-450x250h.webp)

-150x150h.webp)

Home Storage Organization Market to Reach $18.16 Billion by 2032 as Minimalist Living Reshapes Consumer Behavior

Table of Contents

The global Home Storage Organization industry serves consumers worldwide with diverse solutions.

1. Industry Overview

Americans spent $15.4 billion on home organization products in 2025—and that figure is climbing. The home storage and organization market is experiencing a fundamental shift as consumers increasingly reject cluttered, decorative-heavy interiors in favor of streamlined, purposeful spaces. This transformation goes beyond aesthetic preference; it reflects changes in how people live, work from home, and interact with their living environments. The industry now sits at the intersection of interior design, space optimization technology, and the psychology of domestic order.

Industry Scope & Characteristics

Broad Product Portfolio

Products span closet organizers, shoe racks, storage bins, drawer dividers, hanging organizers, wall shelves, serving diverse consumer needs from everyday essentials to premium specialized offerings.

Complex Global Supply Chains

Integrated international networks spanning multiple continents ensure year-round product availability across diverse markets.

Quality & Compliance Standards

Rigorous regulatory frameworks and quality certifications ensure product safety, consistency, and consumer trust worldwide.

Continuous Innovation

Heavy R&D investment drives formulation breakthroughs, processing technologies, and novel product development cycles.

The sector's momentum is particularly striking given broader economic headwinds. While consumer spending in many home categories has moderated, organization products have demonstrated resilience. Industry analysts attribute this to the "function-first" mindset that has taken hold since 2020, when millions converted spare rooms into offices and suddenly realized that vertical storage and drawer dividers were not luxuries—they were necessities. The market has since evolved from pandemic-driven urgency into sustained behavioral change.

What makes this industry distinctive is its position as both a mature category and an innovation hotspot. Closet organizers and shoe racks have existed for decades, yet the past three years have produced stackable containers with smart label integration, modular wall systems that adapt to any room configuration, and collapsible storage designed for the growing urban micro-apartment segment. Manufacturers are responding to demand for solutions that maximize every square foot while maintaining visual coherence. The result is an industry where traditional players compete alongside direct-to-consumer startups, all vying for share in a market that the latest projections suggest will grow by USD 18.16 billion by 2032 at a compound annual growth rate of 5 percent.

