-450x250h.webp)

-150x150h.webp)

The $759 Billion Furniture Boom: Why Dining Room Furniture Is the Hottest Category in 2026

Table of Contents

The global Dining Room Furniture industry serves consumers worldwide with diverse solutions.

1. Industry Overview

The global furniture market hit US$759.08 billion in 2025, ranking among the world's largest consumer goods sectors—and dining room furniture is stealing the spotlight. This category, encompassing dining tables, chairs, bar furniture, and storage pieces like sideboards and china cabinets, is experiencing a transformational surge driven by changing home dynamics and entertaining habits. The dining room has evolved from a formal space used occasionally to the functional heart of modern living, where families gather for meals, work, and connection.

Industry Scope & Characteristics

Broad Product Portfolio

Products span dining tables, dining chairs, bar tables, bar stools, sideboards, china cabinets, dining benches, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

Within this expansive market, the dining room furniture segment stands out with a projected compound annual growth rate of 10.6% from 2026 to 2033, outpacing many adjacent categories. This growth reflects a fundamental shift in how consumers prioritize their living spaces post-pandemic, with dedicated dining areas becoming essential rather than optional. The rise of remote work has blurred lines between kitchen, dining, and office, creating demand for versatile furniture that serves multiple functions without sacrificing aesthetic appeal.

The market's momentum is further fueled by premiumization trends, where consumers willing to invest in statement pieces for their dining spaces. Unlike other furniture categories where budget options dominate, dining room furniture sees strong performance in mid-to-high price brackets, particularly for extendable tables and custom configurations. Manufacturers are responding with innovative designs that maximize space efficiency while maintaining visual impact, positioning dining furniture as both practical and aspirational in the contemporary home.

Historic shifts in consumer behavior have permanently altered demand patterns. The average household now allocates more square footage and budget to dining areas, reflecting priorities around family connection and entertaining. This isn't a temporary trend—it's a structural change that industry analysts expect to sustain through the decade, making dining room furniture one of the most attractive segments for investors, retailers, and manufacturers alike.

