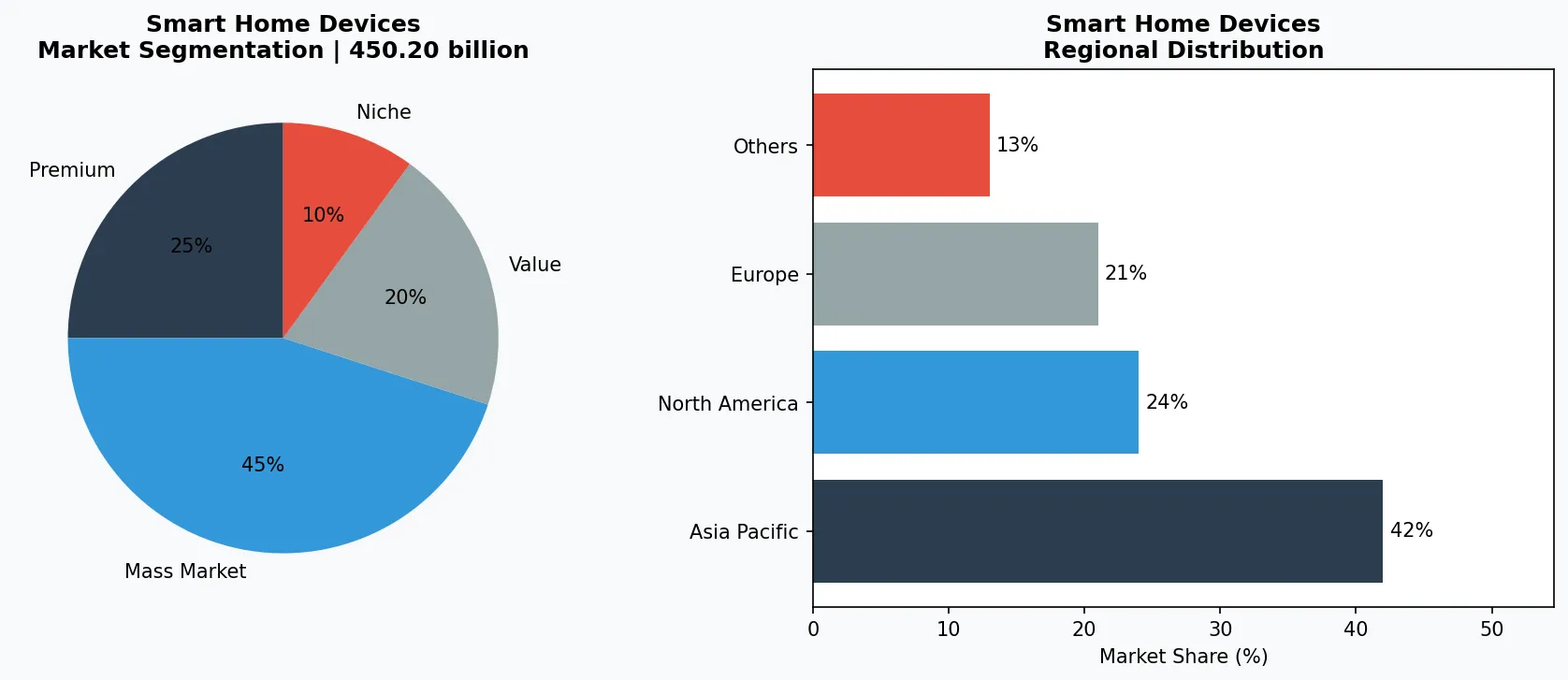

By 2032, the global smart home market is forecast to hit USD 450.20 billion, up from USD 230.76 billion in 2026—a compound annual growth rate of 11.8%. Yet for all that spending, the typical smart home today remains a jumble of silos: a smart lock that ignores the thermostat, a light that won't talk to the camera. The whole-home smart ecosystem promises to change that. It is not merely a collection of connected devices; it is a unified, interoperable platform where every sensor, switch, speaker, and appliance coordinates through a single intelligence layer.