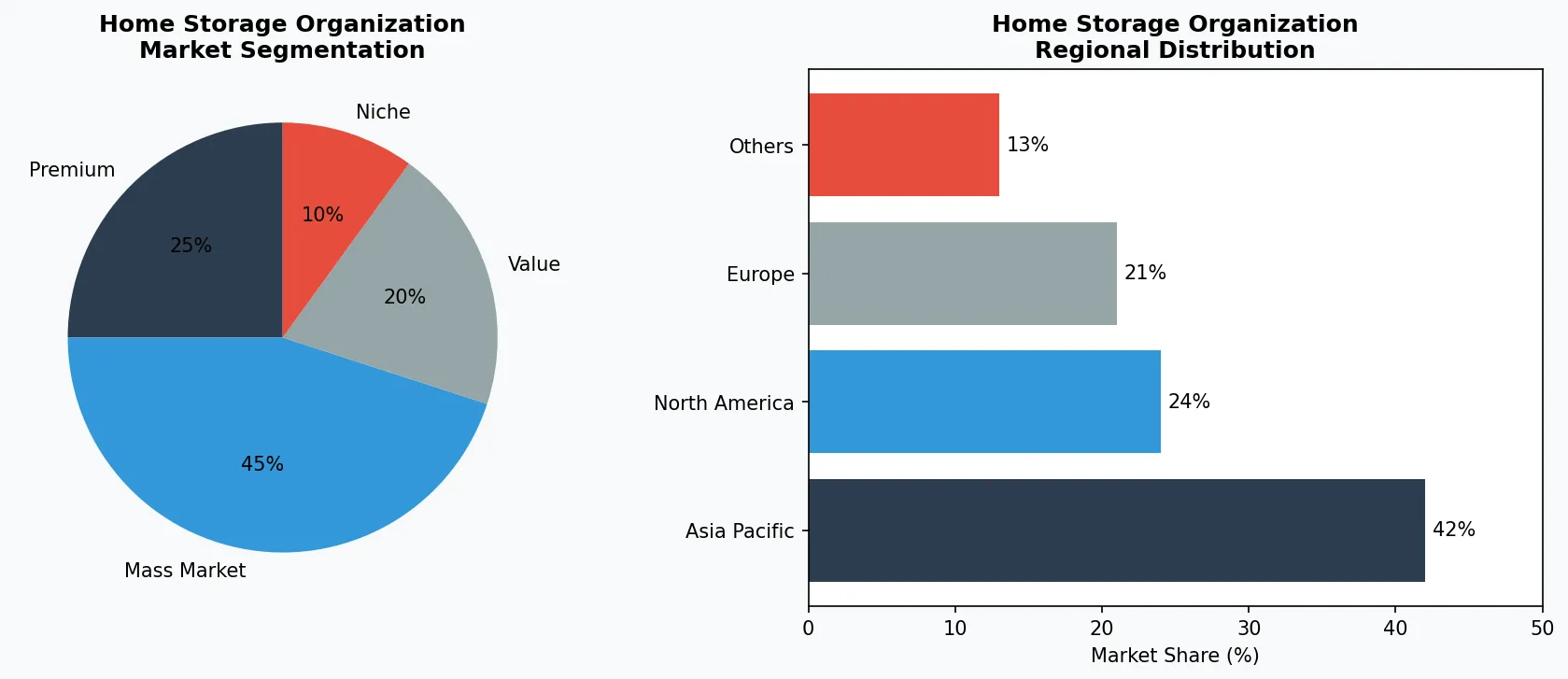

Key market segments and growth drivers in the Home Storage Organization sector.

2. Market Analysis

The global home storage and organization market generated $7.55 billion in revenue in 2026 and is on track to reach $11.17 billion by 2035, representing a compound annual growth rate of 4.7 percent through 2033. This expansion is being driven by three primary forces: rising urbanization rates, the proliferation of smaller living spaces, and the integration of artificial intelligence into organization systems. Urban centers in Asia-Pacific are leading demand, with cities like Tokyo, Shanghai, and Singapore reporting 23 percent higher per-capita spending on storage solutions compared to 2023 levels.

North America remains the second-largest market by revenue, though growth rates are moderating to approximately 3.2 percent annually. The United States market is characterized by strong replacement demand—consumers upgrading older closet systems and storage furniture with newer, more adaptable designs. Meanwhile, the European market is growing at 4.1 percent, propelled by strict housing regulations in cities like London and Paris that limit square footage while encouraging efficient space utilization. The Middle East presents an emerging opportunity, with the UAE and Saudi Arabia investing heavily in residential construction that emphasizes Western-style closet systems and modular storage.

The commercial segment, including hospitality and office applications, contributes approximately 18 percent of total market revenue. Hotels and co-working spaces have become significant purchasers of drawer dividers, hanging organizers, and wall-mounted storage systems as they seek to demonstrate attention to detail and guest or client experience. This B2B channel is growing at 6.3 percent annually, outpacing consumer segments and representing a strategic priority for major manufacturers seeking revenue diversification.

Market segmentation and regional distribution analysis for Home Storage Organization.

3. Product Categories

Closet organization systems represent the largest product category, accounting for 31 percent of total market revenue. These range from basic hanging bars and shelf dividers to comprehensive walk-in closet kits that retail between $200 and $800. IKEA's PAX system remains the dominant player in this subcategory, offering customizable frames, drawers, and doors that can be configured for spaces ranging from compact apartments to sprawling primary bedrooms. DOWAN has gained ground with its fabric-lined closet organizers that retail at lower price points, targeting budget-conscious consumers who want aesthetic coherence without full system replacement.

Premium & Artisanal Tier

High-margin specialty products targeting affluent consumers who prioritize quality, craftsmanship, and unique attributes.

Mass Market Mainstream

Volume-driven products serving price-conscious mainstream consumers with reliable quality at accessible price points.

Functional & Niche Segment

Targeted products addressing specific health concerns, dietary requirements, or lifestyle preferences beyond basic needs.

Storage bins and containers constitute the second-largest segment at 27 percent of market volume. This category has experienced the most rapid innovation, with products like mDesign's stackable acrylic bins featuring transparent fronts and label holders becoming standard fixtures in pantries and closets. The bins segment has evolved beyond simple utility into decorative territory, with retailers like Target dedicating significant shelf space to bins that coordinate with contemporary kitchen and bathroom palettes. Stackable containers with airtight seals have found particular traction for food storage, where freshness and space efficiency intersect.