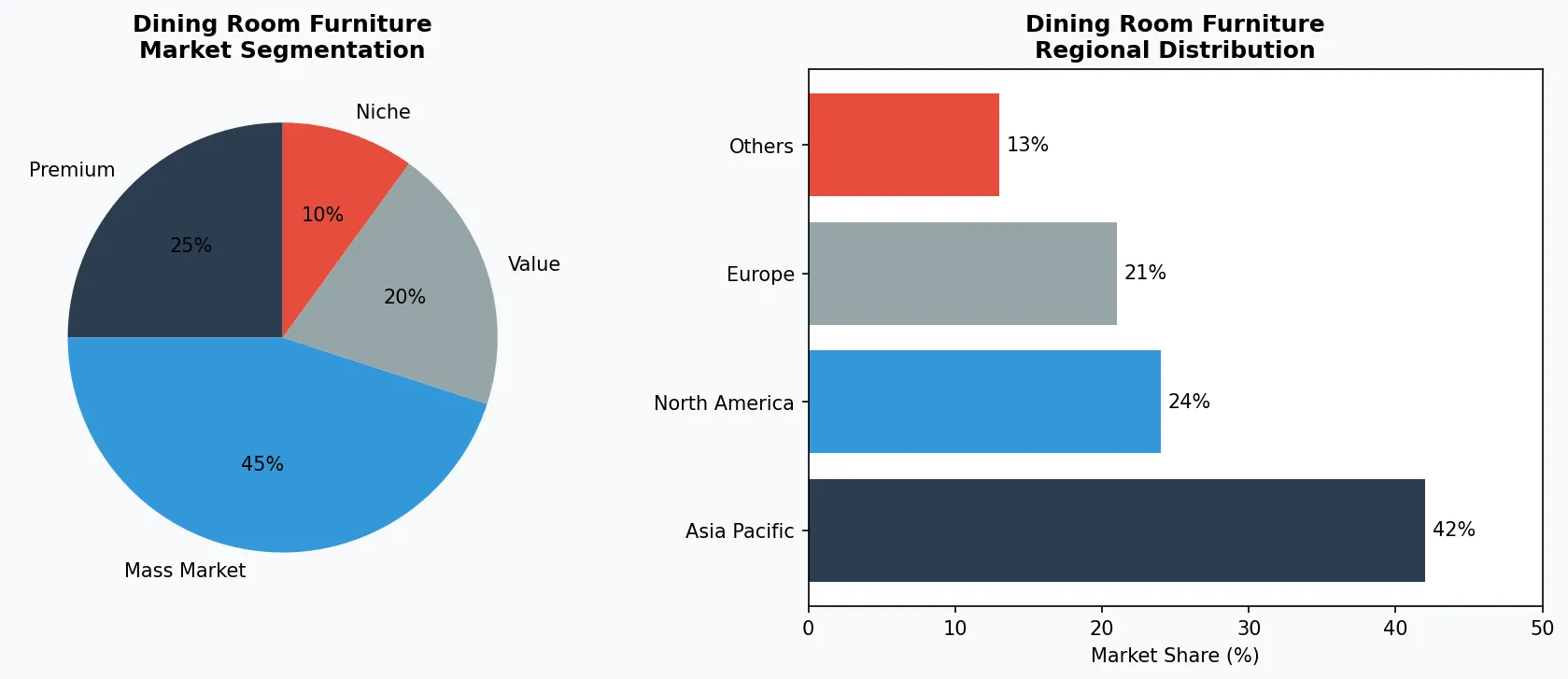

Key market segments and growth drivers in the Dining Room Furniture sector.

2. Market Analysis

The living and dining room furniture market achieved a valuation of USD 256.10 billion in 2026, with projections indicating growth to USD 314.43 billion by the end of the forecast period. This USD 58 billion expansion represents substantial opportunity across the supply chain, from raw material suppliers to retail outlets. The market's 4.19% CAGR reflects steady, sustainable growth rather than volatile boom-bust patterns, making it an attractive segment for long-term business planning and investment.

The dining table market alone illustrates the category's robust fundamentals. Valued at $9.19 billion in 2026, this specific segment is projected to reach $16.01 billion by 2034, representing a 7.19% CAGR. This faster growth rate compared to the broader furniture market indicates concentrated demand for dining tables specifically, driven by replacement cycles, new household formation, and interior design refreshes. The dining table, as the centerpiece of any dining room, serves as the anchor purchase that often dictates subsequent furniture selections.

Three primary drivers fuel this expansion: rising urbanization in developing economies, increasing disposable income in middle-class households globally, and the continued emphasis on home aesthetics following pandemic-era spending habits. The United States and China remain the two largest geographic markets by revenue, collectively accounting for over 35% of global demand. However, Southeast Asian markets including Vietnam, Thailand, and Indonesia are emerging as high-growth regions, driven by manufacturing cost advantages and expanding domestic consumer bases. Europe maintains steady demand, particularly in Scandinavian countries where dining culture remains central to household identity.

E-commerce channels now represent approximately 25% of all dining room furniture purchases, up from under 10% five years ago. This shift has fundamentally altered competitive dynamics, favoring manufacturers with strong direct-to-consumer capabilities and logistics networks. Traditional brick-and-mortar retailers are responding by investing in showroom experiences and augmented reality tools that help consumers visualize products in their homes before purchasing.

Market segmentation and regional distribution analysis for Dining Room Furniture.

3. Product Categories

Dining Tables represent the cornerstone category, with extendable designs commanding premium positioning. The extendable table segment grows fastest, reflecting space-constrained urban living where a 4-seat table that expands to seat 8 provides genuine utility. Materials range from solid hardwoods like oak and walnut to engineered wood with veneer finishes, with pricing spanning from under $200 for flat-pack options to over $5,000 for bespoke solid wood pieces. The market shows particular strength in round and oval configurations, which facilitate conversation and work better in awkwardly-shaped rooms.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Dining Chairs and Seating form the largest volume category by unit sales, with upholstered designs gaining share against traditional hard-seat styles. The trend toward mixed-material construction—combining wood or metal frames with fabric or leather cushions—reflects consumer demand for comfort without sacrificing durability. Bar stools have emerged as a distinct sub-category, driven by open-plan kitchen designs that integrate breakfast bars and raised counters into living spaces. Manufacturers like Man Wah have capitalized on this trend with modular seating systems that work across dining and bar applications.

