-450x250h.webp)

-150x150h.webp)

Robot Vacuums and AI Sensors: How the $50 Billion Home Cleaning Appliances Market Is Being Redefined in 2026

Table of Contents

The global Home Cleaning Appliances industry serves consumers worldwide with diverse solutions.

1. Industry Overview

The global home cleaning appliances market, valued in the tens of billions, is undergoing its most dramatic transformation since the introduction of the electric vacuum cleaner a century ago. Between 2026 and 2033, industry analysts project compound annual growth rates that will reshape how 4.7 billion households worldwide manage domestic hygiene. This is not incremental improvement—this is a fundamental rethinking of what cleaning equipment can do.

Industry Scope & Characteristics

Broad Product Portfolio

Products span vacuum cleaners, robot vacuums, floor scrubbers, steam mops, air purifiers, humidifiers, dehumidifiers, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

The convergence of artificial intelligence, advanced sensor technology, and consumer demand for hands-free home care has created a perfect storm. Robot vacuum cleaners, once relegated to novelty status, now represent the fastest-growing segment, with units equipped with LiDAR navigation and real-time mapping becoming standard rather than premium. Meanwhile, air purifiers and humidifiers have moved from specialty health products to mainstream household fixtures, driven by rising urban pollution concerns and post-pandemic respiratory awareness.

What makes this market distinctive is its position at the intersection of convenience technology and health consciousness. Unlike other appliance categories focused on entertainment or kitchen efficiency, home cleaning appliances directly impact indoor air quality, allergy management, and bacterial exposure. This health dimension has attracted serious investment from major technology players and elevated consumer willingness to pay premium prices for demonstrable performance improvements.

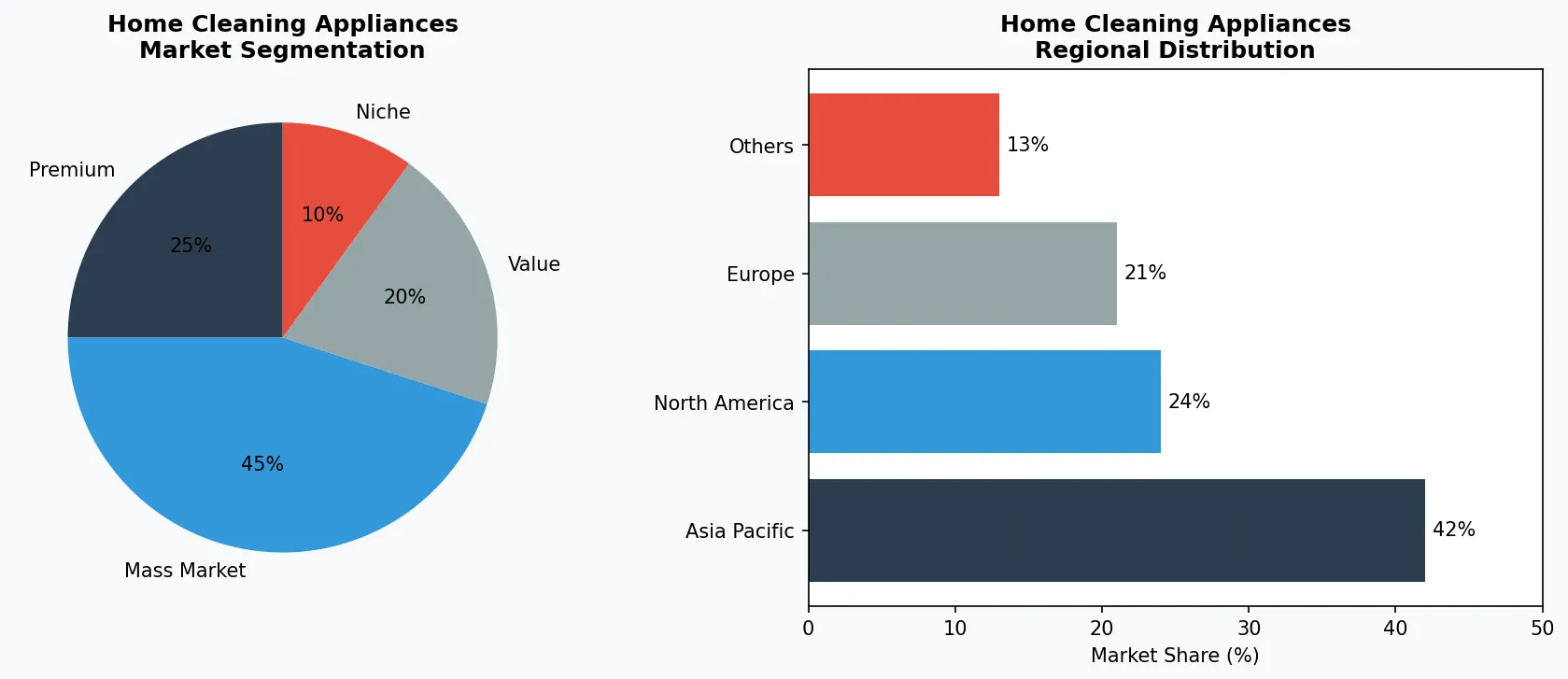

Key market segments and growth drivers in the Home Cleaning Appliances sector.