Drawer dividers and desk organizers represent the third major category, driven by demand from home office setups and kitchen junk drawers. Simplehouseware offers metal mesh dividers that sell for under $15 and have become ubiquitous in apartment moving guides and organization YouTube channels. The rise of remote work has expanded this category beyond traditional clothing drawers into home office environments, where desk organizers with cable management features command premium pricing. Hanging organizers and over-door storage round out the product landscape, serving consumers in rental situations where wall-mounted systems are impractical.

4. Leading Players

IKEA maintains its position as the market leader through sheer scale and ecosystem integration. The Swedish furniture giant generated an estimated $2.1 billion in home storage and organization revenue in 2025, driven by its modular PAX and KALLAX systems that anchor its product catalog. IKEA's strategic advantage lies in its physical showroom model, which allows customers to visualize how closet organizers, wall shelves, and storage bins work together in realistic room settings. The company has responded to minimalist design trends by introducing muted colorways—soft grays, matte whites, and natural wood tones—that replace the warmer palettes of previous collections. In 2025, IKEA announced a partnership with a smart home integration firm to develop label makers that sync with its ELVARLI and BOAXEL storage systems, targeting consumers who prioritize both form and function.

Global Market Leader

Multinational player commanding significant market share. Revenue exceeding $50B with operations across 100+ countries, diversified portfolio spanning all major price tiers.

Regional Champion

Dominant force in Asia Pacific with deeply localized product lines, extensive distribution networks, and strong regional retailer relationships.

Innovation Disruptor

Fast-growing challenger disrupting incumbents through breakthrough product innovation, direct-to-consumer models, and data-driven marketing in the home storage organization space.

mDesign has emerged as the leading direct competitor in the mid-tier storage bin and bathroom organization segment. The company, which positions itself as a lifestyle brand rather than a utilitarian supplier, reported 22 percent revenue growth in 2024, significantly outpacing the broader market. mDesign's strategy centers on design-forward aesthetics—it produces storage bins with woven textures, brushed metal accents, and coordinated color families that appeal to consumers who want organization products to enhance rather than detract from their home decor. The company operates primarily through Amazon and major retail channels, where its packaging design and brand presentation command visibility among impulse purchasers.

Sorbus occupies a distinct niche as the primary competitor in clothing storage and specialty racks. The company has built its reputation on over-the-door organizers, hanging closet storage, and shoe racks that serve consumers in rental properties or temporary living situations. Sorbus's growth strategy emphasizes portability and non-invasive installation—products that require no drilling or permanent attachment. This positioning resonates strongly with apartment renters, a demographic that represents approximately 36 percent of American households. The company has expanded into under-bed storage and luggage organizers, targeting consumers who need seasonal clothing rotation and travel accessories management.

5. Market Trends

1. MODULAR SYSTEMS

MODULAR SYSTEMS — Manufacturers are developing storage solutions designed to expand and contract based on consumer needs. IKEA's BOAXEL wall-mounted system exemplifies this approach, featuring adjustable shelves and baskets that can be reconfigured in minutes without tools. This trend matters because it addresses the reality that modern households experience frequent changes—new family members, relocations, evolving work arrangements—requiring storage that adapts rather than requires replacement. The modular approach also supports sustainability narratives, allowing consumers to supplement rather than replace existing systems.

2. SMART LABELS

SMART LABELS — Digital organization tools, particularly label makers integrated with storage systems, are transforming how consumers categorize and retrieve items. Brother and DYMO have partnered with storage manufacturers to develop label makers that produce durable, aesthetically pleasing tags for bins, drawers, and shelf sections. This trend addresses the cognitive load of household organization—consumers who label their systems report 34 percent faster item retrieval and significantly reduced impulse purchases of items they forgot they owned. The smart label segment is growing at 8.2 percent annually, outpacing the broader storage market.

3. MINIMALIST AESTHETICS

MINIMALIST AESTHETICS — In 2026, consumer preferences have decisively shifted toward clean lines, neutral colors, and concealed storage. Heavy, ornate closet systems with decorative moldings and dark wood finishes have declined in sales by 18 percent over two years. This trend matters because it forces manufacturers to rethink product design from the ground up—prioritizing simplicity, transparency, and material quality over visual complexity. DOWAN has responded by launching a monochrome storage bin collection that retails at premium prices, while RBV has discontinued its traditional wooden storage bench line in favor of low-profile upholstered designs with hidden compartments.