Storage and Display pieces, including sideboards, china cabinets, and credenzas, have evolved from purely functional items to statement furniture that anchors room design. The category sees innovation in dual-purpose designs that combine media storage with dining essentials, reflecting converged living spaces where dining rooms often serve multiple functions. Contemporary designs favor clean lines, floating installations, and integrated lighting that creates visual drama. Material innovation is notable here, with tempered glass, metal mesh, and engineered stone increasingly featured alongside traditional wood.

Dining Benches represent a growing niche that appeals to space efficiency and casual dining aesthetics. Unlike chairs, benches can be tucked completely under tables when not in use, making them ideal for smaller living spaces. The category has expanded beyond traditional farmhouse styles to include upholstered versions, mid-century modern designs, and benches with integrated storage. Mix-and-match approaches, where homeowners pair benches with select chairs, have become a recognized design trend, allowing flexibility as household sizes change.

4. Leading Players

IKEA maintains its position as the global leader in affordable flat-pack dining furniture, with annual revenues exceeding $50 billion across all product categories. The Swedish giant's strategy centers on design innovation at accessible price points, supported by efficient supply chain management and the iconic flat-pack model that reduces shipping costs. Recent initiatives include the SÄLLSKAP collection, which features extendable dining tables and stackable chairs designed specifically for urban apartments. IKEA's sustainability commitments, including commitments to use only renewable or recycled materials by 2030, resonate strongly with European and North American consumers increasingly focused on environmental responsibility.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the dining room furniture space.

Ashley Furniture Industries operates as the largest domestic furniture manufacturer in the United States, with significant production capacity in Vietnam and other Asian markets. The company's competitive advantage lies in speed to market and extensive retail distribution, with Ashley products available through over 700 authorized retailers in North America. Their strategy focuses on trend-reactive design, rapidly translating emerging aesthetic movements into affordable mass-market products. The recently launched Bolanburg collection exemplifies this approach, offering farmhouse-style dining sets that captured the rustic-modern trend before competitors could respond.

Man Wah Holdings, based in Hong Kong with major manufacturing operations in China and Vietnam, has emerged as the global leader in reclining furniture and has aggressively expanded into dining categories. The company's vertical integration—from component manufacturing to finished goods—provides cost advantages that enable competitive pricing while maintaining quality standards. Man Wah's recent acquisition of dining-focused brands has broadened its product portfolio, positioning it to compete across price tiers from entry-level to premium. Strong relationships with major retailers including Walmart, Costco, and Ashley ensure widespread distribution.

Qumei, China's second-largest furniture exporter, has invested heavily in automation and smart manufacturing to compete on efficiency while moving upmarket. The company's strategy emphasizes European design aesthetics adapted for Chinese manufacturing cost structures, targeting consumers who want contemporary European styles at accessible prices. Qumei's recent partnerships with international design studios have elevated product development, while investments in North American showroom networks signal ambitions to compete directly with established Western brands in premium segments.

5. Market Trends

1. EXTENDABLE TABLE INNOVATION

EXTENDABLE TABLE INNOVATION — The shift toward space-efficient dining solutions drives demand for tables that seamlessly transform from intimate 4-seat configurations to expansive 8+ seat arrangements. Modern extension mechanisms now feature soft-close hydraulics and hidden leaf storage, eliminating the awkwardness of older designs. This trend matters because urban living spaces continue shrinking globally while entertaining expectations rise. IKEA's SMSTÖN extendable table exemplifies this category, featuring a patented leaf system that deploys in seconds. Manufacturers report 15-20% higher margins on extendable versus fixed tables, incentivizing continued innovation.

2. MIXED MATERIALS AESTHETIC

MIXED MATERIALS AESTHETIC — Contemporary dining furniture increasingly combines contrasting materials—wood paired with metal, glass with concrete, marble with leather—creating visual interest and durability advantages. This trend reflects broader design culture influences from industrial and biophilic design movements, where texture variety signals sophistication. Strong, the premium brand under Man Wah, has pioneered metal-and-wood combinations in their Confidante collection, achieving retail prices exceeding $3,000 per set. The trend matters because mixed-material construction commands price premiums of 25-40% over single-material equivalents, significantly impacting manufacturer margins.