Industry Scope & Characteristics

Interoperability-Centric Architecture

Unlike standalone smart devices, whole-home ecosystems rely on a central hub or platform that orchestrates multiple device categories (lighting, security, climate). Key technology: Matter protocol and Thread mesh network ensure cross-brand communication without proprietary bridges.

Cloud + Edge Hybrid Supply Chain

Ecosystem products require both hardware manufacturing (sensors, hubs, switches) and cloud backend services for remote access and AI analytics. Suppliers must offer firmware update pipelines and server uptime SLAs – a deviation from traditional appliance supply chains.

Security and Privacy Certifications

Whole-home systems handle sensitive occupancy and video data. ISO 27001 for cloud infrastructure, UL 2900 for networked devices, and Apple HomeKit's MFi certification for encryption are critical compliance markers for B2B sourcing.

AI-Driven Predictive Simulation

R&D focus is shifting from simple rule-based automation to predictive AI models that anticipate user behavior. For example, ecobee's SmartHome uses occupancy patterns to pre-heat rooms and Samsung SmartThings uses machine learning to detect water leaks two days before they occur.

What makes the whole-home ecosystem distinctive is its emphasis on orchestration rather than individual point products. A smart speaker is no longer just a voice assistant; it becomes the command center. A thermostat is not just a programmable controller; it adjusts based on occupancy data from motion sensors and security cameras. This ecosystem approach demands a new architecture: cloud-connected hubs, edge AI processors, and universal protocols like Matter that let devices from different brands communicate natively.

The shift is already accelerating. In 2025, the global smart home market was valued at USD 147.52 billion, and it is projected to jump to USD 180.12 billion in 2026. Analysts expect the segment to expand by over USD 315 billion between 2026 and 2030, representing a CAGR of 24.1%. The growth is driven not by adding more gadgets, but by making them work together seamlessly. For B2B buyers—from property developers to hospitality chains—specifying a whole-home ecosystem means prioritizing platforms over parts, and interoperability over price.

Key market segments and growth drivers in the Whole-Home Smart Ecosystem sector.

2. Market Analysis

The whole-home smart ecosystem is the fastest-growing sub-segment within smart home devices, propelled by three major forces. First, the demand for energy efficiency. Smart thermostats, lighting controls, and HVAC integration can reduce residential energy consumption by 15–30%, according to industry estimates. With energy prices volatile, homeowners and commercial property managers are investing in ecosystem-level automation. The HVAC segment alone is a multi-billion-dollar driver within the overall smart home pie.

Second, the proliferation of AI-enabled hubs. The trend for 2026, as noted by leading tech analysts, is the emergence of a single 'AI box' that consumers buy and grant access to all their devices. This hub acts as a local brain, processing voice commands, running automation routines, and even learning occupant behavior. Companies like Amazon (with Alexa), Google (Nest Hub), and Apple (HomePod) are racing to position their hubs as the indispensable controller of the whole home.

Third, the standardization of wireless protocols via the Matter certification. Launched in late 2022 and adopted by over 700 companies by 2025, Matter eliminates the need for proprietary bridges. A Matter-certified smart lock from one brand can communicate directly with a Matter-certified light from another, using Thread or Wi-Fi. This lowers integration costs and expands the addressable ecosystem. By 2026, Matter is expected to be embedded in 90% of new smart home devices, making whole-home integration accessible even to mid-range budgets.

The market size trajectory underscores the opportunity. From USD 150.26 billion in 2025 to USD 182.08 billion in 2026, the smart home market is growing exponentially. The whole-home segment—defined as systems with at least three interoperable device categories—captures the largest share of this growth, estimated at over 40% of new installations by 2027.

Market segmentation and regional distribution analysis for Whole-Home Smart Ecosystem.

3. Product Categories

The whole-home smart ecosystem comprises four core product categories that work in concert:

Control Hubs & Smart Speakers.

These are the central nervous system. Amazon Echo (Alexa) and Google Nest Hub (Google Assistant) dominate, while Apple HomePod integrates tightly with HomeKit. In 2026, expect hubs to include onboard AI processors that run voice recognition locally, reducing cloud dependency and latency for time-sensitive commands like locking doors.

Security & Access Control.