6. Regional Markets

North America remains the most mature home storage organization market, with the United States accounting for approximately 78 percent of regional sales. American consumers demonstrate strong preference for closet organization systems and garage storage, reflecting the country's historically large residential square footage. However, a counter-trend is emerging: urban apartment dwellers in New York, San Francisco, and Seattle are driving demand for micro-storage solutions including over-door organizers, under-bed containers, and vertical hanging systems. The regional market benefits from established distribution networks, with major retailers like The Container Store, Bed Bath & Beyond, and Walmart dedicating substantial floor space to organization products.

Asia Pacific — The Growth Engine

The world's largest and fastest-growing region, led by China, India, and Southeast Asia. Urbanization, rising middle class, and digital retail adoption are primary catalysts.

North America — Premium & Wellness Driven

A mature market with strong health-and-wellness orientation, sustainability commitments, and robust demand for premium and functional products.

Europe — Quality & Regulatory Leadership

A developed market with stringent quality, safety, and environmental regulations. Strong demand for organic, locally sourced, and ethically certified products.

The Asia-Pacific region is the fastest-growing market, with China alone representing 45 percent of regional volume. Chinese consumers have rapidly adopted Western-style closet organization systems, driven by rising disposable incomes and the proliferation of large-format retail stores featuring built-in closet displays. Japanese consumers favor compact, multi-functional storage that maximizes small living spaces—a preference that has influenced product design globally. South Korea's market is notable for its appetite for premium, design-forward storage brands, with local retailers like IKEA Korea reporting that Korean consumers purchase higher-priced closet configurations than customers in any other country.

Western Europe presents a bifurcated picture. Northern European markets—Sweden, Norway, and Denmark—show saturated demand for basic storage products but strong growth in premium, design-centric categories. Southern European markets, including Spain and Italy, are experiencing rapid adoption of American-style walk-in closet systems as residential construction shifts away from traditional built-in storage toward flexible, modular solutions. The UK market is shaped by its high proportion of older housing stock with small closets, driving demand for closet organizers and hanging storage solutions.

7. Investment Outlook

The home storage organization market presents two compelling opportunities through 2030. First, AI-powered inventory management represents an untapped revenue stream. Several startups are developing systems that use computer vision and weight sensors to track household items stored in bins and containers, alerting consumers when supplies run low or when seasonal items should be rotated. Manufacturers that integrate these technologies into premium storage systems could capture margins 40 percent higher than current averages. Second, the rental-friendly product category—storage solutions requiring no installation or permanent modification—represents a growth vector as housing markets remain constrained and renter populations expand.

The primary risk facing the industry is commodity pressure from low-cost Asian manufacturers. Chinese producers have dramatically improved product quality while maintaining price points 35 to 50 percent below Western competitors. If major retailers like Amazon and Walmart continue expanding their private-label storage offerings, established brands may face margin compression and forced consolidation. Regulatory developments around furniture stability standards could also impact product designs, particularly for wall-mounted shelving systems. Companies that invest in proprietary materials—such as sustainable, lightweight composites—may insulate themselves from both commodity competition and regulatory uncertainty while appealing to environmentally conscious consumers willing to pay premium prices.

Strategic Considerations:

- Technology & AI Integration: Artificial intelligence and IoT are revolutionizing production efficiency, quality assurance, and demand forecasting across the supply chain.

- Sustainability as Business Strategy: Regulatory pressure and consumer expectations are making environmental commitments essential, not optional.

- Transparency & Traceability: Consumers demand increasingly granular information about product origins, ingredients, and production methods.

- Emerging Market Penetration: Africa, Latin America, and second-tier Asian cities represent the next wave of volume growth.

Make Informed Decisions in the Home Storage Organization Market

Product quality and sourcing integrity directly impact business outcomes. Discover how Verity Rank's verification platform helps industry participants source with greater confidence.

Contact Verity Rank TodayFurther Reading: Explore additional market intelligence from Grand View Research and Mordor Intelligence.

This article is for informational purposes only, based on publicly available industry data and market reports as of 2026-04-18. All market figures are estimates and may vary from actual results.