3. EASY-MAINTENANCE MATERIALS

EASY-MAINTENANCE MATERIALS — Consumer demand for furniture that maintains its appearance with minimal effort drives innovation in fabrics, finishes, and surface treatments. Performance fabrics originally developed for outdoor furniture now appear on indoor dining chairs, offering stain resistance and easy cleaning that appeals to families with children. Nano-ceramic table finishes provide heat and scratch resistance previously requiring specialized care. This trend matters because total cost of ownership—including cleaning products, professional services, and replacement frequency—increasingly influences purchase decisions. Lamefor has positioned its entire dining collection around "lifestyle-friendly" materials, targeting busy professional households.

4. SUSTAINABLE SOURCING DEMAND

SUSTAINABLE SOURCING DEMAND — Environmental responsibility has shifted from niche concern to mainstream expectation, with consumers actively seeking furniture made from certified sustainable materials and ethical manufacturing processes. FSC-certified wood, recycled aluminum, and water-based finishes have become standard features in mid-market offerings. This trend matters because sustainability claims now influence purchase decisions for over 60% of millennial and Gen Z consumers, according to industry surveys. Ashley Furniture's partnership with the Sustainable Furniture Council and commitment to deforestation-free supply chains represents a strategic response to this demand.

6. Regional Markets

North America remains the most lucrative market for premium dining room furniture, with the United States accounting for approximately 85% of regional sales. American consumers demonstrate strong preferences for larger dining sets accommodating 6-8 guests, reflecting cultural traditions around family gatherings and holiday entertaining. The market shows particular strength in the South and Midwest, where larger homes and traditional floor plans support dedicated dining rooms. However, coastal metropolitan areas drive demand for space-efficient designs, with extendable tables and bench seating representing disproportionate growth versus fixed-table configurations.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

China represents the world's largest furniture market by volume, though the dining room furniture segment shows distinct characteristics from Western markets. Chinese consumers favor solid wood construction and traditional design elements, with dining tables often positioned as heirloom investments rather than transitional purchases. The market exhibits strong regional variation, with coastal affluent consumers showing preference for contemporary European aesthetics while interior provinces maintain demand for classical Chinese styles. Domestic brands including Qumei and Lamefor dominate, though IKEA has achieved significant market penetration with its affordable flat-pack approach, reporting over 30 million annual visitors to Chinese stores.

Western Europe demonstrates mature market dynamics with steady single-digit growth, driven primarily by replacement cycles and design refreshes rather than new household formation. Scandinavian countries lead in per-capita dining furniture spending, reflecting cultural emphasis on quality investments and well-designed living spaces. Germany and France show strong demand for technically sophisticated products, with features like integrated charging stations and adjustable height mechanisms commanding premium pricing. The United Kingdom presents a notably different profile, with compact urban housing driving demand for multi-functional dining furniture that serves as workspace during daytime hours.

7. Investment Outlook

Two opportunities stand out for stakeholders navigating the dining room furniture market through 2026 and beyond. First, the smart furniture category—furniture with integrated technology features like wireless charging surfaces, embedded speakers, and app-controlled LED lighting—represents an underserved premium segment growing at approximately 25% annually. Manufacturers who successfully integrate technology without compromising aesthetics can command price premiums exceeding 50% while attracting design-conscious early adopters. Second, the contract furniture market—products designed for commercial settings like hotels, restaurants, and corporate cafeterias—offers diversification opportunities as hospitality sector recovery accelerates, with global hotel construction pipelines indicating strong demand through 2027.

The primary risk demanding attention is raw material volatility, particularly for hardwoods and aluminum. Furniture manufacturers operate on thin margins typically ranging 8-15%, leaving limited buffer against input cost increases. Chinese manufacturing costs have risen 20-30% over the past three years due to labor inflation and environmental compliance requirements, and further increases appear likely as regulatory pressures intensify. Companies that have not secured long-term supplier agreements or diversified manufacturing geographies face margin compression or forced price increases that could alienate value-conscious consumers. Strategic hedging through vertical integration, diversified supplier networks across Vietnam, India, and Eastern Europe, and materials innovation (including engineered wood alternatives matching solid wood aesthetics) will separate successful players from those struggling to maintain profitability in the years ahead.

Strategic Considerations:

- ('Technology & AI Integration:', 'Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.')

- ('Sustainability as Business Strategy:', 'Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.')

- ('Transparency & Traceability:', 'Consumers demand increasingly granular information about product origins, ingredients, and production methods.')

- ('Emerging Market Penetration:', 'Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.')

Make Informed Decisions in the Dining Room Furniture Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-15. All market figures are estimates and may vary from actual results.