Smart locks (e.g., August, Yale), video doorbells (Ring, Nest), and indoor/outdoor cameras form the security layer. In a whole-home ecosystem, these devices share data: the camera detects motion, the lock auto-locks when no one is home, and the lights simulate occupancy. Battery-powered sensors that last two years without hardwiring are a key innovation for retrofit installations.

Climate & Energy Management.

Smart thermostats like the Nest Learning Thermostat and ecobee SmartThermostat adjust heating and cooling based on occupancy sensors, weather forecasts, and utility rate signals. They also serve as occupancy sensors for the broader ecosystem, turning off lights and disabling security alerts when a programmed schedule is in place.

Lighting & Ambiance.

Smart bulbs (Philips Hue, LIFX) and smart switches (Lutron Caséta) enable scene-based control. In a whole-home ecosystem, lights respond to voice, motion, and even camera-based occupancy detection. Color-temperature tuning and circadian rhythm schedules are becoming standard features that contribute to wellness.

Starter Ecosystem Bundles

Typically include a smart speaker hub + 2 smart bulbs + 1 smart plug. Example: Amazon Echo 4th Gen + Philips Hue White starter kit. Focus on voice control and scheduling, no third-party integration required.

Mid-Range Security & Climate Kits

Combine a video doorbell, smart thermostat, and motion sensors with a central hub. Example: Google Nest Hub + Nest Thermostat + Nest Doorbell. Uses Matter/Thread for interoperability and allows expansion with third-party locks (e.g., Yale).

Premium Whole-Home Automation Platforms

Professional-grade systems with wired sensors, blind motors, and centralized panels. Example: Lutron RadioRA 3 + Sonos speakers + Somfy shades. Target high-net-worth residential and commercial hospitality, with local control, no cloud dependence.

4. Leading Players

Amazon has built the largest whole-home ecosystem by device count, with over 200 million Alexa-enabled devices sold. Its strategy is platform lock-in: subsidize Echo hardware, build a vast skill store, and integrate deeply with Ring and Blink cameras. Amazon's recent investment in local voice processing aims to reduce privacy concerns and latency, making Alexa faster for routine commands.

Google (Alphabet) pursues a dual hardware/AI strategy. The Nest line of thermostats, cameras, and doorbells integrates with Google Assistant. Google's strength is in AI-driven automation—using its machine learning models to optimize energy usage, predict user patterns, and offer proactive suggestions. The Google Home app serves as a centralized dashboard, but Google's open approach to Matter allows third-party devices to join without requiring a Nest brand ecosystem.

Apple's HomeKit ecosystem is the privacy-first alternative. HomeKit requires hardware-level encryption and local processing through an Apple TV or HomePod hub. While its market share is smaller (estimated at 15% of U.S. smart home owners), Apple commands premium adoption in higher-income households concerned about data security. The 2025 addition of Matter support to HomeKit ensures compatibility without sacrificing security—a key selling point for enterprise buyers.

Samsung differs by offering an appliance-first ecosystem via SmartThings. The company integrates its refrigerators, washers, and ovens with third-party sensors and cameras. SmartThings' strength is in the retrofit market, where a $35 SmartThings Hub can bridge Zigbee, Z-Wave, and Wi-Fi devices, making it a neutral platform for legacy hardware. Samsung's B2B division also targets multi-family housing developers with pre-installed SmartThings wiring.

Platform Orchestrator (Amazon/Google)

Amazon leverages its massive installed base of Echo devices and Alexa skills to drive ecosystem lock-in. Google uses its AI search and machine learning strengths to offer proactive energy and security automation, integrating deeply with Nest hardware.

Hardware-Agnostic Hub Provider (Samsung SmartThings)

Samsung SmartThings takes a neutral stance, supporting Z-Wave, Zigbee, and Matter. Its competitive advantage is appliance integration – SmartThings can control Samsung washers, dryers, and refrigerators, offering a unique value for grocery and laundry automation.

Privacy-First Niche (Apple HomeKit)

Apple HomeKit targets premium buyers with mandatory hardware encryption and local processing. Its MFi certification ensures a curated ecosystem. Strategy: partner with high-end builders and security firms, not mass-market consumers.