2. Market Analysis

The global cleaning appliances market demonstrates robust expansion from 2025 through 2033, with the dishwashing products segment alone projected to grow by $11 billion, toilet cleaners by $3 billion, and surface cleaners contributing additional significant value. These figures reflect fundamental shifts in household time allocation and hygiene standards across developed and developing economies alike.

Three primary growth drivers underpin this expansion. First, dual-income households now constitute the majority of families in North America and Western Europe, creating sustained demand for time-saving automated cleaning solutions. Second, the Asia-Pacific region, led by China, Japan, and South Korea, has emerged as both the largest producer and fastest-growing consumer of smart cleaning appliances, with urban apartment living driving adoption of space-efficient robot vacuums. Third, health and wellness prioritization post-2020 has elevated cleaning appliances from convenience items to health infrastructure, particularly for households with children, elderly residents, or allergy sufferers.

Geographic market leadership is shifting. While North America maintains the highest per-capita spending on premium cleaning appliances, the Middle East and Southeast Asia are emerging as high-growth frontier markets where improving consumer credit access and new residential construction are accelerating adoption rates. Europe remains a strong performer, though regulatory requirements around energy efficiency and materials sourcing are reshaping product development priorities across the continent.

Market segmentation and regional distribution analysis for Home Cleaning Appliances.

3. Product Categories

Robot Vacuum Cleaners represent the crown jewel of the category, with brands like iRobot's Roomba series, Roborock's S-series, and Ecovacs' Deebot line competing for dominance. Modern units feature AI-powered obstacle recognition, multi-floor mapping memory, and self-emptying docking stations that require intervention only monthly. These devices have transitioned from random-bounce navigation to precision cleaning paths that rival traditional canister vacuums in pickup performance.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Floor Scrubbers and Steam Mops address the growing consumer preference for chemical-free cleaning. Brands like Bissell and Shark have developed hybrid steam-and-vacuum systems that kill 99.9% of bacteria without sanitizing chemicals, appealing to families seeking to reduce synthetic cleaning agents around children and pets. The commercial-grade performance now available in consumer-priced units has blurred the line between professional janitorial equipment and home appliances.

Air Purification Systems have evolved beyond simple HEPA filtration to include UV-C sterilization, ion generation, and smart air quality monitoring. Dyson and Xiaomi have introduced units that display real-time particulate counts and automatically adjust filtration intensity based on detected pollution levels. These connected devices integrate with home automation ecosystems, representing a new category of health-monitoring appliances.

Climate Control Appliances, including humidifiers and dehumidifiers from brands like Philips and Electrolux, have gained prominence as consumers recognize the health impacts of indoor humidity levels. Smart models now feature automatic humidity targeting, filter replacement reminders, and compatibility with voice assistants, moving these devices from standalone appliances into integrated home climate management systems.

4. Leading Players

Dyson maintains its position as the premium innovator, with the company's latest vacuum technology achieving 25% greater airflow efficiency than competitors through proprietary cyclone engineering. The British manufacturer's strategy centers on continuous patent development and premium pricing, targeting affluent consumers who view cleaning appliances as lifestyle investments rather than commodity purchases. Dyson's expansion into air purification and humidification reflects a deliberate diversification toward complete indoor air quality management.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the home cleaning appliances space.

iRobot, the pioneer of consumer robot vacuums, faces intensifying competition but retains advantages in software sophistication and brand recognition. The company's recent investment in AI-powered visual recognition allows its latest Roombas to distinguish between pet waste and toys, addressing a historical pain point that caused significant user frustration. iRobot's strategic focus has shifted toward ecosystem integration, with compatible mopping attachments and outdoor cleaning robots in development.

Chinese manufacturers Roborock and Ecovacs have disrupted premium pricing through aggressive engineering investment at lower cost structures. Roborock's partnership with Xiaomi provides supply chain advantages and access to smart home integration platforms, while Ecovacs has invested heavily in European market expansion with localized customer service operations. Both companies are outspending traditional manufacturers on sensor technology and mapping algorithm development, threatening to commoditize features that once distinguished premium brands.