5. Market Trends

1. AI HUB

The trend for 2026 is a dedicated AI box that consumers buy once and grant access to all devices. This hub runs local machine learning models to learn routines, manage energy, and even detect anomalies like water leaks. Amazon's Echo Hub (2024) and Google's next-generation Nest Hub are early examples. Why it matters: reduces cloud dependency, improves response times, and lowers monthly subscription costs for users. Samsung SmartThings is also expected to release a local AI hub by late 2026.

2. MATTER PROTOCOL STANDARDIZATION

Matter is the interoperability standard backed by Apple, Amazon, Google, and the Connectivity Standards Alliance. By 2026, over 90% of new smart home products are expected to be Matter-certified. Why it matters: eliminates the need for multiple apps and bridges, lowering the total cost of ownership for whole-home systems. A Matter-certified Yale smart lock can be controlled from a Google Nest Hub without any extra hardware.

3. BATTERY-POWERED SENSORS

The biggest barrier to whole-home adoption is wiring cost. New ultra-low-power sensors (e.g., Aqara FP2 presence sensor, Eve MotionBlinds) can run for two years on a coin cell battery using Thread protocol. Why it matters: enables retrofitting of existing homes without electricians, opening a massive upgrade market. The trend aligns with smart home market growth from USD 230 billion to USD 450 billion, as installation friction drops.

6. Regional Markets

North America – Matter Adoption Epicenter

Over 40% of U.S. homes have at least one smart device. The region drives Matter protocol adoption; 80% of certified devices are sold here. B2B buyers must ensure Matter 1.3 compatibility to access utility rebate programs (e.g., Nest thermostat rebates in California).

Europe – Energy Management Focus

EU energy directives and high utility prices push whole-home ecosystems toward load shifting and demand response. Products with interoperable heat pumps, EV chargers, and solar inverters are growing fastest. German market leader is Bosch's Smart Home system, integrating with PV systems.

Asia-Pacific – Mobile-First & Rapid Urbanization

China and South Korea lead in mobile-controlled ecosystems (Xiaomi, Samsung SmartThings). In Japan, panasonic's Home+ ecosystem includes earthquake shutoff sensors. The region's CAGR exceeds 20% due to new residential developments pre-wiring for whole-home systems.

7. Investment Outlook

Two concrete opportunities define the whole-home ecosystem horizon. First, the 'AI energy manager' opportunity: by 2027, utilities in the U.S. and Europe will offer dynamic pricing tariffs that reward homes capable of shifting load. An ecosystem that coordinates EV charging, HVAC, and water heating can save homeowners $300–$600 per year. B2B buyers should prioritize ecosystems with open APIs for grid-interactive capabilities. Second, the 'property developer standard' opportunity: large-scale residential builders in North America and Asia are beginning to pre-wire for whole-home ecosystems as a differentiator. Specifying Matter-certified devices from the start reduces post-construction retrofitting costs by up to 40%.

The principal risk remains fragmentation despite Matter. If major platforms (Amazon, Google, Apple) implement proprietary extensions that break universal compatibility, the whole-home dream unravels. B2B buyers should demand certification to the basic Matter profile and avoid platform-specific 'exclusive features' that lock them into one vendor. VerityRank recommends auditing supplier roadmaps for their commitment to Matter 1.3 (2026) and Thread border router support.

Strategic Considerations:

- AI Energy Manager Utility Partnerships: Partner with utility companies to offer ecosystem-controlled demand response; homeowners can save $300–600/year and B2B suppliers can generate recurring SaaS revenue.

- Pre-Wired New Construction Standards: Work with homebuilders to install Matter-certified hubs and Thread border routers during construction; reduces retrofit costs by 40% and creates long-term service contracts.

- Platform Proprietary Extensions Breaking Matter: If Amazon or Google add exclusive features that don't work with other Matter devices, buyers may face lock-in; demand written guarantees of basic Matter interoperability in supplier contracts.

- Cybersecurity Vulnerabilities in the Hub: A compromised central hub exposes all connected devices; require ISO 27001 certification and regular third-party penetration testing reports from hub suppliers.

Frequently Asked Questions

Make Informed Decisions in the Whole-Home Smart Ecosystem Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-06-10. All market figures are estimates and may vary from actual results.