Xiaomi's Mi Home ecosystem approach positions the company to capture consumers entering smart home technology, bundling robot vacuums with security cameras, smart speakers, and air quality monitors through a unified app. This ecosystem lock-in strategy reduces customer acquisition costs while increasing lifetime value, a model that pressures competitors to develop comparable integration capabilities or accept margin compression.

5. Market Trends

1. AUTONOMOUS CLEANING STATIONS

AUTONOMOUS CLEANING STATIONS — Self-emptying robot vacuums are being superseded by comprehensive cleaning stations that wash, dry, and refill mopping pads automatically. iRobot's latest docking systems handle weeks of maintenance autonomously, eliminating the primary user friction point that prevented earlier adoption. This matters because household automation success correlates directly with intervention frequency—the less users must touch their devices, the higher satisfaction and repurchase rates become.

2. BIO-BASED CLEANING SOLUTIONS

BIO-BASED CLEANING SOLUTIONS — The shift toward probiotic and enzyme-based cleaning formulas represents a fundamental departure from chemical disinfection. Rather than killing all bacteria indiscriminately, bio-based cleaners establish healthy microbial ecosystems on surfaces that naturally outcompete pathogens. This trend matters because regulatory pressure on chemical cleaning agents is increasing globally, and consumer preference research shows growing resistance to synthetic fragrances and bleach-based products, particularly in households with young children.

3. SMART SENSING TECHNOLOGY

SMART SENSING TECHNOLOGY — Next-generation sensors can now detect specific contaminant types—pet dander, dust mite allergens, mold spores—and adjust cleaning patterns accordingly. Roborock's latest models use computer vision to identify high-traffic zones and concentrate cleaning effort where buildup occurs most rapidly. This trend matters because it transforms cleaning appliances from reactive tools into proactive maintenance systems, potentially reducing cleaning frequency while improving outcomes.

4. MULTI-FUNCTION CONVERGENCE

MULTI-FUNCTION CONVERGENCE — Appliances that combine vacuuming, mopping, and sanitizing in single passes are replacing single-function devices for floor care. Electrolux and Philips have introduced hybrid systems that simultaneously vacuum dry debris and apply damp sanitization, cutting total cleaning time by 40% compared to sequential single-function use. This convergence matters because consumer research consistently identifies total cleaning duration as the primary barrier to more frequent household maintenance.

6. Regional Markets

North America remains the highest-value market for premium cleaning appliances, with U.S. households spending an average of $340 annually on cleaning equipment and consumables. The region's growth is driven by existing smart home infrastructure penetration—over 65% of American homes now have WiFi-connected devices, creating the foundation for IoT cleaning appliance adoption. Premium segment preferences mean American consumers demonstrate willingness to pay 30-40% price premiums for demonstrated performance improvements, supporting continued innovation investment.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

Asia-Pacific dominates volume growth, with China alone accounting for over 40% of global robot vacuum unit sales. Chinese manufacturers like Roborock and Ecovacs have driven adoption through aggressive pricing that has brought entry-level robot vacuums below $200, expanding the addressable market to value-conscious consumers. The Asia-Pacific market is also distinguished by higher adoption of air purification appliances, driven by documented air quality concerns in major urban centers from Beijing to Mumbai.

Europe presents a distinct profile where energy efficiency regulations and sustainability mandates are reshaping product development. The European Union's Ecodesign regulations are eliminating the least efficient appliance categories and requiring repairability standards that favor established brands with service networks. Germany and Scandinavia lead premium sustainable appliance adoption, while Southern European markets demonstrate strong growth in value segments. This regulatory environment creates both compliance costs and competitive insulation for manufacturers positioned to meet stringent environmental standards.

7. Investment Outlook

Two concrete opportunities stand out for market participants. First, the integration of cleaning appliances with predictive maintenance systems represents significant untapped value—devices that schedule service appointments, order replacement filters automatically, and report efficiency degradation before failures occur will command premium positioning. Second, emerging market expansion into Latin America and Africa offers volume growth at a scale unavailable in saturated North American and European markets, particularly for portable, battery-powered appliances suited to inconsistent power infrastructure.

The primary risk is regulatory fragmentation as governments impose divergent standards on chemical contents, energy consumption, and electronic waste. Manufacturers serving global markets face mounting compliance costs as the EU, United States, and China each pursue distinct regulatory agendas that may require separate product development tracks. Companies that fail to establish regulatory affairs capabilities comparable to their engineering investments risk market access restrictions at precisely the moment consumer demand reaches peak intensity. The window for establishing dominant positions in key markets narrows as these regulatory timelines converge toward 2027-2028 enforcement dates.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Home Cleaning Appliances Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-16. All market figures are estimates and may vary from actual results.